Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Treasuries remain off earlier highs but hold richer despite another 10Y auction tail, whilst equities shunt higher in a break of technical resistance for the S&P E-mini as the USD index gyrates its way higher on the day and oil slumps.

- US CPI headlines tomorrow's docket followed by the FOMC decision on Wed (previews for both at the bottom of this e-mail).

US TSYS: A Mixed Session Ending Modestly Richer Ahead Of US CPI

- Treasuries have seen a volatile session, in part having lurched higher and then more than reversing on questionable Taiwan headlines from The Messenger early on.

- Subsequent attention was then on the twin note auctions, with the 3Y progressing smoothly before the 10Y saw another tail following its recent trend along with soft internals.

- A brief cheapening aside on the latter, the broad trend since then has been one of paring earlier losses, which have accelerated in latest trade for a still mild bull steepening on the day (2YY -2.3bps, 5YY -1.9bps, 10YY -0.4bps and 30YY -0.4bps) after a twist steepening for most of the session.

- TYU3 shifts towards the higher end of the day's range at 113-17 (up 4+ ticks) as volumes start to pick up closer to recent averages in increased activity of late but still lagging at 1.13M ahead of tomorrow’s CPI report and the FOMC decision on Wed. It doesn’t trouble resistance at 114-06+ (Jun 6 high) whilst the key bear trigger at 112-29+ (May 26/30 lows) remains exposed.

EGBs-GILTS CASH CLOSE: Gilt Yields Jump With Data And Event Risk Looming

Gilts easily underperformed across global core instruments Monday, with UK yields up nearly double-digits in parallel across the curve. The German curve twist steepened ahead of the ECB decision on Thursday.

- Amid a fairly quiet session for data and headlines, it was difficult to identify a trigger for large moves in the afternoon, which saw yields spike from 2pm UK time onward. The move was made slightly more baffling by a sharp drop in oil prices alongside.

- There was not much new from BoE's Mann this afternoon, whose comments unsurprisingly leaned hawkish (pointing out her concerns that services inflation remained "sticky"), but desks reported some squaring of long positions in Gilts.

- The latter came in the context of risks looming large for the rest of the week, including data (US CPI Tuesday) and event (Fed, ECB, BoJ decisions) flashpoints.

- Periphery spreads mostly tightened against a risk-on backdrop with equities gaining through most of the session.

- The exception was Greece, which underperformed in the wake of Fitch's decision Friday to to affirm Greece’s BB+; Outlook Stable sovereign credit rating status.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.2bps at 2.914%, 5-Yr is down 0.1bps at 2.421%, 10-Yr is up 1.1bps at 2.388%, and 30-Yr is up 3.4bps at 2.55%.

- UK: The 2-Yr yield is up 9.5bps at 4.636%, 5-Yr is up 9.7bps at 4.347%, 10-Yr is up 9.9bps at 4.338%, and 30-Yr is up 9bps at 4.572%.

- Italian BTP spread down 6.8bps at 166.9bps / Greek up 4.2bps at 132.8bps

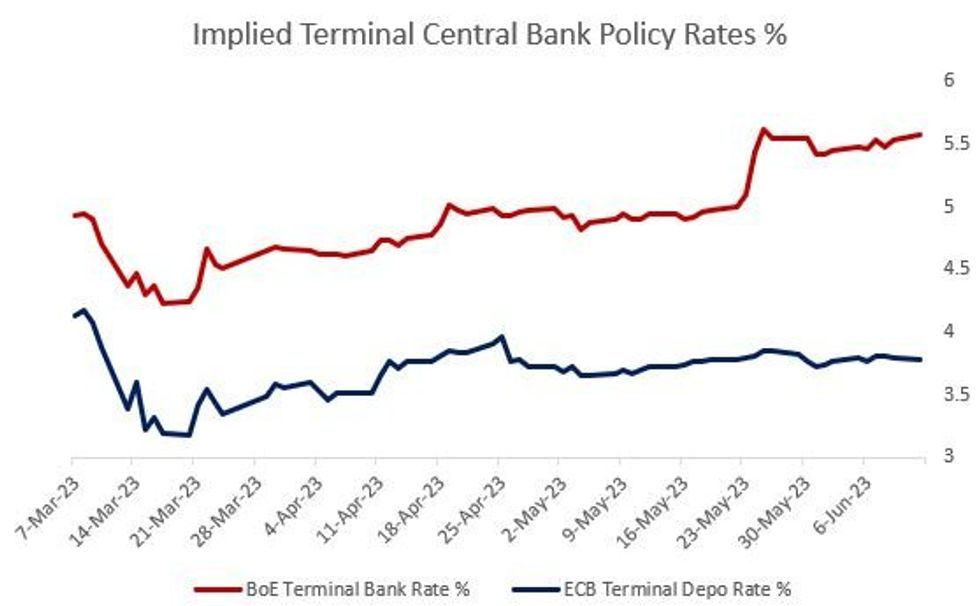

STIR: BoE Hike Pricing Hits 12-Session High, ECB Steady

BoE peak rate hike pricing saw its highest closing level Monday since May 25, with ECB pricing relatively flat ahead of Thursday's decision.

- ECB terminal depo Rate pricing -0.7bp to 3.78% (53bp of further hikes left in the cycle). A very high (92%) implied probability remains of a quarter-point hike on Thursday.

- BoE terminal Bank Rate pricing +4.1bp to 5.58% (108bp of further hikes left in the cycle). While there was no single driver at play, hawkish-leaning commentary by BoE's Haskel and Mann were seen contributing to the move.

- We also note that BoE pricing has lately seemed relatively more sensitive to non-UK central bank (eg Bank of Canada last week) pricing as compared to the ECB, so there is perhaps relatively high event / data risk being considered ahead of the US CPI data tomorrow and the potentially hawkish Fed / BoJ decisions later in the week.

FOREX: Early Greenback Weakness Reverses Course, GBP and CHF Underperform

- With market participants keenly awaiting the latest inflation data from the US on Tuesday, just a day before the June FOMC decision, there was a distinct lack of follow through on early currency moves on Monday. As such, initial greenback weakness swiftly reversed course with the USD index turning positive as we approach the APAC crossover after prior intra-day losses of around 0.35%.

- In similar vein, perhaps the best performing G10 currencies late last week, GBP and CHF, were among the weakest to start this week with potential short-term positioning dynamics in play amid the considerable amount of event risk this week.

- The pullback in GBPUSD places the pair around 90 pips off the multi-week high posted this morning at 1.2599. It’s worth noting that there was little sign of a pick-up in volumes behind the initial sell-off with only light activity noted on the slip from 1.2560 to 1.2535, however the pair did slide all the way to 1.2487 lows.

- Resistance at 1.2545, the Jun 2 high, was cleared last week, and today’s early gains have resulted in a print above 1.2592, 50.0% of the Mar 8 - May 10 bull run. A clear break of this level would expose key resistance at 1.2680, the May 10 high. Initial firm support has been defined at 1.2369, the Jun 5 low.

- USDCHF also extended its recovery on Monday as 0.90 appears to have put a short-term floor in the price action. As a reminder, last week’s more hawkish comments from the SNB prompted a sharp bout of CHF strength that has now completely unwound. EURCHF has notably risen to a one-month high just below the 0.98 handle.

- A quick note that the Chilean peso has fallen a sharp 2.5% on Monday as markets provide a short-term reaction to the freshly announced program to increase their USD reserves.

- Tuesday brings UK unemployment data and German ZEW, however, the focus for global markets remains squarely on US CPI with consensus still buying into the Fed skip narrative for now.

US RATES OPTIONS: Mixed SOFR Trade As Fed Week Begins

Monday's US rates options flow included:

- 0QU3 96.25c, bought for 35 in 5k

- SFRM3 94.75/94.87/95.00c fly, sold at 4 in 2k

- SFRM3 94.81/94.87cs, bought for 1.25 in 5k

- SFRM3 94.75/94.81cs traded for 3.25 in 3.5 in 7.5k.

- SFRM3 94.75/94.81/94.87c fly, traded 2.25 in 4k.

- SFRM3 94.7500/94.6875 put spread paper paid 2.0 on 2.5K, looks like a buyer

- SFRM3 94.81/94.75/94.68p fly traded 1.25 in 3k.

- SFRM3 94.87/94.81/94.75p fly traded 2.25 in 1k.

- SFRN3 94.31/94.18ps, traded 1 in 4k.

- SFRU3 94.25/94.00ps 1x2 traded -0.25 in 3k.

- SFRU3 95.375/95.250 put spread, 6K lots blocked at 11.0. Looks like a seller

- SFRZ3 94.87/94.75/94.62/94.50p condor traded 2.5 in 3k.

- 0QM3 95.56/95.43ps, traded 3 in 3.5k.

- 0QZ3 95.62/95.37/95.12p fly traded 5.5 in 2.5k.

- 0QZ3 98.75/99.00cs traded 1 in 6k.

EU RATES OPTIONS: Multiple Structures Monday Eye September Rate Upside

Monday's Europe rates/bond options flow included:

- OEN3 117.50/118.75cs, bought for 14 in 5k

- SFIU3 94.60/94.75 call spread bought for 7.5 in 4k (vs 94.62)

- SFIU3 94.75/94.85 1x1.25 call spread bought for 1.25 (bought the 1) in 3k

- ERU3 96.75/97.00 call spread bought for 1 in 2.5k

US STOCKS: Equities Break Higher As Resistance Cleared

- Having pushed through Friday’s aforementioned high of 4369.50, ESA has quickly gained to a new high of 4389.50.

- Resistance next sits at the round 4400 and then 4427.19 (1.618 projection of the May 4-19-24 price swing).

- As opposed to earlier gains which looked in lockstep with intraday Treasury gains, this move looks more in isolation, potentially on those technical factors.

- Within the SPX, 0.6% gains are led by IT (+1.7%) and consumer discretionary (+1.7%), the former in turn led by semi-conductors although with NVIDIA lagging after last month’s surges.

- Losses meanwhile are concentrated in energy (-1.4% - unsurprising with WTI’s further slide back notably below $70) and less so utilities/real estate (-0.4%). That said, financials only trading -0.3% mask larger pressures on banks of -0.9%, in turn smaller losses than the KBW index at -1.5% but more in line with its regional version at -1.1%.

- Recent headline from Barclays helps play into the weaker banks theme already established on the day: *BARCLAYS SEEING US DELINQUENCIES RISING SLIGHTLY ON THE MARGINS - bbg

COMMODITIES: Crude Slumps Further As Production Cuts Take A Back Seat

- Crude markets have fallen heavily today, weighed down by economic concerns and weaker demand growth expectations as the OPEC voluntary production cuts have largely been dismissed by the financial markets. Earlier, Goldman lowered its forecast Brent in Dec’23 by $9 to $86/bbl.

- The concern for a US recession is driving WTI quicker than Brent taking the front month spread down to -4.7$/bbl.

- WTI is -4.53% at $66.99, again probing $67.03 (May 31 low) after which lies a key support at $63.90 (May 4 low). The day’s most active strikes for the CLN3 have been $70/bbl calls closely followed by $65/bbl puts.

- Brent is -4.0% at $71.79 having pushed through $73.58 (Jun 8 low) to open $71.50 (May 31 low).

- Gold is -0.2% at $1957.36 as it struggles to gain traction amidst USD strength. It remains above support at $1932.2 (May 31 low).

US TSYS/SUPPLY: 10Y Auction: Another Tail With Soft Internals

- The 10Y auction continued it recent poor run, tailing for four auctions running, this time with 1.5bps (high yield 3.791% vs Bloomberg WI 3.776%). It follows a 1.1bp tail in May and a prior five-auction average tail of 0.6bps.

- Primary dealers see a sizable pick-up at 17.80% (May 13.04%, 5-auction av 13.67%), with the share taken out of indirects at 62.28% (May 67.5%, 5-auction av 67.84%) for its lowest since December.

- Bid-cover also on the low side, at 2.36 vs May 2.45 and 5-auction av 2.47, lowest since March.

- 10YY have lifted ~1bp since shortly before the auction for +4.3bps on the day amidst the bear steepening with 2s10s pushing +3.7bps higher on the day at -81bps.

US TSYS/SUPPLY: 3Y Auction: Very Modest Tail Sees Limited Reaction

The slightest of tails on the 3Y auction: 0.2bp on 4.202% high yield vs Bloomberg's when-issued 4.200%.- Looking at the periphery stats, nothing remarkable:

- Dealer takeup was pretty much exactly in line with the prior 5-auction average (16.74% today vs 16.94%) with indirects taking a slightly lower 61.53% vs 65.15% avg (albeit with a very high 73.4% in May which skewed the average higher).

- Bid-cover at 2.70x slightly softer than May's 2.93x but again, last month was an outlier - the 5 auction average is 2.68x.

- In keeping with the result, there was very modest weakness in the aftermath of the auction, with the tenor cheapening by <0.5bp. We move on to the 10Y re-open at 1300ET.

MNI US CPI Preview, Jun'23: Core CPI Seen Easing Only Slightly As FOMC Meeting Begins

EXECUTIVE SUMMARY

- Consensus puts core CPI inflation at 0.4% M/M in May but with skew to the downside.

- Used car inflation, despite still strong estimates, is seen as the largest single drag on the month relative to April after a particularly strong increase. It could however be offset by a bounce in hotel prices.

- For core services, key rent measures are seen softening slightly after a mild and expected re-acceleration in April, whilst non-housing inflation should accelerate but with market reaction muddied after significant differences with the PCE equivalent last month.

- The market still buys into the Fed skip narrative, with +6.5bps priced for tomorrow’s decision and +20bps for a terminal in July. Falling so close to the decision could distort reaction and whilst a strong print could dial up uncertainty for tomorrow, we see bias towards a larger reaction in the event of a downside miss.

PLEASE FIND THE FULL REPORT HERE:

MNI Fed Preview - June 2023: Analyst Outlook

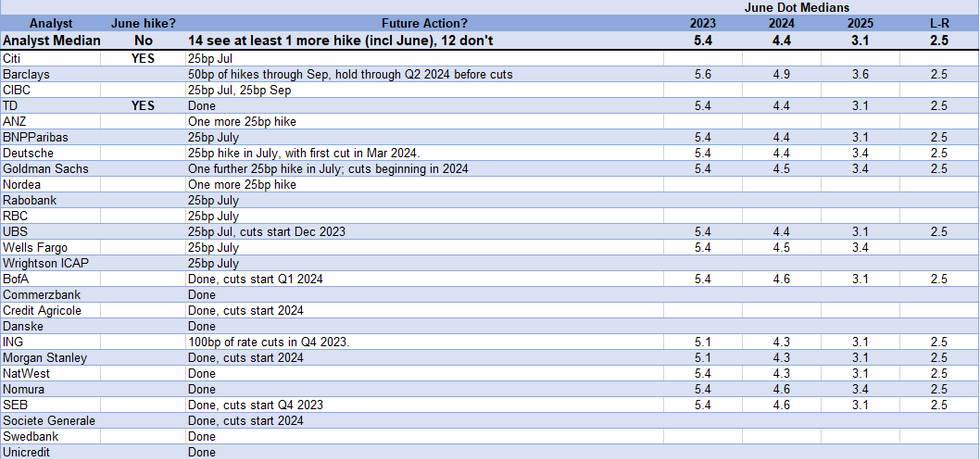

Note to readers: This is an update to the full MNI Fed preview published on Friday June 9. Please see Page 30-36 of this document for sell-side analysts outlooks for the June 2023 FOMC meeting.

EXECUTIVE SUMMARY:

- Of the 31 analyst previews of the June FOMC decision whose previews MNI have seen, all but two see a rate hold.

- Though several noted potential for Tuesday’s CPI data in particular to tilt the balance toward a hike, Citi and TD are alone in having a core view of a 25bp raise.

- Of 26 of those analysts who had explicit rate forecasts, 14 saw at least one more hike in this cycle (June included), while 12 believe the next move will be a cut. None expects >50bp of further hikes.

- The “median of medians” for the June update of the fed funds Dot Plot shows 5.4% for 2023 (up 25bp from Mar), 4.4% for 2024 (up 12.5bp from Mar), and 3.1% for 2025 (unch from Mar), with nobody expecting a change in the longer-run rate at 2.5%. However, expectations for the distribution of dots varies, especially for 2023. Changes to the economic projections are only expected to be limited.

- Our updated preview also looks at analyst expectations for changes to the Statement, including dissents and guidance language.

FOR THE FULL PUBLICATION PLEASE USE THE FOLLOWING LINK:

FedPrevJun2023-2 (inclAnalystSumm).pdf

...

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok