Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

FRANCE DATA

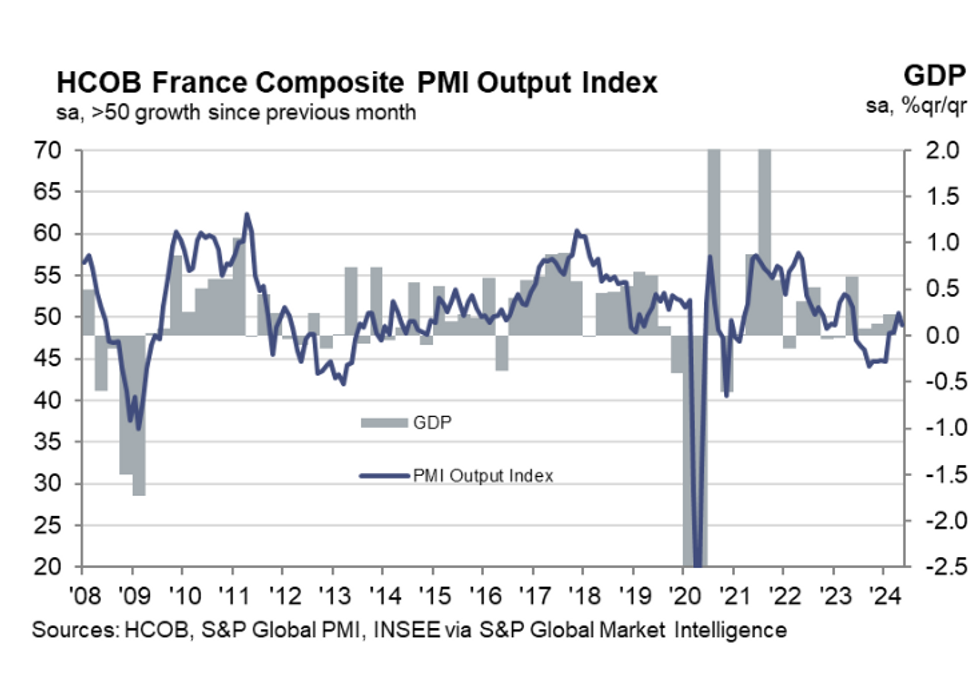

The French March flash PMI saw services drop back into contractionary territory at 49.4 (vs 51.7 cons, 51.3 prior), while manufacturing was above consensus at 46.7 (vs 45.9 cons, 45.3 prior). The composite reading was thus below consensus at 49.1 (vs 51.0 cons, 50.5 prior). Bund futures jumped around 25 ticks on release.

Notably, there continued to be little evidence of input cost pressured being passed onto output prices, indicative of weak corporate pricing power. In the wider scheme of things, this should put downward pressure on unit profits within the national accounts.

Key notes from the release:

- "The overall decline in business activity was only marginal and considerably softer than those seen on average across the ten-month contraction period between June 2023 and March of this year"

- "With exports falling sharply and at the fastest pace in the year-to-date, the latest data suggested that the expansion in total orders was driven by the domestic market".

- "Private sector employment in France continued to improve midway through the second quarter"..."Services companies were again the sole source of hiring in May, although the decrease in staffing levels across manufacturing was the weakest in almost a year".

- "Prices data showed a slight uptick in the rate of input cost inflation across France in May. Faster increases in operating expenses across both sectors resulted in the quickest overall rise for six months. Salaries and certain raw materials such as chemicals and metals inflated cost pressures, anecdotal evidence showed".

- "That said, May survey data signalled one of the softest rates of output charge inflation in over three years"

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok