- MNI Fed Preview - June 2024: Analyst Outlook

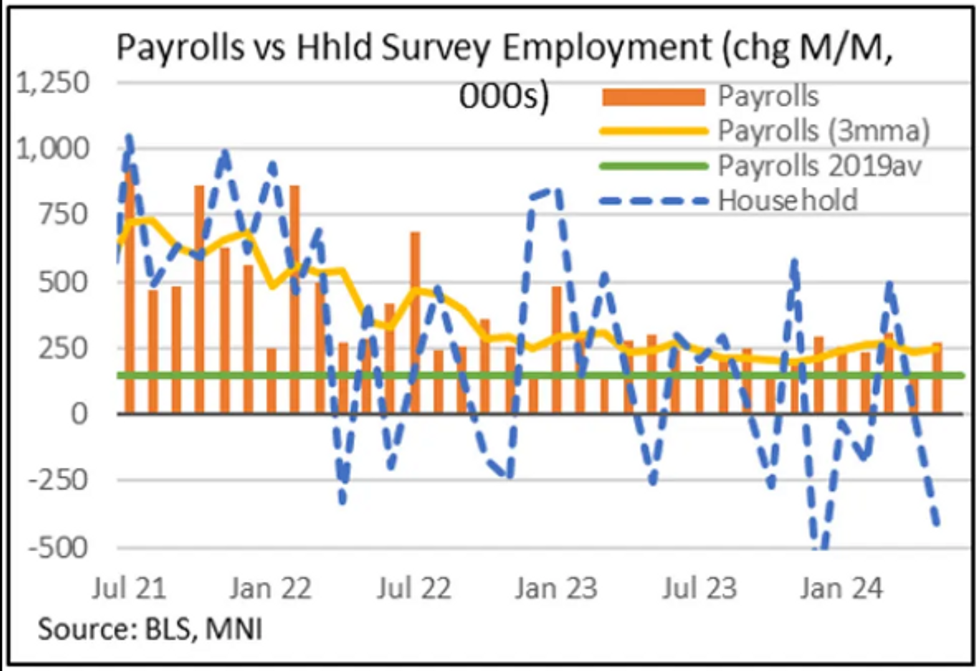

- MNI US Employment Insight, Jun '24: A Tale Of Two Surveys

US

US Fed Preview - June 2024 (MNI): Analyst Outlook: Sell-side Fed rate cut views continue to be pushed back as the June 2024 FOMC meeting approaches, now converging on September as the timing for the first cut. Ahead of March’s meeting, consensus was firmly on June.

- There are still one or two expectations for a July cut, but otherwise it’s nearly unanimous that the first Fed cut will come in Sep or Dec. JPMorgan eyes November, with SocGen the most hawkish on this front, eyeing Q1 2025.

US Employment Insight (MNI) Jun '24: A Tale Of Two Surveys: We've just published our review of the May nonfarm payrolls report, including 23 sell side analysts' takes on the data. PDF HERE

- Nonfarm payrolls not only bounced back in May from a softer April, but exceeded even the highest expectations seen in MNI’s survey of analyst previews with gains of 272k (vs 180k expected).

- A very weak Household survey which conversely saw job losses of 408k and the unemployment rate unexpectedly tick up to 4.0% cast some doubt over the strength implied by the report.

- But the overall take was that the labor market was solid in May, given broad-based strength in the headline payrolls figure across the private sector and the acceleration in wage growth.

- The immediate implication of this report is to eliminate any lingering potential for a first Fed rate cut in July, with a couple of analysts pushing back their expectations to later in 2024.

NEWS

US (MNI): Trump Pledges Tax Free Tips, Play For Swing-State Voters:

Former President Donald Trump made a pitch for low-wage swing-state voters, pledging to scrap taxes on tipped earnings at a campaign event in Las Vegas, Nevada on Sunday.

US (MNI): RFK Inches Closer To Gaining Access To First Presidential Debate Stage

Independent presidential candidate, Robert F. Kennedy Jr., has taken a step closer to qualifying for the first US presidential debate taking place on June 27 on CNN.

SECURITY (MNI): Blinken Intensifies Pressure On Hamas To Accept Hostage/Ceasefire Deal

US Secretary of State Antony Blinken has intensified pressure on Hamas to accept a US-broker ceasefire-for-hostage proposal for Gaza outlied by US President Joe Biden on May 31.

ECB (MNI): Lagarde Talks Down Prospect of Back-to-Back Rate Cuts:

In a joint interview with several European newspapers, ECB's Lagarde states that "we're not declaring victory over inflation yet [...] there might be periods with rates on hold, and rates aren't on a linear declining path". Relatively little here that we didn't get from last week's ECB press conference - the ECB President again stresses that caution is the dominant force at the ECB, and markets shouldn't expect back-to-back policy rate cuts.

EUROPEAN PARLIAMENT (MNI): Right-Wing Parties Cement Status As EPP Retains Top Spot:

The European Parliament elections of 6-9 June delivered, as was widely expected, strong results for parties of the right and far-right. The centre-right European People's Party (EPP) retained its position as the largest single political grouping, but it faces a difficult task in negotiating an agreement with the other main moderate groups; the centre-left Socialists and Democrats (S&D) and the centrist Renew Europe.

FRANCE (MNI): National Rally Projected To Win 235-265 Seats In National Assembly

Reuters reporting that, according to a new Harris Interactive Poll, the right-wing nationalist Rassembelement National (National Rally, RN) of Marine Le Pen is on track to win 235-265 seats in the French National Assembly at legislative elections to take place on 30 June and 7 July.

US TSYS Off Post-Auction Lows, Focus on Midweek CPI, FOMC

- Treasuries held lower levels by the close, just off session lows after the bell as stocks reversed early weakness. Rates held narrow ranges for most of the session, extending lows (TYU4 109-00.5, -9.5) after $58B 3Y note auction (91282CKV2) tailed 1.1bp: 4.659% high yield vs. 4.648% WI; 2.43x bid-to-cover vs. 2.63x prior month (Jan high).

- Relatively quiet start to the week, Treasuries are mirrored weaker EGBs after France President Macron called for snap election following weekend parliamentary elections.

- While far-right forces made strong gains vs. the majority center-right European People’s Party (EPP) in EU elections, Treasury futures pared losses ahead of Wednesday's May CPI and FOMC policy announcement.

- Sep'24 10Y Treasury futures are currently trading -5.5 at 109-04.5 -- inside 8-tic range: 109-00.5 low/109-08.5 high. Friday's sharp sell-off undermines the recent bullish theme, highlighting a potential bearish reversal. The TYU4 contract breached both the 50- and 20-day EMA, while continued decline would strengthen a bearish threat at at 108-27.5 (June 3 low).

- Cash yields are currently mildly higher: 5s +.0141 at 4.4767, 10s +.0296 at 4.4631%, 30s +.0354 at 4.5900%, while curves are steeper: 2s10s +3.804 at -41.735, 5s30s +2.131 at 11.161.

OVERNIGHT DATA

NY FED: ONE-YEAR INFLATION EXPECTATIONS FALL TO 3.17% VS 3.26% PRIOR

MARKETS SNAPSHOT

- Key market levels of markets in late NY trade:

- DJIA up 33.55 points (0.09%) at 38832.76

- S&P E-Mini Future up 10.5 points (0.2%) at 5365.75

- Nasdaq up 49.3 points (0.3%) at 17181.25

- US 10-Yr yield is up 3.2 bps at 4.465%

- US Sep 10-Yr futures are down 6/32 at 109-4

- EURUSD down 0.0037 (-0.34%) at 1.0763

- USDJPY up 0.29 (0.19%) at 157.04

- WTI Crude Oil (front-month) up $2.38 (3.15%) at $77.91

- Gold is up $17.32 (0.76%) at $2310.98

- European bourses closing levels:

- EuroStoxx 50 down 34.83 points (-0.69%) at 5016.48

- FTSE 100 down 16.89 points (-0.2%) at 8228.48

- German DAX down 62.38 points (-0.34%) at 18494.89

- French CAC 40 down 107.82 points (-1.35%) at 7893.98

US TREASURY FUTURES CLOSE

- 3M10Y +3.755, -93.503 (L: -99.907 / H: -93.037)

- 2Y10Y +4.002, -41.537 (L: -45.001 / H: -40.983)

- 2Y30Y +4.581, -28.846 (L: -33.008 / H: -27.83)

- 5Y30Y +2.146, 11.176 (L: 8.924 / H: 12.092)

- Current futures levels:

- Sep 2-Yr futures down 0.625/32 at 101-28.5 (L: 101-27.125 / H: 101-29.25)

- Sep 5-Yr futures down 3.25/32 at 106-0 (L: 105-30.2496000000001 / H: 106-02.25)

- Sep 10-Yr futures down 6/32 at 109-4 (L: 109-00.5 / H: 109-08.5)

- Sep 30-Yr futures down 20/32 at 116-29 (L: 116-23 / H: 117-15)

- Sep Ultra futures down 30/32 at 123-19 (L: 123-11 / H: 124-12)

US 10Y FUTURE TECHS: (U4) Reversal Signal

- RES 4: 111-17+ 1.236 proj of the Apr 25 - May 16 - 29 price swing

- RES 3: 111-09 High Apr 1

- RES 2: 110-27+ 1.00 proj of the Apr 25 - May 16 - 29 price swing

- RES 1: 110-21 High Jun 7

- PRICE: 109-06 @ 11:28 BST Jun 10

- SUP 1: 109-02 Intraday low

- SUP 2: 108-27+ Low Jun 3

- SUP 3: 108-05+ Trendline drawn from the Apr low

- SUP 4: 107-31 Low May 29 and a key support

Treasuries sold off sharply Friday and the contract remains soft for now. The move down undermines the recent bullish theme and highlights a potential bearish reversal. The contract has breached both the 50- and 20-day EMA. A continuation lower would strengthen a bearish threat and open 108-27+, the Jun 3 low. Key short-term resistance is Friday’s high of 110-21, where a break is required to reinstate the recent bullish theme.

SOFR FUTURES CLOSE

- Jun 24 steady at 94.655

- Sep 24 -0.005 at 94.805

- Dec 24 steady at 95.050

- Mar 25 steady at 95.285

- Red Pack (Jun 25-Mar 26) -0.025 to steady

- Green Pack (Jun 26-Mar 27) -0.05 to -0.035

- Blue Pack (Jun 27-Mar 28) -0.05 to -0.045

- Gold Pack (Jun 28-Mar 29) -0.045 to -0.04

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M +0.00143 to 5.32907 (-0.00217 total last wk)

- 3M +0.00922 to 5.34321 (-0.00885 total last wk)

- 6M +0.03015 to 5.30144 (-0.04290 total last wk)

- 12M +0.06755 to 5.13965 (-0.12987 total last wk)

- Secured Overnight Financing Rate (SOFR): 5.33% (+0.00), volume: $1.934T

- Broad General Collateral Rate (BGCR): 5.32% (+0.00), volume: $758B

- Tri-Party General Collateral Rate (TGCR): 5.32% (+0.00), volume: $742B

- (rate, volume levels reflect prior session)

- Daily Effective Fed Funds Rate: 5.33% (+0.00), volume: $100B

- Daily Overnight Bank Funding Rate: 5.32% (+0.00), volume: $281B

FED Reverse Repo Operation

NY Federal Reserve/MNI

- RRP usage climbs back over $400M to $416.481B from $395.462B prior; number of counterparties at 73. Compares to $327.066B on Monday, April 15 -- the lowest level since mid-May 2021.

PIPELINE: $1B ArcelorMittal 2Pt Launched

- Date $MM Issuer (Priced *, Launch #)

- 6/10 $1B #ArcelorMittal $500M 10Y +155, $500M 30Y +180

- 6/10 $600M #Take-Two $300M 5Y +95, $300M 10Y +115

- Expected to issue Tuesday:

- 6/11 $Benchmark ADB 4Y SOFR+30a

FOREX Euro Remains Soft Amid Political Concerns, EURGBP Extends Below 0.8500

- Single currency weakness is garnering much attention to start the week as the post-NFP declines for EURUSD have built momentum, exacerbated by heightened political concerns following European parliamentary elections. EURUSD has weakened 0.4% on Monday as we approach the APAC crossover, notably below support at 1.0788, the May 30 low.

- The independent Euro weakness thrusts multiple EUR crosses into the spotlight, that have been breaching/approaching significant technical levels.

- EURGBP is most interesting here, having closed below the 0.8500 mark for the first time since August 2022 on Friday. Further weakness has seen the cross clear support at 0.8484, the May 29 low and bear trigger, confirming a resumption of the downtrend. Sights are on 0.8408 next and 0.8340 below here as we approach tomorrow’s labour market data from the UK. Resistance moves down to 0.8519, the 20-day EMA.

- Positioning extremes are also likely contributing to the sharp reversal lower for EURCHF (-0.42%), having noted that the net short CHF position now sits at 46.3% of open interest - the largest short in G10, having overtaken the JPY in the past month. This could provide scope for a continuation lower for EURCHF ahead of the June 20 SNB decision.

- Slightly firmer equities see the Antipodeans outperform, with EURAUD and EURNZD both down around 0.7% on the session.

- Event risk comes thick and fast this week, starting with UK labour market figures (Tue) and GDP (Wed). Focus then turns to Wednesday’s key US CPI release before the June FOMC decision. Australia employment crosses Thursday before the BOJ decision rounds off the week.

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 11/06/2024 | 0600/0700 | *** |  | UK | Labour Market Survey |

| 11/06/2024 | 1000/0600 | ** |  | US | NFIB Small Business Optimism Index |

| 11/06/2024 | 1100/1300 |  | EU | ECB's Lane chat at Banking and Payments Federation Conference | |

| 11/06/2024 | - | *** |  | CN | Money Supply |

| 11/06/2024 | - | *** | | CN | New Loans |

| 11/06/2024 | - | *** | | CN | Social Financing |

| 11/06/2024 | 1230/0830 | * |  | CA | Building Permits |

| 11/06/2024 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 11/06/2024 | 1400/1000 | * | | US | Services Revenues |

| 11/06/2024 | 1530/1130 | ** | | US | US Treasury Auction Result for 52 Week Bill |

| 11/06/2024 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 11/06/2024 | 1645/1845 | | EU | ECB's Elderson at Annual Banking Supervision Conference | |

| 11/06/2024 | 1700/1300 | ** | | US | US Note 10 Year Treasury Auction Result |