Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Tuesday's flattening theme on the JGB curve spilled over into Wednesday trade, providing some light support for wider core global FI markets overnight.

- JPY found itself at the foot of the G10 FX table, while the Hang Seng outperformed regional equity benchmark peers on a bid in tech giant Alibaba.

- Central bank speak from both sides of the Atlantic & comments from U.S. Tsy Secretary Yellen provide the highlights of Wednesday's broader docket.

US TSYS: Marginally Richer In Asia

TYM3 deals at 114-20, 0-00+, with a 0-07+ range observed on volume of ~91k.

- Cash tsys sit ~1bp richer across the major benchmarks.

- A bid in JGBs spilled over into the wider space facilitating a recovery off session lows seeing tsys marginally richen. There was no outright fundamental driver for the move.

- Earlier in the session, Tsys were pressured as e-minis moved higher. There was a strong lead from Micron which gave a better forecast for the current quarter than expected, and a 14% rise in Alibaba yesterday in NY, on news of an overhaul that will see the company split into six business units. TU and TY both dealt below Tuesdays low.

- A TU(3,036 lots)/UXY(1,250 lots) block flattener was the highlight flow wise

- There is a thin calendar in Europe today, further out Pending Home Sales provides the main point of interest in an otherwise thin data calendar. Fed VC Barr appears before the House Financial Services Committee. We also have the latest 7 Year supply.

JGBS: Long End Leads The Bid As Curve Flattens

A flow-centric move in JGB futures was seen in early Tokyo afternoon trade, with a pull higher accelerating on a break of the morning high in the contract. We haven’t got much in the way of an outright fundamental explainer for the move, outside of average to low offer/cover ratios at today’s BoJ Rinban operations (covering 3- to 25-Year JGBs).

- JGB futures now sit +17 as we head into the last hour of trade, pulling back from best levels, continuing to operate comfortably within the recently observed range.

- Wider cash JGBs see 2-10bp of richening as the curve flattens, with the firm pricing at yesterday’s 40-Year JGB auction and Dai-Ichi Life’s intentions to repatriate funds into super-long JGBs (noted on Tuesday) likely legacy drivers in the super-long end. The wider curve has reversed the steepening impetus that was observed into yesterday’s 40-Year supply.

- Swap rates are 0.5-3bp lower across the curve, with swap spreads running wider as a result.

- Outgoing BoJ Governor Kuroda failed to move the needle when it came to his latest round of parliamentary comments.

- Meanwhile, newly installed BoJ Deputy Governor Uchida pointed to some degree of willingness to keep the market guessing when it came to future policy moves (similar to Governor-in-waiting Ueda), while stressing the importance of BoJ communication channels.

- Elsewhere, new Deputy Governor Himino pointed to the need to maintain ultra-loose policy settings to support the economy.

- 2-Year JGB supply and the weekly international security flow data headline Thursday’s light local docket.

AUSSIE BONDS: Off Extremes After CPI Data Miss

ACGBs sit slightly cheaper to slightly richer ahead of the bell (YM -1.0 & XM +0.5) but off season extremes. The market scaled back gains sparked by a weaker-than-expected CPI Monthly print for February (6.8% Y/Y versus 7.2% expected) in line with an initial weakening in U.S. Tsys in Asia-Pac trade. U.S. Tsys did however reverse course later in the season, assisting ACGBs to lift off their post-CPI cheaps.

- 3-year and 10-year cash benchmarks are flat.

- The AU-US 10-year yield differential is -6bp at -26bp.

- Swap rates are 1-2bp lower and EFPs slightly tighter.

- Bills strip pricing is -1 to -3bp led by the reds.

- The local calendar is light until Private Sector Credit (Feb) data on Friday.

- The market focus however is already likely tuned into the RBA rates decision next Tuesday given today’s data was the last of the releases flagged by RBA Governor Lowe as key inputs to decision in April.

- Based on market pricing, today’s CPI result, coupled with yesterday’s retail spending outcome, should be enough to offset the resilient business survey and strong jobs data and deliver a pause from the RBA. April meeting pricing attaches an 8% chance of a 25bp hike.

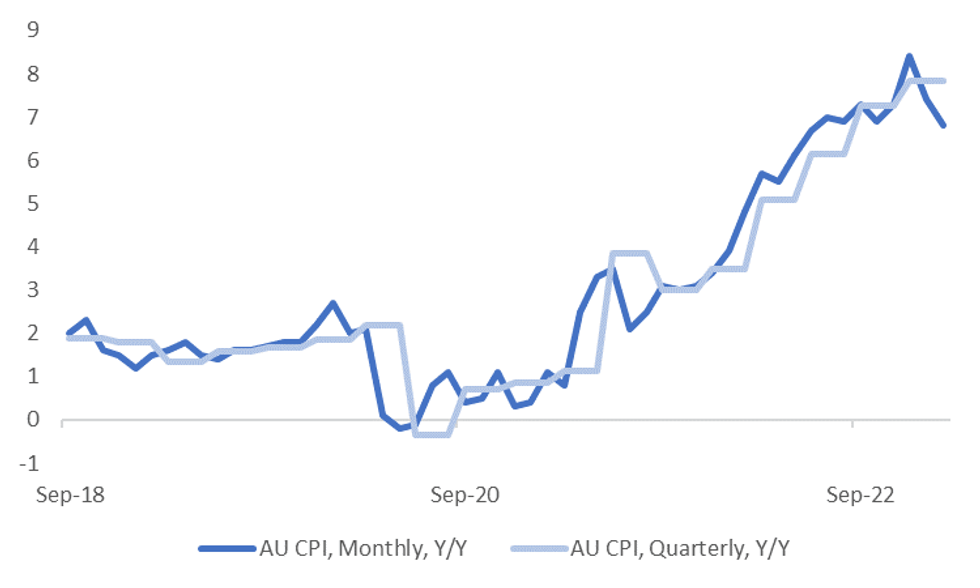

AUSTRALIA: CPI Data Shows Recent Pressure Points Easing

Feb Australian CPI saw a decent downside miss, printing at 6.8% y/y, versus 7.2% y/y forecast and 7.4% prior. Today's outcome is a decent down step from the recent peak of 8.4% recorded in December last year. At face value this it suggests we should see y/y momentum in the quarterly series ease, see the chart below.

- The ABS's measure which excludes volatile items (fruit and vegetables and automotive fuel) fell to 6.9% y/y from 7.5% in Dec. The ABS also noted that a measure excluding holiday and accommodation eased to 6.6% y/y from 6.8%.

- This travel related sub component, recreation, saw the biggest down step in y/y momentum to 6.4% y/y from 10.2%.

- Other sub categories were mixed, but recent inflation pressure points like food and housing recorded lower y/y momentum compared to January.

- Today's result, coupled with yesterday's as expected retail spending outcome, should be enough to offset the resilient business survey backdrop and strong jobs data in terms of next week's RBA decision. All in all, today's data supports the case for a pause next week.

Fig 1: AU CPI Y/Y Momentum Looks To Have Peaked

Source: MNI - Market News/Bloomberg

NZGBS: At Cheaps With Curve Flatter

NZGBs closed at session cheaps with yields 6-11bp higher and the 2/10 curve 5bp flatter. An e-mini-induced cheapening in U.S Tsys in Asia-Pac trade supported the move higher in NZGB yields. Cash 10-year benchmark slightly outperformed U.S. Tsys with the NZ/US yield differential narrowing 1bp to +57bp. The 10-year yield differential has traded in a 40-85bp range since mid-December.

- Swaps closed 3-11bp softer, implying a tighter long-end swap spread, with the 2s10s curve 8bp flatter.

- RBNZ dated OIS closed with pricing 1-10bp softer across meetings with November leading. Terminal rate expectations rose to 5.23% with 25bp of tightening priced for April.

- After a week-long hiatus, the local calendar sees the release tomorrow of ANZ Business Confidence (Mar) and Building Consents (Feb). The market will be focused on the pricing and cost components of the survey given that the February result continued to point to inflationary pressures. Building consents should confirm a trend softening due to a tightening in financial conditions. The data is likely to be cyclone impacted.

- With the global calendar relatively light until Friday when Euro Area CPI (Mar) and US PCE deflator (Feb) are released, the markets will be closely watching to see if global yields remain pressured by improving risk sentiment.

FOREX: Yen Pressured In Asia

The Yen is the weakest performer in the G-10 space on Wednesday.

- JPY has played some catch up with rising US Yields. USD/JPY prints at ¥131.60/70 ~0.6% firmer, resistance was seen at ¥131.76 high from Mar 27. If bulls break through ¥131.76, ¥133.00 high from Mar 22 is the next target.

- AUD is also pressured, the Feb CPI print in Australia was weaker than expectations. AUD/USD prints at $0.6695/0.6700, ~0.2% softer on the day. Downside support doesn't come in until $0.6625 low 24 March. AUD/NZD is also softer, and deals a touch below $1.07 handle.

- The firmer equity backdrop has helped NZD outperform today. NZD/USD is ~0.1% firmer.

- Elsewhere in G-10 the greenback is benefiting from the bid in USD/JPY which has spilled over into the wider G-10 space. EUR and GBP are both down ~0.1%.

- BBDXY is up ~0.2%, Hang Seng is up ~1.9% and E-minis are ~0.4% firmer.

- There is a thin calendar in Europe today, further out US Pending Home Sales provides the main point of interest in an otherwise thin data calendar.

FX OPTIONS: Expiries for Mar29 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0680-85(E1.0bln), $1.0780-00($2.5bln), $1.0850(E549mln), $1.1000-20(E1.3bln)

- USD/JPY: Y128.00-10($585mln), Y130.75($630mln), Y131.60-80($1.0bln)

- AUD/USD: $0.6650(A$681mln), $0.6800(A$566mln)

- USD/CNY: Cny6.8000($1.2bln), Cny6.9100($1.7bln)

ASIA FX: USD/Asia Pairs Mostly Higher

Most USD/Asia pairs are firmer, in line with higher USD index levels (BBDXY +0.15%). However, most of this is indicative of weaker yen levels, rather than broad based USD gains. Equity indices are mostly higher, but away from best levels. This, along with US yields moving off intra-day highs has helped curb USD gains. Still to come is the BoT decision, with +25bps expected. Tomorrow, South Korean manufacturing and non-manufacturing sentiment readings are due, in an otherwise quiet session.

- USD/CNH found selling interest above 6.8900 again, but is only modestly below this level currently (last 6.8870/80). Onshore equities are mixed, with not much positive follow through from surging Alibaba shares, which follows re-organization plans. US-China rhetoric remains elevated ahead of Taiwan President Tsai's expected stop over (March 29-30 in NY, then a week later in Los Angeles).

- 1 month USD/KRW is above NY closing from Tuesday, but remains sub 1300, last near 1297. Consumer sentiment rose to a 9 month high this month, while inflation expectations edged down ahead of CPI data next week. The South Korea authorities are looking at ways to boost domestic spending, including attractive more foreign tourists.

- Spot USD/TWD is a touch higher, last above 30.41. Local equities are only modestly higher (+0.15%), despite positive Micron (A US chipmaker) news after the Tuesday US close. The company revised higher expected sales for Q3. USD/TWD bulls will look for a move back through 30.50, while recent lows have been evident around the 30.30 region.

- USD/INR prints at 82.25/30, ~0.15% firmer in early trade. The Rupee is paring gains seen in the early part of the week, a low of 82.16 was seen yesterday. Bulls first look to break the 20-Day EMA (82.40) from here they target 83 handle. Bears target 200-Day EMA (80.93). A reminder that Indian markets are closed on Thursday for the observance of a national holiday.

- The SGD NEER (per Goldman Sachs estimates) is marginally firmer this morning, we remain well within recent ranges and below cycle highs seen last week. We sit ~0.5% off the upper end of the band. USD/SGD is ~0.1% firmer this morning, last printing at $1.3280/90. The pair is following the broader USD/Asia trend thus far. Bulls first look to break the 20-Day EMA ($1.3369) from here they can target the monthly high at $1.3576. The next downside target for bears is the 2023 low at $1.3032.

- USD/THB is within recent ranges ahead of the upcoming BoT decision later. The pair last tracked around the 34.30/35 region, slightly weaker in baht terms for the session, but in line with regional trends. The pair is wedged between the simple 50-day MA, which is close to 34.00, while on the topside, the 100-day MA is at 34.52. Some EMAs sit slightly higher, relative to current spot, the 50-day near 34.35, the 20-day near 34.39. If the BoT delivers a hike as expected, (19 out of 22 economists surveyed by Bloomberg look for a 25bps hike, the remainder forecast no change), the focus is likely to rest on BoT's language in the statement. Many don't expect a further hike at the next meeting in May.

SOUTH KOREA: Consumer Sentiment To 9 Month High, Inflation Expectations Down A Touch

Out a little early, South Korean consumer confidence rose to 92.0 for March, versus 90.2 prior. For the headline index this is the highest levels since June last year. Looking at the detail, aggregate spending plans eased a touch, but remain around levels from late 2022, so the BoK may take some comfort from this in terms of the consumer spending outlook. Domestic spending momentum will be needed to prevent a sharper economic growth slowdown, given external headwinds are weighing on export growth.

- In terms of inflation, expected levels eased down a touch to 3.9 from 4.0 previously. Again, this series is within recent ranges, but is arguing for a further modest softening in y/y momentum from a CPI standpoint, see the chart below. Note that March CPI prints on April 4.

- Expected wages also eased modestly, down to 112 (from 113 last month).

Fig 1: South Korean Consumer Inflation Expectations Versus Headline CPI Y/Y

Source: MNI - Market News/Bloomberg

EQUITIES: Little Spill Over From Alibaba Surge

Much of the focus today has been on firmer HK and China related tech shares, following the Alibaba re-organization news. The spill over to the rest of the region has been fairly limited though. US equity futures are firmer, with Micron's positive earnings guidance post the Tuesday close, helping at the margins (Eminis and Nasdaq futures are +0.40/+0.50% higher at this stage).

- The HSI sits close to 2% higher, but we are down from early session highs. We were 3% higher in early trade. The HS Tech index has followed a similar trajectory, last up around 2.70%.

- Alibaba is around 13% higher, as the company plans to split up into 6 groups, which could result in fresh IPOs.

- The HS China Enterprise index is around 2.1% higher. Mainland China stocks aren't showing a hugely positive trend, with the CSI 300 up around 0.25%, while the Shanghai Composite index is down slightly at this stage. Northbound stock connect flows are firmer though, +2.84bn yuan for the session so far.

- The Topix has seen some positive spill over from the Alibaba bounce, +0.75% at this stage. The Taiex is a touch higher (+0.15%), while the Kospi is around flat.

- SEA stocks are mostly positive, although gains are under 1% at this stage.

GOLD: Pulls Back Amid Firmer USD/Yields

Gold has moved off recent highs, the precious metal last near $1966.00, versus opening levels around $1973.50. We are off around 0.40% so far in the session, which is in line with the firmer USD trend against the majors.

- In terms of levels, Tuesday highs were around the $1975 region, while gains above $2000 haven't been sustained in recent weeks. On the downside, recent lows come in between $1940/$1950 from Monday/Tuesday of this week. The 20-day EMA is further back at $1928.50.

- Outside of USD drivers/firmer US yields, gold ETF holdings continue to track higher. Now back to early Feb levels. This comes despite lower risk aversion in other asset classes, particularly the equity space.

OIL: Holding Recent Gains

Brent crude is tracking higher in the first part of trade for Wednesday. We were last near $78.80/bbl, around +0.20% above closing levels from the NY session. Some resistance is evident above $79/bbl from a near term standpoint. Still, Brent is around 5% firmer for the week, although most of the gains came from Monday's session. We are now back above the 20-day EMA (just under $78.50/bbl). The 50-day EMA sits higher (near $81/bbl), while the 100-day is higher still (near $84/bbl). WTI is just above $73.50/bbl.

- For Brent, moves above the 100-day EMA have generally been selling points over recent months, so we may have to see a definitive break above this level, before the medium-term outlook turns more positive.

- Outside of the more positive risk backdrop, amid generally positive equity trends, supply side issues remain front and center. Focus is likely to rest with oil inventory data out in the US later today, which follows other data released on Tuesday, which showed a sharp drop in reported inventory levels.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 29/03/2023 | 0600/0800 | ** |  | SE | Retail Sales |

| 29/03/2023 | 0600/0800 | * |  | DE | GFK Consumer Climate |

| 29/03/2023 | 0600/1400 | ** |  | CN | MNI China Liquidity Suvey |

| 29/03/2023 | 0645/0845 | ** |  | FR | Consumer Sentiment |

| 29/03/2023 | 0700/0900 | ** | | SE | Economic Tendency Indicator |

| 29/03/2023 | 0830/0930 | ** |  | UK | BOE M4 |

| 29/03/2023 | 0830/0930 | ** | | UK | BOE Lending to Individuals |

| 29/03/2023 | 0930/1030 | | UK | Bank of England FPC Report/minutes | |

| 29/03/2023 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 29/03/2023 | 1400/1000 | ** | | US | NAR Pending Home Sales |

| 29/03/2023 | 1400/1000 | | US | US House Financial Services Hearing | |

| 29/03/2023 | 1400/1000 | | US | Treasury Secretary Janet Yellen | |

| 29/03/2023 | 1430/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 29/03/2023 | 1530/1130 | ** | | US | US Treasury Auction Result for 2 Year Floating Rate Note |

| 29/03/2023 | 1630/1230 |  | CA | BOC Deputy Gravelle speech "The market liquidity measures we took during COVID" | |

| 29/03/2023 | 1700/1300 | ** | | US | US Treasury Auction Result for 7 Year Note |

| 29/03/2023 | 1850/1950 | | UK | BOE Mann Panellist at NABE | |

| 29/03/2023 | 2045/2245 |  | EU | ECB Schnabel Panels NABE Conference |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.