Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- BOC RAISES KEY INTEREST RATE TO 1% FROM 0.50%

- FED GOV WALLER: ECONOMY CAN TAKE AGGRESSIVE FED ACTIONS, Bbg

- WALLER: REPEATS HE FAVORS FRONT-LOADING POLICY TIGHTENING, Bbg

- WALLER: DOESN'T RELIEVE FED OF JOB OF REMOVING ACCOMMODATION, Bbg

- RUSSIA WILL VIEW U.S. AND NATO VEHICLES TRANSPORTING WEAPONS ON UKRAINIAN TERRITORY AS LEGITIMATE MILITARY TARGETS - RUSSIAN DEPUTY FOREIGN MINISTER TO TASS

US TSYS: Yield Curves Pare Back Steepening Late

Rates finish modestly higher -- bonds at upper half of range since midmorning. Yield curves still steeper but off highs as short end pared gains w/ block sellers in 2s and 5s late. Tsy 2s10s at 34.272 (+3.094) vs. 38.183 high; 5s30s at 4.289 (+1.266) vs. 8.309 high.

- Tsys bounced after delayed buying not necessarily tied to March reading of the Producer Price Index gained +1.4% MoM vs. +1.1% exp (+11.2% YoY vs. +10.6% exp).

- Geopol risk moving closer to front burner again after Russia state media TASS reported US weapons convoy/deliveries to Ukraine to be viewed as valid targets. Meanwhile, Sweden and Finland appear closer in joining NATO (see 0636ET and 0732ET bullets), potentially expanding NATO-aligned country boarders w/ Russia threefold to appr 1000 miles from 300 now.

- Tys pared gains, bouncing back near midday highs after $20B 30Y auction re-open (912810TD0), Bond sale tails slightly: 2.815% high yield vs. 2.804% WI; 2.30x bid-to-cover vs. 2.46x last month.

- Busy day for economic data Thu, Fed speak on early close ahead extended Easter holiday weekend (Friday close): weekly claims, retail sales, import/export prices, business inventories and U-Mich sentiment. NY Fed Williams Bbg interview at 0845ET, Cleveland Fed Mester and Philly Fed Harker after the close.

- The 2-Yr yield is down 3.7bps at 2.3686%, 5-Yr is down 2bps at 2.669%, 10-Yr is down 1.1bps at 2.7101%, and 30-Yr is up 0.2bps at 2.8109%.

CANADA

MNI: BOC RAISES KEY INTEREST RATE TO 1% FROM 0.50%

- BANK OF CANADA STARTING QUANTITATIVE TIGHTENING ON APRIL 25

- BOC SAYS QT WILL INVOLVE ASSET ROLL-OFF OVER TIME

- BOC: RATE MUST RISE FURTHER, PACE HINGES ON ECONOMY, INFLATION

- BANK OF CANADA SAYS ECONOMY IS MOVING INTO EXCESS DEMAND

- BOC SEES 6% CPI IN FIRST HALF, WON'T RETURN TO 2% UNTIL 2024

- BOC SEES NOMINAL NEUTRAL RATE OF 2.5%, UP 25BP FROM PRIOR VIEW

- BOC SEES INCREASING RISK OF ENTRENCHED INFLATION EXPECTATIONS

OVERNIGHT DATA

US MAR FINAL DEMAND PPI +1.4%, EX FOOD, ENERGY +1.0%

US MAR FINAL DEMAND PPI EX FOOD, ENERGY, TRADE SERVICES +0.9%

US MAR FINAL DEMAND PPI Y/Y +11.2%, EX FOOD, ENERGY Y/Y +9.2%

US MAR PPI: FOOD +2.4%; ENERGY +5.7%

US MAR PPI: GOODS +2.3%; SERVICES +0.9%; TRADE SERVICES +1.2%

US MBA: MARKET COMPOSITE -1.3% SA THRU APR 08 WK

US MBA: REFIS -5% SA; PURCH INDEX +1% SA THRU APRIL 8 WK

US MBA: UNADJ PURCHASE INDEX -6% VS YEAR-EARLIER LEVEL

US MBA: 30-YR CONFORMING MORTGAGE RATE 5.13% VS 4.90% PREV

BOC RAISES KEY INTEREST RATE TO 1% FROM 0.50%

MARKETS SNAPSHOT

Key late session market levels:

- DJIA up 370.49 points (1.08%) at 34594.62

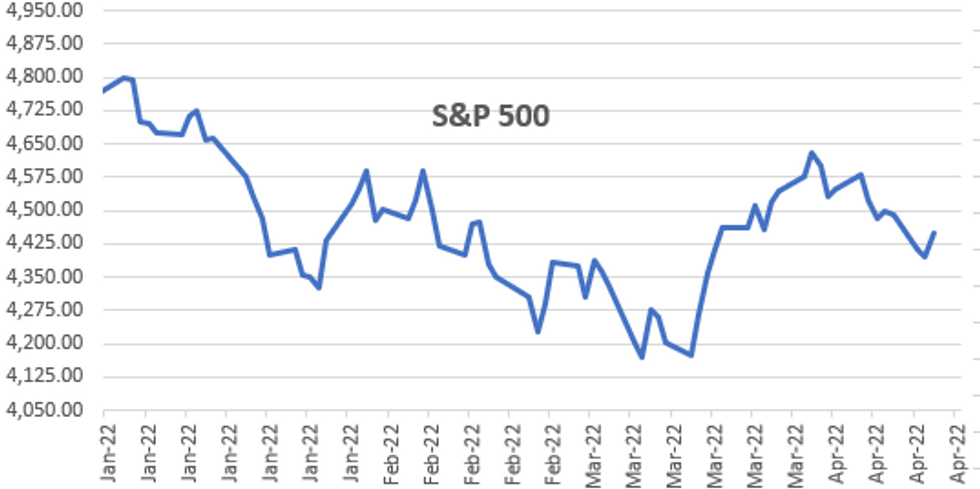

- S&P E-Mini Future up 55.5 points (1.26%) at 4449.25

- Nasdaq up 303.7 points (2.3%) at 13675.92

- US 10-Yr yield is down 1.3 bps at 2.7082%

- US Jun 10Y are up 3.5/32 at 120-19.5

- EURUSD up 0.0056 (0.52%) at 1.0884

- USDJPY up 0.32 (0.26%) at 125.7

- WTI Crude Oil (front-month) up $3.58 (3.56%) at $104.17

- Gold is up $8.31 (0.42%) at $1975.12

- EuroStoxx 50 down 3.51 points (-0.09%) at 3827.96

- FTSE 100 up 4.14 points (0.05%) at 7580.8

- German DAX down 48.51 points (-0.34%) at 14076.44

- French CAC 40 up 4.73 points (0.07%) at 6542.14

US TSY FUTURES CLOSE

- 3M10Y -0.597, 193.307 (L: 188.64 / H: 202.25)

- 2Y10Y +3.299, 34.477 (L: 30.571 / H: 38.183)

- 2Y30Y +4.766, 44.823 (L: 38.573 / H: 50.487)

- 5Y30Y +2.901, 14.804 (L: 10.771 / H: 21.407)

- Current futures levels:

- Jun 2Y up 2.625/32 at 105-29.375 (L: 105-23.375 / H: 106-02.5)

- Jun 5Y up 4/32 at 113-27 (L: 113-12 / H: 114-08)

- Jun 10Y up 7.5/32 at 120-23.5 (L: 119-31 / H: 121-07)

- Jun 30Y up 19/32 at 143-1 (L: 141-11 / H: 143-20)

- Jun Ultra 30Y up 22/32 at 165-8 (L: 163-03 / H: 166-10)

US 10Y FUTURES TECH: (M2) Corrective Bounce

- RES 4: 124–21+ 50-day EMA

- RES 3: 124-18 High Mar 21

- RES 2: 123-04 High Mar 31 and a key resistance

- RES 1: 121-06+/22-05 High Apr 7 / 20-day EMA

- PRICE: 120-11+ @ 11:18 BST Apr 13

- SUP 1: 119-10+ Low Apr 12

- SUP 2: 119-04+ Low Dec 3 2018 (cont)

- SUP 3: 118-02+ 0.618 proj of the Mar 7 - 28 - 31 price swing

- SUP 4: 117-22+ Low Nov 8 2018 (cont)

Treasuries traded to a fresh cycle low of 119-10+ Tuesday before recovering. Rallies appear corrective for now though, with this week’s cycle lows confirming a resumption of the primary downtrend and an extension of the bearish price sequence of lower lows and lower highs. MA studies also point south and scope is for a move towards 119-04+, Dec 3 2018 low (cont). Key short-term trend resistance is at 123-04, the Mar 31 high.

US EURODOLLAR FUTURES CLOSE

- Jun 22 -0.010 at 98.365

- Sep 22 +0.015 at 97.730

- Dec 22 +0.025 at 97.240

- Mar 23 +0.040 at 96.980

- Red Pack (Jun 23-Mar 24) +0.035 to +0.045

- Green Pack (Jun 24-Mar 25) +0.020 to +0.040

- Blue Pack (Jun 25-Mar 26) +0.015 to +0.020

- Gold Pack (Jun 26-Mar 27) +0.015 to +0.020

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements:

- O/N +0.00100 at 0.32729% (-0.00029/wk)

- 1 Month +0.00285 to 0.55414% (+0.04014/wk)

- 3 Month +0.00586 to 1.04429% (+0.03358/wk) ** Record Low 0.11413% on 9/12/21

- 6 Month -0.01257 to 1.55157% (+0.01114/wk)

- 1 Year -0.05628 to 2.25143% (-0.02014/wk)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 0.33% volume: $80B

- Daily Overnight Bank Funding Rate: 0.32% volume: $266B

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 0.29%, $883B

- Broad General Collateral Rate (BGCR): 0.30%, $338B

- Tri-Party General Collateral Rate (TGCR): 0.30%, $327B

- (rate, volume levels reflect prior session)

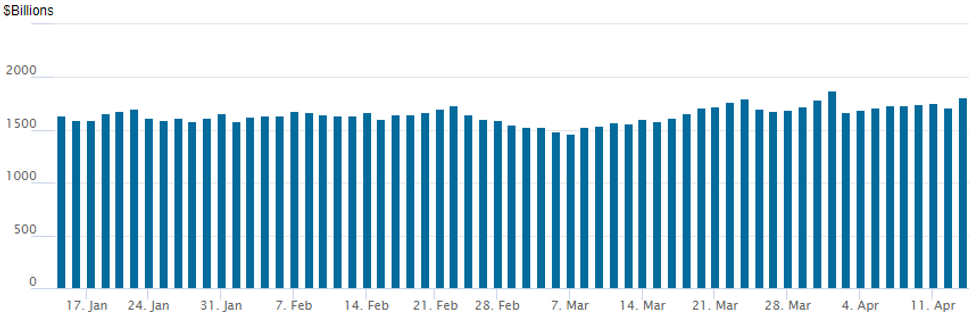

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage surged to 1,815.55B w/ 83 counterparties from prior session 1,710.414B. Compares to all-time high of $1,904.582B on Friday, December 31.

PIPELINE: IDB, Viterra Finance Launched

Wednesday high-grade issuance well off Monday's pace after $12.75B Amazon 7pt jumbo pushed week opener issuance to $23.5B. Running total for week just over $61.5B.- Date $MM Issuer (Priced *, Launch #)

- 04/13 $1B #IDB 3Y SOFR+32

- 04/13 $750M #Viterra Finance $450M 5Y +235a, $300M 10Y +265

EGBs-GILTS CASH CLOSE: Pre-ECB Rally

After jumping on the open following above-expected UK CPI data, European yields fell steady throughout Wednesday's session.

- Yields continued to move lower in the afternoon after and despite a US producer price upside surprise. Bunds bull flattened, Gilts bull steepened.

- Periphery spreads reversed earlier widening as well.

- There was no obvious fundamental driver, but with modest volumes and a long weekend / ECB decision imminent, there appeared to be an element of unwinding positions following an extended rise in yields.

- See our ECB preview (and note the title) - "Be Prepared For A Hawkish Surprise".

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.1bps at 0.074%, 5-Yr is down 2.4bps at 0.549%, 10-Yr is down 2.4bps at 0.766%, and 30-Yr is down 2.6bps at 0.901%.

- UK: The 2-Yr yield is down 1.9bps at 1.489%, 5-Yr is down 1.5bps at 1.549%, 10-Yr is down 0.4bps at 1.799%, and 30-Yr is down 0.4bps at 1.946%.

- Italian BTP spread down 1.2bps at 160.7bps / Spanish up 1.4bps at 93.6bps

FOREX: USD Retreats In Late Session, NZD Remains Poorest Performer

- The greenback has had a strong turnaround over the latter half of Wednesday trade, with the USD index (-0.4%) now looking set to snap its impressive winning streak in April that has seen the index rise from below the 98.00 mark to the earlier peak of 100.52.

- The reversal prompting firm gains in EUR, JPY, GBP and the Canadian dollar following the BOC’s 50bp rate hike and accompanying hawkish rhetoric. CAD has had the additional tailwind of higher crude futures and rising equity indices, placing USDCAD roughly 100 points off session highs.

- EURUSD came within three pips of the March lows and bear trigger of 1.0806, which now marks an interesting inflection point as we head into tomorrow’s ECB rate decision/statement with MNI flagging that markets should be prepared for a potential hawkish surprise.

- The recent failure at 1.1185, Mar 31 high, continues to highlight a bearish threat and last week’s move lower has reinforced this theme, however, a break of 1.0806 is needed to confirm a resumption of the downtrend.

- In similar vein, USDJPY has had a sharp turnaround after breaking the 2015 highs earlier in the session. After breaching 125.86, momentum buying saw the pair clear the 1.26 hurdle and trade as high as 126.32. The broad dollar weakness has seen momentum wane and a close back below the 125.86 mark would be considered a bearish development. With trend conditions still residing in overbought territory – the potential for a consolidation and/or move lower may have been bolstered.

- NZD remains the poorest performing currency in G10 following the RBNZ policy decision overnight. While the bank hiked rates by 50bps against a consensus expectation of a 25bps rise, the decision was perceived as dovish as the bank opted to bring forward the beginning of the tightening cycle, but critically stop short of raising market expectations of a higher terminal rate. The bank's minutes noted that members increased the OCR by more "now, rather than later". NZD weakness followed, putting AUD/NZD at the best levels since mid-2020.

- Aside from the ECB meeting, Aussie Employment and US Retail Sales will headline the data schedule before the long holiday weekend.

Thursday Data Calendar

| Date | GMT/Local | Impact | Flag | Country | Event |

| 14/04/2022 | 2301/0001 | * |  | UK | RICS House Prices |

| 14/04/2022 | 0130/1130 | *** |  | AU | Labor force survey |

| 14/04/2022 | 0600/0800 | *** |  | SE | Inflation report |

| 14/04/2022 | 1100/0700 | * |  | TR | Turkey Benchmark Rate |

| 14/04/2022 | 1145/1345 | *** |  | EU | ECB Deposit Rate |

| 14/04/2022 | 1145/1345 | *** | | EU | ECB Main Refi Rate |

| 14/04/2022 | 1145/1345 | *** | | EU | ECB Marginal Lending Rate |

| 14/04/2022 | 1230/0830 | ** |  | CA | Wholesale Trade |

| 14/04/2022 | 1230/0830 | ** | | CA | Monthly Survey of Manufacturing |

| 14/04/2022 | 1230/0830 | ** |  | US | Jobless Claims |

| 14/04/2022 | 1230/0830 | *** | | US | Retail Sales |

| 14/04/2022 | 1230/0830 | *** | | US | PPI |

| 14/04/2022 | 1230/0830 | ** | | US | Import/Export Price Index |

| 14/04/2022 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 14/04/2022 | 1230/1430 | | EU | ECB President Lagarde Post-meet presser | |

| 14/04/2022 | 1400/1000 | *** | | US | University of Michigan Sentiment Index (p) |

| 14/04/2022 | 1400/1000 | * | | US | Business Inventories |

| 14/04/2022 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 14/04/2022 | 1530/1130 | ** | | US | NY Fed Weekly Economic Index |

| 14/04/2022 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 14/04/2022 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 14/04/2022 | 1920/1520 | | US | Cleveland Fed's Loretta Mester | |

| 14/04/2022 | 2200/1800 | | US | Philadelphia Fed's Patrick Harker |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.