Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- MNI INTERVIEW: Fed Pause Could Make Inflation More Entrenched

- MNI Fed Review - May 2023: High Bar To Further Hikes

- MNI Payrolls Preview: Eyeing Continued Moderation

- MNI: BOC Would Consider Persistent Market Strain For Rate Path

- MNI ECB WATCH: ECB Hikes 25Bps, Signals APP Reinvestments End

US

FED: A possible pause in interest rate hikes from the Federal Reserve in June, seen as more likely after this week’s FOMC decision and an accompanying statement that was more equivocal about future increases, could lead to more deeply embedded inflation pressures that might require even tighter policy down the line, a former top Fed staffer told MNI.

- Andrew Levin, who spent two decades as a Fed board economist, said Fed Chair Powell’s dovish hints that a pause could be forthcoming, including the argument that real interest rates are already substantially positive, fail to take into account still-elevated short-run inflation expectations of consumers and businesses.

- “There’s a very substantial possibility that inflation is going to remain elevated as far as the eye can see,” he said. Levin pointed to the Cleveland Fed's "indirect" measure of consumer inflation expectations over the next 12 months at 5.4%. For more see MNI Policy main wire at 1412ET.

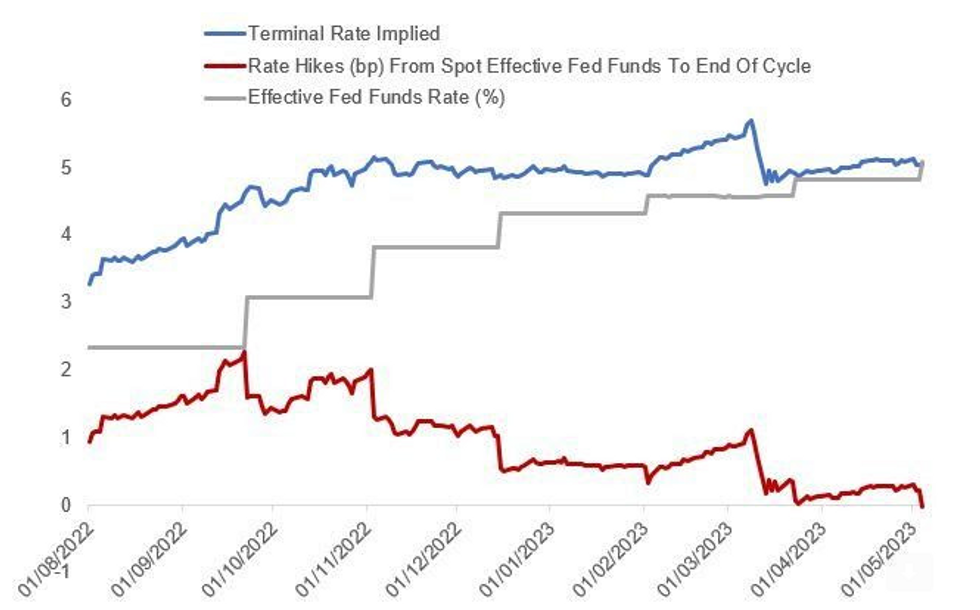

FED: Barring unexpected developments this summer, the Fed’s tightening cycle looks like it has concluded at a terminal rate of 5.00-5.25% following the 25bp hike at the May FOMC meeting.

- Based on Chair Powell's comments at the May press conference and the change in Statement language, the FOMC appears to be clinging to the last vestiges of its tightening bias going forward.

- But any intention to hike rates further is half-hearted at most, and the market and the vast majority of analysts anticipate no further tightening. Though further tightening is possible, the Fed has now set a fairly high bar to delivering another rate hike in this cycle. For more see MNI Policy main wire at 1055ET.

US: Bloomberg consensus looks for further moderation in payrolls growth in April with 180k for its softest since Dec’20, with less clear-cut potential impacts from weather and seasonal adjustment this month.

- JOLTS data saw a second month of lower-than-expected job openings but ADP employment was almost twice as strong as expected in April at +296k and has rarely overshoot payrolls over the past year.

- Aside from the strength and breadth of payrolls, we watch the usual details including the u/e rate (survey hints sizeable hawkish skew) and AHE growth (smaller hawkish skew).

- We see a bias towards a greater market reaction in the event of softer details, with a potential further pulling forward of cut pricing. However, coming straight after the latest FOMC decision, a strong report could start lining up expectations of eking out another hike in June if next week’s CPI also comes in hotter.

CANADA

BOC: Bank of Canada Governor Tiff Macklem says he would only consider adjusting the path of interest rates in response to persistent market tightening and highlighted there are other tools that could be used first, while emphasizing the main focus remains a potential rate hike if inflation gets stuck well above the 2% target.

- Macklem says his country is seeing little spillover from the recent collapse of U.S. lenders, while there is a longer list of inflation risks including rapid wage gains, some elevated price expectations and companies aggressively boosting prices. The remarks are still the most significant to date on how bank failures abroad might contribute to the major downside risk of a serious global recession.

- "We have separate mandates and separate tools for price stability and financial stability. So we can work to achieve both at the same time," Macklem told the Toronto Board of Trade Thursday, remarks that will be followed by audience discussion and a press conference. "If financial stress were to lead to more tightening than expected and if this were to persist, we would need to take this into consideration as we set the policy rate to achieve our inflation target." For more see MNI Policy main wire at 1251ET.

EUROPE

ECB: The European Central Bank raised key interest rates by 25bp on Thursday and signalled more hikes to come in order to boost rates to "sufficiently restrictive" levels to ensure a timely return to its 2% inflation target.

- After its meeting, the ECB also announced its intention to end reinvestments from the asset purchase programme (APP) “as of July,” while assessing regularly the tightening effects of repayments of its its targeted longer-term refinancing operations (TLTROs).

- Underlying price pressures remain strong despite a decline in headline inflation over recent months, the Governing Council concluded, with president Christine Lagarde insisting that the ECB still has ground to cover despite slowing the pace of rate hikes. A line about raising rates to "sufficiently restrictive" levels was added to the statement. (See MNI SOURCES: ECB To Hold Rates At Peak Into 2024). For more see MNI Policy main wire at 1056ET.

US TSYS: Regional Banks Wagged Treasuries, NFP Data Friday, Fed Exits Blackout

US rate markets had another whippy session, finishing higher Thursday, but off midday highs as regional bank concerns had a larger than normal effect on rates in the lead-up to Friday's April employment data (+180k est).

- Short to intermediate Treasury futures saw renewed support after the ECB hiked 25bp to 3.25%, setting the stage for steeper curves as Bonds lagged much of the day.

- Still well bid in early trade, Treasury futures marked session lows after higher than expected Unit Labor Costs (+6.3% vs. +5.5% est, near in-line weekly claims (242k vs. 240k est.

- Short to intermediate Treasury futures see-sawed higher from that point on apparently due to strong risk-off buying on regional bank concerns: PacWest Bank fell more than 60% after it confirmed it was in talks with potential investors early Thursday.

- By midmorning, shares of Western Alliance Bank sold off more than 50% after a FT wrote an article saying the bank was "exploring strategic options including a potential sale of all or part of its business". Western Alliance categorically denied the article and shares bounced but remained under pressure in the second half.

- Incidentally, Reuters exclusive reported "U.S. officials at the federal and state level are assessing the possibility of "market manipulation" behind big moves in banking share prices in recent days, a source familiar with the matter".

OVERNIGHT DATA

- US 1Q Unit Labor Costs +6.3%; Consensus +5.5%

- US 1Q Non-Farm Productivity -2.7%; Consensus -1.9%

- US JOBLESS CLAIMS +13K TO 242K IN APR 29 WK

- US PREV JOBLESS CLAIMS REVISED TO 229K IN APR 22 WK

- US CONTINUING CLAIMS -0.038M to 1.805M IN APR 22 WK

- US MAR TRADE GAP -$64.2B VS FEB -$70.6B

- CANADIAN MAR TRADE BALANCE CAD +1.0 BILLION

- CANADA MAR EXPORTS CAD 63.6 BLN, IMPORTS CAD 62.6 BLN

- CANADA REVISED FEB MERCHANDISE TRADE BALANCE CAD -0.5 BLN

- ECB HIKES KEY DEPOSIT RATE BY 25 BPS TO 3.25%

- ECB UPS REFI RATE, MLF BY 25 BPS TO 3.75% AND 4.0% RESPECTIVE

- ECB TO LIKELY DISCONTINUE APP REINVS AS OF JULY 2023

MARKETS SNAPSHOT

Key late session market levels:

- DJIA down 276.41 points (-0.83%) at 33134.25

- S&P E-Mini Future down 24.75 points (-0.6%) at 4082.75

- Nasdaq down 36.8 points (-0.3%) at 11987.21

- US 10-Yr yield is up 2.4 bps at 3.3599%

- US Jun 10-Yr futures are up 17.5/32 at 116-14.5

- EURUSD down 0.0044 (-0.4%) at 1.1018

- USDJPY down 0.53 (-0.39%) at 134.18

- WTI Crude Oil (front-month) down $0.04 (-0.06%) at $68.56

- Gold is up $9.45 (0.46%) at $2048.54

- EuroStoxx 50 down 23.15 points (-0.54%) at 4287.03

- FTSE 100 down 85.73 points (-1.1%) at 7702.64

- German DAX down 80.82 points (-0.51%) at 15734.24

- French CAC 40 down 63.06 points (-0.85%) at 7340.77

US TREASURY FUTURES CLOSE

- 3M10Y +2.765, -187.772 (L: -199.584 / H: -183.136)

- 2Y10Y +8.186, -38.944 (L: -50.959 / H: -36.04)

- 2Y30Y +10.141, -2.341 (L: -18.308 / H: 3.583)

- 5Y30Y +5.435, 43.5 (L: 33.849 / H: 48.81)

- Current futures levels:

- Jun 2-Yr futures up 11.75/32 at 103-22 (L: 103-13.25 / H: 103-28)

- Jun 5-Yr futures up 18.75/32 at 110-29.5 (L: 110-15.5 / H: 111-11.25)

- Jun 10-Yr futures up 18/32 at 116-15 (L: 115-31 / H: 117-00)

- Jun 30-Yr futures up 3/32 at 131-31 (L: 131-14 / H: 133-00)

- Jun Ultra futures down 10/32 at 140-23 (L: 140-07 / H: 142-18)

(M3) Bullish Engulfing Candle Remains In Play

- RES 4: 117-29+ High Aug 26 2022 (cont)

- RES 3: 117-01+ High Mar 24 and bull trigger

- RES 2: 116-30 High Apr 5 / 6

- RES 1: 116-25+ Intraday high

- PRICE: 116-09+ @ 11:20 BST May 4

- SUP 1: 115-17+/03+ Low May 3 / 20-day EMA

- SUP 2: 114-10 Low May 1

- SUP 3: 113-30+ Low Apr 19 and key short-term support

- SUP 4: 113-23 50.0% retracement of the Mar 3 - 24 bull run

Treasury futures have continued to appreciate and despite today’s pullback from the intraday high, the outlook remains bullish. The focus is on 116-30 next, the Apr 5 / 6 high. Tuesday’s price pattern is a bullish engulfing candle and this also reinforces current conditions, highlighting bullish sentiment and signalling scope for a test of 117-01+, the Mar 24 high and bull trigger. Initial firm support is at 115-03+, the 20-day EMA.

SOFR FUTURES CLOSE

- Jun 23 +0.095 at 95.030

- Sep 23 +0.215 at 95.460

- Dec 23 +0.260 at 95.950

- Mar 24 +0.280 at 96.505

- Red Pack (Jun 24-Mar 25) +0.135 to +0.255

- Green Pack (Jun 25-Mar 26) +0.075 to +0.105

- Blue Pack (Jun 26-Mar 27) +0.040 to +0.070

- Gold Pack (Jun 27-Mar 28) +0.005 to +0.030

SHORT TERM RATES

SOFR Benchmark Settlements:

- 1M +0.00303 to 5.04345 (+.02475/wk)

- 3M +0.01323 to 5.07270 (-.00862/wk)

- 6M +0.00149 to 5.02843 (-.05114/wk)

- 12M -0.03346 to 4.71816 (-.09092/wk)

- O/N +0.24785 to 5.05871%

- 1M +0.01714 to 5.09871%

- 3M -0.00258 to 5.32371% */**

- 6M -0.00343 to 5.39100%

- 12M -0.03943 to 5.26014%

- * Record Low 0.11413% on 9/12/21; ** New 16Y high: 5.33269% on 5/2/23

- Daily Effective Fed Funds Rate: 4.83% volume: $115B

- Daily Overnight Bank Funding Rate: 4.82% volume: $277B

- Secured Overnight Financing Rate (SOFR): 4.81%, $1.544T

- Broad General Collateral Rate (BGCR): 4.79%, $581B

- Tri-Party General Collateral Rate (TGCR): 4.79%, $567B

- (rate, volume levels reflect prior session)

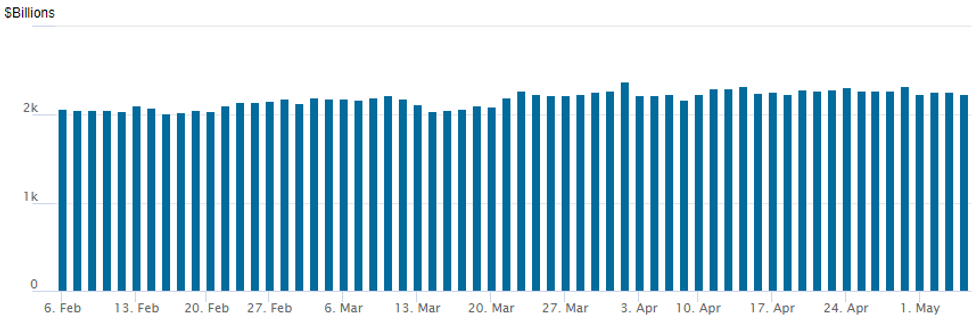

FED Reverse Repo Operation

NY Federal Reserve/MNI

NY Fed reverse repo usage slips back to $2,242.399B w/ 101 counterparties, compares to prior $2,258.222B. Compares to high usage for 2023: $2,375.171B on Friday March 31, 2023; all-time record high of $2,553.716B reached December 30, 2022.

PIPELINE: Corporate Bond Issuance Scarce Ahead NFP

Date $MM Issuer (Priced *, Launch #)

05/03-04 No new US$ debt issuance Wednesday-Thursday,

EGBs-GILTS CASH CLOSE: Bunds Soar As ECB Takes Back Seat To US Bank Woes

- The ECB decision received a mixed reception. Bunds jumped with the 25bp hike vs some lingering expectations of 50bp, and a lack of firm commitment to further tightening in the statement.

- More hawkish was Lagarde's "we are not pausing" and emphasis on requiring multiple future "decisions" to get to sufficiently restrictive territory; the announced end of APP reinvestments starting in July; and a lack of TLTRO bridging loans announced. Periphery spreads closed the day wider.

- Ultimately though US banking concerns and related equity volatility had a much bigger impact, with Treasuries pulling Bunds and Gilts to session highs in a strong risk-off move.

- Hike expectations faded, with ECB terminal dropping by 12bp and BoE 11bp - helping to drive short-end cash curve outperformance.

- Focus early Friday will be on ECB speakers (Simkus and Elderson scheduled), with the US jobs report taking centre stage later.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is down 16.2bps at 2.479%, 5-Yr is down 12.3bps at 2.122%, 10-Yr is down 5.7bps at 2.19%, and 30-Yr is down 0.5bps at 2.366%.

- UK: The 2-Yr yield is down 9bps at 3.678%, 5-Yr is down 8.7bps at 3.482%, 10-Yr is down 4.3bps at 3.653%, and 30-Yr is down 2.6bps at 4.069%.

- Italian BTP spread up 6.1bps at 193.2bps / Spanish up 3bps at 109.8bps

FOREX: EURJPY Slumps Post ECB, NZD Outperforms

- Following the FOMC decision and amid the ongoing concerns for the US banking sector, the Japanese Yen has continued to benefit and is among the best performers in G10 on Thursday. With some residual pricing being pulled out for ECB hiking expectations following the ECB decision, the Euro has underperformed on the day.

- Despite sitting 50 points off session lows, EURJPY remains 0.9% lower as we approach the APAC crossover. The pair continues to retrace the post BOJ bounce from last Friday in what is considered to be a correction for now. Overall, the trend condition remains bullish following recent gains. Price action has seen pierce initial support at 147.50, the 20-day exponential moving average. Below here, key short-term support has been defined at 146.29, the Apr 25 low, where a break is required to signal a short-term reversal.

- In similar vein, USDJPY remained under pressure on Thursday, extending the pullback from Tuesday’s high of 137.77 high to over 400 pips. Today’s 133.50 low fell just shy of last Friday’s, BOJ day, low at 133.38. A clear breach of this support zone would undermine the recent bullish theme and signal scope for a deeper pullback.

- NZD was a standout today, leading the G10 advance. MNI reported last month the RBNZ’s focus would shift to employment figures, which would shape its May 24 decision. Tuesday’s robust data has underpinned NZD since and price action may have been exacerbated by the substantial move lower for AUDNZD to fresh one-month lows below 1.0650 in recent sessions.

- With the key driver for currency markets remaining the downward pressure on front-end US yields and the accumulation of Fed rate cut pricing later this year, emphasis will be on the latest US jobs data before the weekend close. Bloomberg consensus looks for further moderation in payrolls growth in April with the +182k estimate its softest since Dec’20, with less clear-cut potential impacts from weather and seasonal adjustment this month.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 05/05/2023 | 0145/0945 | ** |  | CN | IHS Markit Final China Services PMI |

| 05/05/2023 | 0545/0745 | ** |  | CH | Unemployment |

| 05/05/2023 | 0600/0800 | ** |  | DE | Manufacturing Orders |

| 05/05/2023 | 0630/0830 | *** | | CH | CPI |

| 05/05/2023 | 0645/0845 | * |  | FR | Industrial Production |

| 05/05/2023 | 0700/0900 | ** |  | ES | Industrial Production |

| 05/05/2023 | 0730/0930 | ** |  | EU | IHS Markit Final Eurozone Construction PMI |

| 05/05/2023 | 0800/1000 | * |  | IT | Retail Sales |

| 05/05/2023 | 0800/1000 | | EU | ECB Elderson Speech at European University Institute | |

| 05/05/2023 | 0830/0930 | ** |  | UK | IHS Markit/CIPS Construction PMI |

| 05/05/2023 | 0900/1100 | ** | | EU | Retail Sales |

| 05/05/2023 | 1230/0830 | *** |  | CA | Labour Force Survey |

| 05/05/2023 | 1230/0830 | *** |  | US | Employment Report |

| 05/05/2023 | 1645/1245 | | US | Minneapolis Fed's Neel Kashkari | |

| 05/05/2023 | 1700/1300 | | US | St. Louis Fed's James Bullard | |

| 05/05/2023 | 1700/1300 | | US | Fed Governor Lisa Cook | |

| 05/05/2023 | 1900/1500 | * | | US | Consumer Credit |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.