Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Headlines that China is looking into allowing local governments to purchase unsold homes supported risk appetite today. China real estate stocks rose, while CNH, AUD and NZD rallied. Overall, China equity markets are still tracking lower at this stage though.

- As expected, the 1yr MLF rate was held steady in China. Australian Q1 wages were slightly below consensus expectations, but close to RBA forecasts.

- It has been a steady session for both US Tsy and JGB futures, with focus on the upcoming US CPI print.

- Outside of the US inflation print, appearances from ECB's Rehn, Muller, Villeroy & Makhlouf and Fed's Kashkari & Bowman are due.

MARKETS

US TSYS: Treasury Futures Steady, Volumes Low Ahead Of US CPI

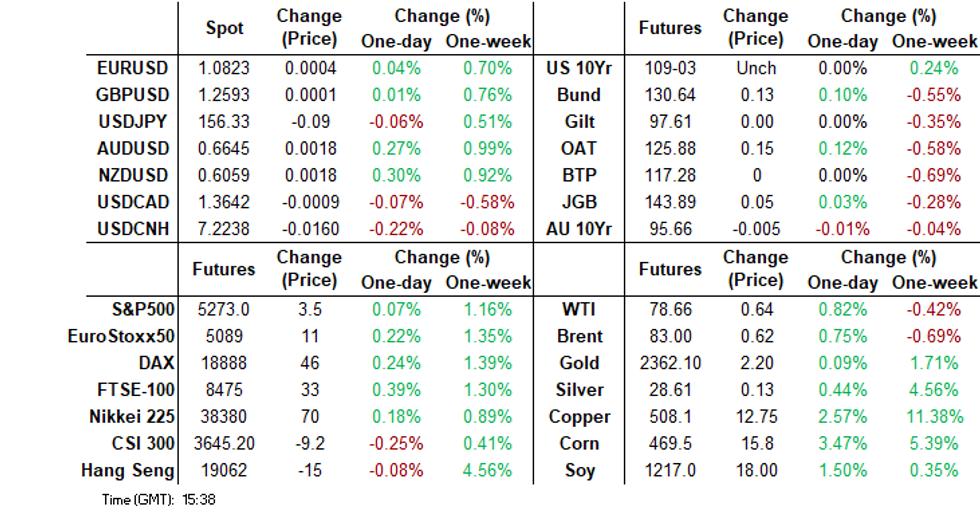

- It has been a very quiet session here in Asia, volumes are low, while ranges have been very tight and trade just off the overnight highs, the 10Y contract trades down ( - 00+) at 109-02+, initial resistance is 109-06+/08+ (Channel top from Feb 1 high / 50-day EMA), while the 2Y trades at 101-22.875 down (- 00.25).

- Cash Treasuries are 0.5bp higher to 0.5bp lower, the curve slightly flatter. The 2Y yield +0.4bps at 4.819%, 10Y unchanged at 4.439%, while 2y10y is -0.829 at -38.565

- US CPI will be the focus today, a upside surprise will dial up concerns that the Q1 acceleration wasn’t just a bump and could see 2Y Treasury yields eye 5% again, with the start point to Fed cuts pushed further out amidst a still high bar to a rate hike, while a downside surprise would still see sensitivity but the onus is on multiple low inflation readings before cut expectations are meaningfully brought nearer.

- U.S. CPI Preview: May 2024 MNI View: Testing Persistence Of Q1 “Bump” In Disinflation Path - (See link)

- Looking Ahead: Busy session today with MBA Mortgage Applications, Empire Manufacturing, Retail Sales & CPI while ECB's Rehn, Muller, Villeroy & Makhlouf and Fed's Kashkari & Bowman are due to speak.

JGBS: Tracking Recent Ranges, Q1 GDP & 20yr Supply On Tap Tomorrow

JGB futures have had an uneventful first part of Wednesday trade. JBM4 was last at 143.88, +.04. We have stuck to recent ranges, with downside limited to 143.84, while moves above 143.90 have not extended.

- Local news flow has been light with no data out today and a quiet auction calendar. Tomorrow there will be focus on the Q1 GDP print (which is expected to be negative), while a 20yr debt auction is due.

- US Tsy futures have been steady, the 10yr sitting unchanged in latest dealings. We have the US CPI print later, which is no doubt keeping some market participants on the sidelines.

- In the cash JGB space, most yields sit close to unchanged. The 10yr was last near 0.96%. The 30- and 40yr tenors have seen a further uptick in yields though.

- Swap rates are mostly lower, the 10yr last close to 1.01%.

RBA: RBA’s Response To Budget To Be Watched Closely

Treasurer Chalmers brought down the FY25 budget on Tuesday and as expected it showed a $9.3bn surplus for FY24 but deeper deficits over the forecast horizon as spending as a share of the economy rises. The signature programmes are cost-of-living relief worth $7.8bn which is aimed at bringing down inflation and $22.7bn for Future Made in Australia industry subsidies. Many don’t agree that the budget is disinflationary and the RBA’s response will be followed closely given the additional $20bn in the economy from policy decisions.

- Treasury’s Q2 2024 CPI forecast was revised down 0.25pp to 3.5% while Q2 2025 was unchanged at 2.75% but Q2 2026 revised up 0.25pp to 2.75%. Despite unchanged 2025, the government estimates that the energy and rent relief will “directly reduce” headline inflation by 0.5pp in FY25. As a result, headline could be back in the RBA’s band by end-2024. The RBA is forecasting 3.8% for Q2 and Q4 2024.

- Growth was left unchanged at 1.75% for FY24, as weaker consumption and dwelling investment were offset by stronger business capex and public demand. GDP was revised down 0.25pp to 2% for FY25 and up 0.25pp to 2.25% for FY26.

- FY25 is now expected to show a deficit of $28.3bn or 1% of GDP up from $18.8bn or 0.7% in the MYEFO. FY26 is now a deficit of $42.8bn or 1.5% of GDP up from $35.1bn or 1.2%. This is reflected in the receipts as a share of the economy little changed despite tax cuts but expenditure has been revised up 0.4pp to 26.4% in FY25 and 0.5pp to 26.6% in FY26.

- FY25 gross debt has been revised down 0.3pp to 33.9% after FY24 was also revised down 0.3pp. Subsequent years are little changed from the MYEFO.

- Cost-of-living relief includes $3.5bn for energy with $300 paid to households over four quarters starting Q3 and $1.9bn in rent assistance. The next election is due by May 2025.

Australian Data: Q1 WPI In Line With RBA, Share Of Large Wage Gains Rises Further

The Q1 wage price index rose a less-than-expected 0.8% q/q to be up 4.1% y/y, the third straight quarter above 4%. Q4 was revised up 0.1pp to 1.0% q/q. The RBA had expected 4.2% y/y and so the result is broadly in line with its forecast and so this data is unlikely to change the current on hold stance.

- The public and private sectors saw wage growth ease rising 0.8% q/q and 0.5% respectively, both the lowest since Q1 2022. They are now up 4.1% and 3.8% y/y down from 4.2% and 4.3% in Q4. The public sector is heavily impacted by the timing of new agreements and wage cap changes and there were large increases in Q3 and Q4 last year.

- The share of employees receiving a pay hike in Q1 eased to 14% from 19% in Q1 2023 with the average rise 4%. In the private sector 12% had an increase down from 14% in Q1 2023 but the size remained at 4.4% around where it has been every quarter since then except Q3 which was impacted by the minimum wage hike.

- The share receiving a wage increase above 3% over the last year rose to 66% from 50% in Q1 2023. A rise of 0-2% picked up slightly for the first time since Q2 2021 but is still 4.1pp below Q1 2023. The share receiving large gains of over 6% continued to trend higher in Q1 at 14.4% up 3.8pp y/y and 4-6% at 31% up 6.5pp y/y.

Source: MNI - Market News/ABS/SEEK

AUSSIE BONDS: ACGB Curve Flattens, US CPI Later & AU Employment Data Thursday

ACGBs (YM -2.0 & XM 0.0) are mixed today, with the curve slightly flatter. Earlier, The Q1 wage price index rose a less-than-expected 0.8% q/q to be up 4.1% y/y, the third straight quarter above 4%. Q4 was revised up 0.1pp to 1.0% q/q. The focus will now turn to US CPI due out later tonight and more locally AU Employment data on Thursday.

- Cross-asset moves: US equity futures are little changed today, the ASX200 is up 0.50% to be a top performer in the region, while in the FX space, AUD and NZD were the top performing G10 currencies as they were supported by positive news from China around the property sector, Iron Ore is down 0.65% at $115.30/ton.

- Issuance: Australia sold A$800m 2.75% 2035 bonds at 4.3516% average yield for a bid/cover ratio of 2.9250x up from 2.8437x prior

- Front-end ACGBs are a touch weaker today as the curve bear-flattened, the 2y10y -1.520 at 28.940 with yields flat to 2bps higher, while the AU-US 10-year yield differential is 1bps lower, now -11bps

- Swap rates are 1-2bps lower

- The bills strip is 1bp lower

- RBA-dated OIS implied rate now pricing 1bps lower into the November meeting, market has softened a touch and is now pricing 7.5bps of easing into year-end to a terminal rate of 4.275%

- Looking ahead, Employment data is due out at 11.30 AEST on Thursday

NZGBS: Richer Ahead of US CPI

NZGBs are 3-4bps richer with the curve slightly flatter, we are trading at best levels of the session as we head into the close, yields have now fallen for the fourth straight day. It has been a quiet day for data int he region, while China announced new plans to support the struggling local property market, focus now turns to US CPI due out later today.

- US treasury futures initially opened a touch weaker this morning, although those moves have been erased and we now trade little changed across the curve with the 10Y at unchanged at 109-03, while the 2Y is (- 00.375) at 101-22.75

- NZGB yields opened lower this morning, and continued that move into the close to finishing the session 3-4bps richer, the 5y10y is little changed -0.400 at 11.80

- NZ population growth is slowing due to reduced inward immigration and increasing emigration of citizens seeking better job prospects abroad. Despite ongoing immigration, which contributes to housing demand and inflation concerns, the pace of population increase in the first quarter was the slowest since 2022, as per BBG.

- Swap rates are 1-3bps lower.

- RBNZ dated OIS is unchanged this morning, with a cumulative 46.5bps of easing is priced by year-end.

- Looking Ahead: Non Resident Bond Holdings on Thursday and PPI input/output on Friday

FOREX: Risk Currencies Buoyed By Potentially More China Property Support

Risk currencies have continued to outperform, with the latest leg higher driven by headlines that China is mulling further support for the troubled onshore property sector.

- China is contemplating a significant proposal to address its struggling property market by having local governments purchase millions of unsold homes, with the aim of converting them into affordable housing (per Bloomberg).

- Both AUD and NZD are +0.30% firmer against the USD. AUD/USD was last around 0.6645/50, just off session highs (0.6651). This right around the May 3 high, while 0.6668 represents the Mar 8 high and is also viewed as key short term resistance.

- The currency largely shrugged off a slightly weaker than expected Q1 wages print. Commodities are higher, led by copper, although iron ore is showing less enthusiasm to the China news, the active contract last near $114/ton.

- NZD/USD was last near 0.6060, not too far from the 200-day EMA (0.6068).

- USD/JPY is close to unchanged, last around 156.40/45. This leaves the yen weaker on crosses, particularly AUD and NZD.

- In the cross asset space, US equity futures sit a touch higher, while regional equities are mostly higher. China mainland markets are lower, but property sub-indices are higher.

- US yields are relatively steady. The BDXY sits down a touch, last at 1251.2 (off just under 0.10%).

- Looking ahead we have the US CPI as the main focus point coming up. Outside of the US inflation print, appearances from ECB's Rehn, Muller, Villeroy & Makhlouf and Fed's Kashkari & Bowman are due.

ASIA STOCKS: China Equities Mostly Lower On US Tariffs, Property Up On Policy Support

Chinese equities are mostly lower today, on the back of mixed earnings from the like of Alibaba who reported a sharp drop in net income with a buyback doing little to help the stock, while Tencent beat expectations, but gave a more cautious tone on the outlook for the Chinese economy while US tariffs on a wide range of Chinese imports including semiconductors, EVs and batteries have done little to help the market today. The property sector has been the only sector higher, after China has announced they are looking into allowing local governments to purchase unsold homes. Earlier, China kept the 1yr MLP on hold at 2.50% and looking ahead the market now awaits earnings from Baidu and JD.com. Hong Kong markets were closed today for Buddha's Birthday.

- China onshore markets are lower today, the CSI300 down 0.29%, we still hold above all moving averages with support now the 20-day EMA at 3,607, the CSI300 Real Estate Index is up 5.20%, while small and growth indices are also lower today although faring slightly better than the large-cap space with the CSI1000 is down 0.17% while the ChiNext off 0.13%.

- In the property space, China is contemplating a significant proposal to address its struggling property market by having local governments purchase millions of unsold homes, with the aim of converting them into affordable housing. This ambitious plan, currently under review by the State Council, involves state-owned enterprises buying distressed developer properties at discounted rates, funded by loans from state banks, as per BBG.

- Looking ahead, Industrial Production & Retail Sales on Friday

ASIA PAC STOCKS: Regional Asian Equities Edge Higher On Strong Tech Earnings

Regional Asian equities were higher slightly higher today, with the MSCI Asia Pacific Index climbing 0.50% and reaching the highest levels since 2022, as tech earnings and gains in the US equity market on Tuesday support the local markets. Japan's Nikkei 225 was up 0.13%, while Topix is up 0.09%, data has been light out of the region today, with eyes turning to GDP due out on Thursday. South Korea was out today for Buddha Birthday, with the local market waiting for Employment data due out on Friday. Taiwan equities have been well supported by higher global semiconductor prices which were driven by the US imposing further tariffs on Chinese semiconductor imports, the Taiex is up 0.80%. Australian equities are higher today, financials were lower, but were more than offset by gains in metals and mining with the ASX200 trading up 0.45%. Elsewhere, New Zealand equities continue their move lower finishing the session down 0.79%, while foreign investors continue selling Indonesian equities now marking 26 of the past 28 days of selling although the market has held up rather well signally demand from local investors remains strong, the JCI is up 1.15%

ASIA EQUITY FLOWS: Tech Stocks See Inflows, While Outflows Continue In Indonesia

- South Korean equities were slightly higher on Tuesday, flows have been mixed over the past few days although still positive with a net inflow of $275m. It's a public holiday in SK today. The 5-day average has dropped due to a strong inflow 6 days and is now just $55m, still above the 20-day average of $41m although both sit well below the 100-day average at $181m.

- Taiwan equities were again higher on Monday, with the Taiex closing at all-time-highs, tech and semiconductor names are leading the way. There is nothing on the local calendar this week, with focus turning to US CPI later tonight. Foreign investors have been buyers of Taiwanese equities recently with the past five-day seeing an inflow of about $1b. The 5-day average is now $205m well above the 20-day average of -$65m and the 100-day average at $75m.

- Thailand equities edged slightly higher on Tuesday with the SET breaking back above the 50-day EMA a level that we have been really unable to hold above over the past year. Equity flow has been mixed over the past week, although positive for the past two days with the 5-day average now at $0.4m, the 20-day average -$7.9m, while the 100-day average is -$17m.

- Indonesian equities continue to see foreign investors selling stocks, we are now at 25 of the past 27 days of selling for a net outflow of $1.84b. The JCI finished Tuesday session down 0.30% and closed below the 200-day EMA while the 14-day RSI trades below 50 at 42, and the MACD indictor shows increasing red bars. The 5-day average is now -$72m in line the 20-day average at -$69m while the 100-day average is still positive at $4.5m

- The Indian Nifty 50 has now marked 8 straight days of net selling from foreign investors with a net outflow of $2.9b as of May 13th. We have however seen the index bounce right off the 100-day EMA, which could show signs of a turnaround in flows over the next few days. The 5-day average now -$494m, the 20-day average is -$268m while the 100-day average is still positive but declining quickly and sits at $30m.

Table 1: EM Asia Equity Flows

| Yesterday | Past 5 Trading Days | 2024 To Date | |

| South Korea (USDmn) | 215 | 275 | 15156 |

| Taiwan (USDmn) | 613 | 1028 | 1867 |

| India (USDmn)* | -155 | -2083 | -2687 |

| Indonesia (USDmn) | -48 | -360 | -29 |

| Thailand (USDmn) | 63 | 2 | -1875 |

| Malaysia (USDmn) * | 6 | 156 | -177 |

| Philippines (USDmn) | 58 | 9.3 | -272 |

| Total | 752 | -973 | 11982 |

| ** Data Up To Apr 13th |

OIL: US Crude Drawdown Supports Prices, US CPI, EIA Data & IEA Report Out Later

Oil prices are up during APAC trading today on the back of a reported crude drawdown. WTI is 0.7% higher at $78.57/bbl off the intraday high of $78.75. Brent is up 0.6% to $82.90 after reaching $83.07 but the benchmark struggled to hold breaks above $83. The USD index is down slightly.

- Bloomberg reported that there was a US crude inventory drawdown of 3.1mn barrels last week, according to people familiar with the API data. Gasoline stocks fell 1.27mn while distillate rose 349k. The official EIA data is released later today, as well as the IEA’s monthly report.

- OPEC members have been producing above quotas in 2024 but the group meets on June 1 to discuss whether to extend output cuts into H2. At the same time though, some large producers want their recognised capacity to be revised upwards. Saudi Arabia needs high prices for fiscal purposes while others want to produce more, which is likely to make agreement difficult.

- Later the focus will be on US April CPI (see MNI preview) which is expected to show a moderate improvement in the annual rates. Recent inflation-related data have printed to the upside and the Fed wants more evidence of slowing inflation before easing, which concerns oil markets re its impact on energy demand.

- There are also US April retail sales and real earnings data. The Fed’s Barr, Kashkari and Bowman speak. Euro area Q1 GDP/employment and March IP are released.

GOLD: Edging Higher, Softer USD Helping, US CPI Coming Up Later

Gold is just under session highs last near $2360.4. We are modestly up from end Tuesday levels, where bullion rallied just under 1%. The main supports came from a weaker USD/softer yield backdrop.

- The USD has remained softer today, particularly against higher beta currencies. This has helped keep dipped in gold supported. Earlier lows were at $2355.

- Levels wise for gold, next resistance is at $2,431.50 - the bull trigger. Any return lower would eye $2,269.1, the 50-day EMA.

- Focus coming up will be on the US CPI print.

PHILIPPINES: MNI BSP Preview - May 2024: Still On Hold

EXECUTIVE SUMMARY

- The BSP is expected to keep interest rates unchanged at 6.50% at tomorrow’s policy meeting. This is the broad sell-side consensus. Our firm bias is also with the status quo. The policy rate has been at 6.50% since October last year.

- Headline inflation remains near the top end of the forecast band, and while domestic growth is cooling, it is likely too early for the central bank to shift in a dovish direction on this basis.

- Broader sell-side views see the BSP easing cycle commencing late in 2024/early 2025.

- Click to view the full preview here:

ASIA FX: CNH Rallies On Potentially More Housing Market Support

USD/Asia pairs are lower across the board. A continued softer dollar backdrop against the majors has helped, while headlines of potentially more housing support in China has been another positive. Regional equity sentiment is mixed but hasn't weighed on risk appetite in the FX space. Still to come today is India's trade balance for April. Tomorrow, we have the BSP decision as the main focus point. No change is expected. Also out is South Korean money supply.

- USD/CNH sits close to session lows around 7.2230. We are around 0.20% stronger in CNH terms. Spot USD/CNY is also lower last just under 7.2250. Sentiment has been aided by headlines around potentially further China property support (per BBG). China is contemplating a significant proposal to address its struggling property market by having local governments purchase millions of unsold homes, with the aim of converting them into affordable housing. Local equity indices are down in terms of the aggregate but real estate indices are higher. Earlier, as expected the 1yr MLF was held steady at 2.50%.

- 1 month USD/KRW is lower, last around 1339, but remains within recent ranges for May so far. We are +0.35% stronger in KRW terms versus end NY levels on Tuesday. The 50-day EMA is around 1356.55 on the downside. A reminder that onshore markets are closed today.

- Spot TWD is around 0.50% firmer, last near 32.25/30, while the 1 month USD/TWD NDF is back to 32.165. We are trending back towards the 50-day EMA (32.14), which is a support zone which held in early May. Equity sentiment is positive amid recent tech gains (the Taiex is up 0.90% today). Offshore investors have added over $1bn to local shares this week.

- USD/THB had fallen to 36.50, but sits slightly higher in recent dealings. This is fresh lows back to mid April for the pair. Consumer confidence edged down in April, while the finance minister will meet with the BoT tomorrow to discuss different opinions on interest rates (per BBG).

- USD/PHP is back to 57.60/65, around 0.40%stronger, but the 1 month NDF has seen a more modest PHP gain. Tomorrow, we have the BSP decision but no change is expected.

- Spot USD/IDR is back towards 16080, around +0.20% firmer in IDR terms so far. April trade figures printed. Export and import growth were weaker than forecast, albeit still in positive y/y territory. The trade surplus eased back to $3559mn, from $4578mn in March.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 15/05/2024 | 0600/0800 | *** |  | SE | Inflation Report |

| 15/05/2024 | 0645/0845 | *** |  | FR | HICP (f) |

| 15/05/2024 | 0900/1100 | ** |  | EU | Industrial Production |

| 15/05/2024 | 0900/1100 | *** | | EU | GDP (p) |

| 15/05/2024 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 15/05/2024 | 1215/0815 | ** |  | CA | CMHC Housing Starts |

| 15/05/2024 | 1230/0830 | *** | | US | CPI |

| 15/05/2024 | 1230/0830 | ** | | CA | Monthly Survey of Manufacturing |

| 15/05/2024 | 1230/0830 | *** | | US | Retail Sales |

| 15/05/2024 | 1230/0830 | ** | | US | Empire State Manufacturing Survey |

| 15/05/2024 | 1300/0900 | * | | CA | CREA Existing Home Sales |

| 15/05/2024 | 1400/1000 | * | | US | Business Inventories |

| 15/05/2024 | 1400/1000 | ** | | US | NAHB Home Builder Index |

| 15/05/2024 | 1400/1000 | | US | Fed Vice Chair Michael Barr | |

| 15/05/2024 | 1405/1505 |  | UK | Bernanke Review of Bank of England Forecasting | |

| 15/05/2024 | 1430/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 15/05/2024 | 1600/1200 | | US | Minneapolis Fed's Neel Kashkari | |

| 15/05/2024 | 1920/1520 | | US | Fed Governor Michelle Bowman | |

| 15/05/2024 | 2000/1600 | ** | | US | TICS |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.