Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Dovish ECB rhetoric (particularly from Villeroy) and heightened geopolitical tensions support core global FI markets, with the former weighing on the EUR.

- Chinese equities finish shy of best levels as property market worry caps/negates early gains.

- The U.S. Treasury’s borrowing estimates headline today’s light docket, coming ahead of Wednesday’s full refunding announcement. Otherwise, Dallas Fed manufacturing index rounds off the regional Fed manufacturing surveys for January.

MNI UST Issuance Deep Dive: Feb 2024 - Refunding Preview

Treasury’s Quarterly Refunding process for the Feb-Apr quarter begins with borrowing estimates released on Mon Jan 29 (0830ET), followed by the refunding announcement itself on Wed Jan 31 (also 0830ET).

- As we noted in our mini-preview earlier in January, there will be three key elements to watch in the refunding announcement itself: the main thing will be the projected increases in Treasury coupon sizes, but also worth noting are the guidance for future quarters, and the (likely) announcement of a buyback program. We elaborate on those in this preview, in addition to the outlook for Monday’s borrowing estimates.

- Virtually all analysts whose previews we have seen expect a similar increase across coupon sizes as seen in the November round, though there are some variations.

- While aggregate nominal coupon amounts wouldn't quite reach the 2021 monthly highs ($336B), the next quarter would mark new records for sizes in the 2Y, 5Y, and 10Y and equal it for the 3Y.

- There is some near-term uncertainty over the borrowing requirements generated by multiple factors including Fed QT.

- This preview includes noteworthy observations from 14 analyst refunding previews.

- Please see PDF for full analysis: MNI_US_DeepDive_Issuance_2024_FebruaryRefunding.pdf

MNI ECB Review - January 2024: Inching Closer To Cutting Rates

The ECB left policy unchanged at the January meeting and although there were no material surprises in the press conference, the underlying messages were notably dovish.

- The words “domestic prices pressures remain elevated” from the December press statement were removed, President Lagarde sounded optimistic on inflation trends and, despite stating that it was premature to discuss rate cuts (presumably as of the January meeting), she did not forcefully push back against the possibility of a policy rate cut in the spring.

- If the ECB operates on a data dependent basis, as often stressed by President Lagarde, then in theory no future policy meeting can ever be off the table. We would still argue that absent a marked shift in the economic and inflation data, June seems the earliest time that the ECB would consider a cut.

- For the full publication, please see: ECB Review January 2024.pdf

US TSYS: Richer, Borrowing Estimates To Kick Start A Heavy Week

- Cash Tsys trade 2-3.5bp richer, building through the overnight session but seemingly buoyed primarily by dovish ECB speak and increased geopolitical tensions with US troop deaths in Jordan over the weekend.

- TYH4 at 111-13 is off today’s high of 111-15+ but remains within yesterday’s range, on solid volumes of 310k. It sits close to resistance at 111-18 (20-day EMA) but the bear cycle is seen as remaining in play, with support at 110-26 (Jan 19 low).

- Treasury’s borrowing estimates at 1500ET headline today’s light session, coming ahead of Wednesday’s full refunding announcement. Otherwise, Dallas Fed manufacturing index rounds out the regional Fed mfg surveys for January.

- Data: Dallas Fed Mfg Jan (1030ET)

- Bill issuance: US Tsy $79B 13W, $70B 26 Bill auctions (1130ET)

US TSY FUTURES: OI Points To Mix Of Short Setting & Long Cover

The combination of the downtick in Tsy futures and preliminary OI data points to the following positioning swings ahead of the weekend.

- Net short setting: TU & FV futures.

- Net long cover: TY, UXY, US & WN futures

- Net OI DV01 equivalent swings were fairly contained, with UXY futures seeing the largest net contract swing and the net curve positioning swing tilted towards long cover.

| 26-Jan-24 | 25-Jan-24 | Daily OI Change | OI DV01 Equivalent Change ($) | |

| TU | 3,966,681 | 3,954,092 | +12,589 | +462,029 |

| FV | 5,945,708 | 5,939,814 | +5,894 | +252,001 |

| TY | 4,713,624 | 4,716,288 | -2,664 | -170,418 |

| UXY | 2,104,820 | 2,119,503 | -14,683 | -1,338,605 |

| US | 1,420,808 | 1,421,552 | -744 | -100,109 |

| WN | 1,658,988 | 1,663,582 | -4,594 | -965,348 |

| Total | -4,202 | -1,860,450 |

STIR: Fed Rates Hold Recent Ranges With FOMC Looming

Fed Funds implied rates sit modestly lower from Friday’s close, primarily following dovish ECB speak and increased geopolitical tensions over the weekend.

- It leaves the rate path within recent ranges, with 13.5bp of cumulative cuts for March, 34bp for May, 59bp for June and 136bp for Dec.

- The Dec’24 implied rate of 3.97% has kept to a rough 3.90-4.02% range in recent sessions, having lifted off levels closer to 3.7% prior to Waller’s Jan 16 comments on not needing to cut as quickly as in past cycles.

- Today sees a quiet docket before JOLTS tomorrow and Wednesday's ECI/ADP data ahead of the FOMC decision.

STIR: OI Points To Mix Of Short Setting & Long Cover Across Most Of SOFR Strip On Friday

The combination of the general move lower in SOFR futures on Friday and preliminary OI data points to the following net positioning swings ahead of the weekend:

- Whites: An apparent mix of short cover (SFRZ3), long cover (SFRH4 & U4) and short setting (SFRM4)

- Reds: An apparent mix of net long cover (SFRH5 & U5) and short setting (SFRZ4 & M5), with the latter slightly more pronounced in net pack terms.

- Greens: Apparent net long cover was seen in all contracts.

- Blues: An apparent mix of net short setting (SFRZ6 & U7) and long cover (SFRH7 & M7), with the latter dominating in net pack terms.

| 26-Jan-24 | 25-Jan-24 | Daily OI Change | Daily OI Change In Packs | ||

| SFRZ3 | 1,201,813 | 1,203,023 | -1,210 | Whites | +5,653 |

| SFRH4 | 1,215,479 | 1,230,139 | -14,660 | Reds | +1,794 |

| SFRM4 | 1,146,387 | 1,123,208 | +23,179 | Greens | -24,531 |

| SFRU4 | 990,925 | 992,581 | -1,656 | Blues | -2,768 |

| SFRZ4 | 1,045,488 | 1,039,767 | +5,721 | ||

| SFRH5 | 536,504 | 539,678 | -3,174 | ||

| SFRM5 | 649,665 | 640,326 | +9,339 | ||

| SFRU5 | 567,190 | 577,282 | -10,092 | ||

| SFRZ5 | 623,759 | 636,298 | -12,539 | ||

| SFRH6 | 418,607 | 422,465 | -3,858 | ||

| SFRM6 | 416,532 | 419,122 | -2,590 | ||

| SFRU6 | 297,393 | 302,937 | -5,544 | ||

| SFRZ6 | 268,720 | 266,899 | +1,821 | ||

| SFRH7 | 131,752 | 135,166 | -3,414 | ||

| SFRM7 | 147,446 | 148,811 | -1,365 | ||

| SFRU7 | 148,860 | 148,670 | +190 |

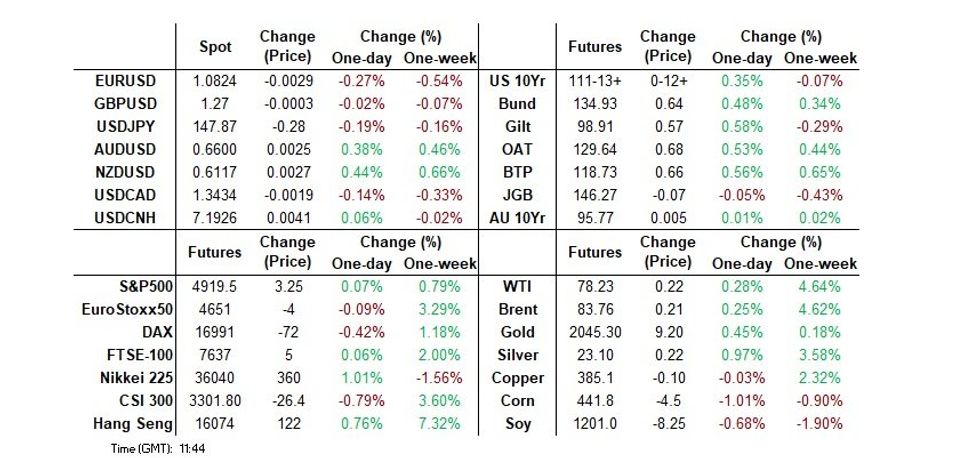

FOREX: A Very Busy Week Ahead

The Dollar was underpinned overnight, going into the European session, after Equity futures gaped lower led by US Troops killed in Jordan and a Tanker was hit in the red sea.

- Equities have since recovered during the early European session, and the Dollar has also pared gains to trade mixed against G10s.

- Best performers are NZD, AUD, CHF and Yen in that order, while the SEK and the EUR are leaning in the red.

- Lower US Yields has kept the USDJPY close to its traded low of 147.71, now trading at 147.83.

- The EUR is offered in G10 so far today, as German Yield drifts lower, and Dovish ECB speakers have kept the lid on the EUR.

- Besides the SEK, which is down a small 0.06%, the EUR trades in the red versus all the majors.

- Some will look at 1.0813 in EURUSD, Friday's low for support, but better is seen at 1.0793 50.0% retracement of the Oct - Dec bull leg.

- Looking ahead, there's no notable data for the session, but this week will be the busiest week so far this year, with Data, Risk Events (CBs), Earnings, Month End and supply.

FX OPTIONS: Expiries for Jan29 NY cut 1000ET (Source DTCC)

- EURUSD: 1.0800 (569mln), 1.0820 (307mln), 1.0825 (200mln), 1.0840 (400mln), 1.0850 (427mln), 1.0890 (279mln), 1.0900 (1.02bn).

- USDJPY: 148.50 (449mln).

- GBPUSD: 1.2700 (672mln).

- USDCAD: 1.3460 (400mln).

- AUDUSD: 0.6570 (300mln), 0.6585 (373mln).

- NZDUSD: 0.6075 (390mln).

- USDCNY: 7.2000 (640mln).

EGBS: Futures Close To Session Highs Following Dovish STIR Feed Through

Core/semi-core EGBs trade at session highs as moves in STIR/ECB-dated OIS markets support the wider FI space, following dovish ECB communication this morning/over the weekend.

- Bank of Portugal Governor Centeno struck a familiarly dovish rhetoric in a RTRS interview released this morning (echoing a similar sentiment to that first reported by MNI before the turn of the year. See here)

- This added to weekend comments from BdF's Villeroy (who is seen as being more reflective as the ECB consensus), who noted "everything will be open at our next meetings".

- The above comments have seemingly outweighed hawkish pushback from Knot and Kazimir, while Vice President de Guindos struck a balanced tone similar to last week's ECB presser.

- Bunds are +79 ticks at 135.08 at typing. A clear break of 135.02 (Jan 26 high) is required to ease bearish pressure. OAT and BTP futures are also around +80 on the day.

- The German and French short-ends lead the rally and promote a bull steepening dynamic, with 2/5-year yields 8-9bps lower today.

- Periphery spreads are generally tighter, with the exception of GGBs.

- Syndication mandates for a new 30-year DBR benchmark and 10-year GGB have just been announced. MNI expects the German 30-year to have a size of E3-4bln, and the Greek 10-year a size of E3.0-3.5bln.

- Today's regional calendar is light, with the week's main focus on the January flash inflation data round (though Q4 '23 flash GDP prints and manufacturing PMI readings will also garner attention). ECB's de Guindos is scheduled to speak again (1310GMT).

EUROPEAN ISSUANCE UPDATE

GILTS: Comfortably Firmer On The Day, Local Inflation Exp. Data Supports Alongside Wider Bid

Gilts continue to look to wider core global FI markets for direction, with dovish ECB speak and heightened geopolitical tensions helping futures move higher and yields lower.

- Gilt futures sit 53 ticks higher on the day at 98.87, with bulls running out of steam just ahead of 99.00 (session high of 98.99).

- A break of 99.00 would expose the 20-day EMA (99.43). A clear break of that level is needed to ease the bearish pressure.

- Cash gilt yields are 2.5-4.5bp lower, with 10s leading the rally.

- Local inputs saw a continued moderation in the Citi/YouGov 1-Year ahead inflation expectation metric, which would have provided some background support.

- Note that the 1-Year ahead measure in that survey moved to fresh cycle lows, but the longer run measure sits 0.2ppt above its own ’23 base.

- On the other hand, continued speculation re: UK fiscal loosening (the potential for further National Insurance cuts got airtime in the local press via weekend source reports) will have provided some (modest) counter, which capped the bid at the open, before a second round of demand came in.

- SONIA futures are -0.5 to +6.5 through the blues, with a light twist flattening bias.

- BoE-dated OIS stabilises showing 107-108bp of cuts through ’24, with ’24 contracts running little changed to 3.5bp softer on the day.

- The BoE will conduct APF sales from its short maturity bucket later today.

| BoE Meeting | SONIA BoE-Dated OIS (%) | Difference Vs. Current Effective SONIA Rate (bp) |

| Feb-24 | 5.201 | +1.3 |

| Mar-24 | 5.171 | -1.7 |

| May-24 | 5.063 | -12.5 |

| Jun-24 | 4.895 | -29.3 |

| Aug-24 | 4.675 | -51.2 |

| Sep-24 | 4.482 | -70.5 |

| Nov-24 | 4.265 | -92.3 |

| Dec-24 | 4.107 | -108.0 |

EQUITIES: EUROSTOXX 50 Futures Clear Resistance

- The uptrend in S&P E-Minis remains intact. Resistance at 4841.50, the Dec 28 high, has recently been cleared, confirming an extension of the price sequence of higher highs and higher lows. Sights are on 4952.45 next, the 1.382 projection of Nov 10 - Dec 1 - 7 price swing. Initial support lies at 4522.80, the 20-day EMA.

- EUROSTOXX 50 futures traded sharply higher last week, resulting in a move through key resistance at 4634.00, the Dec 14 high. The break confirms a resumption of the medium-term uptrend and opens 4662.90 next, the 1.236 projection of the Nov 8 - 24 - 28 price swing, ahead of the 4700.00 handle. Initial support lies at 4522.80, the 20-day EMA.

CHINA STOCKS: Mixed Performance, Evergrande Liquidation Order Knocks Space Off Best Levels

MNI (London) - Benchmark indices finished shy of best levels on Monday.

- The CSI 300 shed 0.9%, while the Hang Seng was 0.8% firmer.

- That came after a fade/reversal of the initial support derived from the CSRC’s announcement re: fully suspending the lending of restricted shares, as it looks to shore up the troubled equity market.

- The pressure came on news that embattled developer Evergrande and its creditors were unable come to a restructuring agreement, resulting in HK courts ordering the liquidation of the company.

- Lingering worry surrounding potential U.S. action vs. Chinese AI & biotechnology names was also flagged.

- There was some counter on that front, with U.S. National Security Advisor Sullivan and China’s Foreign Minister Wang Yi discussing a call between the two countries’ Presidents, per wire source reports. The reports suggested this call could come as soon as the Spring.

- There were also suggestions that a Sino-U.S. call on fentanyl will be held next week.

- News that the city of Guangzhou has relaxed home purchase limits for buyers with local residency helped support the property sector before the Evergrande news weighed.

- Major news outlets flagged comments from analysts pointing to the potential for deeper easing re: property markets in the large cities, along with lower mortgage rates.

- Elsewhere, local wires noted that China will guide listed SOEs to focus on market performance/valuation, with an eye on better rewards for investors (another layer of policymaker support for the broader market).

- Participants and brokerages seem to expect further market-supportive measures.

- We also saw reports of a potential merger of three of the country’s largest bad debt managers under China’s sovereign wealth fund umbrella.

- Net flows re: the mainland via the HK-China Stocks Connect scheme were essentially neutral (CNY0.6bn of net selling).

COMMODITIES: Bull Cycle In Oil Futures Remains In Play

- Gold continues to trade above the Jan 17 low of $2001.9. The recent print below the 50-day EMA and the break of $2013.4, the Jan 11 low, has strengthened a bearish threat and a resumption of weakness would open a key level at $1973.2, the Dec 13 low. For bulls, clearance of 2062.3, the Jan 12 high, is required to signal a reversal.

- In the oil space, WTI futures traded higher last week. The contract has breached resistance at $76.31, the Dec 26 high. The clear break of this hurdle highlights a stronger short-term bullish condition. A continuation higher would signal scope for a climb towards $79.56, the Nov 30 high. On the downside, initial key support lies at $74.55, the 50-day EMA. A break would be a bearish development.

| Date | GMT/Local | Impact | Flag | Country | Event |

| 29/01/2024 | 1310/1410 |  | EU | ECB's de Guindos at Investment Outlook Conference | |

| 29/01/2024 | 1530/1030 | ** |  | US | Dallas Fed manufacturing survey |

| 29/01/2024 | 1630/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 29/01/2024 | 1630/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 30/01/2024 | 2330/0830 | * |  | JP | labor forcer survey |

| 30/01/2024 | 0001/0001 | * |  | UK | BRC Monthly Shop Price Index |

| 30/01/2024 | 0030/1130 | ** |  | AU | Retail Trade |

| 30/01/2024 | 0630/0730 | ** |  | FR | Consumer Spending |

| 30/01/2024 | 0630/0730 | *** | | FR | GDP (p) |

| 30/01/2024 | 0800/0900 | *** |  | ES | HICP (p) |

| 30/01/2024 | 0800/0900 | *** | | ES | GDP (p) |

| 30/01/2024 | 0800/0900 | ** |  | CH | KOF Economic Barometer |

| 30/01/2024 | 0800/0900 | ** |  | SE | Economic Tendency Indicator |

| 30/01/2024 | 0900/1000 | *** |  | IT | GDP (p) |

| 30/01/2024 | 0900/1000 | ** | | IT | PPI |

| 30/01/2024 | 0900/1000 | | EU | ECB's Lane on 'a year with the euro in Croatia' | |

| 30/01/2024 | 0900/1000 | *** |  | DE | GDP (p) |

| 30/01/2024 | 0930/0930 | ** | | UK | BOE M4 |

| 30/01/2024 | 0930/0930 | ** | | UK | BOE Lending to Individuals |

| 30/01/2024 | 1000/1100 | *** | | EU | EMU Preliminary Flash GDP Q/Q |

| 30/01/2024 | 1000/1100 | *** | | EU | EMU Preliminary Flash GDP Y/Y |

| 30/01/2024 | 1000/1000 | * | | UK | Index Linked Gilt Outright Auction Result |

| 30/01/2024 | 1000/1100 | ** | | EU | EZ Economic Sentiment Indicator |

| 30/01/2024 | 1000/1100 | * | | EU | Consumer Confidence, Industrial Sentiment |

| 30/01/2024 | 1355/0855 | ** | | US | Redbook Retail Sales Index |

| 30/01/2024 | 1400/0900 | ** | | US | S&P Case-Shiller Home Price Index |

| 30/01/2024 | 1400/0900 | ** | | US | FHFA Home Price Index |

| 30/01/2024 | 1400/0900 | ** | | US | FHFA Home Price Index |

| 30/01/2024 | 1500/1000 | *** | | US | Conference Board Consumer Confidence |

| 30/01/2024 | 1500/1000 | ** | | US | housing vacancies |

| 30/01/2024 | 1500/1000 | *** | | US | JOLTS jobs opening level |

| 30/01/2024 | 1500/1000 | *** | | US | JOLTS quits Rate |

| 30/01/2024 | 1530/1030 | ** | | US | Dallas Fed Services Survey |

| 30/01/2024 | 1630/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 31/01/2024 | 2350/0850 | * | | JP | Retail sales (p) |

| 31/01/2024 | 2350/0850 | ** | | JP | Industrial production |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.