Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Japan's labor cash earnings printed weaker than expected for August. In real terms, earnings were -2.5% y/y. JGB futures remain in positive territory at 144.81, +14 compared to the settlement levels, after hitting a session high of 144.85 in morning trade. Yen has weakened as well.

- Still the latest insight from the MNI policy team from Tokyo suggests YCC and negative rates could be abandoned in the first half of 2024.

- Elsewhere, cash US tsys are dealing with little change across major benchmarks in the Asia-Pac session. Ranges have been modest ahead of US Non-Farm Payrolls data later today. The USD has ticked higher.

- Looking ahead, outside of nonfarm payrolls, German factory orders, Italian retail sales and the Canadian jobs report are also on the docket. Meanwhile, Fed's Waller is set to speak.

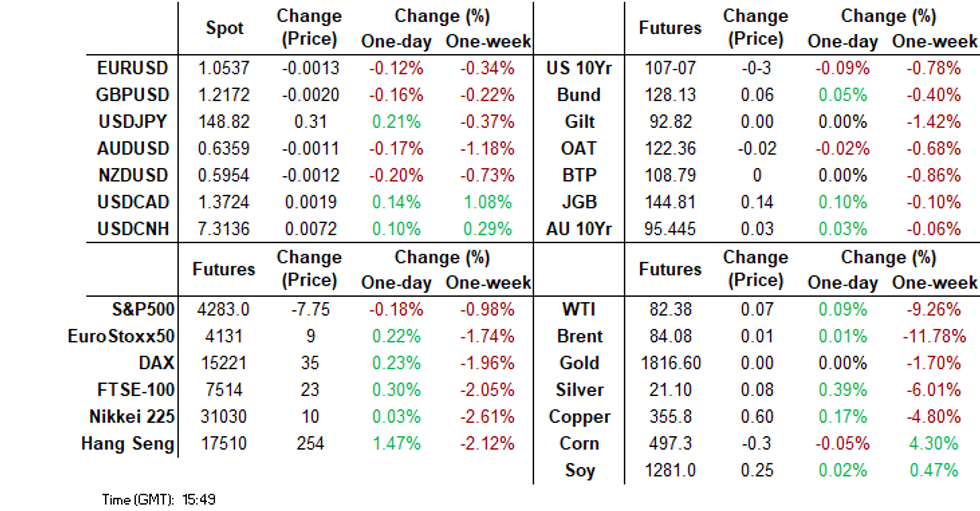

MARKETS

US DATA: MNI NFP Preview - AHE Seen Re-Accelerating, Troubling Fed Targe

- The Bloomberg median sees nonfarm payrolls rising 170k in September (primary dealer median 180k), after August’s 187k, in what was a small beat marred by large two-month downward revisions.

- While industry-specific blips in the data may occur, headline aggregates are not expected to be impacted by either the conclusion of the actors strike, or the walk-out of UAW workers currently impacting Ford, GM and Stellantis.

- Full preview including summary of sell-side views here: https://roar-assets-auto.rbl.ms/files/56086/USNFPO...

US TSYS: Treading Water In Asia-Pac Dealings Ahead Of Non-Farm Payrolls Later Today

TYZ3 is currently trading at 107-09+, -0-00+ from NY closing levels.

- Newsflow has been light so far in the Asia-Pac session.

- Cash tsys are dealing with little change across major benchmarks in the Asia-Pac session. Ranges have been modest ahead of US Non-Farm Payrolls data later today. Bloomberg consensus expects +170k in Septmber payrolls versus +187k prior. The unemployment rate is forecast to dip to 3.7% from 3.8% prior.

JGBS: Futures Holding Firmer, Tight Ranges Ahead Of Payrolls, Monday Holiday

JGB futures remain in positive territory at 144.81, +14 compared to the settlement levels, after hitting a session high of 144.85 in morning trade.

- There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined labour and real cash earnings, which printed weaker than expected.

- US tsys are dealing with little change across major benchmarks in the Asia-Pac session so far. Ranges have been modest ahead of US Non-Farm Payrolls data later today. Bloomberg consensus expects +170k versus +187k prior. The unemployment rate is forecast to dip to 3.7% from 3.8% prior. (See MNI’s US NFP preview here)

- Cash JGBs are dealing mixed, with the belly of the curve outperforming. Yields are 2.1bps lower (7-year) to 1.2bps higher (40-year). The benchmark 10-year yield is 1.0bp lower at 0.802%, above BOJ's YCC soft limit of 0.50% but below its hard limit of 1.0%. It is also below the cycle high of 0.814% set yesterday.

- The swaps curve has bull-steepened out to the 7-year, with rates 0.4bps to 1.5bps lower. Beyond the 7-year, rates are 0.9bp to 1.4bps lower. Swap spreads are generally tighter across maturities.

- The JGB market is closed on Monday for the observance of Health-Sports Day.

JAPAN DATA: Labor Earnings Softer Than Expected, Household Spending Up From Lows

Japan's labor cash earnings printed weaker than expected for August. Household spending was better than forecast, but still remained negative in y/y terms.

- Nominal labor cash earnings were +1.1% y/y, versus +1.5% forecast and a revised 1.1% gain in July. In real terms, earnings were -2.5% y/y against a -2.1% forecast and revised -2.7% fall in July.

- Real earnings momentum is up off early 2023 lows (-4.1% y/y), but the trend doesn't suggest we are set to move back into positive territory. Japan PM Kishida told local unions yesterday that he will strive for sustainable wage gains.

- Spending momentum was better than expected, up from recent lows, but still comfortably away from the average 2022 pace.

AUSSIE BONDS: Richer, At Sydney Session Best Levels, US Payrolls The Focus

ACGBs (YM +4.0 & XM +2.0) are richer and sit at or near Sydney session highs. It has been a light day on the newsflow front, with the RBA’s Financial Stability Report as the highlight.

- (AFR) “A rising number of borrowers are on the brink of financial stress as higher interest payments exceed their incomes and deplete their savings, the Reserve Bank said.” (See link)

- US tsys are dealing with little change across major benchmarks in the Asia-Pac session so far. Ranges have been modest ahead of US Non-Farm Payrolls data later today. Bloomberg consensus expects +170k versus +187k prior. The unemployment rate is forecast to dip to 3.7% from 3.8% prior.

- The cash ACGB curve has bull-steepened, with yields 2-4bps lower. The AU-US 10-year yield differential is unchanged at -16bps.

- Swap rates are 4-5bps lower.

- Bills pricing is +2 to +4 across the strip.

- RBA-dated OIS pricing is 2-5bps softer across 2024 meetings.

- Next week, the local calendar sees Foreign Reserves on Monday, Westpac Consumer and NAB Business Confidence on Tuesday and CBA Household Spending on Wednesday. Also on Wednesday, RBA Assistant Governor (Financial Markets) Christopher Kent delivers a Bloomberg Address in Sydney.

- The AOFM plans to sell A$800m of 2.75% 2027 bond on Wednesday.

NZGBS: Slightly Richer, Narrow Ranges, Awaiting US Payrolls

NZGBs closed flat to 2bps richer, with the 2/10 curve steeper, after dealing within relatively narrow ranges. The local calendar was empty today, with Card Spending data on Tuesday as the next major release.

- NZ-US and NZ-AU 10-year yield differentials closed little changed. Nevertheless, At +80bp and +96bp respectively, the differentials remain close to their widest levels for the year.

- US tsys are dealing flat to slightly cheaper across major benchmarks in the Asia-Pac session so far. Ranges have been modest ahead of US Non-Farm Payrolls data later today. Bloomberg consensus expects +170k versus +187k prior. The unemployment rate is forecast to dip to 3.7% from 3.8% prior.

- The swaps curve has bull-steepened, with rates 2bps lower to flat.

- RBNZ dated OIS pricing is 1-5bps softer for meetings beyond November. Terminal OCR expectations sit at 5.74% (+24bps) for Apr’24.

FOREX: USD Ticks Higher, As the Market Awaits Non-Farm Payrolls

The dollar has ticked modestly higher, as the market awaits the non-farm payroll print later in the US time zone. The BBDXY last close to 1274.20, a touch above NY closing levels from Thursday.

- Cross asset signals have been fairly muted, with US yields back near flat, after rising modestly in the first part of trade. Upticks in oil have generally been sold by the market. It's a similar backdrop for US equity futures, which are close to flat for the major benchmarks.

- USD/JPY sits slightly higher, last near 148.75, close to session highs. Earlier data showed weaker than expected real wages growth, albeit with some offset from better than forecast household spending. Speculation continues on the next BoJ policy shift. The latest piece from the MNI policy team suggests YCC could be scraped by next April (see this link).

- AUD/USD has outperformed modestly, last near 0.6370. A better regional equity backdrop, led by HK has probably helped at the margins. The RBA Financial Stability Review focused on household stress under the higher interest rate burden, but didn't paint an alarming picture.

- NZD/USD was last near 0.596, down slightly, while EUR/USD is around 1.0540 in recent dealings.

- Looking ahead, outside of nonfarm payrolls, German factory orders, Italian retail sales and the Canadian jobs report are also on the docket. Meanwhile, Fed's Waller is set to speak.

EQUITIES: Hong Kong Markets Rebound Ahead Of China's Return On Monday

Most Asia Pac markets are firmer in Friday trade to date. Gains have been led by Hong Kong markets, with more modest gains seen elsewhere. Japan markets are more mixed. US futures have traded relatively tight ranges. Eminis were last near 4289, down slightly, while Nasdaq futures were flat. We do have the US Non-farm payroll print coming up later in the US time zone.

- The HSI is around +1.85% firmer, slightly down on session highs. Gains have been broad based, although liquidity has been quite low. However, there is optimism around the return of China markets next Monday.

- On balance, China data has been better than expected of late, which has seen some sell-side analysts upgrade growth projections. Anecdotes around strong China spending over this week's holiday period is also aiding sentiment. The HS China Enterprise index is up 1.90%.

- Japan stocks are mixed, the Topix is +0.15%, but the Nikkei 225 off -0.30%. Both the Kospi and Taiex are around 0.35% higher at this stage.

- Australia's ASX 200 is +0.50%, buoyed by the materials sector. The large miners are higher after headlines crossed that China's iron ore buying conglomerate (China Mineral Resource Group) is in talks with the companies over next year's supply.

- SEA markets are mostly higher, with Thailand stocks lagging modestly.

OIL: Consolidates Ahead Of NFP, Tracking Sharply Down For The Week

Oil prices have tracked relatively tight ranges in the first part of Friday trade. Brent last near $84.30, after a modest move higher to $84.63/bbl earlier.

- Support was evident in NY trade on dips sub $84/bbl during Thursday trade, but we haven't tested this support point again. At this stage, Brent is tracking 11.5% weaker for the week, with today's modest +0.30% gain on pairing these losses modestly.

- For WTI we got near $83/bbl in early trade, but we sit back at $82.55/bbl in latest dealings. The benchmark contract is -9% down for the week.

- There has been little in the way of fresh macro news on the oil front today. Broadly steady trends in the USD and US rates ahead of the up coming payrolls print, could be keeping trading interest light today.

- For Brent, a break sub $84/bbl could see late August lows near $82/bbl targeted.

GOLD: Steady Ahead Of US Payrolls

Gold is slightly higher in the Asia-Pac session, after closing little changed at $1820.30 on Thursday, as the market awaited US Non-Farm Payrolls later today. Bloomberg consensus expects +170k in September payrolls versus +187k prior. The unemployment rate is forecast to dip to 3.7% from 3.8% prior.

- US Treasuries finished the NY session with a twist-steepening, pivoting at the 20-year, with yields 4bps lower to 3bps higher. There was little selling pressure from another tight reading on jobless claims and a narrower trade deficit, though a dovish tone from the Fed's Daly provided some support.

- SF Fed President Daly said, "If we continue to see a cooling labour market and inflation heading back to our target, we can hold interest rates steady and let the effects of policy continue to work".

- According to MNI’s technicals team, the bearish theme in gold remains intact, with the metal trading just above this week’s low. The recent sell-off resulted in a break of support at $1901.1 and this was followed by a breach of $1884.9, the Aug 21 low. This confirmed a resumption of the downtrend that started in early May. The focus is on $1804.9, the Feb 28 low and a key support. On the upside, firm resistance is at $1884.3, the 20-day EMA.

RBI: Watching Pass Through From Higher Food Prices, Possible OMO Sales Weigh on Local Bonds

As widely expected by the consensus, the RBI left policy rates unchanged at the October policy meeting. The decision to keep the policy rate at 6.50% was unanimous, while 5 out 6 board members also agreed to maintain the policy bias as 'withdrawal of accommodation', which was also in line with the consensus.

- Elevated inflation remains the major risk in terms of the broader macro outlook. The central bank stands ready to address any shocks and will act as necessary. September inflation is expected to ease, but uncertainty remains around the food price outlook.

- Governor Das noted sustained food price gains could lead to broader inflation pressures. Still, the central bank kept it current financial year inflation forecast unchanged at 5.4%.

- Das spoke quite positively in terms of the growth backdrop, particularly in terms of capex. This was evident in terms of detail in Q2 GDP growth report. The current financial year GDP forecast was unchanged at 6.5%.

- There was some focus on liquidity. Das noted that excess liquidity can pose a risk to financial market stability and price stability as well. Das stated the central bank may consider OMO (open market operation) bond sales in the future to manage system liquidity.

- This latter point has seen local bond yields rise, the 10yr up +7bps to 7.29%. USD/INR is down slightly, last near 82.20.

ASIA FX: Dollar Dips Mostly Supported, MAS Policy Review Due Next Friday

USD/Asia have traded mixed in the first part of Friday trade. At the margin USD dips have been supported, as the majors have softened slightly in the G10 space, as the US non-farm payroll print comes into view. The main focus early next week is likely to be the return of China markets from the Golden Week holiday break.

- USD/CNH was softer in earlier trade, but saw little follow through despite higher Hong Kong equities. The pair is back above 7.3100 (earlier lows were at 7.3023). Equity sentiment was buoyed in HK ahead of China markets returning on Monday, with recent growth upgrades cited as one factor, while optimism around China holiday spend was also noted.

- 1 Month USD/KRW sits slightly higher, last near 1348, against earlier lows around 1343.50. FX reserves for September dipped, in line with valuation moves. Onshore equities are modestly higher, but this hasn't positively impacted FX sentiment today.

- USD/INR sits slightly lower, last near 83.25. Ranges have been tight as the RBI delivered an on hold expected. This was widely expected, although the RBI noted they may conduct OMO sales to maintain system liquidity. This has weighed on local bond markets.

- USD/PHP has moved lower during today's session. We got to 56.57, but sit slightly higher now, last near 56.61. We aren't too far recent lows, which come in close to 56.50. A break sub this level could see the market target late August lows near 56.10. On the topside, recent highs remain marked close to 57.00. Outside of broader USD softness/consolidation in recent sessions, the sharp pull back in oil prices has likely aided PHP. The Citi terms of trade proxy has firmed back to mid July levels, although we remain in negative territory and sub early June YTD highs.

- USD/SGD sits above 1.3680 in latest dealings, well within recent ranges. The SGD NEER is off late September highs (per Goldman Sach estimates). Note the MAS policy review will be released next Friday.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 06/10/2023 | 0545/0745 | ** |  | CH | Unemployment |

| 06/10/2023 | 0600/0800 | ** |  | DE | Manufacturing Orders |

| 06/10/2023 | 0645/0845 | * |  | FR | Foreign Trade |

| 06/10/2023 | 0800/1000 | * |  | IT | Retail Sales |

| 06/10/2023 | 1230/0830 | *** |  | CA | Labour Force Survey |

| 06/10/2023 | 1230/0830 | *** |  | US | Employment Report |

| 06/10/2023 | 1600/1200 | | US | Fed Governor Christopher Waller | |

| 06/10/2023 | 1900/1500 | * | | US | Consumer Credit |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.