Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- MNI FED LOGAN: QUITE A BIT OF ROOM FOR QT TO CONTINUE

- MNI FED LOGAN: UNTIL ON RRP FACILITY GETS TO ZERO, ROOM TO CONTINUE QT

- MNI MIDEAST: Netanyahu: Gaza Ground Operation Inevitable; Arab League To Meet Weds: Axios reporting

Key Links: MNI: Fed’s Jefferson-Higher Bond Yields Can Affect Policy Path / MNI: Logan Says Higher Term Premium Could Mean Fewer Fed Hikes / MNI: Fed's Barr Defends Proposal To Raise Capital Requirements / MNI US Employment Insight - Sep'23: Wage Dynamics Counter Biggest Beat Since January

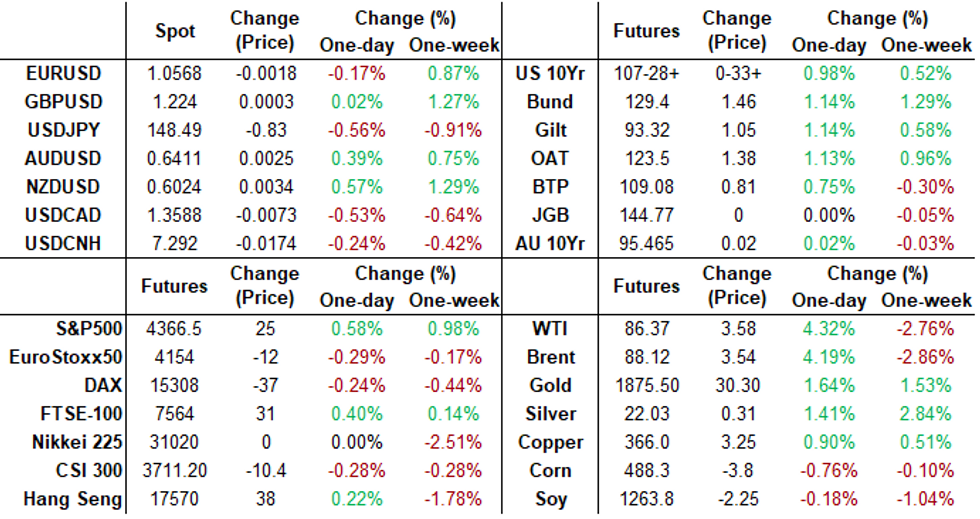

US TSYS Rates, Stocks Near Highs, Different Reasons on Same Event Risk

- Safe haven sentiment dominated markets early Monday following the surprise attack by Hamas against Israel over the weekend, tempered by a partial absence of US market participants due to the Columbus Day Holiday.

- Treasury futures extended session highs in late trade (TYZ3: 107-29 high, +1-02 on light volume: 775k) after balanced comments from Fed Vice Chair Philip Jefferson emphasizing both the threat of more persistent inflation than expected as well as the possibility of a sharper growth slowdown than is currently on investors’ radar.

- “I am particularly attentive to upside risks to inflation, such as those associated with the economy and labor market remaining too strong to achieve further disinflation, as well as risks associated with unexpected increases in energy prices,” said Jefferson.

- Meanwhile, cross assets continued to gain: crude prices remain well bid (WTI +3.5 at 86.29), stocks recovering from early losses to near highs after hte bell (SPX Eminis +24.5 at 4366.0) led by oil and gas shares as well as defense stocks on the back of the Hamas surprise attack on Israel over the weekend.

- Rate hike projections into early 2024 continue to moderate as rates head higher: November at 11.9% (22.2% this morning vs. 30.5% late Fri) w/ implied rate change of +3bp to 5.358%, December cumulative of 6.9bp (9.9bp this morning vs. 12.4bp late Fri) at 5.398%, January 2024 3.9bp (11.9bp Fri) at 5.368%. Fed terminal slips to 5.395% in Jan'24.

SOFR/TREASURY OPTION SUMMARY

SOFR/Treasury options trade revolved around low delta call structures Monday as safe haven support in underlying futures continued in late trade. As such, rate hike projections into early 2024 continue to moderate as rates climbed higher: November at 14% (22.2% this morning vs. 30.5% late Fri) w/ implied rate change of +3.2bp to 5.361%, December cumulative of 6.9bp (9.9bp this morning vs. 12.4bp late Fri) at 5.398%, January 2024 4.4bp (11.9bp Fri) at 5.413%. Fed terminal slips to 5.395% in Jan'24.

- SOFR Options:

- 1,400 0QX3 95.75/96.00 1x2 call spds ref 95.54

- 5,000 0QX3 95.00 puts ref 95.54

- 3,000 SFRZ3 94.62/94.75 call spds, ref 95.54

- 2,000 0QZ3 95.75/96.00 call spds ref 95.54

- 2,000 0QV3 95.62/95.81 1x2 call spds ref 95.51

- 2,000 SFRZ3 94.25/94.37 put spds, 1.25 ref 94.575

- 1,500 0QV3 95.12/95.25/95.37 put flys

- 2,000 0QX3 95.75/96.25/96.50 broken call flys on 1x3x2 ratio ref 95.495

- 1,500 0QV3 95.25/95.37/95.62/95.87 put condors ref 95.49

- 3,000 SFRZ3 94.25/94.37/94.43/94.50 put condors, ref 94.56

- 1,100 SFRH4 95.50/96.50 1x2 call spds ref 94.675

- 2,000 SFRZ3 94.37/94.43 2x3 put spds, ref 94.555

- 4,000 SFRM4 94.87/95.87 call spds

- 6,000 SFRM4 97.50 calls, 5.5 ref 94.885

- Treasury Options:

- over 5,000 TYX3 105.5/106.5 put spreads, 15 ref 107-21

- 10,000 weekly 10Y 105/106 put spds, 5 ref 107-18

- 2,000 TYZ3 109 calls, 43 ref 107-13.5

- 1,400 FVX3 108/109/110 call trees, ref 105-04.25

- 5,500 FVX3 107.75 calls, 3.5 ref 105-03.5

- over 15,900 TYX3 109 calls, 17 ref 107-08 to -09

- 1,500 TYZ3 109 calls, 34 ref 107-03.5

EGBs-GILTS CASH CLOSE: Bunds Lead Rally

Core European instruments rallied strongly Monday, as the Israel-Hamas conflict over the weekend helped boost safe havens.

- An early geopolitical-related bid in Bunds and Gilts faded over the course of the morning.

- While trading in cash Treasuries was closed for holidays, global yields dropped sharply in mid-afternoon on Dallas Fed Pres Logan's comment that higher market yields may mean less need for the Fed to raise rates.

- Just before those headlines crossed, EGBs benefited from a Reuters sources story pointing to little urgency at the ECB to curtail PEPP purchases ahead of schedule.

- Peripheries benefited from the latter in particular, with 10Y BTP yields falling 10+bp in the last 3 hours of European cash trade, but still finished wider of Bunds on the day.

- Bunds and Gilts leaned bull flatter, with some modest outperformance in the curve bellies, German yields down in double-digits across the curve.

- Looking ahead, Tuesday brings another quiet session for European data. BOE's Mann speaks later this evening, with Tuesday morning bringing the minutes of the BOE's financial policy meeting.

EGB Options: Mixed Rates Trade To Open The Week

Monday's Europe rates/bond options flow included:

- DUX3 105.50/105.70 call spread bought for 4.5 in 5k

- OEZ3 116.75/117.75 cs bought in 5k vs selling 2.5k of the 114.50p.Bought the cs for 12.

- ERF4 96.00/95.75 put spread paper paid 5.0on 5K. Covered via 1,250 ERH4.

- 0RZ3 96.62/97.12cs sold at 16.75 in 5k

- 0RZ3 96.12/96.00ps, bought for 1 in 7k

FOREX USD/JPY Pullback Opens Further Gap With Cycle High

- Amid unrest in the Middle-east, a rallying oil price and the partial absence of US market participants, a risk-off feel dominated currency markets into the Monday close. USD/JPY fell comfortably back below the Y149.00 handle, opening a more sizeable gap with the recent cycle high at 150.16.

- Oil-tied currencies saw a solid tailwind on the back of the rallying Brent and WTI crude price. Resultingly, NOK remained the G10 outperformer, while the uncertain geopolitical backdrop dragged SEK, which traded along with the EUR as the session's poorest performer. After finding support at parity last week, NOKSEK eyes the 200-day EMA at 1.0200 as the next key level. Above this, the 50-day EMA at 1.0247 is the bull trigger.

- The EUR traded poorly, falling against all others as a core EGB rally took. Short-term momentum across the German front-end prompted the downtrend in Schatz and Bobl futures to be reversed, prompting a ~10bps move lower in the German front-end. Resultingly, EUR lagged all others, helping EUR/GBP finish lower for a sixth consecutive session.

- Focus Tuesday turns to Australian consumer confidence, Italian industrial production and final US wholesale inventories data for August. The NY Fed also release their 1yr inflation expectations survey later in the session. Central bank speakers include Fed's Perli, Bostic, Waller, Kashkari & Daly as well as ECB's Villeroy.

FX Expiries for Oct10 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0540(E612mln), $1.0600-10(E526mln)

- USD/JPY: Y147.00-20($651mln), Y148.50-60($932mln), Y150.00-05($912mln)

- AUD/USD: $0.6350(A$1.1bln)

- NZD/USD: $0.5910(N$696mln)

- USD/CAD: C$1.3655($639mln)

Late Equities Roundup: Oil Servicers, Defense Stocks Outperform

- Stocks rebounded in the second half, the surprise attack by Hamas against Israel over the weekend helping oil and defense stocks lift indexes to session highs in late trade. Currently, S&P E-Mini futures are up 26.25 points (0.6%) at 4368.25, DJIA up 174.03 points (0.52%) at 33582.88, Nasdaq up 53.2 points (0.4%) at 13485.2.

- Leaders: Energy and Industrials outperformed early Monday, a broad based rally in oil and gas stocks supported Energy as crude rallied (WTI +3.67 at 86.46) in reaction to the attack on Israel: Haliburton +7.06%, Schlumberger +4.85%, Baker Hughes +3.4%. Meanwhile, Industrials sector buoyed as Aerospace and Defense shares remained strong in late trade: Northrop Grumman +11.2%, L3Harris Tech +9.9%, General Dynamics +8.6%.

- Laggers: Consumer Staples,. Financials and Consumer Discretionary sectors underperformed, the former weighed household and personal product stocker weighed on Consumer Staples: Estee Lauder -2.45%, Clorox -1.34%, Proctor & Gamble -0.8%. Meanwhile, Financial services shares traded weaker: Fidelity National -1.76%, State Street Corp and Morgan Stanley -0.6%. Cruise line weighed on the Consumer Discretionary sector: Carnival -4.64%, Royal Caribbean -3.06%, Norwegian -1.62%.

- Reminder, Q4 earnings cycle gets underway with several bank shares reporting this Friday: JP Morgan, Wells Fargo, Blackrock, PNC Financial and Citigroup expected.

US Daily Oil Summary: US to Crack Down on G7 Price Cap Evasion

US treasury Secretary Janet Yellen said the US is preparing to crack down on the G7 $60/bbl price cap evasion on Russian oil in a WSJ interview earlier - though comments with the news outlet were limited.

- The US needs harsher sanctions to cut off Iran’s ability to export oil, Former US House Speaker Kevin McCarthy said, cited by Bloomberg. “Allowing Iran to produce more oil makes us weaker”, he said.

- Declining US rig count data is hiding potential productivity strength suggested by other oil field indicators according to Macquarie Group. Strength in drilling permits and labour activity data could indicate the supply chain catching up and/or improving efficiency.

- Safe haven sentiment dominated markets Monday following the surprise attack by Hamas against Israel over the weekend, tempered by a partial absence of US market participants due to the Columbus Day Holiday. US$ index DXY climbed to 106-600 high (+.558) while USD/JPY fell comfortably back below the Y149.00 handle, opening a more sizeable gap with the recent cycle high at 150.16.

- Nonfarm payrolls growth comfortably beat expectations in September, posting +336k vs. Exp. +170k, topping even the highest analyst estimate. This was complimented by a +119k two-month net revision, countering the prior month’s downward adjustment.

- The average hourly earnings data were again softer than expected in September, rising 0.207% M/M (cons 0.3%) afte1r an unrevised 0.237% M/M in August, making for a second month of below-forecast wage gains.

- A Congressional Delegation to China led by Senate Majority Leader Chuck Schumer (D-NY) and Senator Mike Crapo (R-ID) met with Chinese President Xi Jinping today in Beijing.

- The biggest escalation of violence between Israel and Palestinian terrorist group Hamas in decades has significantly escalated political risk in the Middle East and risks a wider conflagration which could be complicated by political dysfunction in the United States.

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 10/10/2023 | 2301/0001 | * |  | UK | BRC-KPMG Shop Sales Monitor |

| 10/10/2023 | 0600/0800 | * |  | NO | CPI Norway |

| 10/10/2023 | 0600/0800 | ** |  | SE | Private Sector Production m/m |

| 10/10/2023 | 0800/1000 | * |  | IT | Industrial Production |

| 10/10/2023 | 0900/1000 | * | | UK | Index Linked Gilt Outright Auction Result |

| 10/10/2023 | 0930/1030 | | UK | BOE PFC minutes | |

| 10/10/2023 | 1000/0600 | ** |  | US | NFIB Small Business Optimism Index |

| 10/10/2023 | - | *** |  | CN | Money Supply |

| 10/10/2023 | - | *** | | CN | New Loans |

| 10/10/2023 | - | *** | | CN | Social Financing |

| 10/10/2023 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 10/10/2023 | 1300/0900 | | US | New York Fed's Roberto Perli | |

| 10/10/2023 | 1330/0930 | | US | Atlanta Fed's Raphael Bostic | |

| 10/10/2023 | 1400/1000 | ** | | US | Wholesale Trade |

| 10/10/2023 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 10/10/2023 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 10/10/2023 | 1700/1300 | *** | | US | US Note 03 Year Treasury Auction Result |

| 10/10/2023 | 1700/1300 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 10/10/2023 | 1700/1300 | | US | Fed Governor Christopher Waller | |

| 10/10/2023 | 1730/1330 | | US | Fed Governor Christopher Waller | |

| 10/10/2023 | 1900/1500 | | US | Minneapolis Fed's Neel Kashkari | |

| 10/10/2023 | 2200/1800 | | US | San Francisco Fed's Mary Daly |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.