Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Continued hawkish drumbeat from Fed officials set the tone of morning trade in Asia, generating light risk-off flows (which petered out as the session progressed), putting a bid into the greenback. Cleveland Fed's Mester ('22 voter) called for at least a 75bp rate hike at the next FOMC meeting, but kicked the can down the road re: necessity of a 100bp move. Separately, San Francisco Fed's Daly ('24 voter) told the NYT that she would most likely support a 75bp hike, but a 100bp rate rise is "in range of possibilities."

- A stronger than expected labour market report out of Australia led to some looking for a more aggressive step from the RBA in August, while the MAS & BSP implemented off-cycle monetary tightening moves.

- Swedish CPI as well as U.S. PPI & jobless claims will take focus later in the day. Comments are due from Fed's Waller and ECB's Centeno. We will also be on the lookout for any impromptu Fedspeak in the wake of yesterday's CPI print, while Italian political matters (namely a confidence vote in the government) provide another layer of complexity to the session.

US TSYS: Twisting Flatter

The post-CPI twist flattening of the curve spilled over into Asia-Pac trade, with the major cash Tsy benchmarks running 4bp cheaper to 0.5bp richer, pivoting around 20s, as the wings of the curve reflect the respective extremes.

- Hawkish Fedspeak from Mester (’22 voter) added to that particular dynamic, as she noted there was no trade off when it comes to fighting inflation, while stressing that July’s monetary policy decision “doesn’t have to be made today” and flagging the upcoming retail sales data and inflation expectations component of the UoM sentiment survey as key inputs for the July decision. She didn’t directly answer a question re: the potential for a 100bp hike but noted that the step should be as least as large as the 75bp hike deployed last time out. Elsewhere, Fed’s Daly (’24 voter) flagged her current preference for a 75bp hike but noted that a 100bp move is within the scope of the potential outcomes re: the July meeting.

- Trade during the first half of the session was two-way, with a bid to best levels quickly unwound, then extending on the back of spill over from ACGBs on the back of a firmer than expected Australian labour market report. That cheapening move then consolidated during the second half of the session, with TYU2 last dealing -0-13 at 118-16+, 0-02 off the base of its 0-15+ Asia range, although volume is subdued, running just above 90K.

- A quick reminder that various curve inversion measures have registered fresh cycle extremes post-CPI, including the 2-/10-Year yield spread, EDZ2/H3, EDZ2/Z3 & EDZ2/Z4. Note that Fed Chair Powell’s preferred measure, the 3-month/3-month 18 months forward spread, now sits around the 65bp mark, after flattening by ~150bp over the last month.

- Various FV option blocks headlined on the flow side in Asia.

- PPI & weekly jobless claims data is due today, as is Fedspeak from Governor Waller.

JGBS: Curve Twist Flattens, 20-Year Supply Goes Smoothly

JGB futures are -4 ahead of the bell, with the contract sticking comfortably within the confines of its overnight session range.

- Cash JGBs twist flattened, in sympathy with post-CPI U.S. Tsy trade, pivoting around the 10- to 20-Year zone, with the major benchmarks running 1.5bp cheaper to 1.5bp richer across the curve (a similar move was observed in swaps, although the net changes were more modest there).

- Domestic headline flow has seen a continued uptick in worry re: FX market moves amongst senior Japanese policymakers

- Elsewhere, foreign investors registered the largest round of net weekly purchases of Japanese bonds observed since July of last year. We would suggest that this largely represents continued short covering in JGBs (third straight week of net purchases) after the BoJ reinforced the upper end of its permitted 10-Year JGB yield trading band in June (with foreign investors willing to test the BoJ’s resolve at that time).

- In terms of 20-Year supply, the low price observed at the 20-Year auction topped wider dealer expectations (which stood at 99.80 per the wider BBG dealer poll), with the tail narrowing a touch and cover ratio moving further above the 6-auction average. The tail width means that the auction wasn’t overly strong, but it was easily digested, with the previously outlined curve steepness and home bias of the Japanese bond investor community likely supporting takedown.

AUSSIE BONDS: Labour Market Data Adds To Flattening Pressure

The cheapening impetus seen from stronger-than-expected domestic labour market data allowed the Tsy-inspired flattening impetus to extend, with another shunt lower in the unemployment rate outstripping market expectations.

- The space is back from extremes in terms of both cheaps and session flats as we work towards the Sydney close. Cash ACGBs run 2-15bp cheaper across the curve, with 3s sitting ~14.5bp cheaper at typing, after printing as much as 19bp cheaper earlier in the day. YM and XM are -14.0 and -4.5, respectively after the former breached its overnight lows in the wake of the labour market report. EFPs have continued their recent tightening, with the 3-/10-Year box flattening today.

- Bills run flat to 34 ticks cheaper through the reds, bear flattening.

- STIR markets now price in ~64bp of tightening come the end of the RBA’s August meeting, with Goldman Sachs and Nomura being the first two sell-side names to call for such a move. The continued tightening of the labour market, coupled with the frontloading of Fed hike expectations have been in the driving seat today, with the labour market report threatening to force a further frontloading of RBA tightening, in addition to opening the door towards a higher terminal rate.

- Friday will see the release of the AOFM’s weekly issuance slate, as well as a A$700mn of ACGB Apr-27 auction.

JAPAN: Selling Of Foreign Bonds Persists, Foreigners Still Covering JGB Shorts

Japanese investors continued to shed foreign bonds at a swift pace, with Japan’s weekly international security flow data revealing the third consecutive round of net weekly sales that have topped the Y1.0tn mark. The week also represented the seventh consecutive week of net selling of foreign bonds on the part of Japanese investors, with market volatility and elevated FX-hedging costs the key stories here.

- Elsewhere, foreign investors registered the largest round of net weekly purchases of Japanese bonds observed since July of last year. We would suggest that this largely represents continued short covering in JGBs (third straight week of net purchases) after the BoJ reinforced the upper end of its permitted 10-Year JGB yield trading band in June (with foreign investors willing to test the BoJ’s resolve at that time).

- Japanese investors were net buyers of foreign equities for a fourth consecutive week, although the pace moderated from what was seen in the previous week.

- Finally, foreign investors were net buyers of Japanese equities, ending a streak of 3 consecutive weeks of net selling.

| Latest Week | Previous Week | 4-Week Rolling Sum | |

|---|---|---|---|

| Net Weekly Japanese Flows Into Foreign Bonds (Ybn) | -1491.0 | -1414.0 | -4992.8 |

| Net Weekly Japanese Flows Into Foreign Stocks (Ybn) | 687.9 | 1191.8 | 1940.8 |

| Net Weekly Foreign Flows Into Japanese Bonds (Ybn) | 2066.5 | 330.5 | -1747.3 |

| Net Weekly Foreign Flows Into Japanese Stocks (Ybn) | 526.3 | -490.3 | -1324.7 |

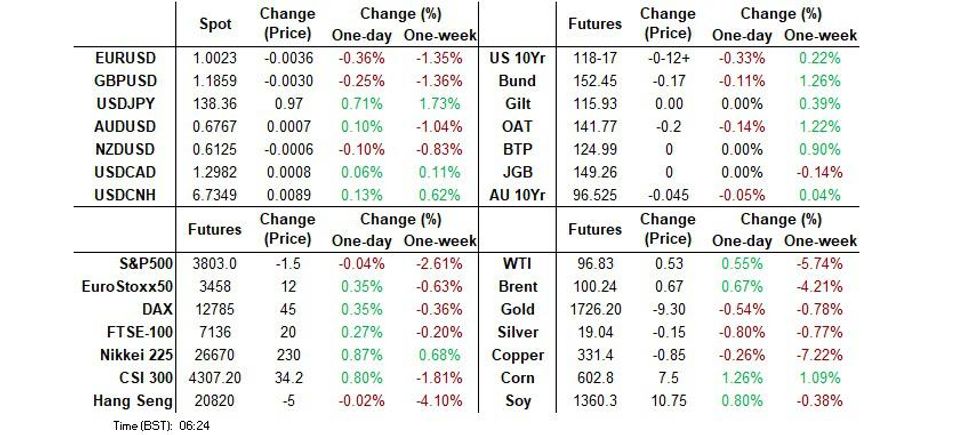

FOREX: Strong Jobs Report Drives AUD Outperformance, Hawkish Fedspeak Props Up USD

Continued hawkish drumbeat from Fed officials set the tone of morning trade in Asia, generating light risk-off flows (which petered out as the session progressed) and putting a bid into the greenback. Cleveland Fed's Mester ('22 voter) called for at least a 75bp rate hike at the next FOMC meeting, but kicked the can down the road re: necessity of a 100bp move. Separately, San Francisco Fed's Daly ('24 voter) told the NYT that she would most likely support a 75bp hike, but a 100bp rate rise is "in range of possibilities."

- Anticipation of increasingly hawkish posturing from the Fed raised the prospect of further widening in U.S./Japan yield gap, with the BoJ committed to keep local interest rates rock bottom. This rendered the yen vulnerable, with USD/JPY climbing into the Tokyo fix to print a fresh cyclical high at Y138.12. Japan's Chief Cabinet Secretary Matsuno said officials will watch FX moves with heightened sense of urgency, but his comments provided only brief, mild reprieve to the yen.

- A stellar labour force survey allowed the Aussie dollar to regain poise and eventually top the G10 scoreboard amid aggressive addition of hawkish RBA bets. The report showed that employment grew by 88.4k in June, far exceeding expectations of all economists surveyed by Bloomberg, with the unemployment rate dropping to a multi-decade low. The OIS strip now prices ~57bp worth of tightening at the RBA's August meeting, suggesting that some participants are bracing for a 75bp hike to the cash rate target.

- Trans-Tasman spillover lent a helping hand to the kiwi dollar, albeit it understandably lagged its Antipodean cousin. AUD/NZD showed above yesterday's peak, even as AU/NZ 2-Year swap spread is back to virtually neutral levels after some minor perturbations caused by Australian jobs data.

- Swedish CPI as well as U.S. PPI & jobless claims will take focus later in the day. Comments are due from Fed's Waller and ECB's Centeno.

FX OPTIONS: Expiries for Jul14 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0095-10(E851mln), $1.0150(E682mln), $1.0190-00(E1.0bln)

- GBP/USD: $1.1820(Gbp616mln), $1.2000(Gbp548mln)

- USD/JPY: Y135.70($1.2bln), Y136.00($976mln), Y139.00($1.5bln)

- NZD/USD: $0.6090-00(N$1.0bln), $0.6120(N$1.3bln)

- USD/CAD: C$1.2925-45($ 710mln)

ASIA FX: Unscheduled Tightening Shields SGD, PHP From Impact Of Hawkish Fedspeak

Hawkish Fedspeak supported most USD/Asia crosses but off-cycle action from a couple of regional monetary authorities created surprise outperformers.

- CNH: The dollar side was the main driver of USD/CNH as the PBOC fix fell virtually in line with expectations. The rate climbed to a session high of CNH6.7369 before trimming gains.

- KRW: Likewise, USD/KRW advanced to near KRW1,312 before paring some gains. South Korea's Vice FinMin Bang pledged that officials will step up monitoring and actively tackle herd behaviour in financial markets.

- SGD: The Singapore dollar easily outperformed its regional peers after the MAS re-centred the S$NEER policy band higher, effectively tightening monetary conditions. It was the third unscheduled policy adjustment this year, with the next regular review coming up in October. The surprise decision overshadowed below-forecast GDP data released at the same time.

- PHP: The BSP followed suit, announcing an off-cycle 75bp hike to its key policy rate. While some speculated that that MAS could soon tweak policy to address persistent inflationary pressures, the BSP was expected to wait until its August meeting and has only recently put a 50bp hike on the table. The peso appreciated after flirting with all-time lows in recent days.

- IDR and MYR weakened after palm oil futures retreated to multi-month lows as recessionary fears spoiled demand outlook. Spot USD/MYR printed fresh cyclical highs, while spot USD/IDR climbed towards the IDR15,000 mark.

- THB: Baht oscillated near recent cycle lows, with liquidity sapped by a national holiday in Thailand. While local financial markets were open, government offices were shut and many people were off.

EQUITIES: Higher In Asia: Chinese Tech Rally Counters Property Developer Weakness

Major Asia-Pac equity indices are 0.4% to 0.7% better off at typing, bucking a negative lead from Wall St.

- The Hang Seng Index deals 0.2% firmer at typing, on track to snap a four-session streak of losses. The property and financial sub-indices posed the most drag, with Chinese-linked developers and banks going offered amidst news of Chinese homebuyers refusing to make mortgage payments (“at least 100 projects in more than 50 cities” are affected, according to BBG reports). On the other hand, China-based tech outperformed, with the Hang Seng Tech Index 1.7% better off at writing.

- The CSI300 trades 0.5% higher, operating around session highs at typing. The industrials and healthcare sub-indices contributed the most to gains in the index, countering losses in the real estate (-2.3%) and financials (-1.7%) sub-gauges. Elsewhere, tech-related equities outperformed, with the ChiNext and STAR50 indices dealing 2.7% and 3.0% firmer apiece.

- The ASX200 deals 0.4% firmer, on track for a third consecutive daily gain. Commodity and tech-related equities lead the bid, with the S&P/ASX All Technology Index adding 1.7% at writing, while major miners sit between 2.4% to 3.9% better off.

- E-minis are flat to 0.1% weaker at typing, back from worst levels at around 0.7-0.8% lower apiece earlier in the session.

GOLD: Lower In Asia; Fed Hawkishness Eyed

Gold deals ~$5/oz weaker at typing to print $1,730/oz, off worst levels. The precious metal operates comfortably within Wednesday’s range, with the day’s move lower facilitated by an uptick in the USD (DXY) and nominal U.S. Tsy yields.

- To recap, gold closed ~$10/oz higher on Wednesday, having whipped between session highs and eleven-month lows ($1,707.5/oz) after the U.S. CPI print. A surge in Fed rate hike expectations following the data release was countered by rising worry re: recession risks, with the inversion on U.S. 2-Year/10-Year yields noted to have hit its largest in over 20 years.

- July FOMC dated OIS now price in ~92bp of tightening for that meeting, pointing to a >60% chance of a 100bp rate hike then (compared to ~75bp priced in pre-U.S. CPI). Fedspeak since the CPI print has seen no explicit ruling out of a 100bp hike for July, with the Fed’s Mester (voter) pointing to economic data due between now and the upcoming FOMC (Jul 26-27) for a decision, while the Fed’s Daly (‘24 voter) stated that a 100bp hike was “possible”.

- From a technical perspective, conditions remain bearish for gold, with focus on support at $1,706.8/oz (1.618 proj of the Mar 8-29-Apr18 price swing). Meanwhile, initial resistance is seen at $1752.3/oz (High Jul 8 / Low May 16, recent breakout level).

OIL: A Little Above Wednesday’s Three-Month Lows

WTI and Brent are ~$0.50 firmer apiece at typing, operating comfortably within their respective ranges established on Wednesday. Brent has struggled to make meaningful headway above the $100 handle in Asia-Pac dealing, with worry re: reduced energy demand in the coming quarters taking focus in recent sessions.

- Both benchmarks have risen from their respective three-month lows made on Wednesday but remain >$10 weaker from levels observed in end-June as rising recession worry continues to counter well-documented tightness in global supplies. Underperformance in crude also comes amidst strength in the USD (DXY), with the latter sitting a little below fresh cycle highs made on Wednesday.

- The International Energy Agency’s (IEA) monthly oil report was released on Wednesday, with the agency tweaking crude demand growth forecasts for 2022 and 2023 by -100K bpd apiece, citing “weaker-than-expected oil demand growth in advanced economies”. A note that this comes after OPEC’s own demand forecast issued earlier this week (unchanged for ‘22, lowered for ‘23).

- The latest round of U.S. EIA inventory estimates pointed to a surprise ~3.3mn bbl build in crude stockpiles, coming after the >8mn bbl build observed last week. Meanwhile, gasoline, distillate, and Cushing hub stockpiles inventories increased.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 14/07/2022 | 0600/0800 | *** |  | SE | Inflation report |

| 14/07/2022 | 0600/0800 | * |  | DE | Wholesale Prices |

| 14/07/2022 | 0800/0400 |  | US | Treasury Secretary Janet Yellen | |

| 14/07/2022 | 1230/0830 | ** | | US | Jobless Claims |

| 14/07/2022 | 1230/0830 | *** | | US | PPI |

| 14/07/2022 | 1400/1000 | ** | | US | WASDE Weekly Import/Export |

| 14/07/2022 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 14/07/2022 | 1500/1100 | | US | Fed Governor Christopher Waller | |

| 14/07/2022 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 14/07/2022 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.