Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- The softer USD has continued today, led USD/JPY in Asia Pac markets. USD/Asia levels are also lower, with fresh China property market support a positive, although property related shares have struggled to hold onto gains today. USD/CNH dipped sub 7.2000 before finding support.

- Cash US tsys sit ~1bp richer across the major benchmarks. Commodities are mostly higher, with iron ore rebounding from recent lows, although AUD/USD hasn't breached 0.6700.

- Tomorrow, markets have a 12% chance of a 25bp hike priced for tomorrow’s RBNZ policy meeting. However, it is important to note that terminal OCR expectations have shifted 10bp firmer since last week and currently sit at 5.75%.

- In Europe today we have the latest UK jobs data and the final print of German CPI. Further out NFIB Small Business Optimism crosses as does Fedspeak from St. Louis Fed President Bullard. We also have the latest 3-Year supply.

MARKETS

US TSYS: Marginally Richer In Asia

TYU3 deals at 111-08, +0-03+, a touch off the top of the 0-05 range on volume of ~76k.

- Cash tsys sit ~1bp richer across the major benchmarks.

- Tsys were marginally pressured in early dealing, participants perhaps using Monday's richening as an opportunity to close out long positions/add fresh shorts.

- A recovery off session loss was seen alongside pressure on the greenback, as an offer in USD/JPY spilled over into broad USD weakness.

- Block buyers in FV (1.5k lots) and UXY (1,737 lots) have also added a layer of support.

- Fedspeak from NY Fed President William's crossed, he noted that a recession is not in his forecast for the US economy. More here.

- In Europe today we have the latest UK jobs data and the final print of German CPI. Further out NFIB Small Business Optimism crosses as does Fedspeak from St. Louis Fed President Bullard. We also have the latest 3-Year supply.

STIR: BoC Expected To Hike, RBNZ Expected To Hold

Ahead of the BoC and RBNZ policy meetings tomorrow, all $-Bloc STIR markets have at least one 25bp hike cumulatively priced over the coming months.

- The Bloomberg survey shows 6 of 23 analysts looking for no change from the BoC this week, although we'd caution that three are from June, one of which is Goldman Sachs who we know have since called for a hike. Notably, there appears to be broad consensus that this could be the final hike, but data dependency could easily put pay to that.

- In contrast, Bloomberg consensus is unanimous in expecting a no-change outcome for the RBNZ after it steered the market in its May Monetary Policy Statement towards no further increases in the OCR would be required. A 13% chance of a 25bp hike is priced for tomorrow's policy meeting. However, it is important to note that terminal OCR expectations have shifted 10-15bp firmer since last week and currently sit just shy of 5.80%.

- RBA-dated OIS pricing attaches a 58% chance of a 25bp hike at the August meeting.

- July 26 FOMC pricing currently gives a 25bp hike a 93% chance with the implied change of +23bp to 5.305%.

Figure 1: $-Bloc STIR

Source: MNI – Market News / Bloomberg

JGBS: Futures Holding Richer, 5-Year Supply Sees Very Strong Demand

In the Tokyo afternoon session, JGB futures are holding firmer, +14bp compared to settlement levels, after today’s supply of 5-year bonds was very well-received. The auction's low price beat dealer expectations, while the cover ratio improved dramatically to 4.680x compared to 3.850x in the previous month's auction. Additionally, the tail decreased to its shortest since February.

- There haven't been many noteworthy domestic factors to highlight, except for the previously mentioned M2 and M2 money stock data, which are unlikely to have had a significant impact on the market. June preliminary machine tool orders are out later today.

- US tsys have extended the strength seen in the NY session in Asia-Pac trading. Cash US tsys are 1-2bp richer than NY closing levels across the benchmarks.

- Cash JGBs are dealing mixed in the Tokyo afternoon session with the belly of the curve outperforming. The benchmark 10-year yield is 0.5bp lower at 0.457%, below the BoJ's YCC limit of 0.50%. The 30-40-year zone is underperforming with yields 1.4-1.7bp cheaper.

- The 5-year benchmark is the outperformer with its yield dealing 2.0bp lower at 0.101%, after today’s supply.

- The swap curve twist steepens, pivoting at the 20-year. Swap spreads are tighter across the curve apart from the 7-year.

- Tomorrow the local calendar sees PPI (Jun) and Core Machine Orders (May) data.

AUSSIE BONDS: Tracking US Tsys Richer

ACGBS are dealing stronger (YM +9.0 & XM +9.5), just off Sydney session highs as US tsys extend the strength seen in the NY session in Asia-Pac trading. Cash US tsys are 1-2bp richer than NY closing levels across the benchmarks.

- There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined Westpac consumer sentiment and NAB business confidence data.

- Cash ACGBs are 9bp richer with the AU-US 10-year yield differential -1bp at +21bp.

- Swap rates are 9-11bp lower with the 3s10s curve steeper.

- The bills strip is richer with pricing +4 to +10, early reds leading.

- RBA-dated OIS pricing is 2-8bp softer across meetings. The market attaches a 54% chance of a 25bp hike at the August meeting.

- Tomorrow the local calendar's highlight is RBA Governor Lowe’s speech to the Economic Society of Australia in Brisbane, titled ‘The Reserve Bank Review and Monetary Policy”. Investors will be hoping to gain insights into the central bank's level of concern regarding inflation after the policy pause this month.

- Tomorrow the AOFM plans to sell A$700mn of the 2.25% 21 May 2028 bond.

AUSTRALIAN DATA: Consumer Sentiment Rises - But Remains Close To Recent Lows

The Westpac July consumer sentiment index rose 2.7% to 81.3. This moves us away from recent lows but sentiment has been stuck at fairly depressed levels since the middle part of 2022. Westpac attributes the July rise to lower inflation reads, rather the early July pause by the RBA.

- Westpac Chief Economist Bill Evans noted: "The key message is that sentiment is probably not going to stage a sustained lift from current deeply pessimistic levels until inflation is much lower and interest rates are firmly on hold.”

- Current conditions edged down to 70.5, but expectations rose to 88.5 (+4.5%m/m). The 1yr ahead economic outlook also improved to 81.4, +5.4% m/m.

- Time to buy a major household item also rose, up 3.1% m/m to 78.8, but this is still around historical lows.

- Unemployment expectations were close to steady, but are still 32% higher since the RBA tightening cycle began in May of last year.

- House price expectations firmed, lifting 1.8% 149.3.

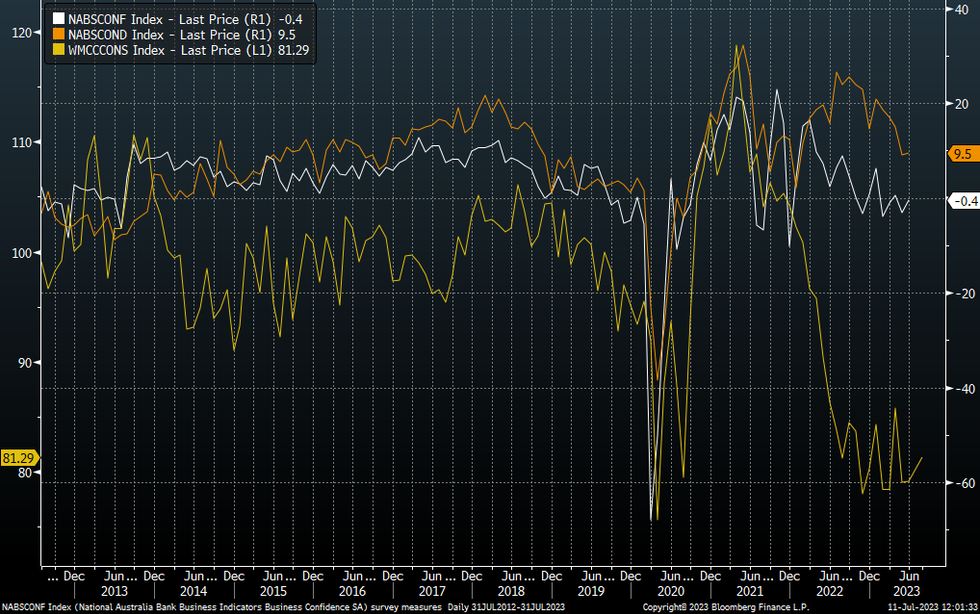

AUSTRALIAN DATA: Business Sentiment Held Up In July

Australia's NAB business survey for June painted a fairly resilient picture for the domestic economy. Business conditions were steady at +9, which is comfortably off mid 2022 highs of +27, but we well above previous trough points that signified more significant economic headwinds (typically comfortably below 0 on this index). Confidence rose as well to flat, from a revised -3 reading in May.

- The business sector continues to pain a more upbeat picture relative to consumer sentiment, see the chart below.

- In terms of the detail, the employment sub-index was unchanged at +5.

- The labour costs q/q term rose to 2.6%, versus 2.0% in May. We are below earlier 2023 highs of 2.7% though. Purchase costs in q/q terms were unchanged at 2.3%.

Fig 1: Business Sentiment Held Up In July

Source: MNI - Market News/Bloomberg

NZGBS: Closed At Bests, RBNZ Expected To Be On Hold Tomorrow

NZGBs ended the session on a positive trajectory, as benchmark yields witnessed a decline of 11-14bp, while the 2/10 curve steepened by 3bp. This movement aligns with the trend observed in US tsys, as their strength from the NY session extended into the Asia-Pac session. The NZ/US 10-year yield differential closed -2bp at +79bp.

- Swap rates are 11bp lower.

- Tomorrow the local calendar sees the release of Net Migration ahead of the RBNZ Policy Decision. In May the RBNZ hiked rates 25bp to be in line with its updated but unchanged Q2 2023 OCR forecast of 5.5%. This last hike gave the Committee confidence that it had done enough to contain inflation and with that, it shifted to a neutral stance.

- With the data since then generally showing slowing activity, survey measures of inflation gradually easing, and rates in line with the RBNZ forecast, The RBNZ is likely to be on hold for the first time since August 2021. See the MNI RBNZ Preview here.

- Markets have a 12% chance of a 25bp hike priced for tomorrow’s policy meeting. However, it is important to note that terminal OCR expectations have shifted 10bp firmer since last week and currently sit at 5.75%.

RBNZ: MNI RBNZ Preview - July 2023: Ready To Watch & Wait

NZ RATES: RBNZ Dated OIS Prices A No-Change Outcome Tomorrow

Today RBNZ dated OIS pricing is 1-6bp softer across meetings beyond July ahead of the RBNZ policy decision meeting tomorrow. See the MNI RBNZ Preview here.

- Bloomberg’s consensus is unanimous in expecting a no-change outcome after the RBNZ steered the market in its May Monetary Policy Statement that it expected that no further increases in the OCR would be required and that now is the time to “watch, worry and wait”.

- A 12% chance of a 25bp hike is priced for tomorrow’s policy meeting.

- However, it is important to note that terminal OCR expectations have shifted 10bp firmer since last week and currently sit at 5.75%.

Figure 1: RBNZ Dated OIS: Today Vs. Yesterday

EQUITIES: China's Real Estate Stocks Higher On Fresh Support Talk

Regional equity market sentiment is mostly positive today. We did have modest positive leads from US & EU markets during Monday trade. US futures are a touch higher (Eminis last near 4446), but the main focus has been on fresh China policy support/stimulus, particularly in the property segment.

- Onshore China media has been focused on further property market support after the authorities urged local financial institutions to extend credit support to the troubled developer sector. The MNI policy team notes that property market restrictions may be eased in H2 (most likely after the July Politburo meeting).

- Other focus points are on boosting business confidence and consumption, see this link for more details.

- The CSI 300 is 0.63% higher at the break, last near 3870 in index terms. The CSI 300 real estate sub index surged at the open but is now up only a modest 0.12%. A Bloomberg measure of real estate owners and developers is doing better at +1.29%. The HSI is +1.53% at the break, the tech sub-index +2.06%.

- Elsewhere, Japan stocks are struggling for positive traction. The Topix last down slightly, while the Nikkei 225 was around flat.

- The ASX 200 is up over 1.10% with banks and mining related names leading the move higher.

- The Kospi is +1.34% firmer, while the Taiex has rallied by a similar amount. In SEA most markets are higher, but gains are more modest at this stage.

FOREX: Yen Firmer In Asia

The Yen is the strongest performer in the G-10 space at the margins in Asia on Tuesday. USD/JPY has fallen ~0.3% and sits below the ¥141 handle.

- USD/JPY prints at ¥140.75/85, and is at its lowest level since mid-June. There was no obvious headline driver for the move with technical flows and a continuation of Monday's price action weighing. Support comes in at the 50-Day EMA (¥140.30).

- AUD/USD is ~0.2% firmer, reflecting the broader USD weakness seen in Asia. The pair still sits below the $0.67 handle, and resistance comes in at $0.6721. Business Conditions were steady in June, with Business confidence ticking higher to sit flat.

- Kiwi is a touch firmer, NZD/USD is up ~0.1%. Gains have been capped at the 200-Day EMA ($0.6223) which is emerging as a key level for bulls.

- Elsewhere in G-10 EUR and GBP are ~0.2% firmer. NOK is up ~0.3% however liquidity is generally poor in Asia.

- Cross asset wise; BBDXY is ~0.2% lower and US Tsy Yields are ~1bp softer across the curve.

- In Europe today we have UK jobs data and the final read of German CPI.

EQUITIES: China's Real Estate Stocks Higher On Fresh Support Talk

Regional equity market sentiment is mostly positive today. We did have modest positive leads from US & EU markets during Monday trade. US futures are a touch higher (Eminis last near 4446), but the main focus has been on fresh China policy support/stimulus, particularly in the property segment.

- Onshore China media has been focused on further property market support after the authorities urged local financial institutions to extend credit support to the troubled developer sector. The MNI policy team notes that property market restrictions may be eased in H2 (most likely after the July Politburo meeting).

- Other focus points are on boosting business confidence and consumption, see this link for more details.

- The CSI 300 is 0.63% higher at the break, last near 3870 in index terms. The CSI 300 real estate sub index surged at the open but is now up only a modest 0.12%. A Bloomberg measure of real estate owners and developers is doing better at +1.29%. The HSI is +1.53% at the break, the tech sub-index +2.06%.

- Elsewhere, Japan stocks are struggling for positive traction. The Topix last down slightly, while the Nikkei 225 was around flat.

- The ASX 200 is up over 1.10% with banks and mining related names leading the move higher.

- The Kospi is +1.34% firmer, while the Taiex has rallied by a similar amount. In SEA most markets are higher, but gains are more modest at this stage.

GOLD: Steady Ahead Of US CPI Data Tomorrow

Gold is slightly firmer in the Asia-Pac session, following a relatively unchanged closing on Monday. Traders are carefully assessing the support provided by declining US Treasury yields and a weaker dollar against expectations the Federal Reserve will pursue additional monetary tightening.

- US tsys finished near their best levels of the NY session, with benchmark yields 1-12bp lower, ahead of US CPI data later this week and the start of the US earnings season.

- US tsys received a boost thanks to the New York Fed's survey on inflation expectations, which showed a decrease in the one-year outlook for inflation. In June, the outlook fell to 3.83% from the previous month's 4.07%, marking the third consecutive decline and reaching its lowest level since April 2021.

- Less hawkish headlines from Fed Daly, Mester and Barr further supported the downward movement in yields. Barr expressed the belief that there is still "more work to do but close to the end," while Daly emphasised that risks are becoming less imbalanced, making decisions more challenging and reliant on additional data.

ASIA FX: Firmer Yen, China Property Support Talks Buoy Asian FX

USD/Asia pairs are lower across the board, aided by fresh China policy stimulus/support hopes and a broader pull back in USD sentiment, which has been led by USD/JPY. Regional equity sentiment is mostly positive as well. USD/CNH is back close to 7.2000, while spot USD/KRW is down 1%. THB and PHP have also rallied strongly, both up 0.80%. Tomorrow, we get South Korea unemployment and bank lending, while India CPI and IP figures are due, along with Malaysian IP. China aggregate credit figures are also still yet to print.

- USD/CNH has sunk more than 350pips from intra-day highs above 7.2360 to fresh lows sub 7.2000. We sit slightly higher now, last around 7.2050/60, still 0.30% stronger in CNH terms for the session. Onshore China media has been dominated by further calls for policy support, particularly for the property sector. The MNI Policy team notes China may relax property related restrictions in H2. Still, China property related shares have struggled to stay in positive territory so far today.

- 1 month USD/KRW got to fresh lows near 1288, but sits slightly higher now around 1292, still +0.40% higher for the won so far in Tuesday trade. Lower USD/JPY levels have helped the pair, while onshore equities are +1.3% higher, with offshore investors adding $283.4mn to local shares.

- The SGD NEER (per Goldman Sachs estimates) has retreated from its highest level since 13 June, printed in early dealing to sit a touch softer. We now sit ~0.5% below the upper end of the band. The pair has fallen a further ~0.1% today and now sits below the 20- and 200-Day EMAs, printing the lowest level since 22 June. A reminder that the only data of note this week is Fridays Advance Q2 GDP print, a fall of 0.2% Q/Q is expected.

- Broader USD/Asia flows are dominating in early trade as the Rupee firms in early dealing. USD/INR is ~0.2% lower, last printing at 82.35/40. The pair remains well within the monthly range. In a blow to India's chip making plans Foxconn has withdrawn from its semiconductor JV worth $19.5bn with Indian firm Vedanta. The domestic data docket is empty today. Tomorrow June CPI and May Industrial Production cross.

- USD/PHP has sunk back to 55.25/30, around 0.75% firmer in PHP terms versus yesterday's closing level. May trade data showed exports and imports better than expected, but the trade deficit wasn't too far off last month's levels, printing at -$4.396bn (prior -$4.843bn). For USD/PHP recent lows near 55.00 aren't too far away.

- USD/THB has slumped back through 34.90, also tracking close to July to date lows.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 11/07/2023 | 0600/0800 | *** |  | DE | HICP (f) |

| 11/07/2023 | 0600/0700 | *** |  | UK | Labour Market Survey |

| 11/07/2023 | 0800/1000 | * |  | IT | Industrial Production |

| 11/07/2023 | 0900/1100 | *** | | DE | ZEW Current Conditions Index |

| 11/07/2023 | 0900/1100 | *** | | DE | ZEW Current Expectations Index |

| 11/07/2023 | 1000/0600 | ** |  | US | NFIB Small Business Optimism Index |

| 11/07/2023 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 11/07/2023 | 1400/1000 | ** | | US | IBD/TIPP Optimism Index |

| 11/07/2023 | 1500/1100 | | US | New York Fed's John Williams | |

| 11/07/2023 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 11/07/2023 | 1530/1130 | ** | | US | US Treasury Auction Result for 52 Week Bill |

| 11/07/2023 | 1700/1300 | *** | | US | US Note 03 Year Treasury Auction Result |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.