Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

Highlights:

- US curve sits flatter ahead of CPI, 10y supply to follow

- NOK firmer as hot core CPI raises rate expectations

- No progress in debt ceiling talks, but another meeting of key figures Friday

US TSYS: Twist Flattening Pre US CPI, 10Y Supply Follows Later

- Cash Tsys trade with a twist flattening pivoting around 5s ahead of the day’s key risk event, US CPI (preview here, noting that BBG consensus has since lifted to 0.4 for core after further survey entries). 2Y and 3Y tenors underperform, possibly some reversal after yesterday’s paring of losses on the surprisingly strong 3Y auction. There appears to have been little progress made at yesterday’s congressional leaders meeting on the debt ceiling, with another meeting pencilled in for Friday.

- 2YY +2.1bp at 4.043%, 5YY -0.3bp at 3.491%, 10YY -1.7bp at 3.501% and 30YY -2.4bp at 3.815%. 2YY have struggled to clear 4.07% in the past two days with the market recently trimming rate cut expectations but still eyeing more than two fully priced 25bp cuts to year-end.

- TYM3 trades 2 ticks higher at 115-08 in a relatively narrow 0-14 range for the day with subdued cumulative volumes of 200k, unsurprisingly ahead of US CPI. It remains close to yesterday’s low of 115-01+ after which sits the 50-day EMA of 114-26+, whilst to the upside lies resistance at 115-27+ (May 8 high).

- Data: Weekly MBA mortgage apps (0700ET), CPI (0830ET), Real Av Earnings (0830ET), Mthly Budget Statement (1400ET).

- Note/bond issuance: US Tsy $35B 10Y Notes (1300ET)

- Bill issuance: US Tsy $36B 17W Bills (1130ET)

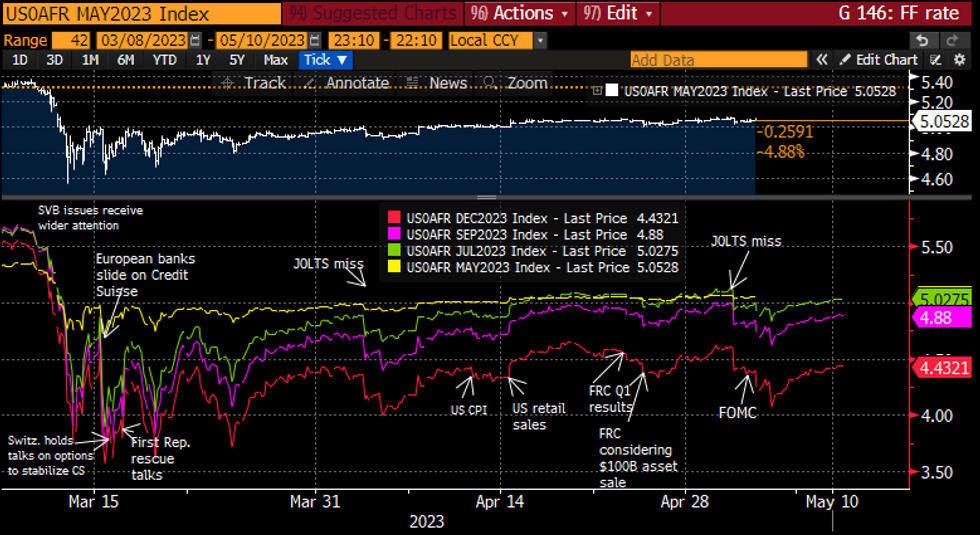

STIR FUTURES: Fed Implied Rates On Balance Higher Pre US CPI

- Fed Funds implied rates are off overnight highs but on balance have nudged higher ahead of US CPI.

- 3.5bp hike for Jun (+0.5bp), 19bp of cuts to 4.89% in Sep (+1bp) before a cumulative 42bp of cuts to 4.66% Nov (+1.5bp) and 64bp of cuts to 4.44% Dec (+2.5bp). The latter compares with 85bp of cuts to year-end priced just before Friday’s payrolls, whilst the 4.44% is at the level seen after last week’s JOLTS miss.

- No Fedspeak scheduled for today with Gov. Waller next up tomorrow on financial stability & climate change.

FOMC-dated Fed Funds implied ratesSource: Bloomberg

FOMC-dated Fed Funds implied ratesSource: Bloomberg

No Progress In Debt Ceiling Talks, But Another Meeting Of Key Figures Friday

As was broadly expected, there appears to have been little progress made on 9 May at the meeting between President Biden, Speaker Kevin McCarthy (R-CA) and other senior Congressional figures regarding the looming debt ceiling.

- Punchbowl News reports that "The Hill staffers and Biden administration officials huddling over the next two days aren’t even on the same page when it comes to what they’re discussing. Democrats believe they are negotiating a spending agreement outside the context of the debt limit. Republicans believe they’re negotiating a debt-limit deal with a spending-cut component."

- Politico notes, though, that " beneath the enduring stalemate was an only-in-Washington bright spot: Nobody walked out of the meeting, or away from the negotiations altogether."

- Following the meeting of aides over 10 and 11 May, Biden, McCarthy, Senate majority leader Chuck Schumer (D-NY), Senate minority leader Mitch McConnell (R-KY) and House minority leader Hakeem Jeffries (D-NY) will meet again on Friday 12 May.

- Following the meeting, Biden floated the prospect of using the 14th Amendment to ensure a default is avoided. Some legal scholars have stated they believe that the 14th amendment makes it unconstitutional for the US not to pay its debt. However, pursuing would likely end up in a legal quagmire running well past the 'X date' this summer.

Core Non-Housing Services Again In Focus

- Ahead of tomorrow's CPI print, we recall that core non-housing services inflation measures saw differing degrees of moderation in March, but in both cases were propped up by volatile items.

- Core services ex OER and tenants’ rents only eased from 0.50% to a still strong 0.40% M/M whilst core services excluding all rent of shelter slowed from 0.45% to 0.25% M/M on account of strong lodging away from home.

- Whilst this category will likely receive plenty of attention this time around, differing weightings vs PCE can again make initial readings more difficult: for instance, Morgan Stanley see core services ex-housing slowing from 0.40% to 0.16% M/M but for the core PCE equivalent to hold at 0.24% M/M.

- Full report found here.

FOREX: NOK on Top as CPI Tips Balance to Further Hikes

- EUR/NOK just off the day's low of 11.5486, finding support at the Monday/Tuesday low. NOK is among the strongest in G10 today following stubbornly high CPI-ATE (6.3% vs. Exp. 6.1%) - which should keep a tightening bias at the Norges Bank. 11.4471 marks the 50-dma for EUR/NOK, with support seen into the mid-April low of 11.3582.

- AUD and SEK sit toward the bottom-end of the G10 table, but ranges are more muted ahead of the inflation release later today. The equity backdrop has not been risk-supportive, with the e-mini S&P trading on the backfoot through the European open.

- The USD Index is modestly higher for a third consecutive session, but remains in a holding pattern below the early May highs of 102.404.

- US CPI takes focus going forward, with markets expecting core CPI to keep pace M/M at 0.4%, while Y/Y slows to 5.5%. The data will be watched carefully for any confirmation that the Fed will pause on rate hikes going forward, with markets still assigning a solid chance of sizeable Fed rate cuts before year-end.

FX OPTIONS: Expiries for May10 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1050(E652mln), $1.1070(E1.1bln), $1.1100(E672mln)

- USD/JPY: Y135.40-50($952mln), Y136.00($822mln)

- USD/CAD: C$1.3450($651mln), C$1.3600($786mln)

- AUD/USD: $0.6900(A$2.8bln)

EQUITIES: E-Mini S&Ps Dip Ahead of US CPI, Remain Above 50-Day EMA

- Eurostoxx 50 futures are holding on to the bulk of its most recent gains and price remains above support at 4231.60, the 50-day EMA. The recent move down is considered corrective and the broader uptrend remains intact. A continuation higher would signal scope for a test of 4363.00, the Apr 21 high and bull trigger. Clearance of this level would confirm a resumption of the uptrend. A clear break of the 50-day EMA is required to signal a top.

- S&P E-minis remain above the 50-day EMA, which intersects at 4103.05. A continuation higher would refocus attention on key resistance and the bull trigger at 4206.25, the May 1 high. A breach of this level would confirm a resumption of the bull trend that started Mar 13. Key support has been defined at 4062.25, the May 4 low. A move through this support would be bearish.

COMMODITIES: Gold Remains in Uptrend Following Friday Move Lower

- WTI futures remain bearish despite the strong recovery from $63.64, the May 4. The trend condition was oversold last week and the recovery is allowing this to unwind. Initial resistance is at $73.93, the Apr 28 low ahead of $76.92, the Apr 28 high. On the downside, the recent print below $64.58, the Mar 20 low and a key support, reinforces a bearish theme. A clear break of it would confirm a resumption of the broader downtrend.

- Gold remains in an uptrend despite last Friday’s move lower. The yellow metal has breached resistance at $2048.7, the Apr 13 high to confirm a resumption of the broader bull cycle. This maintains the bullish price sequence of higher highs and higher lows and moving average studies are in a bull-mode set-up. The focus is on $2070.4, the Mar 8 high ahead of the all-time high at $2075.5. Key support is 1969.3, the Apr 19 low.

| Date | GMT/Local | Impact | Flag | Country | Event |

| 10/05/2023 | - | *** |  | CN | Money Supply |

| 10/05/2023 | - | *** | | CN | New Loans |

| 10/05/2023 | - | *** | | CN | Social Financing |

| 10/05/2023 | 1230/0830 | * |  | CA | Building Permits |

| 10/05/2023 | 1230/0830 | *** |  | US | CPI |

| 10/05/2023 | 1430/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 10/05/2023 | 1700/1300 | ** | | US | US Note 10 Year Treasury Auction Result |

| 10/05/2023 | 1800/1400 | ** | | US | Treasury Budget |

| 11/05/2023 | 0130/0930 | *** | | CN | CPI |

| 11/05/2023 | 0130/0930 | *** | | CN | Producer Price Index |

| 11/05/2023 | 1100/1200 | *** |  | UK | Bank Of England Interest Rate |

| 11/05/2023 | 1100/1200 | *** | | UK | Bank Of England Interest Rate |

| 11/05/2023 | 1200/1400 |  | EU | ECB Schnabel Talk at Federal Ministry of Finance | |

| 11/05/2023 | - | | EU | ECB Lagarde & Panetta in G7 Finance Meeting | |

| 11/05/2023 | 1230/0830 | ** | | US | Jobless Claims |

| 11/05/2023 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 11/05/2023 | 1230/0830 | *** | | US | PPI |

| 11/05/2023 | 1415/1015 | | US | Fed Governor Christopher Waller | |

| 11/05/2023 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 11/05/2023 | 1700/1300 | *** | | US | US Treasury Auction Result for 30 Year Bond |

| 11/05/2023 | 1730/1930 | | EU | ECB de Guindos Panels Diario Madrid Foundation Event |

MNI London Bureau | +44 203-865-3809 | edward.hardy@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok