Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS:

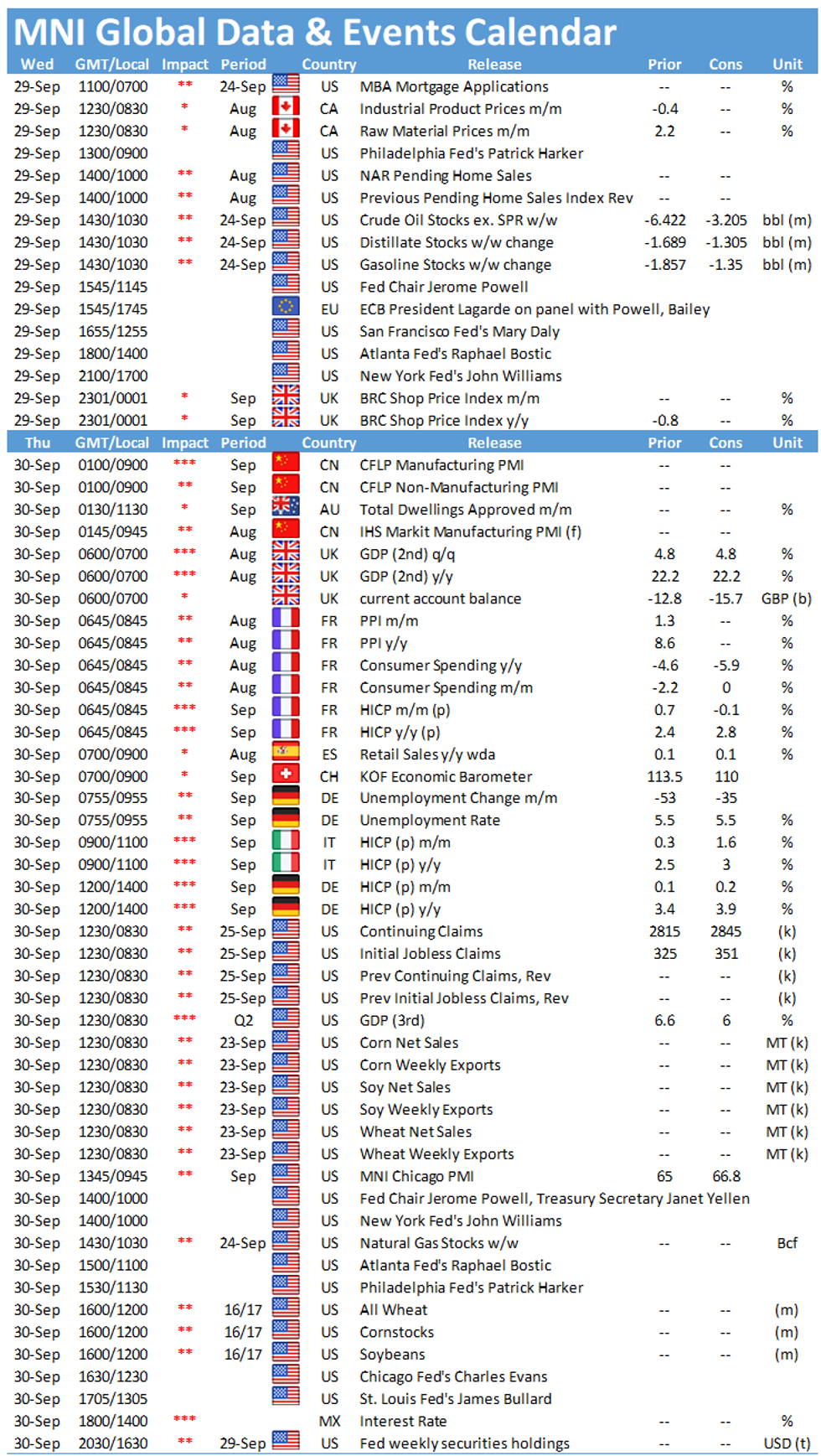

- Markets stabilize, equities off lows, curve inches off steepest levels

- Debt ceiling in focus, government shutdown possible within days

- Central bank speak in focus, with Powell, Lagarde, Bailey and Kuroda appearing on a panel

US TSYS: Steepening Partially Reverses With FOMC Speakers, Gov't Shutdown Eyed

The Treasury curve has unwound some of Tuesday's sell-off / steepening in European morning trade Wednesday, with the long end outperforming

- 10Y and 30Y 6+bp off highs of last 24 hrs. 2-Yr yield down 0.4bps at 0.297%, 5-Yr down 3.2bps at 0.9874%, 10-Yr down 4.3bps at 1.4942%, 30-Yr down 4.4bps at 2.042%.

- Dec 10-Yr futures (TY) up 10/32 at 131-25 (L: 131-10 / H: 131-25.5), 560+k traded.

- Global core bonds have seen gains alongside a rebound in equities, ie a partial reversal of Tuesday's moves (though the dollar remains on the front foot).

- Another heavy Fed speaker slate today: Philly's Harker at 0900ET, Powell (w his BoE, BOJ, and ECB counterparts) on ECB Forum panel at 1145ET, SF's Daly at 1300ET, and Atl's Bostic at 1400ET.

- Government shutdown looms Thurs night without a bill passed to avert; Congress could vote as soon as today on funding Gov't through Dec 3, per various news outlets.

- Meanwhile the House Rules Committee meets this morning to prepare a debt limit suspension through mid-Dec 2022 - though that's likely to be blocked by Senate Republicans.

- On that note, supply today: $30B 119-day bills (1130ET). NY Fed buys ~$2.025B of 22.5-30Y Tsys.

- Conversely, quiet on the data front: weekly MBA mortgage apps at 0700ET and Aug pending home sales at 1000ET.

EGB/GILT SUMMARY - Unwind some of the sell off

EGBs unwinds some of yesterday's sell off, which looks more corrective.

- Bund tested initial yield target at -0.18% yesterday, and yield have moved lower this morning, as the future trades back above the 170 handle.

- Volumes have once again been decent, but moves have been calmer.

- Peripheral spreads are all tighter this morning, Italy lead by 2.8bps versus the German 10yr.

- Gilts have mostly traded inline with Bunds, translating in a flat Gilt/Bund spread, but we are nonetheless still trading close to that 2019 peak at 121.01 (also widest since 2016), now at 119.1.

- Looking ahead, we no tier 1 data out of the US, and most of the focus will be on another packed session full of speakers, which today includes, ECB Centeno, Stournaras, Maklouf, Lane, Guindos, Lagarde, Elderson, Fed Powell, Daily, Bostic, and BoE Bailey

- Dec Bund futures (RX) up 37 ticks at 170.23 (L: 169.61 / H: 170.23)

- Germany: The 2-Yr yield is down 0.6bps at -0.689%, 5-Yr is down 1.5bps at -0.564%, 10-Yr is down 2.2bps at -0.221%, and 30-Yr is down 2.4bps at 0.24%.

- Dec Gilt futures (G) up 19 ticks at 125.76 (L: 125.6 / H: 125.88)

- UK: The 2-Yr yield is down 1.9bps at 0.39%, 5-Yr is down 2bps at 0.608%, 10-Yr is down 2.2bps at 0.972%, and 30-Yr is down 2.2bps at 1.303%.

- Dec BTP futures (IK) up 66 ticks at 152.63 (L: 151.88 / H: 152.66)

- Dec OAT futures (OA) up 42 ticks at 166.39 (L: 165.76 / H: 166.39)

US: Senate Could Vote Today On Stopgap To Avoid Gov't Shutdown

Chad Pergram at FOX News tweets: "Senate could vote on stopgap bill to avert a shutdown today. Then send it to the House. Bill would be "clean" without debt limit increase"

- Senate Republicans have demanded the separation of the gov't funding measure from that of the debt ceiling suspension.

- Several GOP senators have stated that they could support a gov't funding measure that also delivers aid to hurricane-battered states.

- The 'clean' legislation would also not contain the USD1bn funding to replenish Israel's 'iron dome' defence system, which was depleted during the Gaza conflict with Hamas earlier this year.

FOREX: GBP Weakness Pervades as Cable Shows Through Tuesday Low

- For a second session, GBP is the poorest performer in G10, with GBP/USD through the Tuesday low of 1.3521. Explanations are broad and varied, with some positing the images of fuel shortages and supply chain woes are raising the spectre of stagflation, however a number of sell-side analysts are pinning price action on month/quarter-end rebalancing, an effect that may persist into the Thursday fix.

- The broader risk-off themes present in Tuesday trade have faded slightly, with the spike in US Treasury yields abating and European stock markets recovering. Nonetheless, JPY is making solid headway as USD/JPY reverses off the 2021 highs printed overnight at 111.68.

- Lastly, the USD Index showed through the mid-August highs of 93.729 high, improving the near-term outlook further. This opens gains toward levels not seen since early November last year at 94.302.

- Tier one data releases are few and far between Wednesday, keeping focus on the ongoing ECB Sintra forum. Highlights today include ECB's Centeno, Stournaras, Makhlouf & Lane, Fed's Harker, Daly & Bostic and the headline appearances from Powell, Lagarde, Bailey and Kuroda at a joint panel.

FX OPTIONS: Expiries for Sep29 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1700($994mln), $1.1750(E1.2bln), $1.1800-15(E709mln)

- USD/JPY: Y109.90-00($1.3bln), Y111.00-05($558mln)

- GBP/USD: $1.3680(Gbp997mln)

- USD/CAD: C$1.2620($1.4bln), C$1.2630-40($531mln), C$1.2900($2.0bln)

- USD/CNY: Cny6.4400($1bln), Cny6.4965($700mln)

Price Signal Summary - Bond Market Reprieve

- In the equity space, S&P E-minis sold off sharply yesterday and are trading below the 50-day EMA once again - the average intersects at 4407.78 and represents initial resistance. A deeper sell-off would highlight the risk of a pullback towards key support at 4293.75, Sep 20 low. EUROSTOXX 50 futures have also pulled away from recent highs. A deeper pullback would expose the key support at 3974.00, Sep 20 low. 4115.40, the 50-day EMA represents initial resistance.

- In FX, EURUSD remains in a downtrend. The pair has probed support at 1.1664, Aug 20 low. A clear break would confirm a resumption of the broader downtrend and open 1.1621, 1.00 projection of the Jan 6 - Mar 31 - May 25 price swing. GBPUSD remains under pressure following yesterday's sell-off. The focus is on 1.3462, 50.0% retracement of the Sep '20 - Jan bull phase. USDJPY has traded through 110.80, Aug 11 high this week and has today probed key resistance at 111.66, Jul 2 high and the bull trigger. A clear break would strengthen a bull case and open 112.23, Feb 20, 2020 high. The USD Index (DXY) key resistance at 93.73, Aug 20 high has been breached. The break confirms a resumption of the uptrend that started May 25 and reinforces the general bullish USD theme.

- On the commodity front, the Gold traded lower yesterday and the trend needle still points south. The focus is on $1742.5, 76.4% of the Aug 9 - Sep 3 rally. WTI futures have pulled away from yesterday's high of $76.67. Dips are considered corrective and firm support is seen at $73.58, Jul 6 high and a recent breakout level.

- In FI, Bund futures remain in a clear downtrend with the focus on 169.46 next, 1.50 projection of the Sep 9 - 17 - 21 price swing. Short-term gains are considered corrective. Gilt futures remain heavy despite the rebound from yesterday's low of 124.84. Resistance is seen at 126.44, Sep 24 high. Treasuries remain in a downtrend. Scope is seen for weakness towards 131-03+, Jun 25 low. Gains are also considered corrective.

EQUITIES: Markets Bouncing, But Recovery Shallow

- Stock markets are bouncing ahead of the Wednesday NY open, with mainland European markets higher by 1% or so, although the bounce is still comfortably shy of the Tuesday high. The recovery is led by the hardest hit sectors from earlier in the week, with consumer discretionary and tech names leading the nascent recovery.

- The same pattern is repeated across US futures, with the NASDAQ future higher by 1% or so, while the e-mini S&P and Dow Jones follow suit with more mild gains.

- Despite the recovery across Asia-Pacific and European trading hours, S&P E-minis are back below the 50-day EMA - the average intersects at 4407.78. A deeper sell-off would highlight a bearish threat and the risk of a pullback towards the key support at 4293.75, Sep 20 low. Price needs to break above 4472.00, Sep 27 high to reinstate the recent bullish theme. This would expose the bull trigger at 4359.50, the Sep 3 high.

COMMODITIES: Oil Off Highs, But Remains Bullish

- WTI and Brent crude futures sit above the overnight lows, but are yet to make any headway toward the cycle highs printed earlier in the week. WTI eked out a high of $76.67 Tuesday, with Brent outperforming slightly to touch $80.75 before fading.

- Both oil benchmarks sit modestly lower ahead of the NYMEX open, but the short-term bullish themes are intact following the recent build-up in expectations for tight supply across the winter months.

- Gold is bearish and traded lower yesterday. The metal last week cleared former support at $1742.3, Sep 20 low. This confirmed a resumption of the current short-term bear cycle and signals scope for a move towards $1742.5, 76.4% of the Aug 9 - Sep 3 rally. A breach of this level would open the key support at $1690.6 further out, Aug 9 low.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok