Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS:

- Risk assets bounce, but recoveries remain shallow

- Energy names rally sharply as crude retraces Friday rout

- Focus remains on government/CB response to new Omicron variant

US TSYS SUMMARY: Yield Retrace, But Still Way Below Pre-Holiday Levels

Treasuries are retracing after Friday's massive rally, amid speculation over the medium-term implications of the newly-discovered Omicron COVID variant.

- The 2-Yr yield is up 4.1bps at 0.5393%, 5-Yr is up 6.3bps at 1.2225%, 10-Yr is up 6.2bps at 1.5346%, and 30-Yr is up 5.6bps at 1.877%. Of course this is after one of the biggest rallies in recent years on Friday, and yields still much lower vs pre-Thanksgiving.

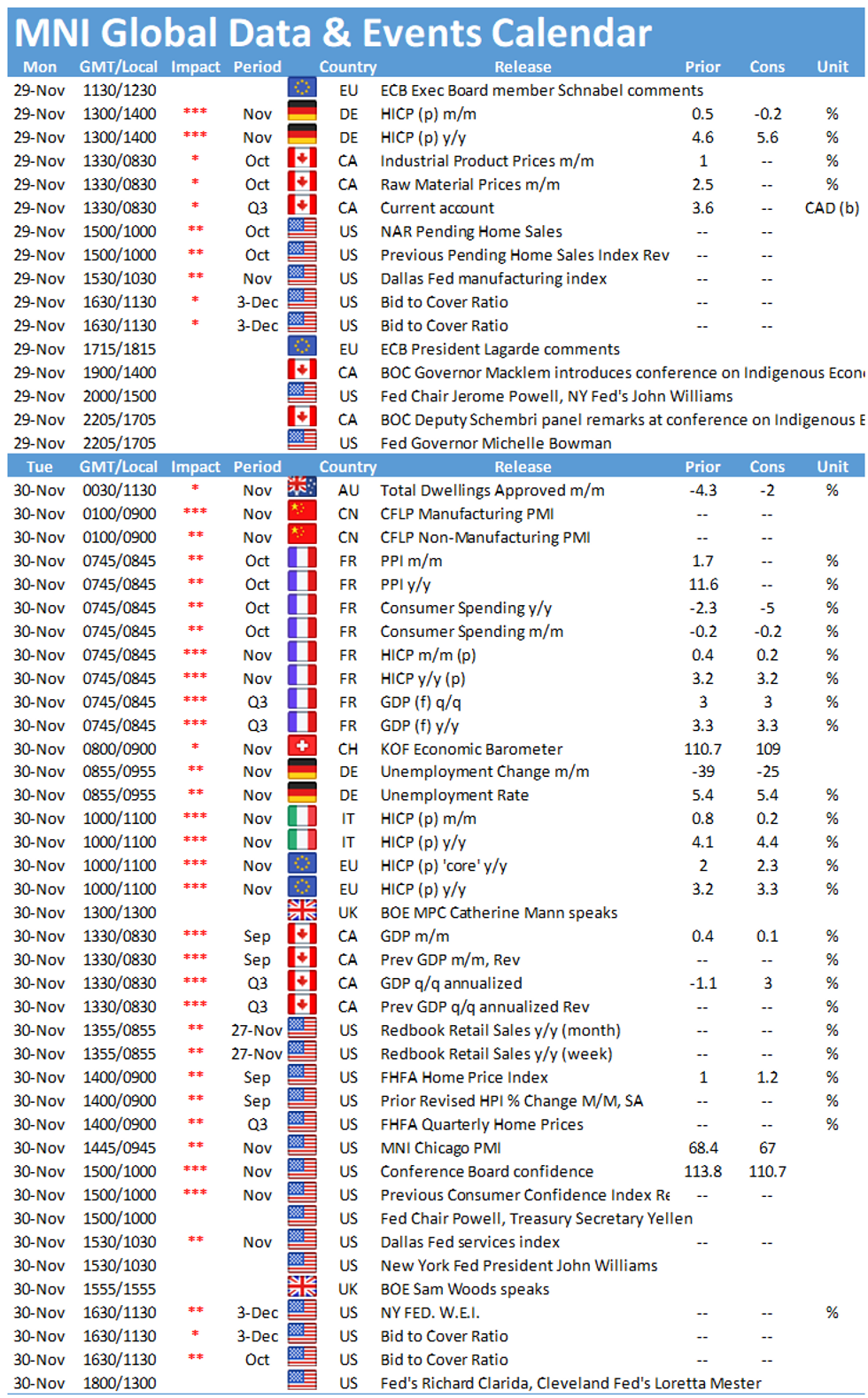

- Fed speakers include NY's Williams and Chair Powell making remarks at a NY Fed innovation event at 1500/1505ET, respectively; NY Fed VP Hassan moderates a panel at that event at 1515ET. Then Gov Bowman takes part in a discussion on central banks and indigenous communities at 1705ET. Relatively more focus on Powell's Congress hearing Tues / Weds.

- D.C. resumes business today: Pres Biden speaks on Omicron at 1145ET, and on the supply chain at 1545ET. Senate back in session, House tomorrow - immediate focus on gov't funding, with shutdown set for end-of-day Dec 3 (and an eye on Dems social spending bill).

- Pending home sales kicks off the week's data at 1000ET, with Dallas Fed Manuf at 1030ET.

- Supply is all bills ($108B combined 13-/26-wk at 1130ET). NY Fed buys ~$7.375B of 2.25-4.5Y Tsys.

EGB/GILT SUMMARY: Markets Reverse Course Following Friday Risk-Off

Following the abrupt risk-off mood at the back end of last week, markets have paired back this morning with equities pushing higher and European sovereign FI selling off.

- The ECB's Villeroy and de Cos reiterated again the official line that the inflation spike is largely transitory, while Isabel Schnabel also stressed that it would be premature to consider policy tighten.

- Gilts have underperformed EGBs with cash yields 2-4bp higher and the curve bear flattening.

- Bund yields are 1-3bp higher on the day.

- The sell-off in OATs has been relatively contained with cash yields up 1-2bp.

- It is a similar story for BTPs where yields have edged up 1bp across the curve.

- German regional CPI data for November accelerated sharply from the previous month with the national estimate due out at 1300GMT.

- Supply this morning came from Germany (Bubills, EUR5.132bn allotted).

EUROPE OPTION FLOW SUMMARY

Eurozone:

RXF2 171.50/170.5ps, bought for 14, 14.5, 15 in 30k. Rolling up strikes

2RH2 99.75/99.50ps, bought for 2.25 in 8k

UK:

3LZ1 99.00/98.87ps, sold at 10.25 in 8.8k

US:

1MZ1 128.5p, sold at 2 in 22k

FOREX: Currencies Revert as Markets Reassess Omicron Risk

- Growth proxies and commodity-tied FX are trading higher ahead of the NY open, with markets reassessing the overarching risks of the new Omicron variant that had sent markets spiraling on Friday. Equities have similarly bounced, with US futures indicating a higher open of 0.7% or so. While risks surrounding the new Omicron variant remain, markets are reassessing the impact on global economies, with renewed lockdowns across the likes of the UK and US looking unlikely.

- Expected vaccine protection also received a boost, with Moderna announcing they expect a new variant-targeting jab to be ready for use by early next year.

- The moves have favoured CAD and AUD, while haven FX has weakened. This puts AUD/JPY back above 81.00, but still well short of the Friday highs at 83.02.

- EUR/USD trades softer, working against much of Friday's rally as markets re-price the US curve, reversing some of last week's volatility that had priced out near-term Fed rate rises through 2022.

- Focus turns to central bank speak, with a number of Fed representatives on the docket including Powell, Williams and Bowman. Although the speech topics aren't directly policy-related, markets remain on watch for clues on policy trajectory in the face of the variant.

FX OPTIONS: Hedging Markets Yet to Price Meaningful Turnaround in Sentiment

- Currency markets remain in rebound mode, with AUD, CAD among the session's best performers while EUR, CHF and JPY lag. Not the same case in vol markets, however, with front-end implied remaining well elevated and risk reversals still indicating a solid downside bias.

- 1m AUDUSD vols trade either side of 10 points, the highest level since March and have nudged implied market pricing for AUD/USD to trade below 0.70 at year-end up to 20.3% from the 14.8% probability priced by markets this time last week.

- Similarly, demand for USD/JPY downside hedges points toward still uneasy market sentiment. Around $4 in USD/JPY puts have traded for every $3 in calls for DTCC-tracked options, with Y105, Y107 and Y110 put strikes garnering particular focus. The larger trades are consistent with put spreads, eyeing a three month expiry and thereby capturing the next two policy decisions from both the Fed and the BoJ.

FX OPTIONS: Expiries for Nov29 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1150-60(E529mln), $1.1250(E583mln), $1.1265-75(E582mln), $1.1300(E1.4bln)

- USD/JPY: Y113.20-25($561mln), Y115.20-25($1.1bln)

- AUD/USD: $0.7100(A$563mln)

- USD/CAD: C$1.2600($1.2bln)

Price Signal Summary - S&P E-Minis Bounce Considered Corrective

- In the equity space, S&P E-minis sold off sharply Friday and despite today's gains, remain vulnerable. Attention is on the 50-day EMA at 4563.83. This average has in the past proved to be a reliable support and represents a key pivot level. Any signs of base building around the EMA would represent a potential bullish development in line with the underlying uptrend. A clear break would instead strengthen a bearish case. EUROSTOXX 50 futures also sold off sharply Friday and despite currently trading above last week's low, still appears vulnerable. A resumption of weakness would open 4004.00, Oct 12 low.

- In FX, trend conditions are unchanged in the USD and the uptrend remains firmly intact. EURUSD objectives remain; 1.1185 Jul 1, 2020 low and 1.1128, 1.764 projection of the Jan 6 - Mar 31 - May 25 price swing. Short-term gains are still considered corrective with resistance at 1.1374, Nov 18 high. GBPUSD bears have paused for breath. Trend signals continue to point south and the next objective is 1.3216, 1.236 projection of the Sep 14 - 29 - Oct 20 price swing. USDJPY traded sharply lower Friday and remains vulnerable. The next key support to monitor is 112.73, the Nov 9 low. A break would strengthen the bearish case. Initial resistance is at 114.19, the 20-day EMA. EURJPY has traded below key support at 127.93, Sep 22 low. This reinforces bearish conditions with the focus on 127.28 next, 1.00 projection of the Jun 1 - Sep 22 - Oct 20 price swing.

- On the commodity front, Gold is consolidating but the outlook remains bearish within the bull channel drawn from the Aug 9 low. The short-term focus is on the channel base at $1757.9 today. WTI futures reversed course Friday and sold off sharply. The break of a number of support levels suggest scope for a continuation lower short-term. The focus is on $66.21, 76.4% retracement of the Aug 23 - Oct 25 rally.

- In the FI space, Bund futures have recovered from recent lows and importantly, support at 170.06, the Nov 5 low remained intact last week. This suggests the recent move lower has been a correction and that a short-term uptrend remains intact. The focus is on resistance at 172.57, Nov 22 high and the bull trigger. Gilts rallied Friday and the contract gapped higher at the open. Futures also traded above resistance at 126.23, high Nov 9 and attention is on the 127.00 handle next.

EQUITIES: Markets Bounce, With Decent Gap Higher Expected On Opening Bell

- US futures trade uniformly in positive territory, with the NASDAQ future trading higher by just over 1% a few hours out from the opening bell. The e-mini S&P has bounced off Friday's 4577.25 to add over 50 points, but the recovery has fallen just shy of a 50% retracement of Friday's slide, with 4642.75 marking a decent enough intraday resistance level.

- Similar gains are seen across Europe, with markets adding 0.8-1.2%, with the EuroStoxx50 leading the charge. Energy names are seeing most support, with the rebound in prices flattering margins and stock prices for the likes of Royal Dutch Shell, BP and Repsol.

COMMODITIES: Crude Bounces, But Well Shy of Friday Highs

- WTI and Brent crude futures trade solidly in positive territory, with prices bottoming out off the Friday lows and recouping as much as 5%. Despite the rally, prices remain well shy of recent levels, with WTI still close to $8 off last week's $79.23.

- The OPEC+ technical meeting scheduled for this week has been bumped back a few days to accommodate for the subsequent market volatility following the disclosure of the Omicron variant. Given the pullback in prices, OPEC+ could pause the planned rollout of a further easing of 400,000bpd in output curbs, which will remain a market focus in the coming sessions.

- Despite the minor bounce in prices, WTI futures remain vulnerable. Friday's breach of support at $74.76, low Nov 22 and the subsequent sharp sell-off has confirmed a resumption of the downtrend and marks an extension of the current bearish sequence of lower lows and lower highs.

- Gold is still consolidating and remains vulnerable. The yellow metal sold off sharply early last week extending the move lower from $1877.2, the Nov 16 high. Price has also traded below the 20- and the 50-day EMAs.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok