Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Hawkish comments from the Federal Reserve and a lack of action when it came to the PBoC’s latest round of MLF operations (no rate cut and a basic rollover of maturing liquidity provisions, vs. expectations for a rate cut and net injection) provided headwinds for the equity markets that were open during Asia-Pac hours.

- Still equity losses and CNH strength were limited.

- Focus remains squarely on the potential for an imminent PBoC RRR cut, with widespread expectations for such a move to occur after market today. Elsewhere, the latest professional forecasters survey from the ECB, U.S. industrial production, NY Fed manufacturing & French CPI data will cross on Friday.

JGBS: Flatter, Futures Back From Best Levels

JGB futures initially nudged higher during Tokyo dealing, briefly unwinding overnight losses, before softening a touch later in the day. The contract last deals -6 vs. Thursday’s settlement.

- The early Tokyo dynamic of long end outperformance (Although 30s and 40s are now less than 0.5bp richer on the session), 7-Year underperformance and a light twist flattening of the curve remains intact, with the relative steepness of the JGB curve likely resulting in support for longer dated JGBs after the turn of the Japanese FY.

- Spill over from a weaker JPY may have provided some incremental support for the space, with little in the way of fundamental drivers observed when it comes to FX trade.

- The previously outlined PBoC inaction (when it came to today’s MLF operations) and run-of-the-mill FX- & BoJ-related commentary from the Japanese policymaking sphere have done little to generate meaningful activity in the JGB space.

U.S.: Easter Weekend Exchange Schedules

The impending Easter holiday weekend will result in the closure/adjustment of trading hours of the major U.S. exchanges over the coming days, please use the links below to access the holiday schedules on an exchange-by-exchange basis.

ASIA: Regional Exchange Easter Holiday Schedules

Below is a summary of select regional exchange schedules over the Easter holiday period:

FOREX: Fresh USD/JPY Highs, CNH Benefits Marginally From PBoC Inaction (For Now)

Fresh cycle highs for USD/JPY supported the broader USD during Asia-Pac dealing, with the greenback sitting atop the G10 FX leader board after geopolitical tension and the need for continued Fed policy normalisation dominated news flow during the backend of Thursday’s NY hours. A reminder that liquidity is challenged owing to the observance of elongated weekends across many major global financial centres.

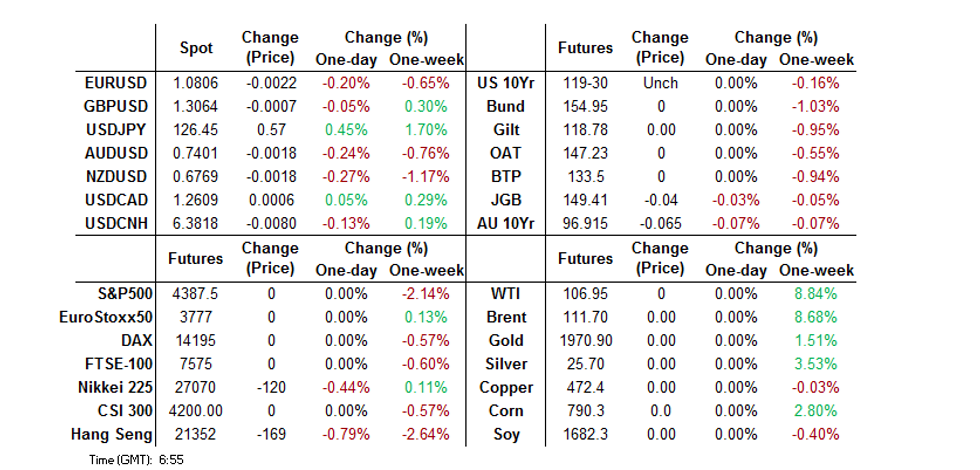

- Gotobi-linked demand surrounding the Tokyo fix was earmarked as a potential driver when it came to the latest leg higher in JPY crosses. USD/JPY has registered a fresh cycle high at Y126.56, with a Fibonacci projection (Y126.71) now providing the nearest point of technical resistance. Worry surrounding the potential for an EU ban or Russian oil imports supported oil in NY dealing and may have played into JPY weakness in early Tokyo trade, as local participants reacted to that move, as well as Thursday’s move higher in U.S. Tsy yields (a reminder that both the U.S. oil and Tsy markets are closed on Friday). The headwinds for the JPY are well documented, with central bank divergence (the BoJ continues to affirm its super dovish stance), yield differentials and Japan’s status as a notable net energy importer weighing on the JPY in recent weeks. USD/JPY is last +50 pips, just below Y126.40.

- USD/CNH has nudged lower in the wake of PBoC inaction re: MLF matters (no rate cut and a simple roll over of existing maturing MLF), although the move has been limited, with the cross sitting ~75 pips softer on the session, hovering around CNH6.3825. Market participants remain focused on the potential for a RRR cut from the PBoC, given recent guidance from the State Council on the matter, with the likelihood being that any such move will come after Beijing market hours (see earlier bullets for more colour on that matter).

- The combination of Thursday’s uptick in the DXY, bid in oil (with worries re: a potential impending EU embargo of Russian oil evident) and move higher for broader U.S. Tsy yields supported USD/KRW in Seoul dealing, with the rate last dealing up the best part of 6 figures at KRW1,230.40. News that South Korea will lift all COVID-19 social distancing rules, except a mask mandate, next week, failed to provide much in the way of meaningful support for the won. Meanwhile, equity market outflows (although not large) added some further pressure to the KRW.

- Focus remains squarely on the potential for an imminent PBoC RRR cut. Elsewhere, the latest professional forecasters survey from the ECB, U.S. industrial production, NY Fed manufacturing & French CPI data will cross on Friday.

EQUTIES: Chinese & Japanese Equities Nudge Lower

Hawkish comments from the Federal Reserve and a lack of action when it came to the PBoC’s latest round of MLF operations (no rate cut and a basic rollover of maturing liquidity provisions, vs. expectations for a rate cut and net injection) provided headwinds for the equity markets that were open during Asia-Pac hours.

- Chinese equities slipped on the above, although the prospect of an imminent RRR cut (based on recent State Council guidance) limited losses. The CSI 300 is -0.5% at typing. Note that northbound Hong Kong-China Stock Connect flows are relatively neutral at present.

- A weaker JPY provided some support for Japanese equities which allowed the Nikkei 225 to unwind most of its early, Wall St. driven downtick. Still, the index sits ~0.3% lower ahead of the bell.

GOLD: Flat In Asia

Gold continues to outperform its fundamental drivers, residing within touching distance of the $2,000/oz mark (last little changed at $1,975/oz), even with U.S. real yields running higher in recent weeks (our weighted U.S. real yield monitor sits at the highest level observed since mid-’20), which has been accompanied by the DXY moving to ~2 year highs. Geopolitical tensions, namely the Russia-Ukraine conflict have clearly facilitated this outperformance, while ETF flows have also provided a flow driven component to the rally in the yellow metal, with total known ETF holdings of gold moving back up to Q121 levels. Asia-Pac trade has been limited, as expected, given the widespread holidays observed across most of the global financial centres.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 15/04/2022 | 0645/0845 | *** |  | FR | HICP (f) |

| 15/04/2022 | 0800/1000 |  | EU | ECB Professional Forecasters Survey | |

| 15/04/2022 | 0800/1000 | ** |  | IT | Italy Final HICP |

| 15/04/2022 | 1230/0830 | ** |  | US | Empire State Manufacturing Survey |

| 15/04/2022 | 1315/0915 | *** | | US | Industrial Production |

| 15/04/2022 | 2000/1600 | ** | | US | TICS |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.