Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- NZD and local NZ rates fell sharply post the RBNZ outcome. It was on hold as expected, but the main change seems to be a more neutral tone to the meeting assessment with November’s more hawkish elements removed.

- The USD is higher against NZD and AUD, but also the rest of the G10 and Asian FX. Regional equity sentiment has mostly been softer. Easing housing restrictions, announced in the Hong Kong budget, haven't been enough to lift the aggregate HSI.

- Finally, Treasury futures have crept higher over the day, although we remain well within Tuesday ranges while yields are 0-2bps lower across the curve.

- Looking ahead, Fed’s Bostic, Collins, Williams and BoE’s Mann speak. US Q4 GDP revisions are released as well as January inventories and trade balance. The European Commission February survey also prints.

MARKETS

US TSYS: Treasuries Steady, Remain Rangebound Ahead of GDP & PCE Data Later

TYH4 is currently trading at 109-21, up + 04 from New York closing levels

Treasury futures have crept higher over the day, although we remain well within Tuesday ranges while yields are 0-2bps lower across the curve.

- Mar'24 10Y futures remain in a tight range in Asia trading 109-23 high vs 109-17+ low, we trade just off the highs at 109-21. Initial supports holds at 109-17, (50.0% of the Oct - Dec bull cycle). A clear break of this retracement would strengthen the bearish condition and signal scope for an extension towards 108-19+, the 61.8% Fibonacci level. On the upside, initial firm resistance is seen at 110-24+, the 50-day EMA.

- Yield 0-2bps lower today with the 2Y yield is -1bp lower at 4.674%, the 10Y yield is -1.2bps lower at 4.291%, while the 2y10y is +0.049 at -39.362.

- Earlier, House Speaker Mike Johnson offered to delay Funding Deadlines (Punchbowl)

- Looking ahead, Wednesday data calendar includes GDP, PCE, Wholesale/Retail Inv, Fed Speak.

JGBS: Futures Holding Weaker, Heavy Local Calendar Tomorrow

JGB futures remain weaker, -7 compared to settlement levels, after dealing in a relatively narrow range in today’s Tokyo session.

- There hasn’t been much in the way of domestic drivers to flag, with Leading & Coincident Indices due later today.

- (Bloomberg) “I would expect the BoJ to end the negative rate in April, but cannot deny the possibility of that to happen in March,” says Inadome, a senior strategist at Sumitomo Mitsui Trust Asset Management. (See link)

- Today’s BoJ Rinban operations showed positive spreads, but lower offer cover ratios across the 5-10-, 10-25- and 25-year+ buckets. On balance, the results are consistent with the mildly weaker open to the Tokyo afternoon session.

- Cash US tsys are dealing flat to 1bp richer in today's Asia-Pac session, with newsflow light.

- The cash JGB curve has bear-steepened, with yields flat to 3bps higher. The benchmark 10-year yield is 0.5bps higher at 0.698% versus the Nov-Dec rally low of 0.555% and the February high of 0.770%.

- The swaps curve has also bear-steepened, with rates flat to 3bps higher. Swap spreads are tighter out to the 30-year.

- Tomorrow, the local calendar sees Retail Sales, International Investment Flows, Industrial Production and Housing Starts data. The MoF also plans to sell Y2.9bn of 2-year JGBs.

AUSSIE BONDS: Cheaper On The Day But Slightly Richer After CPI Monthly Miss, Retail Sales Tomorrow

ACGBs (YM -1.0 & XM -3.5) have strengthened slightly since the release of CPI Monthly data.

- January CPI inflation printed below expectations holding steady at 3.4% y/y, with ex-volatile items & holiday travel dipping 0.1pp to 4.1% and the trimmed mean 0.2pp to 3.8%.

- The first month of the quarter doesn’t include updates for the services component.

- RBA Governor Bullock noted recently that the help from falling goods inflation is probably behind us. January goods inflation was only 0.1pp lower at 3.1% y/y and non-tradeables 0.1pp higher at 0.9%.

- Cash ACGBs are flat to 3bps cheaper on the day, with the AU-US 10-year yield differential 2bps higher at -13bps.

- Swap rates are flat to 2bps higher on the day, with the 3s10s curve steeper.

- The bills strip is little changed, with pricing flat to -1.

- RBA-dated OIS pricing is little changed across meetings on the day. A cumulative 37bps of easing is priced by year-end.

- Tomorrow, the local calendar sees Retail Sales and Private Sector Credit for January and Private Capital Expenditure for Q4.

- TCorp issued A$600mn of its 1.75% 20 March 2034, 4.75% 20 February 2035 and 4.25% 20 February 2036 Benchmark bonds via Yieldbroker tender.

AUSTRALIAN DATA: Steady January Inflation As Goods Prices Stabilise Too

January CPI inflation printed below expectations holding steady at 3.4% y/y and ex volatile items & holiday travel dipped 0.1pp to 4.1% and the trimmed mean 0.2pp to 3.8%. The first month of the quarter doesn’t include updates for the services component but even so is unlikely to drive a shift in the RBA’s on hold stance or tightening bias.

- Headline inflation rose 0.4% m/m but 3-month momentum continued to ease and is around the mid-point of the band. The ABS said that the 3.4% y/y increase in prices was driven by housing (+4.6% y/y), food (+4.4%, fresh food was negative) and insurance (+8.2%) but holiday travel & accommodation fell 7.1% y/y.

- RBA Governor Bullock noted that the help from falling goods inflation is probably behind us and in January goods inflation was only 0.1pp lower at 3.1% y/y and non-tradeables 0.1pp higher at 0.9%.

- Electricity prices were brought down by rebates as they rose only 0.8% y/y and would’ve been 15.3% without them, according to the ABS.

- Rents rose 7.4% y/y in January as the market remains tight.

Source: MNI - Market News/ABS

RBNZ: Inflation Risks “More Balanced”, Forecast Changes Reflect History

The RBNZ left rates at 5.5% and apart from updates to history and their impact on the forecasts, there was little change in its outlook. The main change seems to be a more neutral tone to the meeting assessment with November’s more hawkish elements removed. The tone suggests that the RBNZ is happy with where rates are for now and is not looking to change them in either direction but policy will need to stay restrictive to return inflation to target.

- Inflation risks are now seen as “more balanced” whereas in November the MPC was concerned and “wary of ongoing inflationary pressures”, so there was no longer mention of rates having to “increase further”. But the RBNZ won’t “tolerate upside surprises” and is ready to act to higher inflation driven by geopolitical and climate developments, including higher shipping costs.

- The Q4 2023 OCR was 0.1pp lower than the November projection. Now that 5.5% for Q4 has been put into the forecast the subsequent quarters are 0.1pp lower too. So the peak rate at 5.6% instead of November’s 5.7% is technical. The RBNZ still expects rates to be on hold until Q2 2025 and 200bp of easing over 2025-2026.

- CPI inflation is still forecast to return to target in Q3 2024 with the midpoint in H2 2025. H1 2024 is now projected to be 0.5pp lower helped by Q4 2023 0.3pp lower than the RBNZ forecast in November. But end-2024 is unrevised at 2.5% and end-2025 at 2.0%.

- There were few changes to growth expectations and the unemployment rate was revised down through to Q3 2025 as employment growth is expected to be stronger. Q1 2024 labour costs were revised up 0.2pp to 3.8%.

NZGBS: Sharp Rally After RBNZ Signals It Is Happy With Where Rates Are

NZGBs closed sharply richer, with benchmark yields 9-16bps lower and the 2/10 curve steeper, after the RBNZ left the OCR at 5.50%, as widely expected.

- The main change from the RBNZ was the more neutral tone to the meeting assessment with November’s more hawkish elements removed. The tone suggested that the RBNZ is happy with where rates are for now and is not looking to change them in either direction, but policy will need to stay restrictive to return inflation to target.

- Swap rates are 8-16bps lower, with the 2s10s curve steeper.

- RBNZ dated OIS pricing is 5-21bps softer across meetings. A cumulative 52bps of easing is priced by year-end from an expected OCR peak of 5.54%.

- Before the decision, the market had attached a 29% chance of a 25bp hike at today’s meeting, with an anticipated terminal OCR of 5.65% (reflecting a 61% probability of a 25bp hike) by the May meeting.

- Tomorrow, the local calendar will see ANZ Business Confidence, along with RBNZ Governor Orr’s appearance in front of a Parliament Select Committee on MPS.

- Tomorrow, the NZ Treasury plans to sell NZ$300mn of the 0.25% May-28 bond, NZ$150mn of the 3.5% Apr-33 bond and NZ$50mn of the 1.75% May-41 bond.

NZ STIR: RBNZ Dated OIS Shunts Softer After RBNZ Signals OCR Unlikely To Go Higher

RBNZ dated OIS pricing closed 5-21bps softer across meetings after the RBNZ left the OCR at 5.50%, as widely expected.

- The main change from the RBNZ was the more neutral tone to the meeting assessment with November’s more hawkish elements removed.

- The tone suggested that the RBNZ is happy with where rates are for now and is not looking to change them in either direction, but policy will need to stay restrictive to return inflation to target.

- A cumulative 52bps of easing is priced by year-end from an expected OCR peak of 5.54%.

- Before the decision, the market had attached a 29% chance of a 25bp hike at today’s meeting, with an anticipated terminal OCR of 5.65% (reflecting a 61% probability of a 25bp hike) by the May meeting.

- It is also worth noting that in late December, the market had expected over 100bps of easing by year-end, stemming from an anticipated terminal OCR of 5.53%.

Figure 1: RBNZ Dated OIS Pricing (%)

Source: MNI – Market News / Bloomberg

FOREX: NZD Slumps Post RBNZ, USD Mostly Firmer Elsewhere

The main theme today has been NZD weakness, post the RBNZ's dovish hold (at least relative to expectations). NZD/USD fell to a low of 0.6103 in recent dealings, after tracking at 0.6175/80 in pre RBNZ dealings. We were last near 0.6110/15, around 1% weaker for the session.

- The main change from the RBNZ was the more neutral tone to the meeting assessment with November’s more hawkish elements removed. The tone suggested that the RBNZ is happy with where rates are for now. RBNZ dated OIS pricing closed 5-21bps softer across meetings. Pre RBNZ the market had attached a 29% chance of a 25bp hike at today’s meeting.

- For NZD/USD a clean break sub 0.6100 could see mid Feb lows near 0.6050 targeted.

- AUD/USD has been dragged lower by the NZD move and generally softer regional equity tone. AUDUSD is down 0.35% to 0.6520, close to session lows. Initial support is at 0.6496. AUDUSD fell briefly on the lower-than-expected January CPI outcome which came in unchanged at 3.4% y/y. But then fell sharply following the RBNZ decision. With kiwi underperforming, AUDNZD is 0.6% higher at 1.0665, slightly off session highs (1.0687).

- There are steadier trends elsewhere, albeit with the USD firmer. The BBDXY is up close to 0.1%, last near 1242.75. USD/JPY was sub 150.40 earlier, but we now track back at 150.60

- Looking ahead, Fed’s Bostic, Collins, Williams and BoE’s Mann speak. US Q4 GDP revisions are released as well as January inventories and trade balance. The European Commission February survey also prints.

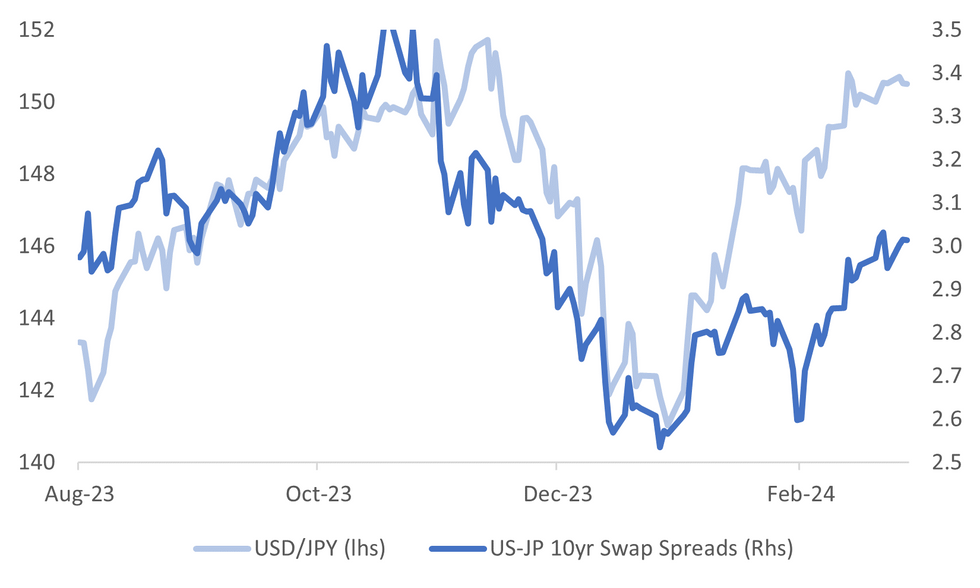

JPY: US Rate Moves Still Dominating Correlations With JPY

USD/JPY correlations against US and Japan yields still remain dominated by the US leg, at least per swap rates. In the past month USD/JPY spot correlations with US-JP 10yr swap differentials sit at 96%, while for 2yr differentials it sits slightly lower.

- Breaking this up into US and JP legs, shows that USD/JPY remains strongly positive correlated with US swap rate moves, both around 96% for the 2yr and 10yr.

- For Japan's 10yr swap rate the correlation has dipped slightly into negative territory, -14%, but is strongly positive for the 2yr, which is somewhat counter intuitive (i.e. higher Japan swap rates correlate with higher USD/JPY levels).

- This of course could change as we approach the next BoJ meeting in March (19th), but for now US rate trends are dominating.

- We did see some yen strength yesterday associated with the CPI beat, but this was not sustianed once US yields started to recover.

Fig 1: USD/JPY Versus US-JP 10yr Swap Rate Differential

Source: MNI - Market News/Bloomberg

ASIA EQUITIES: HK & China Equities Turn Lower, Country Garden Issued Wind-up

Hong Kong and China equities have opened mixed today, but have turned lower as the day has progressed. Hong Kong Budget and GDP were released earlier, with a focus on the property sector, while Macau gaming operator Galaxy Entertain missed their earnings forecast

- Equities markets are mixed, tech were up as much at 1.20% earlier only to have traded lower over the day to now be flat. Property again under-preforms on the back of Country Gardens Wind-up notice, with the mainland property index down 1.73%, while the HSI is down 0.20%. In China, indices have turned lower throughout the day early gains in growth stock have been completely reverse with the CSI100 up as much as 1.50% earlier to now trade 1.40% on the day, while the CSI300 trade down 0.10%

- China Northbound flows were +12.24b yuan on Monday, the forth highest daily inflow since July 2023, the other three have occurred in the past month.

- Major companies with earnings due out today include Baidu Inc and Sun Hung Kai Property. Baidu will be closely watched as earnings are expected to have grown by the slowest rate in a year, while investments in AI may also be a drag on results. Galaxy Entertainment the Macau Casino and Hotel company missed their earnings forecast earlier, although occupancy rates in their hotels remained near 100%.

- Earlier Chinese Property developer Country Garden was issued with a wind-up notice in a Hong Kong court with the first hearing expected to take place on May 17th, this follows from yesterday when China Vanke Co was reported to be in talks for a debt restructure.

- Hong Kong's GDP and Budget were released earlier with GDP coming in at 4.30% YoY inline with expectations, while QoQ was 0.4% vs 0.5% expected. The focused for the budget was on the easing of property curbs after house prices had fallen to the lowest in seven years, measures to curb housing demand have been cancelled with immediate effect. Other parts of the budget have been focused on improving tourism and hosting events with an additional HK$1.1B in funding, while there is also a focus on attracting foreign investment inflows.

- Looking ahead to Thursday, HK has Budget Balance and Money Supply data due, while the China calendar remains empty.

ASIA PAC EQUITIES: Equities Mostly Lower, SK Exception as Zuckerberg To Meet Samsung

Regional Asian Equities are mostly lower today, with South Korea the exception as it was announced Zuckerberg will visit Seoul to discusses AI with Samsung. Elsewhere investors have been looking to book in profit ahead of a busy few days for US data, and recent rallies in Asia equities leaving the BBG APAC Index down 0.32%.

- Japan equities are off lows from earlier to trade mixed, banks are weighing on the index today after yesterday pushing higher on the back of 2y JGBs hit their highest levels since 2011, the Topix Bank index is down 0.40%. Earlier Bank of Japan Executive Director Seiichi Shimizu says there hasn’t yet been enough certainty that the bank’s stable inflation goal will be achieved, and that the Bank will consider adjusting it's monetary easing once the price goal is in sight. Currently the Topix is flat, while the Nikkei 225 trades 0.20% lower.

- South Korean equities are higher today, after news broke that Mark Zuckerberg will visit Seoul to discuss AI technology with Samsung. The "Korea Discount" is nearing yearly lows again after recent policy announcements underwhelmed the market, while foreign equity inflows also continue to slow with the 5-day average is now at $40m, while the 20-day sits at $286m

- Taiwan Equities have followed wider markets lower today, the Philadelphia semiconductor index closed 0.20% lower on Tuesday which hasn't helped. Equity flows were negative on Tuesday and continue to slow, although still in positive territory on a rolling average as the 5-day average is now at $132m while the 20-day sits at $331m, currently the Taiex is 0.50% lower.

- Australian equities are closed flat today, after weakness in Financials and materials sectors outweighed gains in tech, energy and real estate. Earlier Australia had construction work done data out coming in just above expectations at 0.7% vs 0.6%, while CPI came in below expectations at 3.4% vs 3.6%,

- Elsewhere in SEA, NZ equities higher after the RBNZ kept rates on hold, up 0.60%, Indonesia recorded a fourth day of foreign equity outflows, although their equity is up 0.36% today, while Singapore & Malaysia equities are 0.30-0.50% lower.

Asian Equity Flows

- China equities saw their third largest northbound inflow for the year, and forth highest since July 2023, with little in the way of market headlines investors may be looking to get back into the market after two recently quiet days. The 5-day average is ticking higher sitting at 5.6b now, while the 20-day is at 2.93b yuan.

- South Korean equity flow momentum is slowing quickly, investors had looked to take profit prior to US data releases the second half on the week, while announcement around closing the "Korea discount" through the "Value-up" program have failed to live up to expectations. In economic data, SK saw an increase of 2% in tech exports largely due to higher sales to the US. The 5-day average is now $39.3m vs $171m a week prior, while the 20-day average now sits at $286m

- Taiwan equities saw a $446m outflow yesterday, as investors looked to book profits after opening the day at fresh all-time highs and ahead of US data later today and Thursday, similar to others in the region inflows are slowing with the 5-day average now $132m vs the 20-day at $331m

- Indonesian equities have marked their forth day of outflows, although markets have remained largely flat for that period, outflows look to be largely focused coming from the communication sector. The 5-day average now sits at -$41.5m vs the 20-day at +$39m

- Thailand Equities also saw consecutive days of outflows, economists have cut GDP exception to 2.90% vs 3.5% prior, while foreign arrivals rose 48% YoY. 5-day average of $30.2m still holds well above the 20-day average of just $5.8m

Table 1: EM Asia Equity Flows

| Yesterday | Past 5 Trading Days | 2024 To Date | |

| China (Yuan bn)* | 12.2 | 28.1 | 28.3 |

| South Korea (USDmn) | 14 | 197 | 7715 |

| Taiwan (USDmn) | -446 | 665 | 4802 |

| India (USDmn)** | -31 | 540 | -3245 |

| Indonesia (USDmn) | -75 | -208 | 1219 |

| Thailand (USDmn) | -64 | 153 | -688 |

| Malaysia (USDmn) ** | -14 | 138 | 472 |

| Philippines (USDmn) | 1 | 14.3 | 200 |

| Total (Ex China USDmn) | -614 | 1498 | 10477 |

| * Northbound Stock Connect Flows | |||

| ** Data Up To Feb 26 |

OIL: Crude Falls On US Stock Build, EIA Data Out Later

Crude gave up some of Tuesday’s gains early in APAC trading driven by another large US crude stock build but has recovered somewhat as geopolitical developments and the extension of OPEC cuts continue to put the market on edge. WTI is down 0.4% to $78.56/bbl, close to the intraday high, and Brent is -0.4% to $82.36/bbl. The USD is up 0.1%.

- Bloomberg reported a crude inventory build of 8.428mn barrels, according to people familiar with the API data, after +7.2mn the previous week. But product stocks continued to rundown with gasoline -3.3mn and distillate -500k. Refinery outages have resulted in crude builds and product drawdowns. Official EIA data is out later and includes refining capacity utilisation.

- The UK Navy reported a rocket exploded 3-5NM from a vessel but it is safe and will continue to its next port. The US has hit 230 targets to date in Yemen to contain attacks on Red Sea shipping. The Iran-backed Houthis have said they will only reconsider striking vessels once Israel ceases its “aggression” in Gaza. So, it seems that problems for shipping in the area are likely to continue.

- Later the Fed’s Bostic, Collins, Williams and BoE’s Mann speak. US Q4 GDP revisions are released as well as January inventories and trade balance. The European Commission February survey also prints.

GOLD: Steady Ahead Of US PCE On Thursday

Gold is steady in the Asia-Pac session, after closing little changed at $2030.48 on Tuesday.

- There has been very little movement in precious metals over the past 24 hours in line with the narrow ranges for the USD index as market participants await US PCE inflation on Thursday. The core PCE price index is expected to show a rise.

- For a market that still has an aggressive easing cycle priced despite the recent paring of easing expectations, participants will be particularly wary of any upside surprise from the PCE data.

- The Federal Reserve has specified that bringing inflation back toward its 2% target is necessary before it will start to cut borrowing costs.

- The swap market assigns around a 50% chance of a June rate cut, with little likelihood of any move before then. Lower rates are typically positive for bullion, which doesn’t offer any interest.

HONG KONG: Budget Focuses On Reviving Housing Market

Hong Kong's annual budget presentation is underway, with much of the market focus on the easing of property curbs.

- Finance Secretary Paul Chan stated that with immediate effect, measures to curb housing demand would be cancelled (BBG). This includes stamp duty, which went further than some in the market expected. This applies across local residents and offshore buyers as well.

- Special stamp duty, buyers' stamp duty and new residential stamp duty will no longer need to be paid for residential property transactions (per BBG).

- We will also hear from the HKMA later today on property lending adjustments.

- All of these steps are designed to aid the ailing Hong Kong housing market.

- There has been an equity market response. The HSI pared losses of as much as 1%, to now back close to flat. The Hang Seng properties index is now up around 1.8%.

- Other parts of the budget are focused on improving tourism and hosting events, while also focusing on foreign investment inflows.

- In terms of the economic outlook. Growth is expected at 2.5-3.5% for 2024, against a 3.2% rise last year. For 2025-2028 economic growth is expected to average 3.2%.

ASIA FX: USD/Asia Pairs Push Higher, THB & Won Underperform

USD/Asia pairs are higher across the board, albeit to varying degrees. A generally weaker regional equity tone, coupled with higher USD levels against the majors (particularly versus NZD post the RBNZ )are the factors aiding USD strength. THB, KRW and IDR are the weakest performers, while CNH and MYR are showing steadier trends. Tomorrow, we have Thailand IP and current account reads. Taiwan IP and Q4 GDP is also out, along with Indian GDP figures as well.

- USD/CNH has mostly crept higher during the session. The pair was last near 7.2170, close to Feb 20 highs. Local equity sentiment has been volatile but markets have struggled for positive territory. Spot USD/CNY remains wedged under 7.2000, which appears to be a short term line in the sand ahead of the 'Two Sessions' in early March.

- 1 month USD/KRW has mostly firmed higher, but has remained within Feb ranges. The 1 month NDF is in the 1333/34 range currently, around 0.20% weaker in won terms. Onshore equities have bucked the softer trend elsewhere, the Kospi up 0.75% at this stage. Meta head Mark Zuckerberg will visit Seoul to discusses AI with Samsung, is likely aiding equity sentiment but there has been little positive spill over to the won.

- USD/THB has spent much of the session on the front foot, the pair last near 36.00, around 0.5% weaker for the session so far. The pair has not been able to maintain moves above this level in Feb to date. Baht volatility remains more elevated compared to the rest of the region. Local Thailand stocks are weaker today (-0.6%). Offshore investors also sold local equities yesterday.

- USD/IDR spot has crept higher, last near 15675, which is close to recent highs, but still comfortably below earlier Feb highs close to 15800. Regional equity losses, coupled with a weaker portfolio backdrop are likely driving some caution in IDR, albeit within contained ranges.

- Spot USD/MYR sits a touch above earlier lows, last near 4.7615. This is close to late Tuesday lows for the pair. We were up close to 0.35% in MYR terms for yesterday's session, which came post the central bank's verbal rhetoric that the ringgit should be trading at stronger levels. The recent move lower now sees us challenging the 20-day EMA. We haven't spent time below this support level since the early stages of Jan this year.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 28/02/2024 | 0700/0800 | ** |  | SE | PPI |

| 28/02/2024 | 0700/1500 | ** |  | CN | MNI China Liquidity Index (CLI) |

| 28/02/2024 | 0900/1000 | ** |  | IT | ISTAT Consumer Confidence |

| 28/02/2024 | 0900/1000 | ** | | IT | ISTAT Business Confidence |

| 28/02/2024 | 1000/1100 | ** |  | EU | EZ Economic Sentiment Indicator |

| 28/02/2024 | 1000/1100 | * | | EU | Consumer Confidence, Industrial Sentiment |

| 28/02/2024 | 1100/1200 | | EU | ECB's Lagarde and Cipollone in G20 and CB Governors meeting | |

| 28/02/2024 | 1200/0700 | ** |  | US | MBA Weekly Applications Index |

| 28/02/2024 | 1330/0830 | * |  | CA | Current account |

| 28/02/2024 | 1330/0830 | * | | CA | Payroll employment |

| 28/02/2024 | 1330/0830 | *** | | US | GDP |

| 28/02/2024 | 1330/0830 | ** | | US | Advance Trade, Advance Business Inventories |

| 28/02/2024 | 1530/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 28/02/2024 | 1530/1530 |  | UK | BOE's Mann at FT future forum event 'The economic outlook..' | |

| 28/02/2024 | 1700/1200 | | US | Atlanta Fed's Raphael Bostic | |

| 28/02/2024 | 1715/1215 | | US | Boston Fed's Susan Collins | |

| 28/02/2024 | 1745/1245 | | US | New York Fed's John Williams | |

| 29/02/2024 | 2350/0850 | * |  | JP | Retail sales (p) |

| 29/02/2024 | 2350/0850 | ** | | JP | Industrial production |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.