Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

Highlights:

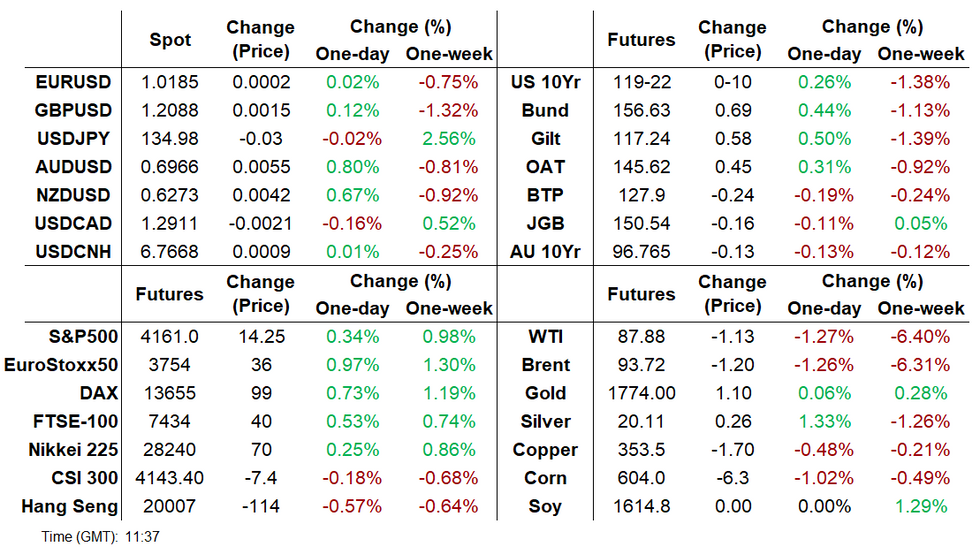

- Friday's post-nonfarm payrolls moves have partially unwound Monday, with the dollar and bond yields edging lower

- With a light data/speaker docket Monday, attention is already turning to Wednesday's US CPI report

- Italian political risk (and Moody's lowering their outlook) sees BTPs underperform

US TSYS: Treasuries Flatten Further Into Extremely Light US Docket

- Cash Tsys have bull flattened overnight as levels see a partial retracement of Friday's substantial post-payrolls sell-off, helped in part by a dampening in risk with China announcing its intentions to conduct "regular" drills near Taiwan before a limited European morning aside from a small beat in Sentix Investor confidence.

- Continued hawkish Fedspeak over the weekend (see separate bullet) keeps front-loaded hike expectations at the forefront of market attention and with it 2s10s only just off fresh post-2000 flats seen on the immediate reaction to a storming payrolls report at -41bps vs -44bps, with TD not ruling out -80bps in their payrolls review as the long-end pencils in a greater likelihood of a downturn.

- 2YY -1.2bps at 3.214%, 5YY -2.2bps at 2.932%, 10YY -2.9bps at 2.799% and 30YY -3.0bps at 3.037%.

- TYU2 trades 9 ticks higher at 119-21 as it moves off Friday's low of 119-07+ and with support at the 50-day EMA just below at 119-05+. Resistance is seen at 120-29 (Aug 4 high). Volumes are low but typically so for this time of year.

- No data or scheduled Fedpseak on an empty docket aside from bill issuance with US Tsy $54B 13W, $42B 26W bill auctions at 1130ET.

STIR FUTURES: Fed Hike Path Keeps To Payrolls Surge Higher

- Fed Funds implied hikes keep to post-payrolls increases, having opened higher still with a potential boost from weekend Fedspeak before retreating through Asia hours ahead of a very light US docket with an eye instead on US CPI on Wed.

- It leaves 69bps priced for Sept before a cumulative 122bp to Dec and 130bps to a peak of 3.64% in Mar’23, with just shy of 60bps of cuts thereafter to Dec’23.

- Governor Bowman sees the case for continuing 75bp hikes until inflation slows in a meaningful way and needs "unambiguous evidence" before marking down her price forecasts, whilst currently seeing few if any indications that inflation has peaked.

- Daly (’24 voter) meanwhile seemed more open to a larger than 50bp hike with 50bp absolutely in play, need to keep open mind vs 50bp reasonable thing to do in Sept prior to payrolls).

Cumulative hikes implied by FOMC-dated Fed Funds futures at specific meetingsSource: Bloomberg

Cumulative hikes implied by FOMC-dated Fed Funds futures at specific meetingsSource: Bloomberg

EGB/Gilt: Italian Politics In The Spotlight

European government bonds have started the week on a strong footing with BTPs being the notable exception amid a fresh bout of political instability. Equities have similarly edged higher, while G10 currencies are gaining ground against the dollar.

- Having agreed to form an alliance with the Democratic Party and the +Europe party just last week, the centrist Azione has now pulled out with party head Carlo Calenda starting that "the pieces just didn't fit together". The alliance was formed in an attempt to prevent a more right-wing government coming to power following the September 25 vote.

- BTPs have traded lower with yields up 1-4bp, the curve bear flattening and spreads over bunds widening.

- Bunds opened higher and have held on to the majority of the morning's gains. Cash yields are down 2-5bp with the belly of the curve outperforming.

- OAT yields are now 1-4bp lower on the day.

- Gilts have outperformed EGBs this morning with yields down 4-8bp. Second quarter GDP data will be published on Friday and follow's last week's particulary downbeat economic assessment from the Bank of England.

- France will offer EUR4.6-5.8bn of BTFs later today.

- The European data slate was light this morning with no tier one releases to note.

RATES / BOND OPTIONS

Europe:

- RXU2 161c, sold at 36 in ~1.6k

FX OPTION EXPIRY

Of note:

AUDUSD ~1bn at 0.70- EURUSD; 1.0100 (542mln), 1.0175 (234mln), 1.0200 (225mln).

- USDJPY: 134.85 (230mln), 135.00 (300mln).

- GBPUSD: 1.1990 (517mln).

- USDCAD: 1.2950 (872mln).

- AUDUSD: 0.6910 (777mln), 0.7000 (972mln).

- USDCNY: 6.75 (545mln).

Price Signal Summary - S&P E-Minis Trend Needle Still Points North

- In the equity space, S&P E-Minis are consolidating, the outlook however remains bullish. Fresh highs last week reinforces the current trend direction and this signals scope for a climb towards 4204.75 next, May 31 high and the next key resistance. Initial key support is 3998.05, the 50-day EMA. EUROSTOXX 50 futures trend conditions remain bullish and last week’s high print reinforces this theme. The contract has cleared the 76.4% retracement of the Jun 6 - Jul 5 downleg, at 3722.40. This opens 3840.00, the Jun 6 high. Initial firm support to watch is 3597.20, the 50-day EMA.

- In FX, the EURUSD short-term conditions are bullish as long as price holds above support at 1.0097, the Jul 27 low. A resumption of gains would signal scope for a continuation higher inside the bull channel drawn from the Feb 10 high - the top intersects at 1.0370. Weakness below 1.0097 would alter the picture. A bullish short-term theme in GBPUSD remains intact and last week’s pullback is considered corrective. Price has recently traded above the 50-day EMA and the next objective at 1.2332, the Jun 27 high. Potential is also seen for a climb towards 1.2406, the Jun 16 high and a key resistance. Initial support to watch lies is at 1.2004, Friday’s low. USDJPY is trading closer to its most recent highs. It is still possible that recent gains are a correction. The price levels to watch are; 136.91, the former bull channel support breached on Jul 28 and a key resistance and 130.41, last Tuesday’s low and a bear trigger.

- On the commodity front, Gold maintains a firmer tone despite Friday’s pullback. The yellow metal has recently breached the 50-day EMA and attention is on trendline resistance at $1799.6. The trendline is drawn from the Mar 8 high. A breach of the line would represent an important technical break and highlight a stronger reversal of the 5-month downtrend. Initial firm support lies at $1754.4 the Aug 3 low. In the Oil space, WTI futures remain vulnerable following last week’s move lower. Price has breached support at $88.23, Jul 14 low and a key support. This opens$85.37, the Mar 15 low.

- In the FI space, a short-term bull cycle in Bund futures remains intact and the recent pullback is considered corrective. Scope is seen for a climb to 159.79 next, the Apr 4 high (cont). Initial firm support is 154.88, the 20-day EMA. The trend condition in {GB} Gilts remains bullish and pullbacks are considered corrective. Two support level to watch are:

- 116.33, 50-day EMA.

- 116.27 Trendline support drawn from the Jun 16 low.

EQUITIES: Early Europe Gains Led By Tech And Real Estate

- Asian markets closed mostly higher: Japan's NIKKEI closed up 73.37 pts or +0.26% at 28249.24 and the TOPIX ended 4.24 pts higher or +0.22% at 1951.41.China's SHANGHAI closed up 9.907 pts or +0.31% at 3236.934 and the HANG SENG ended 156.17 pts lower or -0.77% at 20045.77.

- European equities have gained to start the week, with Tech and Real estate names leading: the German Dax up 39.63 pts or +0.29% at 13632.63, FTSE 100 up 30.59 pts or +0.41% at 7470.07, CAC 40 up 42.03 pts or +0.65% at 6514.34 and Euro Stoxx 50 up 17.85 pts or +0.48% at 3748.87

- U.S. futures have edged higher too, with the Dow Jones mini up 54 pts or +0.16% at 32811, S&P 500 mini up 9.5 pts or +0.23% at 4156.25, NASDAQ mini up 55.5 pts or +0.42% at 13284.25.

COMMODITIES: Silver Gains Stand Out Amid Broader Softness

- WTI Crude down $0.7 or -0.79% at $88.42

- Natural Gas down $0.2 or -2.52% at $7.86

- Gold spot down $1.57 or -0.09% at $1773.38

- Copper down $0.4 or -0.11% at $354.8

- Silver up $0.14 or +0.68% at $20.0257

- Platinum down $4.2 or -0.45% at $931.77

FOREX: A mixed start in FX ahead of US CPI Wednesday

- A mixed start for FX, EUR and USD started the session in the red, with some market participants fading some of the post US NFP price action.

- EURUSD traded back above the 1.0200 figure, and printed a 1.0215 high, but failed to pullback towards pre NFP level, was trading circa 1.0231 pre data.

- EURUSD has since faded and is now trading at 1.0182 at the time of typing.

- Similar for Cable, traded above 1.2100 in early trade, and printed 1.2123, just short of the pre NFP levels at around 1.2140.

- Cable is now trading at 1.2082.

- Some desks have likely squared, locked some positions in early trade, but liquidity, turnovers remains on the very low side.

- Market participants will likely position for the US CPI, with consensus going for a slowdown median reading of 0.2% MoM versus 1.3% last Month.

- Range for the data is 0.0% to just 0.4%.

- Looking ahead, there's no tier 1 data for the session, and notable data for the week, sees Norway CPI, German CPI final, US CPI, Czech CPI, Russia CPI (wed), US PPI (thu), Swedish CPI, UK GDP, French and Spain final CPIs, US prelim Michigan (fri).

| Date | GMT/Local | Impact | Flag | Country | Event |

| 08/08/2022 | 1500/1100 | ** |  | US | NY Fed survey of consumer expectations |

| 08/08/2022 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 08/08/2022 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 09/08/2022 | 2301/0001 | * |  | UK | BRC-KPMG Shop Sales Monitor |

| 09/08/2022 | 0900/1000 | ** | | UK | Gilt Outright Auction Result |

| 09/08/2022 | 1000/0600 | ** | | US | NFIB Small Business Optimism Index |

| 09/08/2022 | 1230/0830 | ** | | US | Preliminary Non-Farm Productivity |

| 09/08/2022 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 09/08/2022 | 1400/1000 | ** | | US | IBD/TIPP Optimism Index |

| 09/08/2022 | 1530/1130 | ** | | US | US Treasury Auction Result for 52 Week Bill |

| 09/08/2022 | 1700/1300 | *** | | US | US Note 03 Year Treasury Auction Result |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok