Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Firmer-than-expected Spanish CPI data and supply burden caps early rally in core global FI markets. GBP struggles.

- China equities soften on familiar areas of worry, 10-Year Chinese yields breach COVID lows.

- Mid-tier U.S. data & ECB speak due, greater focus on this week's tier 1 risk events.

MNI Eurozone Inflation Preview – January 2024

EXECUTIVE SUMMARY

The January flash eurozone inflation round is expected to show a pullback in Y/Y price gains versus December, with overall HICP printing 2.7% Y/Y (2.9% prior) and core 3.2% Y/Y (3.4%).

- This would represent a resumption in the overall downtrend: December’s Y/Y headline figure reflected an 0.5pp uptick but that was largely the result of base effects (German energy subsidies in December 2022), and while sequential core inflation ticked higher (+0.0% M/M vs -0.2% prior), Y/Y slipped to 3.4% Y/Y (vs 3.6% prior) and core momentum saw a deceleration (see our December HICP recap in the next section).

- January’s prints are set to be “noisy” with multiple hard-to-predict factors coming into play. The theme of energy-related distortions is expected to continue, with German, French, Italian, and Dutch energy support measures dropping out from year-earlier comparisons. Food and core goods prices are seen continuing to disinflate.

- While services prices are seen as disinflationary, there is uncertainty generated in part by annual weighting changes. Added to these uncertainties are tax changes to start the year, as well as the typical annual re-pricing of goods and services across multiple industries.

- In terms of the impact on ECB policy, below-expected incoming readings, along with progress on wage dynamics, will probably be required to bring a cut earlier than the summer.

- Click for full preview:Jan2024EZCPIPreview.pdf

MNI Riksbank Preview: February 2024 - QT Acceleration Eyed

EXECUTIVE SUMMARY:

- The Riksbank is widely expected to leave the policy rate on hold at 4.00% in its first meeting of 2024, with most focus on whether (or, more likely, by how much) the pace of government bond sales will be increased.

- The MNI Markets Team expects no change to the policy rate and an increase in the pace of bond sales to around SEK6.5bln/month.

- Of the analyst previews we have seen, there is a unanimous expectation for rates to be held steady. With respect to QT, all but one analyst that expressed a view expect an increase from the current pace of SEK5bln/month, with estimates ranging from SEK5bln (no change to the current pace) to SEK8bln. The median estimate is SEK7bln.

- A larger-than-expected QT acceleration would likely see the SEK strengthen, particularly given the Riksbank’s view that the policy has already been SEK-positive. However, this may be offset by any softening in the guidance surrounding upside policy rate risks. We will likely need to let the dust settle on the policy announcement and the press conference to see how markets have digested the decision in its entirety.

- Click for full preview: MNI Riksbank Preview - 2024-02.pdf

US TSYS: A Little Richer Still After Borrowing Estimates Rally

Cash Tsys have pulled back off best levels with the aid of stronger than expected Spanish CPI and Italian GDP growth, but still trade 0.5-2bp richer. It still sees yields consolidate/push a little lower from yesterday’s late rally on lower-than-expected Treasury marketable borrowing estimates, limiting upside issuance risks for Wednesday’s refunding announcement.

- TYH4 at 111-21 has pulled back from a high of 111-27+ amongst strong volumes of almost 400k. Yesterday’s price action saw clearance of the 20-day EMA with next resistance seen at 112-01+ (Jan 17 high) as short-term gains are still considered corrective from a technical perspective.

- JOLTS probably headlines today’s data whilst US earnings are in full swing with Pfizer and Starbucks still to come pre-market, before more notably Alphabet and Microsoft after the close. Any surprises will be met with an eye of tomorrow’s FOMC decision, refunding announcement and important data including the Employment Cost Index.

- Data: FHFA House Prices Nov (0900ET), S&P CoreLogic House Prices Nov (0900ET), Conf Board consumer survey Jan (1000ET), JOLTS labor data Dec (1000ET), Dallas Fed services Jan (1030ET)

- Bills issuance: US Tsy $80B 42D CMB bill auction (1130ET)

US TSY FUTURES: OI Points To Mix Of Long Setting & Short Cover

The combinations of Monday's rally and preliminary OI data points to the following positioning swings to start the week:

- Net long setting: FV, TY & US futures.

- Net short cover: TU, UXY & WN futures.

- Net short cover seemed to be the dominant positioning factor across the curve, although the net curve OI DV01 equivalent swing was limited, with the same holding true when examining the equivalent movement in contract-by-contract OI.

- A reminder that a couple of rounds of dovish ECB speak and issuance expectations in light of shallower-than-expected borrowing estimates from the Treasury helped drive Monday's firming.

| 29-Jan-24 | 26-Jan-24 | Daily OI Change | OI DV01 Equivalent Change ($) | |

| TU | 3,944,084 | 3,965,492 | -21,408 | -801,437 |

| FV | 5,940,228 | 5,938,153 | +2,075 | +88,789 |

| TY | 4,722,326 | 4,706,846 | +15,480 | +992,877 |

| UXY | 2,097,584 | 2,104,806 | -7,222 | -661,078 |

| US | 1,429,564 | 1,422,090 | +7,474 | +1,013,412 |

| WN | 1,652,280 | 1,659,236 | -6,956 | -1,479,378 |

| Total | -10,557 | -846,815 |

STIR: Fed Rate Path Treading Water With Multiple Risk Events Eyed

Fed Funds implied rates are little changed overnight as they continue to tread water with tomorrow's FOMC decision and a busy week for data ahead.

- Cumulative cuts: 12.5bp for Mar, 33bp for May, 58bp for Jun and 137bp for Dec.

- Today’s main interest for Fed pricing is likely in JOLTS and Conf Board consumer confidence. JOLTS quit rates have returned to pre-pandemic averages but openings to the number of unemployed are still elevated on historical basis despite an already sizeable decline.

STIR: OI Points To Mix Of SOFR Futures Long Setting & Short Cover On Monday

The combination of yesterday's move higher in SOFR futures and preliminary OI data points to the following positioning swings on Monday:

- Whites: Net short cover was seemingly seen in all contracts outside of what looked to be net long setting in SFRH4, with the former dominating in net pack terms.

- Reds: An apparent mix of net long setting (SFRH5 & U5) and net short cover (SFRZ4 & M5), with the former dominating in net pack terms.

- Greens: Net long cover was seemingly seen in all contracts outside of some apparent short cover in SFRH6, with the former dominating in net pack terms.

- Blues: A mix of net long setting (SFRH7 & M7) and net short cover (SFRZ6 & U7), with the former dominating in net pack terms.

- All net pack OI swings, and indeed the contract specific moves, were relatively contained.

| 29-Jan-24 | 26-Jan-24 | Daily OI Change | Daily OI Change In Packs | ||

| SFRZ3 | 1,200,563 | 1,201,813 | -1,250 | Whites | -8,790 |

| SFRH4 | 1,231,925 | 1,225,989 | +5,936 | Reds | +8,961 |

| SFRM4 | 1,138,468 | 1,145,556 | -7,088 | Greens | +4,605 |

| SFRU4 | 983,824 | 990,212 | -6,388 | Blues | +2,366 |

| SFRZ4 | 1,038,682 | 1,039,588 | -906 | ||

| SFRH5 | 541,886 | 535,880 | +6,006 | ||

| SFRM5 | 646,614 | 649,665 | -3,051 | ||

| SFRU5 | 574,101 | 567,189 | +6,912 | ||

| SFRZ5 | 624,882 | 621,759 | +3,123 | ||

| SFRH6 | 415,472 | 418,607 | -3,135 | ||

| SFRM6 | 418,710 | 416,532 | +2,178 | ||

| SFRU6 | 299,832 | 297,393 | +2,439 | ||

| SFRZ6 | 267,670 | 268,110 | -440 | ||

| SFRH7 | 133,297 | 131,735 | +1,562 | ||

| SFRM7 | 148,692 | 147,365 | +1,327 | ||

| SFRU7 | 148,777 | 148,860 | -83 |

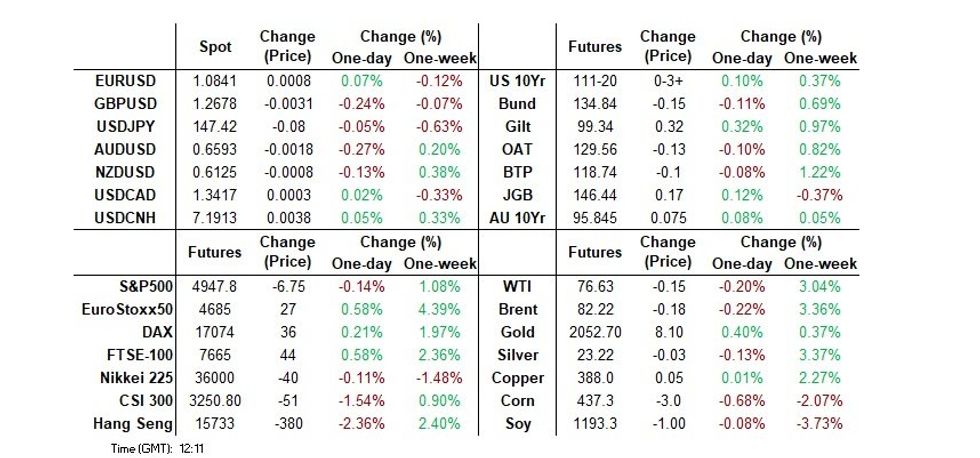

FOREX: GBP is the early worst performer in G10s

Most G10s pairs have stayed within tight ranges, overnight and during the European early session.

- EURUSD still trade in 30 pips range.

- The EUR was under small early pressures, but failed to break the 1.0800 handle, and the initial immediate support of 1.0793, printed a 1.0796 low Yesterday and a 1.0812 low today, with the bounce aided by better GDPs in Europe.

- The Yen was the early small best performer, as Yield saw further downside continuation, but Treasury futures are off their highs, capped by the European GDP data and ahead of heavy supply on this side of the Pond.

- The SEK is now leading in G10, up 0.27%, Economic tendency, Consumer and Mfg Confidence, came above last, but these aren't real market movers and overall USDSEK stays in that 10.5145/10.3675 range it has traded within for the past 10 sessions, now at 10.41.

- Worst early performer is the Pound, albeit off its low, still down 0.27%, but still short of the next support situated at 1.2642, printed a 1.2672 low so far today.

- Looking ahead, US JOLTS is the main data remaining for the session, while ECB Vasle and Nagel are still due to speak.

FX OPTIONS: Expiries for Jan30 NY cut 1000ET (Source DTCC)

- EURUSD: 1.0815 (289mln), 1.0820 (385mln), 1.0825 (659mln), 1.0830 (360mln), 1.0835 (250mln), 1.0865 (329mln), 1.0875 (511mln).

- USDJPY: 147.20 (551mln), 148.00 (642mln).

- AUDUSD: 0.6640 (276mln).

- USDCNY: 7.1500 (416mln).

EUROPEAN ISSUANCE UPDATE

2.50% Mar-26 Schatz Auction Results

- E5bln (E4.129bln allotted) of the 2.50% Mar-26 Schatz. Avg yield 2.49% (bid-to-cover 1.49x).

Aug-54 Bund Syndication: Launched

- E6bln (Inc E1bln retained) of the Aug-54 Bund (DE000BU2D004). Books closed in excess of E74bln (ex JLN interest, pre-rec). Spread set earlier at 1.80% Aug-53 Bund (DE0001102614) +4.5bp mid

5/10-year BTP and CCTeu Auction Results

- E3.5bln of the 4.10% Feb-29 BTP. Avg yield 3.14% (bid-to-cover 1.35x)

- E1.5bln of the 4.35% Nov-33 BTP. Avg yield 3.69% (bid-to-cover 1.68x)

- E2bln of the 3.35% Mar-35 BTP. Avg yield 3.85% (bid-to-cover 1.63x)

- E2bln of the 1.15% Oct-31 CCTeu. Avg yield 5.23% (bid-to-cover 1.5x)

Greece 10-year Syndication: Launched

- E4bln of the new Jun-34 10-year GGB (ISIN: GR0124040743)

- Books closed in excess of E35bln (inc E1.425bln JLM interest)

- Spread set previously at MS+80bps (guidance was MS+85bps area).

0.125% Mar-51 I/L Gilt Auction Results

- GBP900mln of the 0.125% Mar-51 linker. Avg yield 1.333% (bid-to-cover 3.1x).

- Another solid UK linker auction with the average price a similar premium over the pre-auction mid-price to the November auction and a similar bid-to-cover.

EGBS: Bunds Pare Gains Following Higher-Than-Expected Spanish CPI

Bunds are trading flat on the day, having fallen almost 50 ticks from early session highs following this morning's higher-than-expected Spanish inflation data. OAT and BTP futures are also now little changed.

- While it is hard to interpret any significant read-throughs from the Spanish print to the Eurozone-wide figure, it nonetheless sets the tone for potential upside risks to the region's inflation data over the next few days.

- The slightly firmer-than-expected run of Q4 flash GDP figures in Spain, Italy and the Eurozone will have also factored in.

- The move off highs comes after lower-than-expected borrowing estimates from the US Treasury and China-centric worry seemed to promote a bid through Asia-Pac hours.

- Supply from Germany, Italy and Greece will have also weighed in the run-up to the respective bidding deadlines.

- German and French cash yields are unchanged/a touch higher, while 10-year periphery spreads to Bunds are generally little changed.

- Later today, ECB-speak includes the hawkish leaning Vasle (1230GMT) and Nagel (1530GMT). This morning, the usually hawkish Kazaks re-asserted the importance of labour market data as a prerequisite for rate cuts.

GILTS: Off Best Levels, Curve Twist Flattens

Matters from the continent tempered the early gilt bid, with the burden of EGB issuance and firmer-than-expected Spanish CPI data noted.

- Futures have recovered from session lows to trade +35 at 99.37 around the middle of their early 31-tick range.

- Cash gilt yields are 1.5bp higher to 1.5bp lower, with the curve twist flattening.

- The early rally was centred on expectations surrounding U.S. Tsy issuance matters and China-related worry during Asia-Pac hours.

- Domestic credit data printed on the softer side of expectations.

- Long end I/L supply saw solid demand metrics, as covered elsewhere.

- SONIA futures are flat to 4.0bp firmer, with a light flattening bias.

- STIRs are off dovish session extremes alongside the pullback from best levels in gilts.

- BoE-dated OIS prints 1bp softer to 1bp firmer on the day through ’24 contracts. ~109bp of cuts are seen through ’24 on the whole.

| BoE Meeting | SONIA BoE-Dated OIS (%) | Difference Vs. Current Effective SONIA Rate (bp) |

| Feb-24 | 5.201 | +1.3 |

| Mar-24 | 5.165 | -2.3 |

| May-24 | 5.049 | -13.9 |

| Jun-24 | 4.883 | -30.5 |

| Aug-24 | 4.667 | -52.1 |

| Sep-24 | 4.477 | -71.0 |

| Nov-24 | 4.255 | -93.3 |

| Dec-24 | 4.098 | -108.9 |

GILTS: Highlights of Annual GEMM / investor consultation meetings

- Both GEMMs and investors supported proportional reductions in long conventional issuance with increases in shorts/mediums.

- Both GEMMs and investors also supported less linker issuance - with GEMMs preferring a focus towards 10/20-year maturities rather than longer-dated issued.

- Both GEMMs and investors supported building out the green gilt curve with 5 and/or 20-year maturities. GEMMs supported around GBP10bln of green issuance.

- "A number of GEMMs" suggested T-bills should "make a positive contribution to financing in 2024-25." While "investors who offered an opinion generally supported" this too.

EQUITIES: S&P E-Minis Bull Cycle Extends

The uptrend in S&P E-Minis remains intact and Monday’s rally reinforces current conditions. Resistance at 4841.50, the Dec 28 high, has recently been cleared, confirming an extension of the uptrend. Sights are on 4982.62 next,1.50 projection of Nov 10 - Dec 1 - 7 price swing. Initial support is at 4844.18 20- day EMA.

- EUROSTOXX 50 futures traded sharply higher last week and the contract started this week’s session on a bullish note, with price holding on to its recent gains. Key resistance at 4634.00, the Dec 14 high, has been cleared. The break confirms a resumption of the medium-term uptrend and sights are on the 4700.00 handle next. Initial firm support lies at 4522.80, the 20-day EMA.

COMMODITIES: Short-Term Bullish Theme In Oil Remains Intact

- Gold remains in consolidation mode and continues to trade above the Jan 17 low of $2001.9. The recent print below the 50-day EMA and the break of support at $2013.4, the Jan 11 low, has strengthened a bearish threat and a resumption of weakness would open a key level at $1973.2, the Dec 13 low. For bulls, clearance of 2062.3, the Jan 12 high, is required to signal a reversal.

- In the oil space, WTI futures traded higher last week. The contract has breached resistance at $76.31, the Dec 26 high. The clear break of this hurdle undermines the recent bearish theme and highlights a stronger short-term bullish condition. A continuation higher would open $79.56, the Nov 30 high. On the downside, initial key support lies at $74.55, the 50-day EMA. Monday’s move lower appears - for now - to be a correction.

CHINA STOCKS: Familiar Sources Of Worry & Want For Further Support Weighs

MNI (London) - Benchmark indices struggled on Tuesday, as deeper property market worry in the wake of the Evergrande liquidation order in HK and a combination of continued economic fear/want for policy and equity market-specific support, provided headwinds.

- The CSI 300 was 1.8% worse off, while the Hang Seng lost 2.3%. both remain a little above YtD lows owing to last week’s rally.

- Details of Hong Kong’s plan re: new security laws also seemed to weigh.

- Media outlets tried to play down worry surrounding the Evergrande situation, pointing to limited impact for Evergrande’s unfinished housing projects and the rights of onshore bond holders.

- However, worry about the precedent set by the move and the situation for offshore bondholders, in addition to potential shockwaves through the sector, seemed to dominate.

- Chinese builder Radiance announced its intentions to hold meetings with March 2024 bondholders, with that line trading at ~$0.65 on the dollar.

- Note that Vice Premier He stressed the need for cities to follow through on national guidance re: property developer funding on Monday.

- There were also reports pointing to the potential for banks to extend loan periods for some property projects.

- BYD struggled after softer-than-expected earnings data.

- Sands China moved lower after a negative brokerage move.

- Electricity providers seemed to benefit from expectations surrounding demand related to cold weather.

- Lower Chinese yields (benchmark 10s breached their ’20 COVID low) did little to support equities.

- International flows were supportive at the margin, with modest net inflows for the mainland (CNY1.7bn) lodged via the HK-China Stock Connect links.

CHINA RATES: 10-Year CGB Yield Hits Fresh Low On Easing & Liquidity Expectations

MNI (London) - 10-Year Chinese government bond yields have moved through their COVID low, showing as low as 2.463% in recent trade, shedding ~3bp on the day. The benchmark has registered the lowest level on BBG records, which date back to 2005.

- The broader CGB curve has bull steepened, with desks flagging sizeable demand for front end and belly CGBs on the part of large onshore banks.

- When it comes to the drivers of the latest move lower in Chinese yields, heightened worry re: the property sector in the wake of the liquidation order for China Evergrande has been earmarked as a major factor, with expectations surrounding LNY liquidity provisions, the well-documented economic worry re: China and expectations for deeper policy easing in the wake of the latest RRR cut from the PBoC all factoring in.

- Monday’s move lower in core global FI yields would have helped as well.

| Date | GMT/Local | Impact | Flag | Country | Event |

| 30/01/2024 | 1355/0855 | ** |  | US | Redbook Retail Sales Index |

| 30/01/2024 | 1400/0900 | ** | | US | S&P Case-Shiller Home Price Index |

| 30/01/2024 | 1400/0900 | ** | | US | FHFA Home Price Index |

| 30/01/2024 | 1400/0900 | ** | | US | FHFA Home Price Index |

| 30/01/2024 | 1500/1000 | *** | | US | Conference Board Consumer Confidence |

| 30/01/2024 | 1500/1000 | ** | | US | housing vacancies |

| 30/01/2024 | 1500/1000 | *** | | US | JOLTS jobs opening level |

| 30/01/2024 | 1500/1000 | *** | | US | JOLTS quits Rate |

| 30/01/2024 | 1530/1030 | ** | | US | Dallas Fed Services Survey |

| 30/01/2024 | 1630/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 31/01/2024 | 2350/0850 | * |  | JP | Retail sales (p) |

| 31/01/2024 | 2350/0850 | ** | | JP | Industrial production |

| 31/01/2024 | 0030/1130 | *** |  | AU | CPI inflation |

| 31/01/2024 | 0030/1130 | *** | | AU | CPI Inflation Monthly |

| 31/01/2024 | 0130/0930 | *** |  | CN | CFLP Manufacturing PMI |

| 31/01/2024 | 0130/0930 | ** | | CN | CFLP Non-Manufacturing PMI |

| 31/01/2024 | 0700/0800 | ** |  | DE | Import/Export Prices |

| 31/01/2024 | 0700/0800 | ** | | DE | Retail Sales |

| 31/01/2024 | 0700/1500 | ** | | CN | MNI China Liquidity Index (CLI) |

| 31/01/2024 | 0730/0830 | ** |  | CH | Retail Sales |

| 31/01/2024 | 0745/0845 | *** |  | FR | HICP (p) |

| 31/01/2024 | 0745/0845 | ** | | FR | PPI |

| 31/01/2024 | 0855/0955 | ** | | DE | Unemployment |

| 31/01/2024 | 0900/1000 | *** | | DE | North Rhine Westphalia CPI |

| 31/01/2024 | 0900/1000 | *** | | DE | Bavaria CPI |

| 31/01/2024 | 1200/0700 | ** | | US | MBA Weekly Applications Index |

| 31/01/2024 | 1300/1400 | *** | | DE | HICP (p) |

| 31/01/2024 | 1315/0815 | *** | | US | ADP Employment Report |

| 31/01/2024 | 1330/0830 | *** |  | CA | Gross Domestic Product by Industry |

| 31/01/2024 | 1330/0830 | ** | | US | Employment Cost Index |

| 31/01/2024 | 1330/0830 | ** | | US | Treasury Quarterly Refunding |

| 31/01/2024 | 1445/0945 | *** | | US | MNI Chicago PMI |

| 31/01/2024 | 1530/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 31/01/2024 | 1900/1400 | *** | | US | FOMC Statement |

| 01/02/2024 | 2200/0900 | ** | | AU | IHS Markit Manufacturing PMI (f) |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.