Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- FED’ S POWELL TRIES TO CORRAL HAWKS BY JUNE - SAHM - MNI INTERVIEW

- BANK OF ENGLANG'S ANDREW BAILEY SAYS RATE CUTS "IN PLAY" IN UPBEAT TAKE ON UK ECONOMY - FT

- BOJ MARCH TANKAN TO SHOW WEAKER SENTIMENT, SOLID CAPEX - MNI

- UEDA SAYS BASIC STANCE IS TO LET MARKET DECIDE LONG-TERM YIELDS - BBG

- RBA SAYS BANKS ARE STRONG, HOUSEHOLDS RESILIENT TO HIGHER RATES - BBG

- HIGH NZ IMMIGRATION TO PRESSURE RATES - MNI INTERVIEW

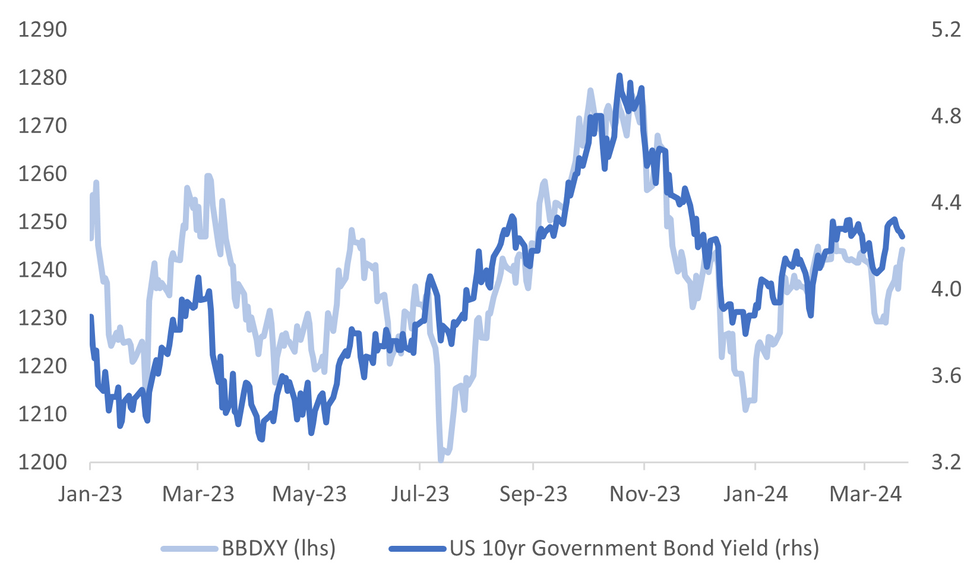

Fig. 1: USD Index & US 10yr Tsy Yield

Source: MNI - Market News/Bloomberg

U.K.

CONSUMER (BBG): UK consumers are at their most upbeat about their personal finances since 2021, suggesting household budgets remain resilient after the economy’s brief recession last year.

BOE (FT): The Bank of England governor has signalled markets are right to expect more than one interest rate cut this year, saying he is increasingly confident inflation is heading towards target. Andrew Bailey told the Financial Times that rate cuts were “in play” at future meetings of the BoE Monetary Policy Committee amid signs that tighter policy had quelled the risk of a wage-price spiral.

BOE (MNI BOE WATCH): The Bank of England's Monetary Policy Committe voted eight-to-one for unchanged policy at its March meeting, with no member voting for a rate hike for the first time since September 2021 as Jonathan Haskel and Catherine Mann dropped their previous call for a 25-basis-point rise and Swati Dhingra again backed a cut.

EUROPE

ECB (MNI SOURCES): European Central Bank policymakers would be wary of permitting a “significant divergence” in interest rates with the Federal Reserve during their widely-expected easing cycles, sources told MNI.

GERMANY (BBG): Germany’s far-right AfD lost support nationwide as it confronted public resistance and an insurgent party that’s focused on criticizing immigration as well as the country’s support for Ukraine’s war effort.

UKRAINE (BBG): The International Monetary Fund has approved the next disbursement to Ukraine within a $15.6-billion loan program, a move that bolsters the nation’s finances as aid from the US, its key ally, remains stalled.

RUSSIA (BBG): The European Union is set to propose punitive tariffs on the imports of some Russian agricultural products as early as Friday, a move that should all but halt trade of the restricted items destined for the bloc, according to people familiar with the matter.

POLAND (BBG): Poland’s ruling party is gearing up for a drawn-out probe of central bank Governor Adam Glapinski, a lawmaker involved in the case said, warning of potential attempts to scupper the proceedings. The motion to start the probe will be submitted in parliament on Tuesday, Janusz Cichon, who has led the work on the dossier, told Bloomberg in an interview.

U.S.

FED (MNI INTERVIEW): Federal Reserve Chair Jerome Powell’s remarks at this week's policy meeting suggest he wants to cut interest rates in June, though FOMC projections show he will have to work to get some of his more hawkish colleagues on board, former Fed economist Claudia Sahm told MNI.

FED (BBG): Former Treasury Secretary Lawrence Summers criticized the Federal Reserve for continuing to signal that it’s prepared to lower interest rates in coming months, despite a strong economy that’s giving off projections of still-too-high inflation.

TECH (BBG): Regulators on both sides of the Atlantic are training their eyes on Apple Inc., unnerving investors with fears over fines and threatening its market dominance.

CORPORATE (BBG): Nike Inc. warned investors that sales will take a hit later this year as it works to realign merchandise to better match what shoppers want to buy.

US/CHINA (RTRS): The Biden administration said China's top chipmaker SMIC (0981.HK), opens new tab might have violated U.S. export rules to produce a chip to power Huawei's Mate 60 Pro phone, but is still evaluating the situation, a senior Commerce Department official stated during a congressional hearing on Thursday.

OTHER

ISRAEL (BBG): A top Israeli official said his country’s military is ultimately going to invade the southern Gaza city of Rafah and defeat Hamas “even if the entire world turns on Israel, including the United States.”

JAPAN (MNI BRIEF): The year-on-year rise of Japan's annual core consumer inflation rate accelerated to 2.8% in February from January's 2.0%, 10 basis points lower than expected, data released by the Ministry of Internal Affairs and Communications showed Friday.

JAPAN (MNI): The Bank of Japan's March Tankan survey due April 1 will show a temporary worsening of major business sentiment over the quarter, but small- and major-firm capital investment plans are expected to remain solid, economists told MNI.

JAPAN (BBG): Governor Kazuo Ueda says Bank of Japan’s basic stance is to let market players decide long-term bond yields. Wants to monitor the impact of recent policy shifts on financial markets, Ueda says in response to questions in parliament.

AUSTRALIA (BBG): Australian banks are “well prepared” to handle an expected increase in loan losses in the period ahead as elevated inflation and high borrowing costs squeeze household incomes, crimping their ability to meet their obligations.

NEW ZEALAND (MNI INTERVIEW): High New Zealand immigration levels have continued into 2024 and will add further demand pressure, keeping inflation elevated, and making monetary-policy easing a tougher sell, a former treasury official has told MNI.

MEXICO (MNI BANXICO WATCH): Mexico's central bank initiated a new monetary easing cycle Thursday, cutting interest rates by 25bp, to 11.00% as expected but offering no clear clues into next policy steps in a statement that suggested policymakers will be strictly guided by data without prejudging the outcome of future meetings.

CHINA

PROPERTY (BBG): Chinese authorities are examining the role of PricewaterhouseCoopers LLP in China Evergrande Group’s accounting practices after the developer was accused of a $78 billion fraud, ramping up pressure on the global accounting giant that audited a slew of developers before the sector’s meltdown.

CHINA/US (BBG): China’s Commerce Minister Wang Wentao meets HP President and CEO Enrique Lores and urged the American computer firm to step up innovation investment in China, according to a statement on the ministry’s website.

AUTOS (YICAI): Consumer’s are expected to have purchased around 750,000 new energy vehicles in March, up 37.1% y/y and 93.2% m/m, as price cuts for EVs after the Chinese spring festival spurred demand, according to the Passenger Car Association. The narrow passenger car market in total sold 1.65 million units, a slight increase of 3.7% y/y, the association added.

LGFV (YICAI): Local governments should ensure the timely repayment of principal and interest on statutory debt amid sharply declining land-sale revenue, according to Yicai.com in a commentary. The issuance of local government special bonds has surged to stabilise growth in recent years. While nearly 90% of the principal is repaid by rollovers, the interest can only be met with fiscal funds.

CHINA MARKETS

MNI: PBOC Drains Net CNY11 Bln Via OMO Fri; Rates Unchanged

The People's Bank of China (PBOC) conducted CNY2 billion via 7-day reverse repo on Friday, with the rates unchanged at 1.80%. The operation has led to a net CNY11 billion after offsetting CNY13 billion maturity today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.8552% at 09:33 am local time from the close of 1.8690% on Thursday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 50 on Thursday, compared with the close of 48 on Wednesday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 7.1004 on Friday, compared with 7.0942 set on Thursday. The fixing was estimated at 7.2102 by Bloomberg survey today.

MARKET DATA

NEW ZEALAND FEB EXPORTS NZD 5.89BN; PRIOR 4.82BN

NEW ZEALAND FEB IMPORTS NZD 6.11BN; PRIOR 5.90BN

NEW ZEALAND FEB TRADE BALANCE NZD -218MN; PRIOR -1089MN

NEW ZEALAND FEB TRADE BALANCE 12MTH YTD NZD -11991MN; PRIOR -12620MN

JAPAN FEB NATIONAL CPI Y/Y 2.8%; MEDIAN 2.9%; PRIOR 2.2%

JAPAN FEB NATIONAL CPI EX FRESH FOOD Y/Y 2.8%; MEDIAN 2.8%; PRIOR 2.0%

JAPAN FEB NATIONAL CPI EX FRESH FOOD, ENERGY Y/Y 3.2%; MEDIAN 3.3%; PRIOR 3.5%

UKMAR GFK CONSUMER CONFIDENCE -21; MEDIAN -19; PRIOR-21

SOUTH KOREA FEB PPI Y/Y 1.5%; PRIOR 1.3%

MARKETS

US TSYS: Treasury Futures Edge Higher, Fed's Barr & Bostic Speak Later Today

- Jun'24 10y futures have edged slightly higher as we head into the Asia break, volumes remain on the light side, while we trade well within Thursday's ranges after making lows on the open of 110-12+ and trade near highs of 110-16 at 110-15+ up + 03 for the day. 5Y futures have traded similar up +02 to 106-30 just off highs made earlier of 106-30+.

- Looking at technical levels: Initial support lays at 109-24+ (Mar 18 low/ the bear trigger), further down 109-14+ (Nov 28 low), while to the upside initial resistance is seen at 110-26+ (Mar 21 high), while above here 111-01+ (50-day EMA), a break above here would open a retest of 111-24 (Mar 12 high).

- Treasury curves have bull-steepened today with yields 1-2bps lower, the 2y is -1.7bps at 4.619%, the 10y is -1.4bp at 4.253%, while the 2y10y is -0.320 at -36.826, down from a high of -32.00 on Thursday.

- Looking ahead: It's an empty calendar for Friday, while Fed's Barr & Fed's Bostic will speak later today

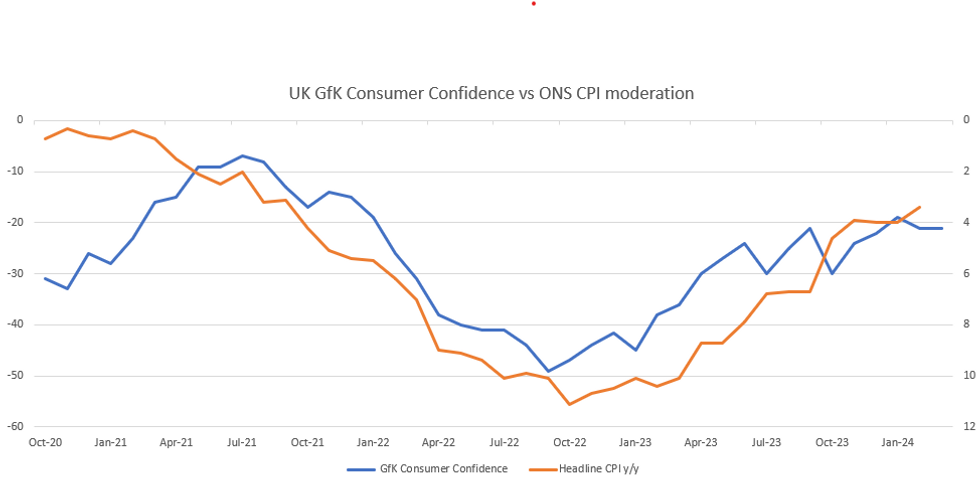

UK DATA: UK Consumer Confidence Unchanged for Second Consecutive Month

UK GfK Consumer Confidence printed weaker than expected remaining at -21 in February (vs -19 forecast) although on a year-on-year basis, this month's reading is a +15 point improvement.

- The chart below shows that since inflation moved notably above the 2% target in mid-2021 consumer confidence has generally been inversely correlated. And hence since headline inflation started to moderate towards the end of 2022, consumer confidence has improved.

- However, more recently as inflation has begun to approach more 'normal' levels, the relationship is beginning to weaken, as price increases become less dominant in consumers' minds.

- In terms of the month-on-month changes, 2 subcomponents were down, whilst 3 increased. The General Economic Situation over the last 12 months and the Major Purchase Index both fell 2 points to -45 and -27, although both remaining above March 2023 levels.

- Meanwhile, Personal Financial Situation over the next 12 months improved 2 points to 2, after stalling at 0 for 2 successive months, this a a significant 31 points improvement year-on-year. Finally, Personal Financial Situation in the last 12 months and General Economic Situation over the next 12 months both improved by 1 point, keeping all subcomponents comfortably above levels seen in March 2023.

- March's survey was conducted among a sample of 2007 individuals from March 1st to March 15th, 2024.

JGBS: Futures Supported On Dips As US Tsy's Rally, Ueda Wants To Scale Back Bond Purchases Eventually

JGB futures went lower post the lunch time break, getting to 145.29, but from there we rebounded and last track near 145.42, +.01. This is close to where we started the session.

- Some modest downside pressure may have been evident from comments by BoJ Governor Ueda, who appeared before parliament. The Governor stating that the central bank will eventually scale back its bond purchases (long end rates should ultimately be determined by the market). This is unlikely to be in the near term as Ueda stated the central bank will assess the market reaction to the recent policy shift.

- Still, the continued push higher in US Tsy futures, last at 110-18, +05+ for the 10yr future, has likely had some positive spill over to the JGB futures space. Broader risk aversion in the equity space has likely helped this move.

- In terms of JGB yields, the 2yr has hit multi decade highs above 0.205%. Most other parts of the curve are firmer in yield terms, although more so at the front end. The 10yr JGB yield was last up a touch to 0.745%.

- In the swap space, the 10yr was last around 0.88%, little changed for the session.

- Earlier data showed national CPI a touch below expectations, but y/y headline momentum still rebounded from Jan levels (to 2.8% from 2.2%). Core CPI, ex fresh food and energy, continued to moderate to 3.2% y/y.

AUSSIE BONDS: Yields Push Lower, Curve Bull-Flattens, RBA's Review Out Earlier

ACGBs (YM +5 & XM +5) are richer today after recovering some of the sell off post US data overnight. The RBA release half-yearly review earlier stating the the economy remains highly resilient.

- US Current Account Balance slightly narrowed at -$194.8b vs -$209.0b expected, while futures saw some pressure after slightly lower than estimated weekly jobless claims data: 210k vs. 213k est (prior up-revised to 212k from 209k, however).

- The RBA released its Financial Stability Review, stating that the Australian financial system remains highly resilient. Less than 1% of home loans are 90 or more days in arrears, although mortgage repayments have increased by 30-60% since the May 2022 rate hike. Most borrowers are expected to cope well if rates remain higher for an extended period, and local commercial property owners exhibit little financial stress. While banks anticipate a slight increase in arrears, they are projected to remain low overall (See link)

- Cash ACGBs are 3-7bps cheaper, the curve has bull-flattened with the 2yr -4.3bp at 3.800%, the 10y is -5.8bps at 4.031%, while the 2y10y is -0.450 to 21.25

- The AU-US 10-year yield differential 2bps lower at -20bps, while AU swap rates are 2-7bps lower.

- RBA-dated OIS pricing is 1-3bps softer for meetings beyond June. A cumulative 41bps of easing is priced by year-end.

- Looking ahead: The calendar is empty on Monday, while Tuesday we have Westpac Consumer Confidence

NZGBs Slightly Cheaper, Trade Balance Narrowed, Conway To Speak Tuesday

NZGBs did very little on Friday closing in line with opening levels, yields were 1-3bps higher and curves bear flattened. Earlier NZ trade balance data was released showing an improvement to the deficit at -NZ$218m from a revised -NZ%1,089m in Jan. The 12-month deficit is steadily improving from mid-2023 lows, near -NZ$17bn to now just under -NZ$12bn.

- (Bloomberg) -- Recession Is Back, Soft Path to Drive RBNZ Pivot. NZ has entered a recession as GDP fell 0.1% in Q4 2023, driven by declines in residential construction and inventories, while per-capita GDP also decreased for the fifth consecutive quarter, signalling challenges for the economy despite expectations of gradual recovery in 2024 amid significant monetary policy tightening. (See link)

- Swap rates closed flat to 1.5bps lower, with the 2s10s curve flatter.

- The NZ trade weight Index made new yearly lows down 0.61% to 70.73, while the AU-NZ 2yr swap is just off monthly highs at -0.81, the NZD is down 0.46% to 0.6018, while Equities finished up 0.48%.

- RBNZ dated OIS has edged lower again with pricing 3bps softer for meetings beyond October. A cumulative 76bps of easing is priced by year-end.

- Next Week: RBNZ's Conway speaks about Feb MPS on Tuesday, while ANZ consumer Confidence on Wednesday

FOREX: USD Index Above Pre FOMC Levels, Yuan Fall Weighs, While Yen Outperforms

The BBDXY is up more than 0.20%, putting the index up around the 1244.40 level. This is above pre FOMC levels from earlier in the week and back to earlier highs from March.

- The USD has benefited from a break higher in onshore USD/CNY spot, which finally pushed through resistance at 7.2000 at the onshore open today. USD/Asia pairs are higher across the board, while AUD and NZD are comfortably the weakest performers in the G10 space.

- AUD/USD is off around 0.70%, last near 0.6525. We aren't too far from earlier lows in the week (0.6504). Weakness in China/HK equities has also been in focus, with earnings concerns along with fresh investment/regulatory fears from the US another headwind. The RBA Financial Stability Review stated the system remains highly resilient. Borrowers are coping with higher rates, in aggregate, at this stage.

- NZD/USD was last near session lows at 0.6010/15, which is also fresh lows for the year. The pair has dipped 0.50% so far today. Outside of the 0.6000 level, note the Nov 17 intra-session low from lats year 0.5940.

- Yen has outperformed, amid the risk averse backdrop. USD/JPY initially went a touch above post BoJ highs (getting to 151.86), but just shy of 2023 highs at 151.91. Lower equities and lower US yields have helped the yen. We sit back near 151.50/55 in recent dealings. Feb national CPI was close to epxectations.

- BoJ Governor Ueda appeared before parliament, stating that the central bank will eventually scale back its bond purchases. This is unlikely to be in the near term as Ueda stated the central bank will assess the market reaction to the recent policy shift.

- Looking ahead, UK retail sales are out, along with the German IFO. In the US the Fed's Barr & Fed's Bostic will speak.

ASIA STOCKS: HK Equities Erase Thursday Gains Down 2-5%,China Equities Down 1-2%

Hong Kong & China equities have pushed lower throughout the day with HK equities erasing all of Thursday's move higher, while the CSI300 has hit a key technical resistance while the weaker yuan isn't helping. The Biden administration is investigating if SMIC violated export rules for chips powering Huawei's Mate 60 Pro, while introducing new restrictions on chip tool shipments to China. Meanwhile, Chinese President Xi Jinping will meet US business leaders to reassure amid declining foreign investment, and a new US bill aims to restrict American investment in certain Chinese stock index products. Additionally, China's NEV retail sales are set to soar in March, with a projected 37% year-on-year and 93% month-on-month surge driven by price cuts.

- Hong Kong equities are lower today after giving up all of yesterday rally, the HSTech Index is down 4.23% which could be tied back to the US investigating is SMIC violated exports rules, while the Mainland property Index is down 2.42%%, the wider HSI is down 3.04%. In China the CSI300 has hit the 200-day EMA has bounced straight off it, the index now trades off 1.46%, while the smaller cap CSI1000 is down 1.69% and ChiNext is also down 1.83%.

- China Northbound flows were -6.02billion yuan on Thursday, with the 5-day average at 3.62 billion, while the 20-day average sits at 2.911 billion yuan.

- A quick wrap of the past week in the China property space, China Builder Radiance defaults on dollar bond, China Vanke secured a 14yr 1.4b yuan loan from Industrial Bank which will be used to repay the companies debts, China Evergrande's $78 Billion has been accused of a $78b fraud in the 2 years prior to defaulting, China State-Owned developer Yuexiu cancels 1B yuan bond issuance.

- The Biden administration is investigating whether China's top chipmaker, SMIC, violated U.S. export rules to produce a chip for Huawei's Mate 60 Pro phone. There are concerns about whether SMIC illegally obtained U.S. tools to manufacture the chip, prompting a review by the administration. Despite pressure from China hardliners, no conclusion has been reached yet. Additionally, the administration announced new restrictions on shipments of chipmaking tools to advanced Chinese chip factories and is urging allies to stop shipments to China as well.

- Chinese President Xi Jinping is set to meet with several US business leaders next week during an annual forum in Beijing, with attendees including figures such as Tim Cook of Apple and Stephen Schwarzman of Blackstone. This meeting follows the China Development Forum, which has seen less publicity than usual, amid efforts by Chinese leadership to reassure foreign companies amid declining investment from abroad.

- A new bill in Congress aims to restrict US mutual funds from investing in certain Chinese stock index products, part of a broader effort targeting investments in China. The legislation seeks to prevent American investors from being misled about the value of Chinese companies, with additional measures proposed to increase scrutiny on Chinese companies' financial practices and their role in US supply chains. However, the bill still faces significant hurdles in Congress before potentially becoming law.

- According to preliminary data from the China Passenger Car Association, retail sales of new energy vehicles (NEVs) in China are expected to surge by 37% year-on-year and 93% month-on-month to reach 750,000 units in March. This increase is attributed to price cuts in NEVs. Additionally, retail sales of passenger vehicles are forecasted to rise by 3.7% year-on-year and 50% month-on-month to 1.65 million units in March.

ASIA PAC STOCKS: Asian Equities Mostly Lower As Tech Names Plunge, Japan Higher

Regional Asian equities are mostly lower on Friday with the exception of Japanese equities, in a sign investors are rethinking the optimism that propelled the region’s shares higher in the prior session, as fresh signs of persistent inflation appeared in the US, tech stocks are the worst performing sector in the region largely being pulled lower by weaker equity prices in the Hong Kong and Chinese markets, while the US Justice department is suing Apple for violating antitrust laws which may also be weighing on the tech sector.

- Japan equities have edged higher today, earlier National CPI missed expectations coming in at 2.8% y/y vs 2.9% expected, Finance Minister Suzuki spoke in Tokyo earlier about FX moves, while BoJ Governor Ueda appeared before parliament, where he mentioned the bank will eventually scale back its bond purchases, but not for the time being. The Topix Bank Index is the top performing sector up 1.61%, the wider Topix Index is up just 0.53%, while the Nikkei 225 broke above 41,000 for the first time earlier, however trades just off those levels now at 40,920 up 0.25% for the day.

- South Korean PPI data was out earlier this morning rising to 1.5% from 1.3% in January, equities are slightly lower in early trading with the Kospi down 0.25% after surging higher Thursday on higher tech prices, while foreign investors flooded the SK equity market on Thursday with $1.678b of inflows.

- Taiwanese equities opened higher this morning, however has turned lower after Asian tech stocks in China & HK plunge, the Taiex is currently down 0.16%. Late on Thursday the Central Bank rose interest rates from 1.875% to 2.00% with analysts suggesting that the Taiwan central bank's unexpected interest rate hike, aimed at addressing inflation concerns, is likely to be the final adjustment for this cycle, with minimal market impact given Taiwan's relatively low policy rate compared to the rest of Asia. Foreign investors bought Taiwan equities on Thursday with $529m of inflows, breaking a run of 5 consecutive days of outflows.

- Australian equities are lower today, as banks weigh on the markets the surge in employment on Thursday has pushed chances of a rate cut back further with just 41bps of cuts priced in for the year. The ASX200 closed down 0.15%

- Elsewhere in SEA, New Zealand Trade Balance narrowed from the month prior coming in at -$218m vs -$1,089m, equities closed up 0.53%, Singapore equities are down 0.35%, Philippines equities down 0.90%, Malaysian equities are down 0.12%, Indonesian equities are unchanged while Indian equities are 0.20% higher.

OIL: Tracking Lower Amid Heightened Risk Aversion/Higher USD

The active Brent front month contract (K4) has weakened today, last near $85.20/bbl. This isn't too far off Thursday lows in US trade (close to $85/bbl). We are down 0.70% so far today and tracking marginally lower for the week at this stage. WTI was last near $80.50/bbl having followed a similar trajectory so far today.

- Sentiment today has been weighed by a firmer USD backdrop, (BBDXY +0.20% and above pre FOMC levels), while China related asset sentiment has faltered in the FX and equity space, another headwind at the margins.

- Developments elsewhere indicated that Israel would invade Rafah no matter what the US states (BBG). Houthi rebels in Yemen also reportedly told Russia and China that its vessels will not be targeted in the red sea as they move through the area.

- For Brent, we sit nearly 3% off recent highs ($87.70/bbl). Still, we are comfortably above all key EMAs, with the 20-day back near $84.10/bbl. A resumption of the up move could bring Oct 20 highs from last year into play (at $88.30/bbl).

GOLD: Down Amidst Firmer USD Backdrop, But Still Up For The Week

Gold sits lower in the first part of Friday trade. The precious metal was last near $2175, around 0.30% weaker for the session so far. This follows Thursday's drop by a similar amount. We did break above $2200 for the first time (highs near $2221) post the FOMC, but these gains weren't sustained.

- Gold has likely faltered amid a stronger USD backdrop, with the BBDXY index back above pre FOMC levels, last close to 1244.0. The risk averse tone evident particularly in equities has likely helped contain the fallout for gold so far in Friday trade. Gold is still up for the week at this stage, last nearly 1% firmer.

- Levels wise, the trend backdrop remains supportive, all key EMAs are trending higher. The 20-day, the nearest to spot, is back at $2136.6. Topside focus will remain on a fresh push back above $2200.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 22/03/2024 | 0700/0700 | *** |  | UK | Retail Sales |

| 22/03/2024 | 0700/0800 | ** |  | DE | Import/Export Prices |

| 22/03/2024 | 0730/0730 | | UK | DMO to release calendar for FQ1 (Apr-Jun) Ops | |

| 22/03/2024 | 0800/0900 |  | EU | ECB's Lagarde in Euro Summit | |

| 22/03/2024 | 0900/1000 | *** | | DE | IFO Business Climate Index |

| 22/03/2024 | 1100/1100 | ** | | UK | CBI Industrial Trends |

| 22/03/2024 | 1230/0830 | ** |  | CA | Retail Trade |

| 22/03/2024 | 1300/0900 |  | US | Fed Listens event | |

| 22/03/2024 | 1400/1500 | ** |  | BE | BNB Business Sentiment |

| 22/03/2024 | 1600/1200 | | US | Fed Vice Chair Michael Barr | |

| 22/03/2024 | 1630/1630 | | UK | BOE to announce APF sales schedule for Q2-24 | |

| 22/03/2024 | 1700/1300 | ** | | US | Baker Hughes Rig Count Overview - Weekly |

| 22/03/2024 | 1700/1800 | | EU | ECB's Lane lecture on inflation and MonPol at AMSE | |

| 22/03/2024 | 2000/1600 | | US | Atlanta Fed's Raphael Bostic |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.