Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

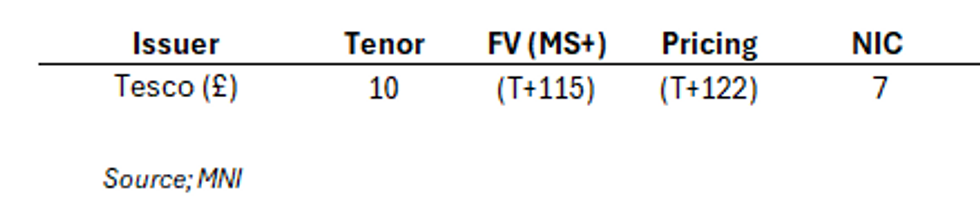

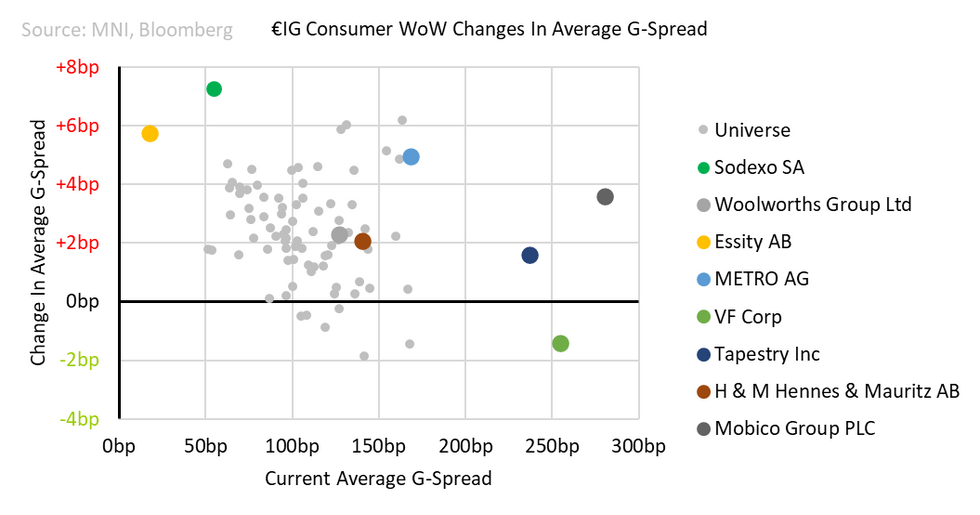

Though earnings thus far has not been a cause for concern, US April retail sales has flashed red for the first month of the 2Q. The weakness it was in non-store (i.e. online), general merchandise and health & personal care. There was growth in electronics & appliances, clothing and department stores. We wouldn't read too much into the sector level data - US card data from Bloomberg's "Second measure" did have headline weakness in April as well but sector trends did not line up with weakness more broad-based including in apparel & department stores. Outside of macro, primary was quiet with a single £Tesco 10Y that screened cheap to us - final pricing giving the staple a 5s10s term premium to match Tobacco risk. Vol in secondary was low but that should change with VF earnings next week. Key notes from this week linked below.

- Tesco sterling deal restores our faith in €31s

- A Tobacco update on Imperial earnings

- No weakness to slow down Avolta's rally

- A revisit to rising star favourite Coty after it receives its first IG rating

- Discount for IG apparel retailers looks harsh

- IS JABHOL still a consumer holdco?

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.