Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

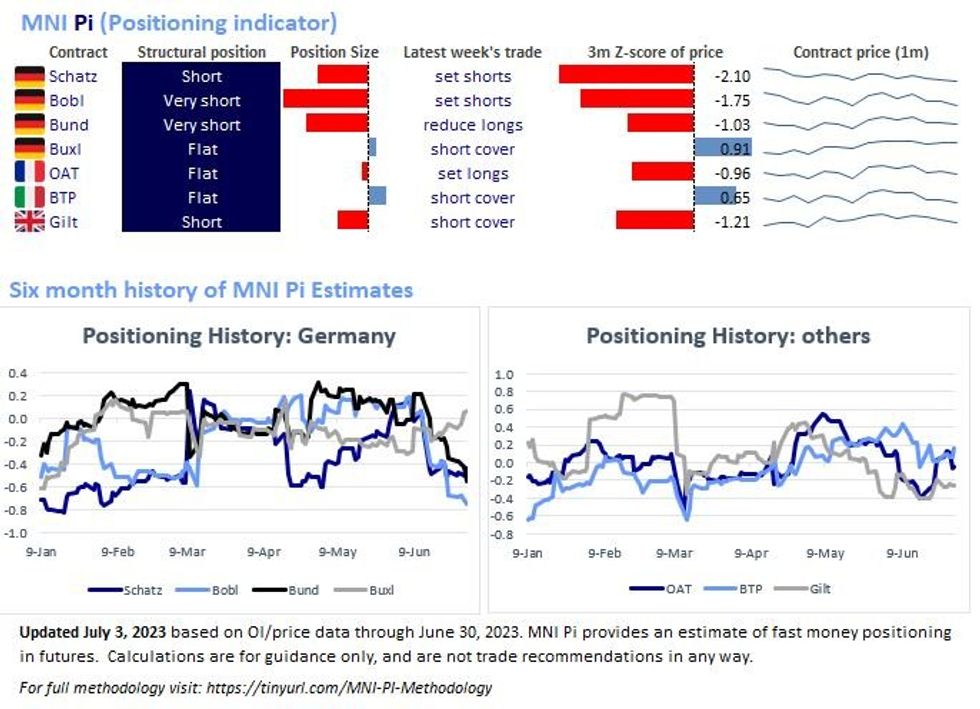

MNI Europe Pi (Positioning Indicator): More Decisive Shorts

MNI Europe Pi (Positioning Indicator): More Decisive Shorts

EXECUTIVE SUMMARY:

- Structural positioning has moved more decisively "short" since our last update on Jun 19, by when we had already seen some short leanings following the quarterly Eurex futures roll.

- The most notable divergence has been in Buxl remaining resolutely flat vs the rest of the German curve at short/very short.

- Trade last week was mixed, mostly between setting and covering shorts.

Full PDF Analysis:

- GERMANY: Schatz remains short, same as our last update, but Bobl has moved to "very short" from merely short prior (shorts were set last week for both contracts). Bund meanwhile has shifted from flat to "very short", with longs reduced last week. Buxl remains flat (short cover was seen last week).

- OATs have edged out of structurally short territory, where it spent a brief period earlier in June after flipping from long, and now sit flat. Some long-setting was seen last week.

- Gilts remain in the short territory it found itself in our last update vs flat for most of the weeks leading up to the late-May contract roll. There was some short cover last week.

- BTP structural positioning remains flat, where it has spent most of the past 2 months (after a stint in "long" territory in May). The contract saw some short covering last week.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok