Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

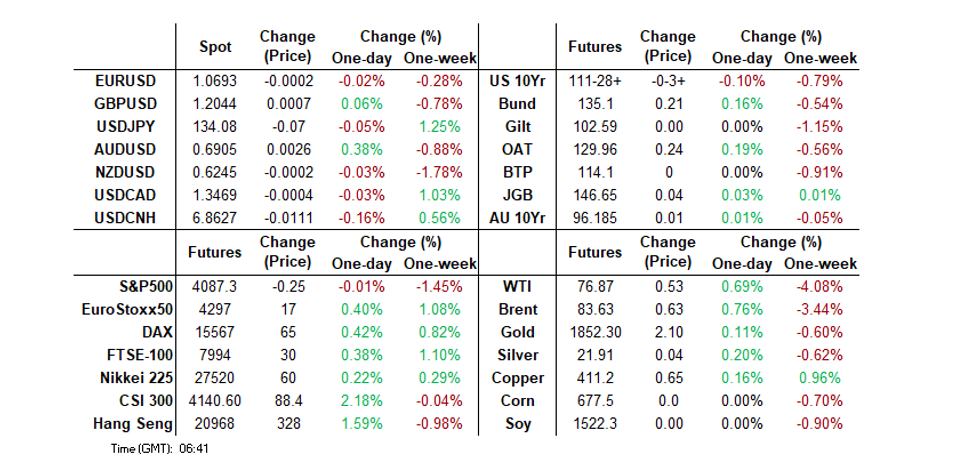

- Cash Tsys are closed on Monday due to observance of the Presidents Day holiday. Tsy futures saw modest pressure in early trade, with local participants looking to lean against Friday's bid. However heightened geopolitical tensions (centred on Sino-U.S. relations and the latest round of North Korean missile launches) likely limited the follow through. Pressure then extended a little as Asia-Pac participants perhaps used the opportunity to set fresh shorts/exit longs after Friday's richening, with continued regional focus on the recent repricing of market expectations re: Fed tightening. Moves across G-10 have been limited.

- The CSI is up ~2% at this stage. Reports pointed to better higher frequency activity indicators in Feb, such as rail traffic. Goldman Sachs also put out a bullish China stock note. A Reuters report that banks should curtail lending, after record lending in Jan, didn't appear to impact market sentiment in a negative way.

- Eurozone consumer confidence provides the only data of note on Monday, with the U.S. & Canadian public holidays thinning out wider liquidity.

US TSYS: Futures Cheaper In Asia, Cash Closed

TYH3 deals at 111-28, -0-04, a touch above the base of its 0-06+ range on volume of ~45K.

- Cash tsys are closed on Monday due to observance of the Presidents Day holiday.

- Tsys saw modest pressure in early trade, with local participants looking to lean against Friday's bid. However heightened geopolitical tensions (centred on Sino-U.S. relations and the latest round of North Korean missile launches) likely limited the follow through.

- Pressure then extended a little as Asia-Pac participants perhaps used the opportunity to set fresh shorts/exit longs after Friday's richening, with continued regional focus on the recent repricing of market expectations re: Fed tightening.

- Little in the way of meaningful macro headline flow crossed in the latter half of the session.

- The broader macro docket is very thin on Monday, with wider liquidity set to be hampered by the U.S. holiday.

US TSYS: Not Much MOVEment Alongside Recent Repricing

The ICE-Bank of America MOVE index remains comfortably shy of cycle highs even after the recent data/Fedspeak-inspired shift in Fed-dated OIS markets, although the index remains elevated vs. “normal” post-GFC levels and has bounced from YtD lows seen in early February. Friday’s lack of follow through when it came to breaches/tests of YtD highs in 5+-Year Tsy yields will have capped vol. at the backend of last week, while the minutes covering the most recent FOMC meeting and PCE data suite providing the focal points during the current holiday-shortened week.

Fig. 1: ICE-Bank of America MOVE Index

Source: MNI - Market News/Bloomberg

JGBS: Contained Swings Largely Derived From Core Global Fi Moves

Spill over from wider core global FI markets was largely in the driving seat on Monday, with JGB futures initially showing just through their overnight session high, before fading, then stabilising off session lows. That leaves the contract +6 into the bell, with cash JGBs running little changed to 2bp richer, as 7s outperform on the curve.

- Swaps saw a bull flattening move, sitting 0.5-2.0bp lower, leaving swap spreads mixed.

- A modest round of cheapening in the super-long end after the BoJ’s 25+-Year Rinban purchases were scaled back by Y50bn was quickly unwound on the subdued offer/cover ratio seen in that bucket.

- 20-Year JGB supply and flash Jibun Bank PMIs headline locally on Tuesday.

- Further out, Japanese PM Kishida’s nominee to succeed outgoing BoJ Governor Kuroda, Kazuo Ueda, will appear at a confirmation hearing in the lower house of parliament on Friday. The government has touted Ueda’s communication skills as a major factor behind his nomination. A reminder that the Bank is expected to move away from ultra-loose policy settings in the post-Kuroda era and this hearing could give the first meaningful insight into Ueda’s preferences when it comes to policy settings.

- Some BoJ watchers have outlined their views re: the risk of a further YCC tweak at the BoJ’s March meeting, which could put less pressure on Ueda during the early days of his governorship.

AUSSIE BONDS: Market Coils With Cash U.S. Tsys Closed

With nothing on the local data docket, Aussie bonds gave up early gains and tracked U.S. Tsy futures lower to close with YM -2.0 and XM +2.0. Cash ACGB yields close 4-5bp higher than morning lows, with the 3/10 cash curve 4bp flattener on the day.

- Swaps rates also reversed morning strength to close -2bp to +2bp, with the 10-year outperforming.

- Except for June bills which closed +1.0, the bill strip was 4-6bp lower today led by the reds.

- March meeting RBA-dated OIS holds its morning level at an 88% chance of a 25bp hike. Terminal rate expectations however move 5bp higher to be back at the top of the recent 4.10 to 4.22% trading range.

- On the news front, Treasurer Chalmers, in an interview on Sky News Australia, appeared keen to reiterate the message that the ongoing review of the RBA is to make sure "that they are accountable for that decision as an independent organization.”

- Looking ahead, the RBA Meeting Minutes are released tomorrow, but the focus remains on Wednesday’s Q4 WPI data.

NZGBS: Cyclone Recovery Task Force Announced

NZGBSs were virtually unchanged at the close with early strength given up as U.S. Tsy futures slid.

- Swaps were mixed on the day with the 2-year rate 5bp higher and the 10-year rate -2bp.

- Awaiting the RBNZ’s first-rate decision since November, UBS became the first sell-side name to adopt the base case of the RBNZ pausing its tightening cycle this week to assess the implications of Cyclone Gabrielle. RBNZ-dated OIS covering this week's meeting was was little changed, showing ~46bp of tightening, with suggestions that the UBS note came out near/after the local market close. Terminal OCR expectations were higher today, closing +5bp at ~5.29%.

- Elsewhere, PM Hipkins announced a Cyclone Recovery Task Force and a Cyclone Support Package. He also said he would consider possible wage subsidies and changes to immigration settings. Earlier, Finance Minister Robertson estimated the cost of cyclone repair at ~NZ$13bn, with insurers set to cover a portion of the burden.

- Note that Robertson also stressed the need for the RBNZ to combat inflation, with a mandate that gives the Bank the capability to look through current events. It seems as if he was trying to dispel the idea of no move at the upcoming meeting, with the inflationary environment very different to what was seen at the time of the ’11 earthquake (which triggered a 50bp cut from the RBNZ).

- PPI data headlines tomorrow's local docket.

FOREX: Moves In G-10 Limited, US Cash Markets Closed

Moves across G-10 have been limited on Monday, U.S. markets are closed due to the observance of the Presidents Day holiday impacting wider liquidity. USD was firmer in early trade, heightened geopolitical tensions (centred on Sino-U.S. relations and the latest round of North Korean missile launches) boosted the greenback however there was little follow through.

- AUD is the strongest performer in G-10 space at the margins. AUD/USD is ~0.2% firmer, last printing at $0.6890/95 having found resistance at $0.69 this afternoon. Firmer Iron Ore and Copper are aiding the AUD at the margins. AUD/NZD firmed, printing its highest level since November.

- NZD/USD prints at $0.6240/45, little changed from opening levels. Found support below $0.6330, before firming to session highs as Finance Minister Robertson noted that the RBNZ needs to combat inflation and that the bank has a mandate which gives them the ability to look through current events. UBS became the first sell side name to adopt a base case of the RBNZ pausing its hiking cycle to assess the implications of Cyclone Gabrielle.

- Yen is little changed today, USD/JPY has been rangebound today. USD/JPY faced resistance above ¥134.50, before an offer with support coming in at ¥134.00. The local data calendar this week is headlined by Jibun Bank PMIs tomorrow and National CPI on Friday.

- EUR and GBP are little changed having observed narrow ranges today.

- Cross asset flows are muted, US Equity futures are little changed from opening levels as is BBDXY.

- In Europe today the docket is thin, Eurozone Consumer Confidence providing the only data of note. U.S. cash markets are closed for the observance of the Presidents Day holiday, wider liquidity will be impacted.

FX OPTIONS: Expiries for Feb20 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0610(E682mln), $1.0670-75(E510lmln), $1.0682-90(E705mln), $1.0700-15(E1.2bln)

- EUR/GBP: Gbp0.9000(E809mln)

ASIA FX: Weaker USD, But Mixed Degrees Of Follow Through

USD/Asia pairs are off from recent highs, but follow through today has been varied. This has been particularly the case for USD/CNH and USD/KRW (1 month). Baht has been a stronger performer at the other end of the spectrum. Still to come is Taiwan export orders. Tomorrow, South Korea consumer confidence and the first 20-days of trade figures for Feb are due.

- USD/CNH got above 6.8800 in early trade but is now back to the 6.8700 level. Onshore equities are higher amid growth optimism, although the authorities have reportedly told banks to curtail lending following the bumper results in Jan. As expected, the 5yr and 1yr LPRs were left unchanged.

- 1 month USD/KRW drifted lower but hasn't seen much follow through, last around 1293, so only slightly down on NY closing levels from the end of last week. Onshore equities are around flat, while the North Korean missile tests haven't impacted asset market sentiment.

- Spot USD/TWD is back below 30.40, so off recent highs. Coming up is export order data. The market expects a -24.05 y/y print. US-China tensions could remain in focus, as various visits take place this week and potential for a US-Taiwan bilateral trade agreement to be signed sooner than expected.

- USD/HKD has fallen 0.20% to sub the 7.8300 level before support kicked in. This is the firmest HKD move since late lats year and reflects the liquidity drain from last week as the HKMA defended the weak side of the peg (7.8500). Short terms HK rates have shot higher today.

- The RBI is said, link here, to have sold USD via NDF's to prevent USD/INR from weakening past 83 handle on Friday. FX reserves data up to Feb 10, showed reserves trending back lower (back under $567bn), although part of this will reflect the impact of firmer USD levels on valuations. USD/INR has softened in early trade, down ~0.1%, last printing at 82.70/75. This is line with broader USD trends in the region.

- USD/THB is up slightly from session lows, last around 34.36 (-0.70% for the session). The pair got close to the 100-day EMA on Friday (34.66/67), while the 50-day EMA sits near 34.025. The baht is the best performer within the Asian FX space so far today, although part of this is catch up with the weaker USD trend post Friday's onshore close. The USD/THB RSI got close to 70 on Friday (moves above this level on the RSI are considered overbought conditions), so that may have encouraged some profit taking flows in long USD/THB positions.

EQUITIES: China Outperforms, NZ Slumps

Regional equities are mixed to start the week. China bourses are the main story from a positive standpoint, with most other major indices close to flat. NZ stocks were a notable underperformer, down over 2%, as the country continues to assess the impact of Cyclone Gabrielle. US futures started the session off weaker, but are now back close to flat. The President's Day holiday in US markets today could also be impacting liquidity.

- The CSI is up over 1.30% at this stage. Early reports pointed to better higher frequency activity indicators in Feb, such as rail traffic. Goldman Sachs also put out a bullish China stock note. A Reuters report that banks should curtail lending, after record lending in Jan, didn't appear to impact market sentiment in a negative way.

- The China moves have seen positive spill over to Hong Kong, where the HSI is up around 0.50% at this stage.

- The Kospi was firmer in early trade, with little impact from fresh missile tests by North Korea. However, sentiment has softened this afternoon, the index back to -0.1% for the session. Japan's Nikkei 225 is around flat at this stage, while Taiex is +0.45%.

- NZ stocks fell by more than 2%. Cyclone Gabrielle is expected to have meaningful economic headwinds in the near term.

- In SEA, only Thai stocks are firmer at this stage.

GOLD: Bullion Slightly Higher, Watch Fed Events Later In Week

Gold prices rose 0.3% on Friday to be up on the week and during APAC trading today they’re stable at around $1844.55/oz (+0.25%), close to the intraday high after a low of $1837.38, despite geopolitical tensions related to North Korea. The USD is also flat.

- Bullion is currently in a bear trend and in a corrective cycle. It remains below its 50-day simple moving average.

- The US is closed today for the President’s holiday. There is euro area preliminary consumer confidence for February later. Importantly for gold, the FOMC minutes are published Wednesday and there are Fed speakers over the rest of the week. Preliminary February PMIs and US January consumer spending are also scheduled.

OIL: Crude Recovers Moderately On Optimism Re China Demand

Oil prices are up during today’s APAC trading after declining sharply on Friday to be lower on the week. Crude is moderately higher today with WTI up 0.6% to $76.80/bbl and Brent up 0.6% to $83.55. Chinese demand hopes have been driving the market today.

- WTI and Brent are back above the February 9 lows of $76.52 and $83.05 respectively. Today WTI reached a low of $76.12 followed by a high of $76.85 and Brent a low of $82.73 and high of $83.64. Brent is above its 50-day simple moving average, whereas WTI is below.

- Demand fears came to the fore again late last week with rising US stocks and hawkish Fed comments but optimism re China continues. Data showed that air travel is rising robustly with the top 3 airlines at 70% capacity.

- The US is looking to introduce new export controls and sanctions on Russia, focussed on energy, defence, financial institutions and certain people, according to Bloomberg, as the first year anniversary of Russia’s invasion of Ukraine approaches.

- The US is closed today for the President’s holiday. There is euro area preliminary consumer confidence for February later. The FOMC minutes are published Wednesday and there are Fed speakers over the rest of the week. Preliminary February PMIs and US January consumer spending are also scheduled this week.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 20/02/2023 | 0700/0800 | *** |  | SE | Inflation report |

| 20/02/2023 | 1000/1100 | ** |  | EU | Construction Production |

| 20/02/2023 | 1500/1600 | ** | | EU | Consumer Confidence Indicator (p) |

| 21/02/2023 | 2200/0900 | *** |  | AU | Judo Bank Flash Australia PMI |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.