Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Cash JGBs are richer beyond the 1-year, with the futures-linked 7-year leading (yield is 2.7bps lower). Q4 GDP data, which printed weaker than expected and signaled a technical recession, aided sentiment in the space. Yen fell modestly but reversed losses, as lower US yields dominated. US cash yields are 1-3bps richer across the curve, as the bear flattening theme continues from the US session.

- In Australia, the January labour data came in weaker-than-expected and showed the more convincing signs that the labour market is easing, but the ABS has some holiday-related caveats. RBA-dated OIS pricing is 4-11bps softer for meetings beyond May, with a cumulative 38bps of easing priced by year-end.

- In Indonesia, Defence minister Prabowo has declared victory in Indonesia’s election. Polls leading up to the vote had him as the likely winner and that he would surpass the required 50% level, so the result is not a surprise.

- Looking ahead, the Fed’s Waller speaks on the US dollar, ECB’s Lagarde and Lane and BoE’s Mann and Greene also speak. Retail sales, trade prices, Philly & Empire indices, jobless claims, IP and NAHB housing index all print in the US. UK Q4/December GDP, IP and trade are released.

MARKETS

US TSYS: Treasury Futures Rise On Low Volume Ahead of Busy US Data Calendar

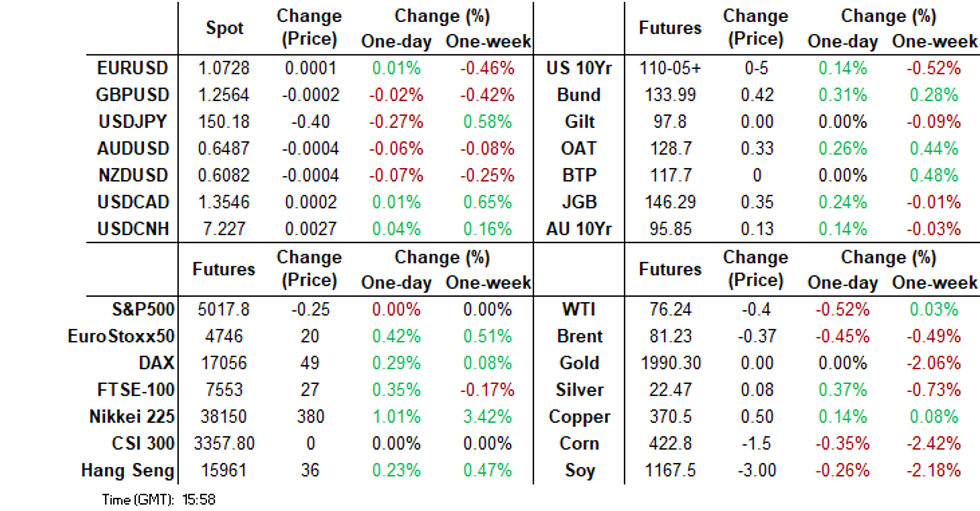

TYH4 is currently trading at 110-04+, up + 04 from New York closing levels.

Treasury futures are just off highs of the day as we head into the Asia lunch break, there has been very little in the way of notable market headlines.

- Mar'24, 10Y futures opened near lows of the day at 110-00+, and have been grinding higher throughout the Asia Session, hitting highs of 110-07+, as we break for Asia lunch we trade just off the highs at 110-04+, while volumes still remain on the lower side.

- Key levels to watch heading into a busy US session for Data include initial support at 109-17 (50.0% of the Oct 19 - Dec 27 bull phase). A break below here could open up new yearly lows and a test of 109-05+ (lows of Nov 28). To the upside, initial resistance lies at 110-16 (the lows from Feb 9th), while a break above opens up a move to 111-06 (20-day EMA).

- Cash yields are 1-3bps richer across the curve, as the bear flattening theme continues from the US session. The 2Y yield is -1.0bp lower at 4.569%, while the 10Y yield is -2bp lower at 4.236%.

- Post the US Close, Fed's VC Barr discussed the economy and recent data, noting that January's data was stronger than expected. High-interest rates are dampening both sales and purchases of homes. However, he emphasized that the data is on a good path, but it is still too early to determine if there will be a soft landing.

- Later today weekly Claims, Retail Sales, Imp/Exp$, IP/Cap-U, TIC Flows are due out. While Fed speak includes Fed Gov Waller on the US$ international role at 13:15 ET, and Atlanta Fed Bostic on monetary policy (text, Q&A) later in the evening at 19:00 ET.

JGBS: Futures Holding Post-GDP Gains

In afternoon dealings, JGB futures remain sharply richer and close to session highs, +39 compared to settlement levels.

- Outside of the previously outlined Q4 GDP data, which printed weaker than expected and signalled a technical recession, the local calendar showed Industrial Production (Final) and Capacity Utilization data for December. IP was revised down to 1.4% m/m (-1.0% y/y) versus 1.8% and -0.7% prior. Meanwhile, Capu printed -0.1% versus +0.3% prior.

- At face value, today’s data should diminish BoJ prospects for a near-term shift away from NIRP (say at the March meeting).

- (DJ) Japan dropped a rank to become the world's fourth-largest economy after a weak end to 2023, as growth in tourism spending failed to offset sluggishness in domestic private consumption and capital spending. (See link)

- Cash JGBs are richer beyond the 1-year, with the futures-linked 7-year leading (yield is 2.7bps lower). The benchmark 10-year yield is 2.6bps lower at 0.727% versus yesterday’s high of 0.765%

- The swaps curve has bull-flattened, with rates 1-3bps lower. Swap spreads are mostly tighter across maturities.

- Tomorrow, the local calendar is relatively light, with Weekly International Investment Flows and the Tertiary Industry Index as the only releases. The MoF will also conduct an Auction for Enhanced-Liquidity 15.5-39-years.

AUSSIE BONDS: Sitting At The Session’s Best Levels After Jobs Data Miss

ACGBs (YM +11.0 & XM +12.5) have richened 7bps since January’s Employment Report disappointed with a jobs gain of just 481 versus expectations of +25k. The Unemployment Rate also rose to 4.1% versus 4.0% est. and 3.9% prior.

- The January labour data showed more convincing signs that the labour market is easing, but the ABS had some holiday-related caveats. To add to the generally softer tone of the report, hours worked fell 2.5% m/m to be up only 0.7% y/y, the lowest in 4 years ex-COVID.

- Accordingly, the data is likely to confirm that the RBA is on hold for now but services inflation will need to show significant moderation as it is delaying the target return.

- Meanwhile, Melbourne Institute Consumer Inflation Expectations for February printed at 4.5%. Expectations have been at 4.5% for the last 3 months.

- Cash ACGBs are 6-7bps richer after the data and 12bps richer on the day.

- The AU-US 10-year yield differential is 5bps lower at -9bps versus a pre-data level of -4bps.

- Swap rates are 10-12bps lower on the day.

- The bills strip has bull-flattened, with pricing +1 to +12.

- RBA-dated OIS pricing is 4-11bps softer for meetings beyond May, with a cumulative 38bps of easing priced by year-end.

- Tomorrow, the local calendar is empty.

AUSTRALIAN DATA: Labour Market Easing But Impacted By Summer Holidays

The January labour data came in weaker-than-expected and showed the more convincing signs that the labour market is easing, but the ABS has some holiday-related caveats. Employment grew 0.5k and the unemployment rate rose 0.15pp to 4.1%, the highest in two years and close to the RBA’s Q2 2024 forecast of 4.2%. This data is likely to confirm that the RBA is on hold for now but services inflation will need to show significant moderation as it is delaying the return to target.

- The increase in the unemployment rate was driven by a 22.3k increase in the number of unemployed in February as job creation couldn’t cover the 22.8k people who entered the labour force. The 12 month increase in unemployed was relatively stable though at +77.9k up from +77.1k in December.

- The unemployment rate was a low 4.1% coming in at 4.058%. The ABS also noted that January 2024 was impacted by a “higher-than-usual number of people” not employed saying they will start a job in the next 4 weeks as was the case in 2023 and this may be the start of a new seasonal trend. This makes the February data released on March 21 key to determining labour market strength.

Source: MNI - Market News/ABS

- Both full-time and part-time employment was soft with full-time jobs (FT) rising only 11.1k and part-time (PT) shrinking 10.6k. 3-month momentum deteriorated across the board but remains positive for the total and PT.

- Employment growth is now at 2.6% y/y down from 3.2% y/y in early Q4 and is now below both labour force (3.0%) and working age population growth (2.9%), implying unemployment may rise further.

- To add to the generally softer tone of the report, hours worked fell 2.5% m/m to be up only 0.7% y/y, the lowest in 4 years ex Covid, with FT down 2.9% m/m and -7.8% y/y, but this data was impacted by holiday leave.

Source: MNI - Market News/ABS

RBA: RBA In “Good Position” To Return Inflation To Target As Expected

RBA Governor Bullock has appeared before the Senate economics committee and few questions from senators were centred around monetary policy and the outlook for the economy. But she said that the RBA is in a “good position” to return inflation to target within a reasonable timeframe but there continue to be significant uncertainties.

- Bullock said that the central bank is watching growth and inflation developments overseas closely. She said that global inflation impacts Australia through import prices and so the significant decline seen in other countries has helped bring domestic goods prices down. But services inflation remains elevated and we’re seeing that here too and the central bank is watching this closely for any implications in Australia. She said that persistent services inflation is delaying the return to target.

- Risks that inflation expectations become unanchored remain the longer that inflation is above 3%.

- The inflation forecast difference between the RBA and Treasury is not material and Bullock reiterated that the further out a projection is the greater the uncertainty.

- The RBA expects rents to peak around 10% in the next quarter or two and Bullock emphasised that supply and demand are the fundamental issue around the cost of housing. There are signs that advertised rents have peaked.

- She reiterated that the November hike wasn’t a mistake as aggregate demand continued to exceed supply.

NZGBS: Closed On A Strong Note, RBNZ Gov. Orr Speaks Tomorrow

NZGBs concluded the trading day on a robust note, marked by a 13-14bp decrease in benchmark yields. US tsys have provided a favourable backdrop for the local session after yesterday’s rally and the extension of that strength in today's Asia-Pac session. Cash US tsys are 2-3bps richer across benchmarks.

- Moreover, the strength in local bonds was reinforced by two key factors: a more favourable-than-anticipated Operating Deficit for the Government and a decline in Net Migration.

- The positive momentum extended with support from ACGBs following disappointing Employment data, which bolstered buying interest.

- Additionally, strong demand was evident in the weekly NZGB supply, reflected in cover ratios ranging from 3.15x to 3.80x.

- Swap rates closed 8-14bps lower, with the implied short-end swap spread wider.

- RBNZ dated OIS pricing flat to 4bps softer across meetings. A cumulative 48bps of easing is priced by year-end.

- Tomorrow, the local calendar sees BusinessNZ Manufacturing PMI, along with a speech by RBNZ Governor Orr about “the changing drivers of inflation over the past couple of years and the shift from transitory to more stubborn underlying inflation” at the NZ Economics Forum.

FOREX: Lower US Yields Help Yen Shrug Off GDP Contraction

The BDDXY sits little changed for the first part of Thursday trade. We were last near 1247.8. Yen strength has been evident, particularly at the expense of AUD, although AUD/JPY is up from session lows.

- Yen shrugged off an earlier Q4 GDP miss, which left the country in a technical recession for the second half of last year. USD/JPY got to highs of 150.58 but we now sit back at 150.15 close to session lows.

- A further pull back in US yields, led by the back end (10yr -2bps to 4.23%) has aided the yen. US equity futures are little changed.

- AUD/USD was weighed down by weaker Jan jobs data, which showed the unemployment rate ticking higher to 4.1%. We got to 0.6478, but now sit at 0.6485, only marginally weaker for the session.

- NZD/USD has remained rangebound today, currently trading at down 0.04% to 0.6084. Heading into a busy US session for data, important levels to watch are, 0.6040 (lows from Feb 5th) a break below here could signal further weakness, potentially opening a move to 0.6000 (lows from Nov 22nd). Currently, the 20 and 50-day EMAs are positioned at 0.6115/6135.

- The AUD/NZD cross was supported on dips to 1.0650, the pair last near 1.0660.

- Looking ahead, the Fed’s Waller speaks on the US dollar, ECB’s Lagarde and Lane and BoE’s Mann and Greene also speak. Retail sales, trade prices, Philly & Empire indices, jobless claims, IP and NAHB housing index all print in the US. UK Q4/December GDP, IP and trade are released.

CHINA/HK EQUITIES: Hong Kong Equities Rebound, As Investors Bank On Equity Market Support

Hong Kong equities opened lower today, that was met with buyers as most Indices now trade higher for the day, investors taking the view China will look to deliver stronger measures to help repair investor confidence.

- Equities markets in Hong Kong opened lower today, however early jitters quickly evaporated to see indices trade higher. Investors are banking on China policy makers announcing further market positive policies over the coming week, as has been the case over the past few trading session any signs of market weakness have been quickly met with swift buying and support. The Hang Seng is 0.45% higher after down as much as 0.80% earlier, HS tech is up 0.65%, while the mainland property index trades 1.88% lower after being down as much as 3.50% earlier.

- In other China & Hong Kong equity news, Michael Burry, made famous from the movie "The Big Short", has been adding to his exposure to Chinese Tech stocks recently betting on a recovering, while China's state media have reported that hotel sales at major e-commerce platforms have surged more than 60% from a year earlier and finally, Chinese property developer Redsun received a wind-up notice in Hong Kong, in what is not unexpected news as their debt has been trading at about 1c since October.

ASIA PAC EQUITIES: Regional Asian Equities Higher, Taiwan Hits All-Time Highs

Regional Asian Equities are mostly higher today, with Taiwan outperforming post-break. There have been little in the way of market headlines today, apart from Indonesian Defence Minister Prabowo Subianto claiming victory in the presidential elections.

- Japan equities are higher today after tech and exporter names push higher as the weaker yen and falling yields benefit both sectors. The Nikkei 225, has hit 3 year highs relative to the Topix on the back of strong results and performance from the tech sector, while the Topix lags largely due to an under performance in banks stocks with links to US commercial real estate exposure. Earlier today, Japan Q4 GDP was released and was weaker than expected, with the economy now in a technical recession, annualized q/q GDP fell -0.4% versus a +1.1% forecast. Q3 was also revised lower, to -3.3% (from -2.9%). Currently the Nikkei 225 is 0.% higher, while the Topix is 0.10% higher.

- Taiwan equities surged to all-time highs on growing demand for AI tech. Taiwan Semiconductor Manufacturing Co (TSMC) leads, up 7.90% as January sales rise 7.9% YoY. Taiex trades 2.93% higher.

- South Korea equities slightly lower as individuals and foreign investors withdrew $149m from equities markets today. There has been little in the way market headlines, potential profit-locking due to SK equities' recent out-performance in Asia could be the catalyst. The Kospi is 0.20% lower today.

- Australia equities closed higher today up 0.77%, after the unemployment rate edged higher to 4.1% from 3.9% previously, highlighting the nations cooling labor markets and prompting bets of an earlier rate cut as traders bought forward bets of the first rate cut to September from November. Financials have led the move higher, while Wesfarmers earnings beat pushed their shares 4.67% higher.

- Elsewhere, NZ equities closed down 0.18%, Philippines equites climb higher ahead of BSP meeting later today, while Indonesia rises by 1.57% after Defence Minister Prabowo Subianto claims victory in the presidential elections.

OIL: Crude Continues Fall Following Large US Crude Stock Build, IEA Report Later

Oil prices have continued falling during the APAC session after declining around 1.5% on Wednesday following a large crude inventory build in the US. WTI is down 0.6% to $76.20/bbl, close to the intraday low. Brent is down 0.5% to $81.22. The USD index is little changed.

- The EIA reported a larger-than-expected 12.02mn barrel inventory build in the US but with refining capacity dropping 1.8pp to 80.6% gasoline stocks fell 3.66mn and distillate -1.92mn. Product destocking provided some support to prices.

- Market signals, such as timespreads and refining margins, are implying tighter supply, according to Bloomberg. The IEA monthly report with supply and demand projections is published today. Earlier this week its chief Birol said that markets should remain “comfortable” as output rises and demand eases.

- There is a swathe of US data which will be important for dollar moves and the Fed outlook with markets shifting to a “higher for longer” view, which impacts the energy consumption outlook.

- Later the Fed’s Waller speaks on the US dollar, ECB’s Lagarde and Lane and BoE’s Mann and Greene also speak. Retail sales, trade prices, Philly & Empire indices, jobless claims, IP and NAHB housing index all print in the US. UK Q4/December GDP, IP and trade are released.

GOLD: Holding Below $2000

Gold is steady in the Asia-Pac session, after closing unchanged at $1992.33 on Wednesday.

- Bullion saw little respite from a weaker USD and lower US Treasury yields after yesterday’s CPI-induced rout.

- US Treasuries recouped some of Tuesday’s post-CPI sell-off. US Treasuries bull-steepened, with yields 2-8bps lower. Comments from the Fed's Goolsbee, downward revisions to December PPI data, a rethink of the CPI data, and a lack of follow-through selling presented a buying opportunity for the bond bulls.

- Chicago Fed’s Goolsbee (’25 voter) stuck to his dovish guns: “As I always say, especially about inflation, one month is no months. Let’s not get amped up when you get one month of CPI that was higher than what you expected it to be.”

- US PPI data for December was revised down from -0.1% to -0.2%.

- Looking ahead, Thursday brings a heavy US data calendar with weekly Claims, Retail Sales, Imp/Exp, IP/Cap-U, and TIC Flows.

- Fed speak includes Fed Gov Waller on the USD's international role at 13:15 ET, and Atlanta Fed Bostic on monetary policy (text, Q&A) later at 19:00 ET.

PHILIPPINES: MNI BSP Preview - February 2024: No Change, Still Too Early For Rate Cuts

- The strong consensus, and our own firm bias, is for the BSP to remain on hold at today's policy meeting. Whilst the central bank and the government authorities will be pleased with the sharp trend down in inflation pressures through 2023, they will be mindful of the risks around the 2024 outlook, particularly with less favourable base effects.

- The offshore backdrop has also turned less dovish, with US developments generally pushing back the timing of the Fed cutting cycle. This is also likely to feed into the BSP thinking.

- Click to view the full preview here:

INDONESIA: Prabowo Next President, Rupiah Little Changed

Defence minister Prabowo has declared victory in Indonesia’s election. Polls leading up to the vote had him as the likely winner and that he would surpass the required 50% level, so the result is not a surprise. The count has to be confirmed by March 20 and Prabowo will take over as President on October 20. Then we will find out if he will stick to current President Jokowi’s policies, as he’s promised. He has been a controversial candidate and unpredictable in the past.

- 1-month USDIDR NDFs rose to 15624 on the election result but are currently lower at around 15570.

- While the official results will not be known for a while, survey companies were at polling stations and their “quick count” has been released, which was an accurate indicator in the past. It showed that Prabowo is likely to win with around 58% of the vote with Anies in second on 25% and Ganjar 17%.

- Having popular President Jokowi’s son Gibran as his running mate provided a lot of support to the former general but there was controversy over the dispensation over age. There have also been reports of irregularities during the campaign and on voting day.

- Jokowi and Ganjar’s party the PDI-P is ahead in the “quick count” for parliamentary seats. Followed by Golkar and Gerindra (Prabowo’s party).

INDONESIA DATA: Surplus Narrows As Exports Weaken

Indonesia’s January trade surplus narrowed to $2.0bn from $3.3bn as there was a sharp drop in exports growth of 8.1% y/y while imports rose moderately by 0.4%. The outcome was weaker than expected. Export weakness was driven by mining & others falling 23.5% y/y. Manufacturing shipments were also soft down 3.7% y/y while agriculture held up at +0.1% y/y. Consumer goods imports were strong rising 11% y/y signalling robust spending ahead and capital goods +10.2% pointing to strong capex in line with large infrastructure projects.

Indonesia exports vs imports y/y% 3m ma

Source: MNI - Market News/Refinitiv

ASIA FX: PHP Firms Ahead Of BSP Decision, IDR Edges Down Post The Election

USD/Asia pairs are mixed in the first part of Thursday trade. PHP has been an outperformer ahead of the BSP decision later (no change expected). USD/KRW has tracked recent ranges, amid mixed equity trends. USD/IDR 1 month is higher post the election result, with Defence Minister Prabowo claiming victory. Tomorrow, we have South Korea trade prices and unemployment on tap, Singapore exports and Malaysian Q4 GDP.

- 1 month USD/KRW has gravitated higher but remains within recent ranges. The pair is last near 1331 after getting near 1328 in NY trade on Wednesday. Onshore equities have struggled to make fresh gains today, while offshore investors have sold $147.3mn of local shares so far.

- Taiwan markets have returned from the LNY break, surging by around 3% amid continued tech optimism. USD/TWD 1 month has drifted a little higher though, last a t31.36, in line with a generally firmer USD tone in recent weeks. Spot sits 0.20% weaker in TWD terms, near 31.41 in recent trade.

- Defence minister Prabowo has declared victory in Indonesia’s election. Polls leading up to the vote had him as the likely winner and that he would surpass the required 50% level, so the result is not a surprise. 1 month USD/IDR has drifted higher, last near 15635, weaker by around 0.3%, but well within recent ranges. Comments from an advisor suggested the new government will fine tune energy subsidies. Fiscal discipline will be a focus point for investors. On the data front, Indonesia’s January trade surplus narrowed to $2.0bn from $3.3bn as there was a sharp drop in exports growth of 8.1% y/y while imports rose moderately by 0.4%. The outcome was weaker than expected.

- Spot USD/PHP tracks at 55.97 as the BSP decision comes into view. Post US CPI highs in the pair came in around 56.33. On the downside recent dips sub 56.00 haven't proven sustainable. Note the 200-day EMA is near 55.91. We don't expect the BSP to shift policy rates or meaningful change their outlook around staying restrictive long enough to ensure inflation returns to target.

- Baht remains an underperformer within the EM Asia FX space, off 5.5% year to date, with MYR the next worst at -3.9%. USD/THB sits below earlier highs, last close to 36.11. Earlier we got to 36.18, which was fresh highs back to early Nov last year (Nov 1 high was 36.335). Local asset trends in terms of sideways equities price action are not helping THB. Portfolio flows are negative this week for equities (-$78.5mn) and just positive for Feb to date. Bond outflows have been more prominent (-$551.8mn).

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 15/02/2024 | 0700/0700 | ** |  | UK | UK Monthly GDP |

| 15/02/2024 | 0700/0700 | ** | | UK | Trade Balance |

| 15/02/2024 | 0700/0700 | *** | | UK | GDP First Estimate |

| 15/02/2024 | 0700/0700 | ** | | UK | Index of Services |

| 15/02/2024 | 0700/0700 | *** | | UK | Index of Production |

| 15/02/2024 | 0700/0700 | ** | | UK | Output in the Construction Industry |

| 15/02/2024 | 0800/0900 | *** |  | ES | HICP (f) |

| 15/02/2024 | 0800/0900 |  | EU | ECB's Lagarde statement at ECON hearing | |

| 15/02/2024 | 1000/1100 | * | | EU | Trade Balance |

| 15/02/2024 | 1200/1300 | | EU | ECB's Lane seminar at Florence School | |

| 15/02/2024 | 1300/1300 | | UK | BOE's Greene fireside chat with Fitch Ratings | |

| 15/02/2024 | 1315/0815 | ** |  | CA | CMHC Housing Starts |

| 15/02/2024 | 1330/0830 | *** |  | US | Jobless Claims |

| 15/02/2024 | 1330/0830 | ** | | US | WASDE Weekly Import/Export |

| 15/02/2024 | 1330/0830 | ** | | CA | Monthly Survey of Manufacturing |

| 15/02/2024 | 1330/0830 | ** | | US | Import/Export Price Index |

| 15/02/2024 | 1330/0830 | *** | | US | Retail Sales |

| 15/02/2024 | 1330/0830 | ** | | US | Empire State Manufacturing Survey |

| 15/02/2024 | 1330/0830 | ** | | US | Philadelphia Fed Manufacturing Index |

| 15/02/2024 | 1350/1350 | | UK | BOE's Mann panellist at 40th NABE Conference | |

| 15/02/2024 | 1415/0915 | *** | | US | Industrial Production |

| 15/02/2024 | 1500/1000 | * | | US | Business Inventories |

| 15/02/2024 | 1500/1000 | ** | | US | NAHB Home Builder Index |

| 15/02/2024 | 1530/1030 | ** | | US | Natural Gas Stocks |

| 15/02/2024 | 1815/1315 | | US | Fed Governor Christopher Waller | |

| 15/02/2024 | 2100/1600 | ** | | US | TICS |

| 15/02/2024 | 0000/1900 | | US | Atlanta Fed's Raphael Bostic |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.