Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- MNI ISRAEL: IDF Reports First Israeli Ground Troops Have Entered Gaza

- N.KOREA DELIVERED ARMS TO RUSSIA FOR USE IN UKRAINE: KIRBY, Bbg

- US TREASURY ASKS DEALERS IF 6-WK BILL SHOULD BE BENCHMARK TENOR

- FAIN: UAW STRATEGY HAS CHANGED, NEW STRIKES CAN COME ANYTIME, Bbg

- ERDOGAN: US ACTIVITY IN SYRIA IS THREATENING TURKEY'S SECURITY, Bbg

- ECB'S LAGARDE: THERE IS MORE POLICY LAG IN PIPELINE FROM PAST HIKES, Bbg

Key Links: MNI: Harker-Fed Can Hold Rates Steady, Supports High-For-Long / MNI INTERVIEW: Fed "Sweating" Yields But Lean To Hike- English / MNI US Inflation Insight, Sep'23: Strong Core Keeps Hike Alive / MNI TV: Key Exclusive Highlights For Week 41 / MNI GLOBAL WEEK AHEAD - RBA MINUTES, UK DATA, EZ HICP AND EMs

US TSYS Geopol Risk, Mixed UofM Data Buoy Rates

- Middle East conflict lent to Friday morning's risk-off/safe haven bid in US rates. Meanwhile, Russia war with Ukraine enters day 597. Dec'23 10Y futures marked an early session high of 108-00 before slipping back to 107-23.5 ((+16) after the bell; curves bull flattening: 2Y10Y -5.299 at -42.896.

- Tsys pare gains briefly, rebound slightly after University of Michigan data comes out mixed: Sentiment lower (63.0 vs. 67.0 est, 68.1 prior), Current Conditions (66.7 vs. 70.3 est, 71.4 prior), Expectations (60.7 vs. 65.7 est, 66.0 prior). Inflation expectations higher 1 Yr Inflation (3.8% vs. 3.2% est, 3.2% prior), 5-10Y (3.0% vs. 2.8% est, 2.8% prior).

- "After stabilizing earlier this year, concerns about inflation have grown again. These concerns underpin the sharp 15% deterioration in consumers’ assessments of their personal finances in this month. About 49% of consumers reported that high prices are eroding their living standards, up substantially from 39% last month and matching the all-time high last recorded in July 2022. Consumers pointed specifically to prices of food and groceries (highest share in over a year) as well as gas and fuel (highest in 2023)."

- Projected rate hikes into early 2024 consolidating: November holding at 7.8%, w/ implied rate change of +1.9bp to 5.348%, December cumulative of 8.3bp (10.6bp late Thu) at 5.412%, January 2024 cumulative 8.1bp (10.6bp late Thu) at 5.410%. Fed terminal at 5.438% in Jan'24. Fed terminal at 5.41% in Jan'24-Feb'24.

- Focus on Monday Data Calendar: Empire Mfg, Fed Speak, Tsy Bill Sales. Q4 equity earnings resume with Charles Schwab Monday; Bank of NY Mellon, Bank of America, Goldman Sachs on Tuesday.

SHORT TERM RATES

SOFR Benchmark Settlements:

- 1M +0.00083 to 5.33533 (-0.00574/wk)

- 3M +0.00896 to 5.40283 (-0.00391/wk)

- 6M +0.02414 to 5.46408 (+0.00962/wk)

- 12M +0.04785 to 5.41705 (+0.02049/wk)

- Daily Effective Fed Funds Rate: 5.33% volume: $103B

- Daily Overnight Bank Funding Rate: 5.32% volume: $255B

- Secured Overnight Financing Rate (SOFR): 5.31%, $1.467T

- Broad General Collateral Rate (BGCR): 5.30%, $579B

- Tri-Party General Collateral Rate (TGCR): 5.30%, $568B

- (rate, volume levels reflect prior session)

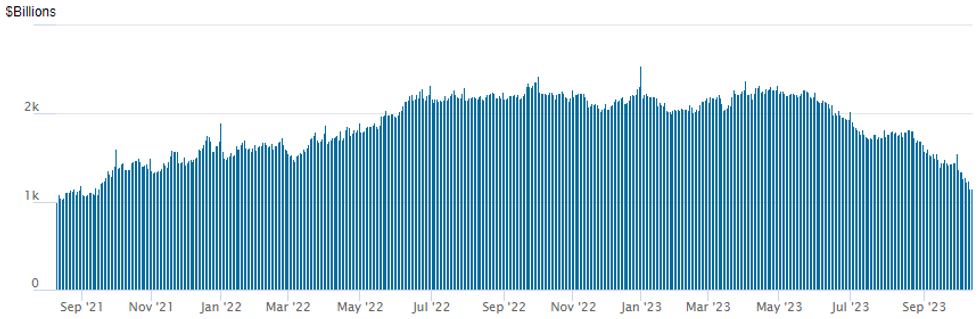

FED REVERSE REPO OPERATION: New Cycle Low

NY Federal Reserve/MNI

Repo operation usage extends to new lowest since mid-September 2021 at $1,157.319B w/98 counterparties vs. $1,151.818B in the prior session. The high for 2023 stands at $2,375.171B on Friday March 31, 2023; all-time record high of $2,553.716B reached December 30, 2022.

SOFR/TREASURY OPTION SUMMARY

SOFR/Treasury option flow remained mixed on moderate volumes Friday, SOFR leaning towards better low delta calls as underlying futures held gains since midmorning. Ongoing Middle East conflict spurred safe haven buying early. Projected rate hikes into early 2024 are consolidating: November holding at 7.8%, w/ implied rate change of +1.9bp to 5.348%, December cumulative of 8.3bp (10.6bp late Thu) at 5.412%, January 2024 cumulative 8.1bp (10.6bp late Thu) at 5.410%. Fed terminal at 5.438% in Jan'24. Fed terminal at 5.41% in Jan'24-Feb'24.

- SOFR Options: Reminder, October options expire Friday

- +5,000 SFRH4 95.50/96.00/96.50 call flys, 1.0

- Block, 5,000 SFRM4 96.00/97.00 call spds, 8.5 vs. 94.86/0.10

- +10,000 SFRZ3 95.00/95.50 call spds, 1.0 vs. 94.54/0.05%

- -4,000 0QX3 95.25 puts, 8.5

- +2,500 SFRZ3 94.56/94.68/94.81/94.93 call condor w/ 94.62/94.87/95.00 call fly, 6.75 total db

- Block, 5,000 SFRZ3 94.06/94.37/94.43 broken put trees, 1.5 1-leg over vs. 94.565/0.10%

- 2,000 0QZ3 94.75/95.00/95.25 2x3x1 put fly ref 95.43

- 3,000 0QZ3 95.25/95.50 put spds vs. 2QZ3 95.87/96.12 put spds

- 2,500 0QZ3 95.50 calls 21.0 last

- 8,000 SFRZ3 94.62/SFRF4 94.68 put calendar spd

- 5,000 SFRZ3 94.56 straddles ref 94.555

- 5,000 SFRV3 94.56/94.62/94.68/94.75 call condor ref 94.555 to -.56

- 4,500 SFRV3 94.50/94.62 put spds ref 94.56

- 1,000 SFRX3/SFRZ3 94.62/94.68 call spd spd ref 94.555

- Treasury Options:

- 10,000 TYX3 108 calls, 42 ref 107-30/0.46% total volume >15k

- 2,500 USZ3 104/106/108/110 put condors, 19 ref 112-31

- 7,000 TYX3 108.5 calls, 24

- over 4,200 FVZ3 106.5 calls, 19 last

- over 2,400 FVZ3 104 puts, 17.5 last

- over 5,400 TYZ3 109 calls, 37 last

- over 4,600 TYX3 106 puts, 8 last

- over 4,400 TYX3 107 puts, 22 last

- over 6,600 TYX3 109 calls, 14 last

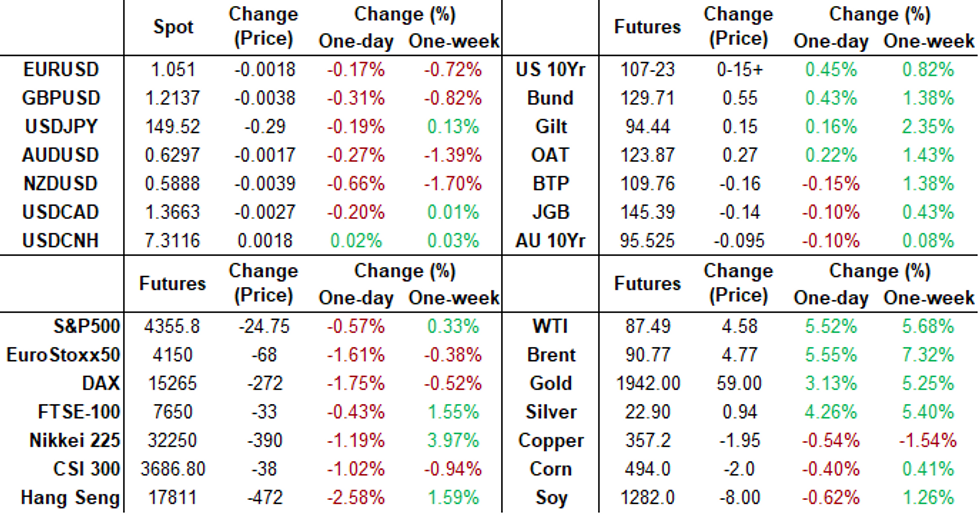

EGBs-GILTS CASH CLOSE: Safe Haven Bid Into The Weekend

Friday's trade saw a strong safe haven bid develop going into the weekend, with geopolitical risk boosting core European FI.

- Bunds and Gilts climbed for most of the session before fading toward the cash close.

- At their strongest intraday point, bonds regained the ground lost Thursday after the strong US inflation report - as the dollar gained and equities fell in anticipation of potential risk-off weekend developments in the Middle East.

- The German curve bull flattened with the UK's twist flattening.

- In line with the safe-haven bid, periphery spreads widened for most of the session, with 10Y BTP widening past the 200bp mark once more to close on the wides (204bp). ECB's Visco and Simkus played down fragmentation risks and the need for ECB intervention over spreads.

- The UK takes centre-stage next week with labour market data out Tuesday and CPI on Wednesday.

- Potential ratings actions after Friday's close include Moody's on the EU and DBRS on Malta.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 2.2bps at 3.139%, 5-Yr is down 3.7bps at 2.679%, 10-Yr is down 4.9bps at 2.737%, and 30-Yr is down 4.2bps at 2.933%.

- UK: The 2-Yr yield is down 0.4bps at 4.846%, 5-Yr is down 1.1bps at 4.46%, 10-Yr is down 3.7bps at 4.386%, and 30-Yr is down 3.5bps at 4.829%.

- Italian BTP spread up 6.2bps at 203.9bps / Greek up 5.8bps at 156.3bps

EGB Options: Limited Upside Trades Friday

Friday's Europe rates / bond options flow included:

- OEX3 116.50/117/cs vs 115.5p, bought the cs for 1 in 1k

- RXX3 132c, bought for 21 in 2k

FOREX USD Index Ends Week On Firm Footing Amid US Inflation Worries/Risk Off

- US PPI, CPI and the University of Michigan inflation expectations data beat expectations this week. One of these in isolation could have been brushed off by the Fed, but all three happening on three consecutive days could be too much to ignore. This has underpinned a strong greenback recovery and the USD index looks set to close the week around 0.65% higher.

- Furthermore, equities slipped to their worst levels of the session amid headlines from Politico stating that an Israeli ground invasion of Gaza is imminent. Additional newswires then confirmed Israeli military a number of a small raids have been conducted by their personnel inside the Gaza Strip. The first time that it has confirmed forces are on the ground.

- The real haven flow on Friday has seen the Swiss Franc outperform all others in G10. EURCHF trades down 1% on the session and the move has been exacerbated by the break below the year’s lows at 0.9516, triggering an extension to lows of 0.9457 as of typing. The next notable downside target resides at 0.9410, the September 2022 lows.

- GBPUSD also trades with a downward bias, continuing to grind lower throughout the US session with US PPI, CPI and the University of Michigan inflation expectations data all beating expectations this week and underpinning the greenback recovery. For now, last week’s fresh cycle lows remain in view, which has reinforced bearish conditions over the medium-term. 1.2028, the Mar 16 low will be the key downside target and any short-term gains are considered corrective.

FX Expiries for Oct16 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0550(E990mln), $1.0540-50(E763mln), $1.0685-95(E2.6bln)

- USD/JPY: Y148.00($544mln), Y149.35-55($554mln)

- GBP/USD: $1.2755(Gbp584mln)

- AUD/USD: $0.6400(A$968mln), $0.6480-00(A$620mln)

- USD/CAD: C$1.3550($1.0bln)

- USD/CNY: Cny7.3200($1.1bln)

Late Equities Roundup: Crude Surge Buoys Energy Sector Stocks

- Stocks remain mixed in late Friday trade, off early, pre-data highs with Dow stocks still outperforming. Currently, S&P E-Mini futures are down 27.5 points (-0.63%) at 4356, Nasdaq down 169.3 points (-1.2%) at 13411.88, DJIA up 4.98 points (0.01%) at 33649.24.

- Leaders: Energy, Utilities and Consumer Staples sectors outperformed in late trade, oil and gas shares buoyed the former as crude prices surged higher on Middle East concerns (WTI +4.59 at 87.50): APA +5.3%, Marathon +4.55%, EOG Resources +4.1%. Gas and electricity providers supported the Utilities sector: ATO +1.12%, NextEra +2.26%, PG&E +1.41%.

- Of note, Financial sector shares firmer but off first half highs. Banks still leading in late trade: JP Morgan, PNC Financial, Blackrock, Wells Fargo and Citigroup all beat Q4 earnings expectations this morning: Wells +3.93%, JPM +3.1%, Citi +2.53%.

- Laggers: Consumer Discretionary, Information Technology and Communication Services sectors underperformed, autos weighed on the former amid renewed threat of union worker strikes: Aptiv -2.52%, GM -2.34%, BorgWarner -1.58%, Ford -1.42%. Semiconductor shares weighed on the IT sector: ON Semiconductor -4.16%, NXP -3.93%, Teradyne and Microchip Technology both -3.75%. Media and entertainment shares weighing on the former in early trade: Match Group -5.5%, Meta -3.22%, Live Nation -2.50%.

- Banks announce Q4 earnings early next week: Next Monday: Charles Schwab; Tuesday: Bank of NY Mellon, Bank of America, Goldman Sachs.

E-Mini S&P TECHS: (Z3) Bear Cycle Hits Pause

- RES 4: 4566.00 High Sep 15 and a key resistance

- RES 3: 4514.50 High Sep 18

- RES 2: 4431.80 50-day EMA

- RES 1: 4430.50 High Oct 12

- PRICE: 4359.00 @ 1510 ET Oct 13

- SUP 1: 4235.50 Low Oct 4

- SUP 2: 4194.75 Low May 24

- SUP 3: 4166.25 1.50 proj of the Jul 27 - Aug 18 - Sep 1 price swing

- SUP 4: 4134.00 Low May 4

The e-mini S&P trades higher for a fifth consecutive session, with the index narrowing in on the cluster of resistance at the 50/100-dmas for the Dec contract. Overall, a bear cycle remains in play, however downside momentum has paused in favor of a corrective rally. Pivot resistance remains above at the 50-day EMA at 4431.80, with the medium-term outlook remaining bearish the longer price holds below this level.

COMMODITIES Brent Crosses $90/b Amid Geopolitical Risks

Brent crude has crossed the $90/b level as the oil complex continues to see a geopolitical risk premium due to the intensifying conflict in between Israel and Hamas and fears of further escalation.

- Brent DEC 23 up 5% at 90.27$/bbl

- WTI NOV 23 up 5% at 87.08$/bbl

- Particularly of concern if the possibility of the conflict spreading and involving Iran.

- The weekend attacks risk retaliation towards Iranian oil infrastructure as well as the potential for US sanctions against it to be further tightened.

- Whether the US tightens the implementation of sanctions on Iran could remove up to 0.5m b/d of Iranian oil from the market, Vandana Hari, Founder of Vanda Insights told CNBC.

- Headlines on Wednesday suggested Iran was unaware of the attacks, prompting a sell off which has since reversed as Israeli retaliation intensifies.

- The conflict has also halted any possibility of a US-backed normalization deal between Israel and Saudi Arabia. Reuters reported Oct. 13 that Saudi Arabia was putting the plans on ice due to the escalation. There was some hope that a deal could bring Saudi Arabia to end its voluntary output cut of 1m b/d early.

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 16/10/2023 | 0800/1000 | ** |  | IT | Italy Final HICP |

| 16/10/2023 | 0830/0930 |  | UK | BOE's Pill Speech at the OMFIF BOE's Pill Speech at the OMFIF | |

| 16/10/2023 | 0900/1100 | * |  | EU | Trade Balance |

| 16/10/2023 | 1230/0830 | ** |  | CA | Monthly Survey of Manufacturing |

| 16/10/2023 | 1230/0830 | ** | | CA | Wholesale Trade |

| 16/10/2023 | 1230/0830 | ** |  | US | Empire State Manufacturing Survey |

| 16/10/2023 | 1430/1030 | ** | | CA | BOC Business Outlook Survey |

| 16/10/2023 | 1430/1030 | | US | Philadelphia Fed's Pat Harker | |

| 16/10/2023 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 16/10/2023 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 16/10/2023 | 2030/1630 | | US | Philadelphia Fed's Pat Harker |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.