EXECUTIVE SUMMARY

- FED’S BOSTIC - PENT-UP EXUBERANCE CALLS FOR PATIENCE - MNI BRIEF

- UK MAY GFK CONSUMER CONFIDENCE INDEX -17

- JAPAN APRIL CORE CPI AT 2.2% VS. MARCH 2.6% - MNI BRIEF

- COPPER PRICES TO FALL, CHINA DEMAND TO REMAIN FLAT - MNI

- RBNZ ‘ABSOLUTELY’ PREPARED TO HIKE RATES IF NECESSARY, SILK SAYS - BBG

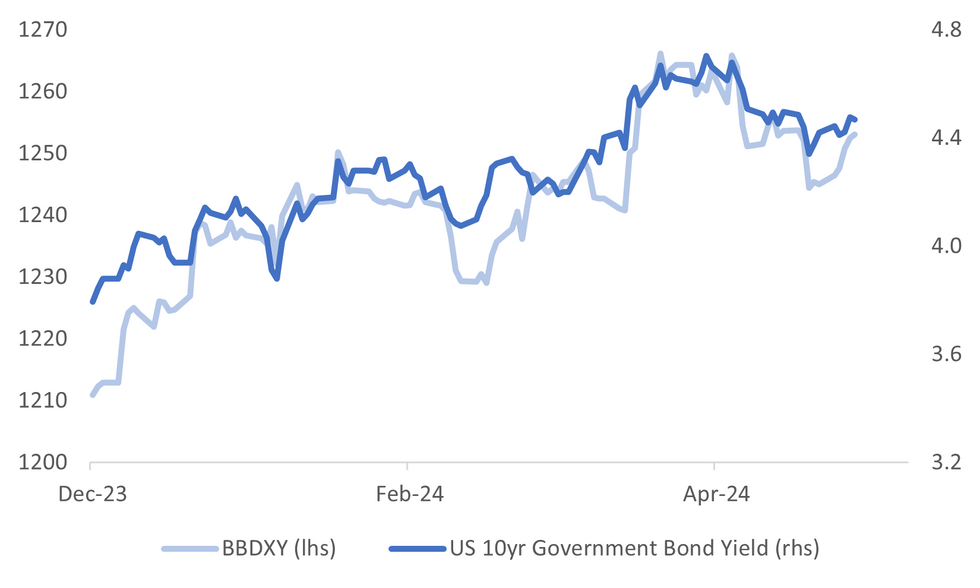

Fig. 1: USD BBDXY Index Versus US Nominal 10yr Yield

Source: MNI - Market News/Bloomberg

UK

CONSUMER (MNI): UK GfK Consumer Confidence rose slightly more than expected by 2 points to -17 (vs -18 consensus, -19 prior) in May, and rose 10 points on a year-on-year basis - the highest level seen since December 2021.

POLITICS (BBG): Keir Starmer will pitch for votes in Scotland at a campaign event Friday that will see the Labour leader try to take advantage of turmoil in the Scottish National Party to cement his path to power at the UK election.

BOE (MNI BRIEF): Governor Andrew Bailey and other senior Bank of England officials have cancelled planned speeches as the central bank adheres to government rules on refraining from public comment during an election campaign, a spokesperson for the Bank confirmed Thursday.

EUROPE

EU (MNI): Talks among eurozone finance ministers aimed at catalysing progress towards Capital Markets Union by launching a pan-European savings product are shifting towards the idea of each member state being able to launch its own savings product but marketed with a European Union label, officials told MNI.

UKRAINE (RTRS): The United States is preparing a $275 million military aid package for Ukraine, which will include 155mm artillery shells, precision aerial munitions and ground vehicles, three U.S. officials told Reuters on Thursday.

U.S.

FED (MNI BRIEF): Federal Reserve Bank of Atlanta President Raphael Bostic said Thursday the U.S. labor market is strong with still considerable upward pressure on prices, but one concern about cutting interest rates is that businesses seem to be poised to pounce on the first hint of a cut.

US/ISRAEL (RTRS): Republican U.S. House Speaker Mike Johnson said on Thursday Israeli Prime Minister Benjamin Netanyahu would soon address a joint meeting of Congress amid heightened tension with President Joe Biden over the Israeli leader's handling of the war in Gaza.

OTHER

JAPAN (MNI BRIEF): The year-on-year rise of Japan's annual core consumer inflation rate decelerated to 2.2% in April from March’s 2.6%, showing the pass-through of cost increases is weakening, data released by the Ministry of Internal Affairs and Communications showed on Friday.

MEXICO (MNI BRIEF): The Central Bank of Mexico's board believes inflationary shocks will take longer to dissipate, which is why they have revised upward forecasts for headline and core inflation, minutes of the last monetary policy meeting released Thursday showed. Most members stated that services inflation is likely to be more persistent.

NEW ZEALAND (BBG): New Zealand’s central bank is prepared to raise interest rates if economic developments mean current policy settings aren’t restrictive enough to bring inflation back to target, Assistant Governor Karen Silk said.

ASIA PAC (BBG): Taiwan has become “one of the most dangerous flashpoints” in the region as the US-China rivalry intensifies, Singapore Deputy Prime Minister Gan Kim Yong said on Friday.

CHINA

COMMODITIES (MNI EM): China’s copper demand will remain roughly unchanged over 2024 at single digit percentage growth over 2023 levels despite recent property-sector support and a historic global price rally, while reports of official domestic smelter output cuts are yet to materialise, local analysts have told MNI.

REFORM (PEOPLE’S DAILY): China will further deepen reforms comprehensively, improving systems that support innovation and urban-rural integration, to build a high-level socialist market economy, the People’s Daily reported citing President Xi Jinping. Promoting the reform of the economic system must proceed from practical needs and focus on the most urgent matters, Xi emphasised.

TECH (SHANGHAI SECURITIES NEWS): The China Securities Regulatory Commission will give priority to supporting equity and debt financing for companies with key technology breakthroughs, and improve the capital market’s inclusiveness of new industries, new business models, and new technologies, Shanghai Securities News reported citing Zhou Xiaozhou, director of the Comprehensive Department at the CSRC.

TRADE (MOFCOM): China believes certain countries have violated WTO rules and deviated from green-development principles, He Yadong, spokesperson for the Ministry of Commerce said at a press conference responding to media reports Beijing may retaliate against Western tariffs on Chinese cars.

SUPERVISION (SHANGHAI SECURITIES NEWS): At least 53 listed Chinese companies or their senior executives have been probed by regulators this year in a sign of tightened supervision, the Shanghai Securities News reported.

CHINA MARKETS

PBOC conducts CNY2 bln via Omo Fri; liquidity unchanged

The People's Bank of China (PBOC) conducted CNY2 billion via 7-day reverse repo on Friday, with the rates unchanged at 1.80%. The operation has led to no change to the liquidity after offsetting the CNY2 billion maturity today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.8000% at 09:36 am local time from the close of 1.8282% on Thursday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 49 on Thursday, compared with the close of 40 on Wednesday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 7.1102 on Friday, compared with 7.1098 set on Thursday. The fixing was estimated at 7.2486 by Bloomberg survey today.

MARKET DATA

NEW ZEALAND MAY ANZ CONSUMER CONFIDENCE 84.9; PRIOR 82.1

NEW ZEALAND MAY ANZ CONSUMER CONFIDENCE M/M 3.4%; PRIOR -5.0%

NEW ZEALAND APR EXPORTS NZD 6.42b; PRIOR 6.38b

NEW ZEALAND APR IMPORTS NZD 6.32b; PRIOR 5.90b

NEW ZEALAND APR TRADE BALANC NZD 91m; PRIOR 476mn

JAPAN APR NATL CPI Y/Y 2.5%; MEDIAN 2.4%; PRIOR 2.7%

JAPAN APR NATL CPI EX FRESH FOOD Y/Y 2.2%; MEDIAN 2.2%; PRIOR 2.6%

JAPAN APR NATL CPI EX FRESH FOOD & ENERGY Y/Y 2.4%; MEDIAN 2.4%; PRIOR 2.9%

UK MAY GFK CONSUMER CONFIDENCE -17; MEDIAN -18; PRIOR -19

MARKETS

US TSYS: Treasury Futures Edge Higher On Increased Volume, 2s10s Near Ytd Low

- Treasury futures have edged higher throughout the day, volumes have also picked up the TU is up (+ 00.375) at 101-16.25, while TY is (+ 01) at 108-24. Futures are now on track for their biggest weekly drop in 5 weeks as rate cut projections get pushed back and the 2s10s curve trading near ytd lows.

- Volumes: TU 47k, FV 102k, TY 119k

- Tsys Flows: Block Flatter FV-US, DV01 160k

- Treasuries traded lower Thursday on the back of strong PMI data, extending the pullback from the recent 109-31+ high on May 16. Support to watch lies at 108-15 (May 14 lows), on the upside initial resistance is 109-07 (50-day EMA).

- The treasury curve has slightly bear-flattened throughout the trading session with yields now 1-1.5bps lower, the 2Y yield -1.3bps at 4.922%, 10Y -1.2bp to 4.465%, while the 2y10y +0.319 at -45.962

- Regionally: ACGBs are 5bps higher, NCGBs are 3-4bps, JGBs are +/- 1bp, the 10Y touched 1%.

- Rate cut projections have receded vs late Wednesday levels (*): June 2024 at -0% w/ cumulative rate cut 0.0bp at 5.328%, July'24 at -10.0% (-16.0%) w/ cumulative at -2.5bp (-5.2bp) at 5.302%, Sep'24 cumulative -14.2bp (-17.8bp), Nov'24 cumulative -21.2bp (-26.2bp), Dec'24 -34.8bp (-40.6bp).

- Looking ahead: Durables/Cap Goods and the latest UofM Sentiment, Fed's Waller to Speak while June Treasury options expire as well.

JGBS: Cash Bonds Little Changed, BoJ Ueda and Uchida At BoJ-IMES Conference On Monday

JGB futures are weaker, -9 compared to the settlement levels, and sit in the middle of the day’s range.

- Outside of the previously outlined National CPI, there hasn't been much in the way of domestic drivers to flag. Department Sales data is due along with a Liquidity Enhancement Auction for OTR 5-15.5-year JGBs.

- According to MNI’s technicals team, a bear trend in JGB futures persists, erasing the corrective bounce last week. The contract is for now trading just above key support and bear trigger at 143.44, the Nov 1 low. A stronger reversal higher is required to signal the end of the recent downward phase. Key resistance is at 145.95, the Mar 28 high. A break would signal scope for a climb towards the bull trigger at 147.74, the mid-January high.

- Cash US tsys are dealing ~1bp richer in today’s Asia-Pac session after yesterday’s sell-off.

- Cash JGBs are little changed. The benchmark 10-year yield is 0.4bp higher at 1.006% versus the YTD high of 1.011%.

- The swaps curve has slightly bull-flattened, with rates flat to 1bp lower. Swap spreads are mostly tighter.

- On Monday, the local calendar will see BoJ Governor Ueda and Deputy Governor Uchida deliver remarks/speeches at the BoJ-IMES Conference. Leading and Coincident Indices are also due on Monday.

ACGBS: Cheaper, Narrow Ranges, CPI Monthly Next Wednesday

ACGBs (YM -6.0 & XM -6.0) remain cheaper after dealing in narrow ranges in today’s Sydney session.

- The local calendar was empty today apart from Nov-28 supply, which showed firm pricing but with a less aggressive bid.

- Cash US tsys are dealing ~1bp richer in today’s Asia-Pac session after yesterday’s sell-off.

- Cash ACGBs are 5-6bps cheaper with the AU-US 10-year yield differential at -15bps.

- Swap rates are 5bps higher, with EFPs tighter.

- The bills strip has bear-steepened, with pricing -1 to -7.

- RBA-dated OIS pricing is 3-5bps firmer for 2025 meetings. Only 5bps of easing is priced by year-end.

- Next week, the local calendar will see Retail Sales on Tuesday, CPI Monthly, Westpac Leading Index and Construction Work Done on Wednesday, and Private Capital Expenditure and Building Approvals on Thursday. RBA's Hunter will conduct a Fireside Chat on Thursday.

- Next week, the AOFM plans to sell A$600mn of the 1.50% 21 June 2031 bond on Wednesday and A$700mn of the 2.75% 21 November 2029 bond on Friday.

- Looking ahead to Friday's US data calendar, the focus will be on Durables/Cap Goods and the latest UofM Sentiment.

NZGBS: Cheaper, Narrow Ranges, NZ Govt. Budget Next Thursday

NZGBs closed 3-4bps cheaper after dealing in narrow ranges in today’s session. Outside of the previously outlined ANZ Consumer Confidence and Trade Balance data, there hasn't been much in the way of domestic drivers to flag.

- Cash US tsys are dealing ~1bp richer in today’s Asia-Pac session after yesterday’s sell-off.

- Swap rates closed 5-6bps higher, with the 2s10s curve unchanged.

- RBNZ dated OIS pricing is 3-6bps firmer for meetings beyond October, with Mar-25 leading. A cumulative 21bps of easing is priced by year-end.

- (AFR) The New Zealand central bank is leading the world with its unalloyed and politically independent commitment to crushing inflation by imposing a recession and driving up unemployment to put downward pressure on wage growth and rampant services costs. (See link)

- Next week, the local calendar will see Filled Jobs on Tuesday, ANZ Business Confidence on Wednesday, and Building Permits and the NZ Government Budget on Thursday.

- Looking ahead to Friday's US data calendar, the focus will be on Durables/Cap Goods and the latest UofM Sentiment.

FOREX: NZD Tests 0.6100, JPY Continues To Slide, Fed Waller To Speak Later

The BBDXY sits slightly higher for the first part of Friday trade, last trade just above Thursdays highs at 1,253.08. The NZD has been the outperformer again today as the hawkish RBNZ continues to provide support for the currency, while the CHF and AUD are the worst performers, although ranges have been tight.

- NZD/USD hovers just below 0.6100 today, and unchanged for the session. We are still comfortably below the post RBNZ high of 0.6150, however is maintaining the kiwi outperformance theme.

- Earlier, ANZ ANZ Consumer Confidence rose to 3.4% m/m from -5.0% in March, while the trade balance surplus narrowed to $91m from $588m in March.

- AUD/USD is down 0.10% and struggling to break back above 0.6600. The pair is down 1.39% for the week, with AU CPI next week.

- USDJPY has ticked higher throughout the session and holds above 157.00 at 157.09, although slightly below Thursday highs of 157.20. 10Y JGBs rose to 1.005%, the highest level since 2012.

- Looking ahead, UK Retail Sales and The Fed's Waller to speak later today

ASIA STOCKS: HK & China Property Slump On Worries Recent Measures Are Not Enough

Hong Kong & Chinese equities are lower today. HK markets have continued their four day losing streak as investors off-load stocks as US rate cut expectations are pushed back out to December from November, property is the worst performing as investors grow concerned that the most recent measures to support the struggling sector are not enough, while tech stocks are lower on concerns around Alibaba's convertible bond issuance. The calendar was empty for the region today.

- Hong Kong equities are lower today, with property the worst performing sector. The Mainland Property Index is down 4.22%, while the HS Property Index is down 2.98%, HStech Index is down 1.82% while the wider HSI is down 1.24%. In China, the CSI300 is down 0.50%, while the small-cap CSI1000 and CSI2000 Indices have recovered some of the mornings losses to trade down 0.30% and 0.05% respectively, while the growth focus ChiNext Index is down 0.75%

- (MNI) Copper Prices To Fall, Chinese Demand To Remain Flat - (See link)

- (MNI) China Press Digest May 24: Reforms, Tech Listing, Tariffs - (see link)

- Alibaba is aiming to raise $4.5 billion through a convertible bond sale to fund stock buybacks. The sale includes a greenshoe option to increase the deal by $500 million. The proceeds will also support Alibaba's core e-commerce and cloud businesses, which have lost market share due to regulatory crackdowns and internal issues. Alibaba's stock fell 1.2% after the announcement. The bonds will have an annual coupon of 0.25% to 0.75%, a 30%-35% conversion premium, and mature in seven years.

- President Xi has called for deeper reforms in key sectors such as property, employment, and childcare to boost the weakening economy. Xi emphasized that reforms should enhance livelihoods and promote Chinese-style modernization. Xi's comments raise expectations for significant policy measures to be unveiled soon.

- Next week, Hong Kong has Trade Balance data on Monday, Retail Sales on Friday, while China has PMI on Friday.

ASIA PAC STOCKS: Equities Head Lower, US Rate Cut Expectations Are Pushed Out To Dec

Asia markets have tacked US equities lower, following higher than expected US PMIs which caused US yields to push higher as rate cut expectations get pushed out to December from November. Earlier, Japan's CPI beat estimates although it did fall from the month prior, the 10Y yield continues to trade near 1% while the market prices about a 10bps hike for the July meeting, there is little else on the regional calendar today.

- Japanese equities have opened lower today, inflation eased for the second month falling to 2.5% from 2.7% in March, while the yield on 10-year government bonds exceeded 1% as markets anticipate a possible rate hike by the BoJ in July. Despite cooling prices, speculation on further policy tightening persists, with some experts expecting the BOJ to wait until October to raise rates again, potentially increasing pressure on the yen which has slipped back above 157. The Topix is down 0.30%, while the Nikkei 225 is down 1.03%.

- Taiwan equities have followed global markets lower this morning, TSMC lead the decline, although it's off opening lows. China commenced its most extensive military drills in a year around Taiwan on Thursday, increasing pressure on President Lai Ching-te just days after his inauguration. Despite this, markets have remained calm. The Taiex is down just 0.08%

- South Korean equities are lower today amid board risk-off sentiment in the region, Samsung Electronics has been the biggest contributor to the losses and the Kospi is now on track for its worst weekly performance for the month. The Kosdaq is down 0.70%, while the Kospi is down 1%.

- Australian equities are tracking global markets lower, all sectors are in the red other than energy stocks. The ASX200 is down 1%, and is now testing the 50-day EMA, a break below here could signal a move to 7,636 and the 100-day EMA.

- Elsewhere in SEA, New Zealand equities closed down 0.60%, earlier the trade Balance surplus narrowed, Singapore equities have fallen 0.47%, Malaysian equities are down 0.65%, while the Philippines PSEi are down 0.70%, while Indian equities are down 0.20%

GOLD: Down Sharply Again On Stronger US PMI Data

Gold is little changed in the Asia-Pac session. This comes after bullion slid 2.1% to $2329.27 on Thursday, following the stronger-than-expected US PMI data, which saw markets push back expectations again for the first Fed rate cut later this year.

- US Treasury yields finished up 4-6bps across benchmarks. The 10-year rate was up 5bps at 4.48%.

- US STIR is back to pricing just 35bps of cuts this year, with November no longer fully priced.

- The yellow metal is now around $130 below the record high reached on Monday.

- Although gold has pulled back from its recent high, the medium-term trend structure remains bullish and short-term weakness is considered corrective, according to MNI’s technicals team.

- On the upside, attention remains on $2,452.5 next, a Fibonacci projection. The 50-day EMA, at $2297.2, represents a key support.

- Silver has also pulled back more than 7% from Monday’s high, with the precious metal down another 2.0% yesterday to $30/oz.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 24/05/2024 | 0600/0700 | *** |  | UK | Retail Sales |

| 24/05/2024 | 0600/0800 | *** |  | DE | GDP (f) |

| 24/05/2024 | 0600/0800 | ** |  | SE | PPI |

| 24/05/2024 | 0645/0845 | ** |  | FR | Manufacturing Sentiment |

| 24/05/2024 | 0700/0900 | ** |  | ES | PPI |

| 24/05/2024 | 0700/0900 |  | EU | ECB's Schnabel speech at Germany PhD conference | |

| 24/05/2024 | 1230/0830 | * |  | CA | Quarterly financial statistics for enterprises |

| 24/05/2024 | 1230/0830 | ** | | CA | Retail Trade |

| 24/05/2024 | 1230/0830 | ** |  | US | Durable Goods New Orders |

| 24/05/2024 | 1335/0935 | | US | Fed Governor Christopher Waller | |

| 24/05/2024 | 1400/1000 | ** | | US | U. Mich. Survey of Consumers |

| 24/05/2024 | 1700/1300 | ** | | US | Baker Hughes Rig Count Overview - Weekly |