Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

UK DATA

MNI (London)

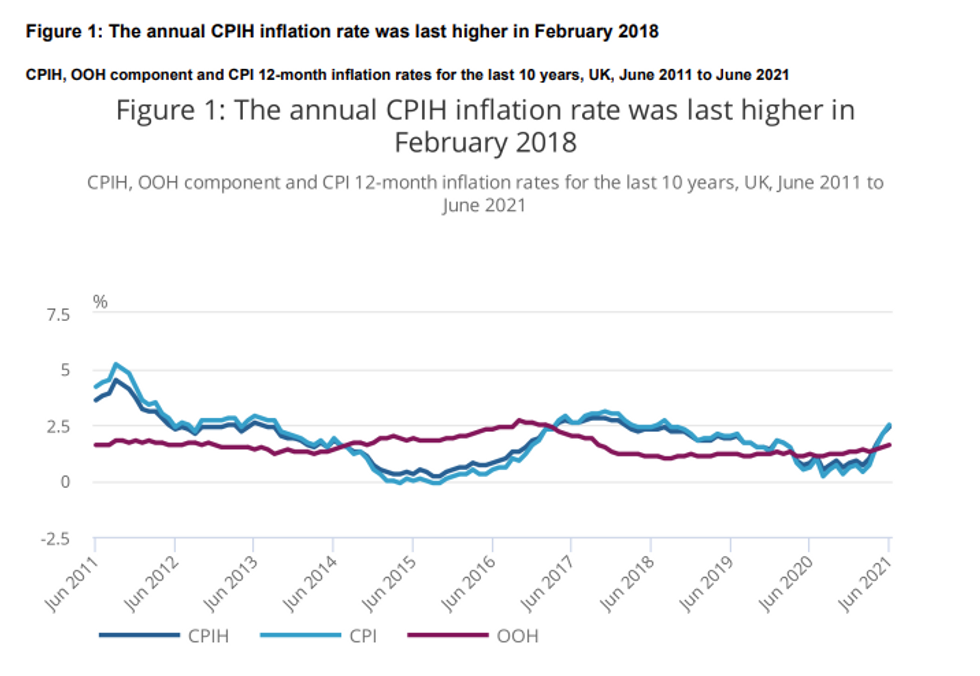

JUN CPI +0.5% M/M, +2.5% Y/Y VS +2.1% Y/Y MAY

JUN CORE CPI +0.5% M/M, +2.3% Y/Y VS +2.0% Y/Y MAY

JUN OUTPUT PPI +0.4% M/M; +4.3% Y/Y VS +4.4% Y/Y MAY

JUN INPUT PPI -0.1% M/M; +9.1% Y/Y VS +10.4% Y/Y MAY

- The Y/Y CPI jumped to 2.5% in Jun, beating markets expectations (BBG: 2.2%). This marks the second straight reading above the BOE's 2.0% target, a fourth consecutive gain and the highest level since Aug 2018.

- Core inflation rose to 2.3%, showing the highest level since Feb 2018 and coming in stronger than markets projected (BBG: 2.0%).

- The largest upward contribution came from transport, adding 0.11pp to price growth, with prices for second-hand cars (adding 0.08pp and biggest monthly rise on record) and fuels and lubricants (adding 0.06pp) being the main drivers. Fuel prices continued to increase in Jun and continue to be driven by base effects.

- The second largest positive contribution stemmed from food as well as restaurants and hotels, both adding 0.07pp to price growth in Jun.

- Clothing and footwear was another main driver of CPI growth in Jun, contributing 0.06pp to price growth. The ONS noted that clothing prices increased in Jun in contrast to a normal seasonal pattern of summer sales, which contributes to the upward pressure.

- The largest downward pressure came from games, toys and hobbies; however, price movements are particularly large in this category.

- Output inflation decelerated to 4.3% in Jun, down from 4.4% seen in May. The increase was again led by transport equipment.

- Input inflation slowed to 9.1% in May, showing the first deceleration since Aug 2020. Metals and non-metallic minerals continued to be largest drivers.

Source: Office for National Statistics

MNI London Bureau | +44 203-865-3814 | irene.prihoda@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok