Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS:

- Vaccine rollout risk across Europe remains a focus, MHRA, EMA judgement awaited

- EUR/USD bounce extends, tops 200-dma

- Fedspeak awaited, with four speeches and FOMC minutes due

US TSYS SUMMARY: Belly Outperforming, FOMC Minutes Eyed

A modestly risk-off overnight session has seen Treasuries continue to edge higher, with the belly outperforming.

- Jun 10-Yr futures (TY) up 4.5/32 at 131-26.5 (L: 131-18.5 / H: 131-30). High was hit early in the European session, where there was some attention on regulators' decisions on the safety of the AstraZeneca vaccine (EU authority holds presser at 1000ET).

- The 2-Yr yield is down 0.4bps at 0.1527%, 5-Yr outperforming w yield down 1.9bps at 0.8528%, 10-Yr down 1.4bps at 1.642%, and 30-Yr down 1.2bps at 2.3106%.

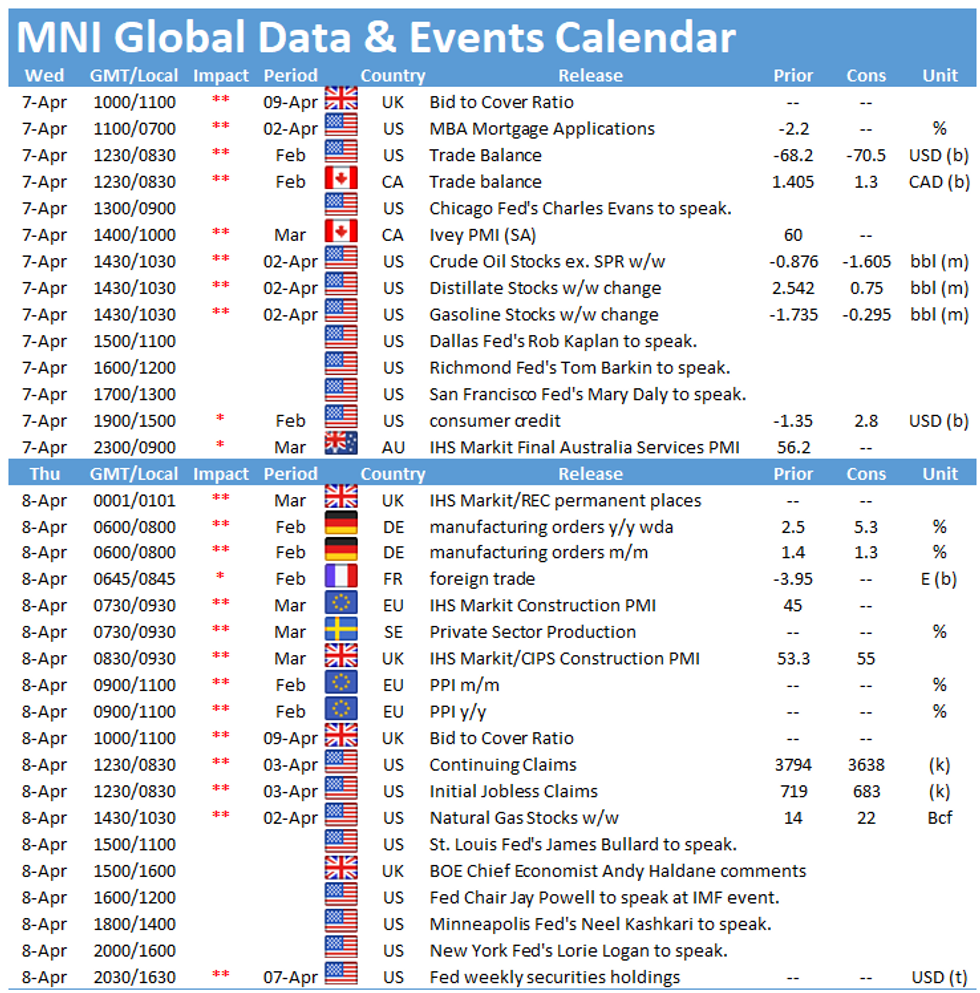

- Minutes from the March FOMC meeting out at 1400ET. Fed speakers today include Chicago's Evans (0900ET), Dallas's Kaplan (1100ET), Richmond's Barkin (1200ET), and SF's Daly (1300ET).

- WSJ published an interview w Kaplan this morning in which he describes his thinking behind his 2022 hiking dot in the Summary of Economic Projections, and discussed his thoughts on pre-emptive vs reactive monetary policy and "the difference between being accommodative or even highly accommodative and keeping rates at zero".

- Otherwise, a light calendar - Feb trade balance data at 0830ET and Feb consumer credit at 1500ET.

- In supply, 1130ET sees auction of $35B of 119-day bills. NY Fed buys ~$6.025B of 4.5-7Y Tsys.

EGB/GILT SUMMARY - EGBs Stay Better Bid

EGBs stays better bid, underpinned as the US starts to join the session.

- Bund has brushed aside the Bobl supply with focus turning to risk event today.

- EMA is scheduled to have a presser at 15.00 UK time/10.00ET, regarding the Astra vaccine.

- As such core FTQ have been favoured so far today.

- Gilt have followed suit, but have lagged somewhat behind, with some Heavy UK supplies, equating to some 53k Gilts.

- ALL EYES here are also on Astra concerns, as the market awaits on the UK regulators and what they might decide on Astra and younger people.

- No set time or date yet regarding a UK announcement.

- Looking ahead, focus is on the risk events noted above, and out of the US, sees a few Fed speakers on the Economy, including Fed Evans, Barkin, Daly, while Fed Kaplan is in a Panel hosted by UBS.

- FOMC minutes is also due, but most desk don't expect to much, but will still be watched

EUROPE ISSUANCE: UK & German Auctions, Italian & Portuguese Syndications

UK DMO sells GBP2bln 0.875% Jan-46 gilt, Avg yield 1.332%, Bid-to-cover 2.54x

- Sells GBP3bln of 0.375% Oct-26 gilt, Avg yield 0.468% (Prev. 0.454%), Bid-to-cover 2.56x (Prev. 2.53x)

Germany allotted E3.307bln 0% Apr-26 Bobl, Avg yield -0.66% (Prev. -0.62%), Bid-to-cover 1.41x (Prev. 1.38x)

Italian Syndication - Dual-tranche:

- 0.25% Mar-28 BTP tap, Final Spread BTPS +9bps

- New 1 Mar 2072 BTP, Final Spread BTPS +47bps

Portuguese Syndication:

- New 10Y PGB Benchmark, spread set MS +28bps

EUROPE OPTION FLOW SUMMARY

Eurozone:

RXK1 171/170ps, bought for 18 in 3.25k

RXK1 168.5p, bought for 3 in 5k

OEM1 134.75/134.50ps 1x1.5, bought for 1.25 in 5k

OEM1 134.75/134.50ps 1x1.5, bought for 1.5 in 5k

OEM1 135.75c, bought for 11 in 2.5k

ERZ2 100.50p, bought for 11.5 in 3k (ref 100.525)

2RM1 100.50/100.37/100.25p fly vs 0RM1 100.50p, bought the fly for 1.5 in 1.5k

UK:

0LU1 99.75^, sold at 17.5 in 1.45k

FOREX: EUR Recovery Continues, Hitting April High

- CHF, EUR are among the session's strongest performers Wednesday, indicating a modest risk-off feel - although equity futures are holding the bulk of the week's gains ahead of the NY crossover. The USD index holds just below the 200-dma at 92.427.

- Caution and concern over vaccine rollouts across Europe remain a market focus, with both UK and EU medicines regulators due to give their judgements on the AstraZeneca vaccine as soon as today. A negative judgement would be a considerable hurdle to re-opening plans across the UK and the continent, so remains a key market risk.

- PMI revisions for March across the Eurozone generally fared a little better than expected, helping nudge the Eurozone composite PMI to its best level since July last year.

- US & Canadian trade balance, Canada's Ivey PMI and the FOMC minutes are highlights Wednesday, as well as speeches from Fed's Evans, Kaplan, Barkin & Daly. G20 FinMins also hold a press conference.

FX OPTIONS: Expiries for Apr07 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1800-10(E775mln), $1.1825-35(E1.3bln), $1.1850(E1.1bln-EUR puts), $1.1925-35(E915mln), $1.1940-50(E743mln)

- USD/JPY: Y107.95-05($893mln), Y108.15-25($1.2bln), Y109.00($1.4bln), Y109.75($500mln), Y109.80-85($510mln), Y109.95-110.00($2.9bln, mainly USD puts)

- EUR/GBP: Gbp0.8550-55(E950mln-EUR puts)

- AUD/USD: $0.7450(A$709mln), $0.7610-20(A$591mln), $0.7705-20(A$732mln)

- USD/CNY: Cny6.60($1.7bln-USD puts)

Price Signal Summary - Equity Space Bullish Mood Intact

- In the equity space:

- S&P E-minis are consolidating and bullish trend conditions remain intact. The focus is on 4080.99, 1.236 projection of the Feb 1 - Feb 16 - Mar 4 price swing.

- EUROSTOXX 50 bullish activity extends with the index approaching 4000.00. A break would open 4047.72, 2.236 projection of the Dec 21 - Jan 8 - Jan 28 price swing

- In the FX world, EURUSD continues to climb as the correction extends. The focus is on 1.1900 and 1.1944, the 50-day EMA. The moving average highlights a key resistance. The GBPUSD outlook remains bearish. Recent gains have stalled at the former bull channel base drawn off the Nov 2 low. Resistance has been defined at 1.3919, yesterday's intraday high. EURGBP rallied yesterday. The price pattern is a bullish engulfing candle. This exposes the next key resistance zone at 0.8646, Mar 24 high and S/T reversal trigger and 0.8654, 50-day EMA. USDJPY remains bullish but has entered a corrective phase. The next support is at 109.31, 20-day EMA.

- On the commodity front:

- Gold is holding onto recent gains. Key resistance is at $1755.5, Mar 18 high, where a break is required to suggest scope for a stronger bounce.

- Brent (M1) key directional triggers are:

- Resistance at $65.39, Mar 29 high and key support at $60.33, Mar 23 low and the bear trigger

- WTI (K1) directional triggers are:

- Resistance at $62.27, Mar 30 high and support at $57.25, Mar 23 low and the bear trigger

- In the FI space, Bunds (M1) remain vulnerable despite recent gains. Key support to watch is at 170.52, Mar 18 low. The key support and bear trigger in Gilts (M1) is at 126.79, Mar 18 low.

EQUITIES: Stocks Mixed, Europe Lags While US Futures Remain Firm

- European indices are mixed ahead of Wednesday NY hours, with UK's FTSE-100 outperforming while Spanish, Italian markets lag and the EuroStoxx50 sits lower by 0.2%.

- Across the Stoxx600, real estate, utilities and communication services firms are at the top of the pile, while healthcare and tech names are anchoring European indices.

- Stocks tied to economic re-opening remain strong, suggesting an underlying strength in the vaccine investment thesis, as Deutsche Lufthansa and Carnival are among the best performing names on the continent.

- In futures space, the three main US indices are higher, indicating a better open on Wall Street later today. Tech-led NASDAQ futures are strongest, higher by around 0.2%, while the S&P and Dow Jones futures are just above unchanged.

COMMODITIES: A Relatively More Muted Session for Crude

- WTI crude futures continue to oscillate either side of the 50-dma ($60.29 for the continuation contract) in a relatively more muted session so far for oil markets. The quieter markets come despite reports in the Middle East that an Iranian-flagged carrier came under attack in the Red Sea - a relevant point ahead of key discussion in Vienna between the EU, Iran and US.

- Weekly DoE crude oil inventories take focus going forward, with markets expecting the figures to have shown a 1.6mln bbl draw in reserves over the most recent week of data.

- In precious metals markets, both gold and silver are in very minor negative territory despite some further weakness in the US dollar so far Wednesday. Persistent equity strength may be weighing, with the e-mini S&P holding just below this week's all time highs printed at 4,076.00.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.