Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

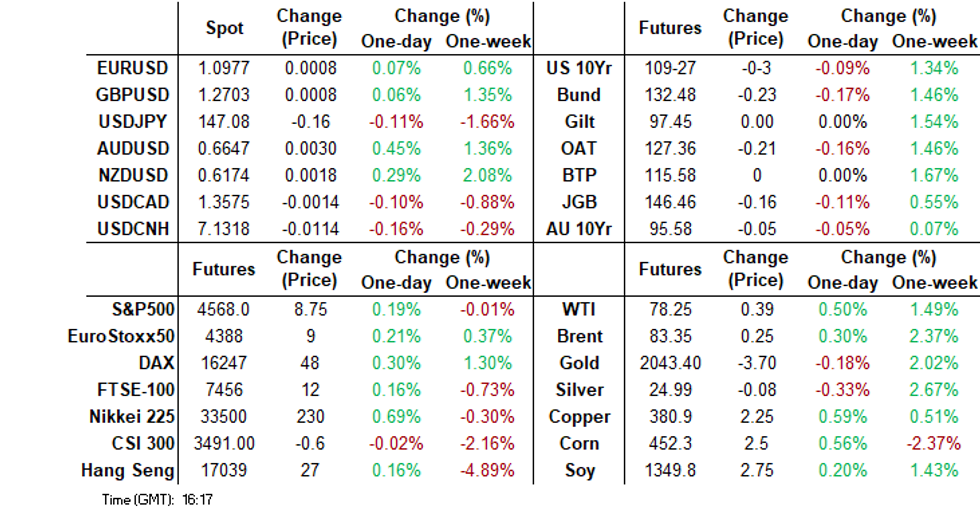

- Cash US tsys are dealing flat to 2bps cheaper in the Asia-Pac session, with a slight steepening bias apparent. The weaker-than expected Official China PMI failing to move the market in a positive direction despite a softening across most-sub-indices.

- USD upticks against the majors have been sold, although pairs are respecting recent ranges. USD/Asia pairs are modestly higher into month end (ex USD/CNH). China and Hong Kong equities have struggled for positive traction, with aggregate indices tracking lower for the fourth straight month.

- JGB futures have reversed course during the Tokyo afternoon session, the catalyst for afternoon weakness appears to have been weak demand metrics at today’s 2-year JGB auction. Elsewhere, oil prices are creeping higher ahead of the upcoming OPEC meeting.

- Looking ahead, ECB President Lagarde speaks and euro area preliminary CPI data are released. Later the Fed’s Williams speaks on innovations in central banking and there are US jobless claims, October income/spending & deflators, and MNI November Chicago PMI.

MARKETS

US TSYS: Yesterday’s Strong Rally Slightly Pared Ahead Of Monthly PCE Data

TYH4 is currently trading at 110-08, -0-02 from NY closing levels, after giving up earlier Asia-Pac session gains.

- According to MNI’s technicals team, the focus is on 110-25, a Fibonacci projection, whilst initial key support has been defined at 108-18+ (Nov 27 low).

- Cash US tsys are dealing flat to 2bps cheaper in the Asia-Pac session, with a slight steepening bias apparent. There has been little in the way of meaningful newsflow, with weaker-than expected Official China PMI failing to move the market in a positive direction despite a softening across most-sub-indices. Possibly, local participants have focused on yesterday’s upward revision to Q3 US GDP.

- Later today sees the monthly PCE report, weekly jobless claims, the MNI Chicago PMI and pending home sales, before Chair Powell swings into focus on Friday.

JGBS: JGB Curve Shifts From A Bull-Flattening To Bear-Steepening

JGB futures have reversed course during the Tokyo afternoon session, with the morning’s strong gain giving way to a significant loss, -25 compared to the settlement levels.

- Weaker-than-expected retail sales gave the market a reason to extend US-tsy-induced overnight gains.

- However, by the lunch break, those gains had been pared despite the cautious tone to a speech from BOJ Nakamura. Bloomberg reported that Nakamura said it will take a little more time before the bank can adjust monetary policy, as it needs to act with caution.

- The catalyst for afternoon weakness appears to have been weak demand metrics at today’s 2-year JGB auction. It followed a similar result at the 40-year auction earlier in the week.

- As highlighted in our auction preview, the interplay between the emerging bullish sentiment towards short-term global bonds and a diminished outright yield was anticipated to be intriguing. It is evident that the latter factor significantly influenced the bidding dynamics in today's auction.

- The cash JGB curve shifted from a bull-flattening in the morning session to a bear-steepening.

- The swaps curve has also shifted to a bear-steepening, with rates 1-5bps higher. Swap spreads are mixed.

- Tomorrow, the local calendar sees Jobless Rate, Job-To-Applicant Ratio, Capex, Company Profits and Jibun Bank Japan PMI Mfg data.

AUSSIE BONDS: Reverses Weaker Through The Session, Capex Data & US Tsys Weigh

ACGBs (YM +1.0 & XM -2.5) are mixed after giving up the initial positive reaction to the previously outlined weaker-than-expected Q3 capex data. The market possibly turned its attention to the fact that the data showed the 5th consecutive quarter of growth and Q2 was revised up 0.6pp to 3.4%. It now stands 10.7% higher y/y. Additionally, investment expectations showed a positive outlook, with plans revised 8.5% higher for this financial year.

- Slightly cheaper cash US tsys in the Asia-Pac session has also likely weighed on the local market. Weaker than expected China PMI data failed to deliver a bid to global bonds.

- The cash 3/10 curve has twist-steepened, with yield movement bounded by +/- 2bps. The AU-US 10-year yield differential is 1bp wider at +11bps.

- The swaps curve has bear-steepened, with rates flat to 4bps higher.

- The bills strip is mixed, with pricing -2 to +2.

- RBA-dated OIS pricing is little changed across meetings.

- NSW TCorp has priced an A$1.5 billion increase to the 4.25% 20 February 2036 benchmark bond. The transaction was priced at 5.24% and a spread of 82.73bps over the ACGB 2.75% June 2035.

- Tomorrow, the local calendar sees CoreLogic House Price and Judo Bank Australia PMI Mfg data.

AUSTRALIAN DATA: Investment Outlook Positive

Q3 private capex was lower than expected rising 0.6% q/q but this was the 5th consecutive quarter of growth and Q2 was revised up 0.6pp to 3.4%. It now stands 10.7% higher than a year ago. Building investment rose moderately to be up 13.7% y/y and looking forward residential building approvals seem to be recovering with October showing rises for houses and multi-dwellings. When Q3 GDP is released on December 6, private investment growth is likely to have slowed following two very strong quarters.

- Q3 investment in buildings rose 0.7% q/q after 4.4% and machinery equipment slowed to +0.5% from 2.2%. Mining was the driver at +5.6% q/q whereas non-mining sectors fell 1.3% after rising strongly previously.

Source: MNI - Market News/ABS

- Investment expectations showed that the capex outlook is positive with plans revised 8.5% higher for this financial year. Imports of capex goods have also been robust. The ABS notes the strong rise for the information media and telecoms sector as new data centres are planned.

- October dwelling approvals rose 7.5% m/m with houses up 2.2% and non-houses +19.5%. Annual growth in the total and two main components are off their lows and there is positive 3-month momentum for house approvals. This is good news given Australia’s housing shortage but the level is still 11.5% below February 2020.

Source: MNI - Market News/ABS

NZGBS: Richer, 5Y Outperforms, Business Confidence Highest Since 2015

NZGBs closed off the best levels, flat to 7bps richer, with the 5-year outperforming.

- The move away from the session’s best levels was likely assisted by ANZ’s business survey, which came in stronger again in November. Confidence rose to 30.8, the highest since early 2015. The measure rose sharply in October helped by post-election optimism and a more pro-business government but so far this tendency is not proving temporary. Yesterday the RBNZ spoke about demand slowing less than expected and this data suggests that it could be picking up again.

- Today’s weekly bond auctions also did little to support the local market with the three cover ratios lower than previous offerings at 1.94x to 3.75x.

- Slightly cheaper cash US tsys in the Asia-Pac session has also likely weighed on the local market.

- Swap rates closed 2-7bps lower, with the 2s10s curve steeper.

- RBNZ dated OIS pricing closed little changed after yesterday’s hawkish hold from the RBNZ. OIS pricing is still 1-7bps firmer than pre-RBNZ decision levels.

- Tomorrow, the local calendar sees CoreLogic House Prices and ANZ Consumer Confidence.

NZ DATA: ANZ Business Survey Broadly Positive

ANZ’s business survey was stronger again in November with confidence rising to 30.8 from 23.4, highest since early 2015, and the outlook to 26.3 from 23.1. Both are above their historical averages. These measures rose sharply in October helped by post-election optimism and a more pro-business government but so far this tendency is not proving temporary. Yesterday the RBNZ spoke about demand slowing less than expected and this data is suggesting that it could be picking up again.

NZ ANZ business survey

Source: MNI - Market News/Refinitiv

- Inflation expectations eased 0.1pp to 4.8%, moderating but possibly too slowly, another concern of the RBNZ. They have been gradually coming down but remain above the 3.1% average. Business costs also remain high but eased further, although pricing intentions edged up to 46.8, around the 3-month average.

Source: MNI - Market News/Refinitiv

- Employment remained positive at 5.4% and while it is below the historical average, it is higher than most of 2023.

- Investment remains positive and although capacity pressures eased almost 3 points, they remain slightly above average. Profits turned positive for the first time since mid-2021. Given the focus on housing demand in the RBNZ’s November Statement, it is good news that residential construction rose to 0 from -12.5.

- Exports have been a weak spot in the economy but they improved again in November. They are still lacklustre though.

RBNZ: MNI RBNZ Review - November 2023: Watching Inflation Risks

- The RBNZ left rates at 5.5% as was widely expected but given the statement, press conference and forecast revisions it was a hawkish hold that reiterated the “high for longer” message. The impact of strong population growth has become “apparent” and it is “increasing the risk of inflation remaining above target”.

- The MPC noted that it “would likely need to increase” rates again if inflation is higher than expected and Governor Orr stated that it is “willing” to act if needed and a 25bp rise had been discussed.

- There were near-term upward revisions to growth and downward ones to inflation as expected, but a recession is no longer forecast and the H2 2024 CPI projections are now higher. As a result, the 2024 OCR is 20bp higher than current rates and 50bp of easing has been taken out of the trajectory by Q3 2026.

- The next meeting is not until February 28 and there will be a lot of information for the MPC to digest by then. For easing to begin the RBNZ needs to be “confident” that inflation will be at the mid-point of the band in 1 to 2 years.

- See full review here.

EQUITIES: China & Hong Kong Markets Tracking Lower For 4th Straight Month

Regional equities are mixed in Asia Pac markets as we approach month end. China and Hong Kong markets are a touch higher, despite weaker official PMI data in China. Trends are mixed elsewhere, with markets not showing a strong directional bias. US futures are higher, but only modestly. Eminis last near 4565, +0.12%, while Nasdaq futures are +0.18%, near 16052.5.

- US yields are a touch higher, but remain close to recent lows. The recent pull back in core yields hasn't done much to aid broader equity sentiment.

- The early impetus in HK stocks was to the downside, however the HSI is +0.18% higher at the break. The tech sub index is -0.55%, but above session lows. Note the HSI is tracking down 0.51% for the month, which would be the 4th straight run of monthly losses.

- The CSI 300 is up 0.24% at the break. The official PMIs disappointed in Nov, with manufacturing moving further into contractionary territory, while services just stayed above the 50.0 expansion point. Like the HSI, the CSI 300 is tracking lower for the 4th straight month.

- Elsewhere, Japan, South Korea and Taiwan stocks are all close to flat.

- The ASX 200 is up 0.55%, aided by financial moves.

- In SEA, most markets are weaker. Indonesia stocks are outperforming, up 0.60% at this stage.

JAPAN DATA: Inflows Into Local Stocks Cools, Purchases Of Japan Bonds Steps Up

Offshore inflows into Japan stocks lost momentum last week, barely remaining positive. At ¥4.2bn this is well below the average pace seen in previous weeks. It does extend the run of positive weekly inflows to 9 though. Offshore investors stepped up their purchases of local Japanese bonds. The ¥864.1bn in net inflows was the strongest weekly pace since the first half of October.

- In terms of Japan outbound flows. Local investors were net sellers of both offshore bonds and stocks last week. Selling of offshore stocks was the largest since the end of August.

Table 1: Japan Weekly Investment Flows

| Billion Yen | Week ending Nov 24 | Prior Week |

| Foreign Buying Japan Stocks | 4.2 | 286 |

| Foreign Buying Japan Bonds | 864.1 | 421.9 |

| Japan Buying Foreign Bonds | -84.5 | 4 |

| Japan Buying Foreign Stocks | -209.8 | 120.7 |

Source: MNI - Market News/Bloomberg

FOREX: AUD & NZD Outperform, But Remain Within Recent Ranges

USD upticks have been faded today, although most pairs have stuck to recent ranges. The BBDXY was last 1232.70/80, off nearly 0.1% for the session. US yields have ticked higher but remain close to recent lows (nearly +2bps for some parts of the curve). Equity sentiment has improved somewhat, although gains for US futures and cash Asia Pac bourses have been fairly modest.

- USD/JPY dipped in the first part of trade, but support was evident at 146.85. We last tracked near 147.10, +0.10% firmer in yen terms. Retail sales and IP data didn't shift sentiment, while we saw a poor 2yr auction in the bond space.

- Bank of Japan board member Toyoaki Nakamura said that it will take time and careful consideration to adjust easy policy.

- AUD and NZD are the top performers, both up by around 0.40%, but remaining within recent ranges. NZ data was better, but largely second tier. NZD/USD last tracked near 0.6180, sub post RBNZ highs.

- AUD/USD is just above 0.6640, shrugging off the weaker China PMI data. The AUD/NZD cross has been supported on dips to 1.0730. Copper prices are tracking higher, amid supply concerns.

- Looking ahead, ECB President Lagarde speaks and euro area preliminary CPI data are released. Later the Fed’s Williams speaks on innovations in central banking and there are US jobless claims, October income/spending & deflators, and MNI November Chicago PMI.

OIL: Crude In Narrow Ranges As Waits For OPEC+ Decision

Crude has been trading in a narrow range during the APAC session ahead of today’s OPEC+ meeting. It is being held online and so there is still the possibility that it could be delayed again if the group is still divided over output cuts. Existing cuts are expected to be extended into 2024 but there is a lot of uncertainty over whether they will be deeper in response to recent price weakness, if they don’t then crude is likely to fall sharply. Oil prices are down moderately as is the USD index.

- Brent is down 0.2% to $82.71/bbl, off the intraday high of $82.93 and the earlier low of $82.39. WTI is 0.1% lower at $77.78/bbl after a high of $77.96 and low of $77.46.

- Bloomberg is reporting that Saudi Arabia wants other OPEC members to reduce output as it has done. There is a disagreement over quotas for Nigeria and Angola, they have been underproducing for some time. The WSJ reported that delegates told it that OPEC+ is considering deepening its output cuts by up to 1mbd. Non-OPEC output has been rising, especially in the US.

- Later the Fed’s Williams speaks on innovations in central banking and there are US jobless claims, October income/spending & deflators, and MNI November Chicago PMI. Also ECB President Lagarde speaks and euro area preliminary CPI data are released. Canadian Q3 GDP prints.

GOLD: Consolidates After A Five-Day Rally

Gold is slightly higher in the Asia-Pac session, after closing 0.2% higher at $2044.24 on Wednesday.

- The precious metal briefly eclipsed the $2050 mark, closing in on the yearly high of $2063 after a five-day rally.

- US Treasuries extended the recent rally, led by the 2-year. US Treasury yields finished 7-9bps lower. This upward movement was underpinned by favourable market data. Softer European CPI inflation data, coupled with a "Goldilocks"-esque adjustment to Q3 US GDP, contributed to a 6bp drop in the US tsy 10-year yield to 4.26%.

- Fed rate cut bets deepened thanks to the lack of pushback from most Fed officials.

- The core PCE price index will be released Thursday. It’s forecast to decelerate to 0.1% in October from the previous month.

- According to MNI’s technicals team, the trend condition in gold unsurprisingly remains bullish and this week’s strong rally reinforces this set-up. The clear break of resistance at $2009.4, the Nov 7 high, has confirmed a resumption of the uptrend and signals scope for an extension towards 2063.0, the May 4 high and a key resistance. Note the all-time high is at $2070.4 (Mar 8 ‘22).

CHINA DATA: Weaker Export Orders Weigh On Both Manufacturing & Services PMIs

The detail in the manufacturing PMI showed easing across most of the sub-indices. Output back to 50.7 (from 50.9), new orders to 49.4 (from 49.5). Employment ticked up slightly to 48.1, but remains close to recent lows, having not shown much improvement in 2023 to date.

- New export orders fell more noticeably to 46.3, from 46.8. We are -0.4pts down on levels of a year ago for this index, so it isn't suggesting a sharp further slowing in y/y export growth.

- On the prices side, trends were mixed. Input prices eased to 50.7 from 52.6, while output prices rose to 48.2, from 47.7. For both indices we are well below earlier 2023 highs.

- On the services side, new export orders were noticeably weaker, down to 46.8 from 49.1.

- Most other components showed modest improvement, albeit from fairly lows levels.

- Aggregate new orders rose to 47.2 (from 46.7). Employment firmed a touch to 46.9 from 46.5.

BOK: Staying Restrictive Long Enough To Bring Inflation Back Towards Target

The BoK statement presents a fairly evenly balanced outlook as we progress into 2024. The central bank has left the door ajar for a further tightening, although the bar for such a move is likely to remain fairly high.

- Whilst inflation forecasts for this year and next were nudged higher, the BoK still sees the general trajectory of inflation as skewed to the downside. "...inflation is projected to maintain its underlying slowing trend owing to the weakening of demand-side pressures and to declines in the prices of global oil and agricultural products."

- On growth, "domestic economic growth is expected to maintain its improving trends with an ongoing recovery in exports." It was also noted the pace of the consumption recovery is slow, while the outlook has a high degree of uncertainty. There are also high uncertainties regarding household debt and external conditions.

- Equally though the central bank stated "will maintain a restrictive policy stance for a sufficiently long period of time until the Board is confident that inflation will converge on the target level."

- Hence a near term policy pivot in the first stages of 2024 is unlikely.

SOUTH KOREA DATA: Industrial Production Growth Weaker Than Expected, As Chip Production Falls

South Korea Oct IP growth was much weaker than expected, falling 3.5% in the month, versus a 0.4% expected rise. This is the largest m/m drop since Dec last year. The prior print was +1.7%. This bought y/y momentum to 1.1% from 2.9% prior, which was also comfortably sub forecasts (4.5%).

- The IP drop was weighed heavily by a drop in semi-conductor production, off 11.4%. Some offset came elsewhere from other electronics production.

- Other detail showed retail sales down 0.8% m/m, while facilities investment fell by 3.3% m/m, albeit after an 8.7% gain in Sep.

- All industry output fell 1.6%, the largest drop since April 2020.

ASIA FX: USD/Asia Pairs Firm, IDR & THB Underperform

USD/Asia pairs are mostly higher ahead of month end. China PMIs were weaker than expected, but didn't have a lasting impact on sentiment. USD/CNH found selling interest above 7.1400, while local equities have struggled for positive traction. IDR and THB, along KRW have seen losses, particularly for the rupiah. Tomorrow, we get the Caixin PMI in China, along with South Korean Nov trade figures.

- USD/CNH got to highs of 7.1455 not long after the PMI misses. Manufacturing stayed in contraction, services nearly joined it. However, we found selling interest and pulled back to 7.1230 before stabilising. Local equities are struggling to end the month on a positive note. The pair was last near 7.1330.

- Spot USD/HKD has continued to climb, the pair last near 7.8100, just below session highs (7.8109). This puts us back above the 20-day EMA (near 7.8050), while the 50-day is near 7.8130. The pair hasn't been above the 20-day EMA since early Nov. Recent lows rest at 7.7861. The move up in USD/HKD has coincided with a ticker higher in US-HK 3 month interest rate differential (last -23bps, versus recent wides of -32bps). Still, USD/HKD started moving higher before the yield differential shifted back in favor of the USD. Yesterday's Hong Kong equity weakness, where the HSI closed very close to YTD lows may have been a factor.

- 1 Month USD/KRW has tracked recent ranges, last near 1289, slightly above NY closing levels from Thursday. The BoK held rates at 3.50% as expected. Policy is likely to stay restrictive for some time to ensure inflation comes down, although less members saw the need to tighten policy. Earlier data showed weaker than expected IP figures, due to a slump in chip production for Oct.

- The rupiah is underperforming in the first part of Thursday trade. USD/IDR is +0.60% higher, last tracking near 15485. his leaves it as comfortably the worst performer in EM Asia FX for the session so far. US yields have stabilized somewhat, but are only a touch above recent lows. Today's move high in USD/IDR is also at odds with Wednesday weakness in US real yields. Month end could be seeing USD buying flows coming through. BI noted at its annual meeting late yesterday that it may be in an extended pause phase, as rates stay high to curb inflation risks (BBG).

- USD/THB has regained some ground, last near 34.94, +0.35% firmer for the session. This is in line with broader USD consolidation. Yesterday's on hold BoT outcome highlighted the increased volatility of the baht (8-9% now versus 3.-4% prior, BBG). Recent lows in the pair rest under 34.60, while the simple 200-day is around 35.00.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 30/11/2023 | 0700/0800 | ** |  | DE | Retail Sales |

| 30/11/2023 | 0700/0800 | ** | | DE | Import/Export Prices |

| 30/11/2023 | 0730/0830 | ** |  | CH | Retail Sales |

| 30/11/2023 | 0730/0730 |  | UK | DMO to publish gilt operations calendar for FQ4 | |

| 30/11/2023 | 0745/0845 | ** |  | FR | PPI |

| 30/11/2023 | 0745/0845 | ** | | FR | Consumer Spending |

| 30/11/2023 | 0745/0845 | *** | | FR | GDP (f) |

| 30/11/2023 | 0745/0845 | *** | | FR | HICP (p) |

| 30/11/2023 | 0800/0900 | ** | | CH | KOF Economic Barometer |

| 30/11/2023 | 0800/0900 |  | EU | ECB General Council Meeting | |

| 30/11/2023 | 0855/0955 | ** | | DE | Unemployment |

| 30/11/2023 | 0930/0930 | | UK | Decision Maker Panel Data | |

| 30/11/2023 | 1000/1100 | *** | | EU | HICP (p) |

| 30/11/2023 | 1000/1100 | ** | | EU | Unemployment |

| 30/11/2023 | 1000/1100 | *** |  | IT | HICP (p) |

| 30/11/2023 | 1330/0830 | *** |  | US | Jobless Claims |

| 30/11/2023 | 1330/0830 | ** | | US | WASDE Weekly Import/Export |

| 30/11/2023 | 1330/0830 | *** |  | CA | GDP - Canadian Economic Accounts |

| 30/11/2023 | 1330/0830 | *** | | CA | Gross Domestic Product by Industry |

| 30/11/2023 | 1330/0830 | *** | | CA | CA GDP by Industry and GDP Canadian Economic Accounts Combined |

| 30/11/2023 | 1330/0830 | * | | CA | Payroll employment |

| 30/11/2023 | 1330/0830 | ** | | US | Personal Income and Consumption |

| 30/11/2023 | 1330/1430 | | EU | ECB's Lagarde at 5th ECB Forum | |

| 30/11/2023 | 1405/0905 | | US | New York Fed's John Williams | |

| 30/11/2023 | 1445/0945 | *** | | US | MNI Chicago PMI |

| 30/11/2023 | 1500/1000 | ** | | US | NAR Pending Home Sales |

| 30/11/2023 | 1530/1030 | ** | | US | Natural Gas Stocks |

| 30/11/2023 | 1600/1600 | | UK | BOE's Greene speech at Leeds University | |

| 30/11/2023 | 1630/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 30/11/2023 | 1630/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 01/12/2023 | 2200/0900 | ** |  | AU | IHS Markit Manufacturing PMI (f) |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.