Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

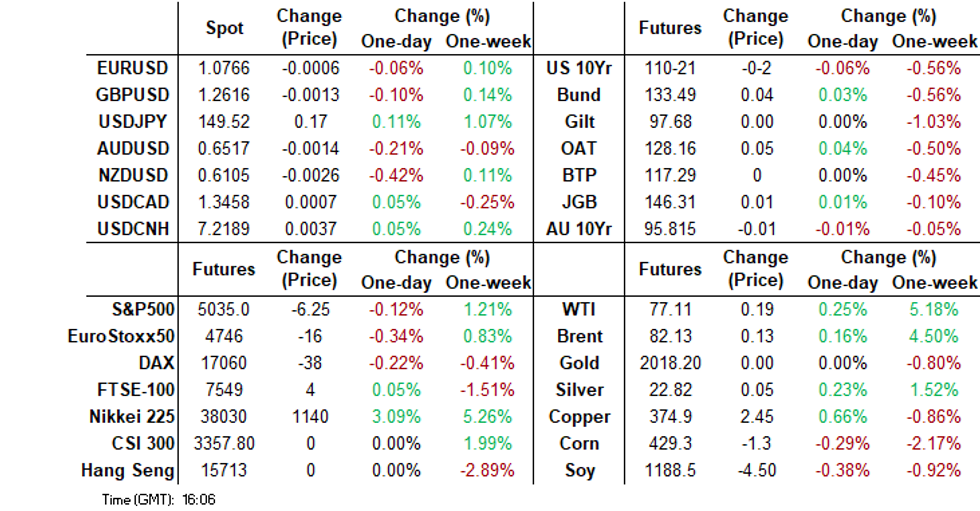

- NZD underperformed during APAC trading today after NZ inflation expectations eased further. Aussie also underperformed but not as much as kiwi. Other G10 currencies are minimally lower against the greenback.

- Asian equities are mostly higher today, Japan leads the way while the BBG Asia Index is 1.63% higher, Tech and Semi-Conductor names outperforming while Bitcoin trades above $50,000 for the first time in 2 years.

- Treasuries are trading in a very small range during the Asia session, volumes have remained low, ahead of US CPI later today.

- Looking ahead the focus today is on the US CPI (see MNI US CPI Preview) which is forecast to moderate to 0.5pp to 2.9%. There is also US real earnings for January and UK employment/wages are released (see MNI UK Data Preview). The ECB’s Buch and Tuominen make appearances.

MARKETS

US TSYS: Treasuries Futures Trend Lower, US CPI Later

TYH4 is currently trading at 110-20, - 03 from New York closing levels.

Treasuries are trading in a very small range during the Asia session, volumes have remained low, ahead of US CPI later today.

- Treasuries futures have traded rangebound today, hitting a low of 110-19+ and a high of 110-23+, and currently trading at 110-20, volatility is expected to remain low heading into the US session.

- Taking a look at the technical levels ahead of US CPI later today - Mar'24 10Y future levels to watch on the downside are 110-16 Dec 13 & Feb 9 lows, a break of 109-31+ the Dec 11 lows, would opens a bigger move down to 109-17, 50.0% of the Oct 19 - Dec 27 bull phase. To the upside a break above 111-09 the 20-day EMA, opens up a move to the Feb 1 highs of 113-06+, which could then put in play the 113-12 the Dec 12 high and bull trigger.

- Cash yields have done little today, the curve is unchanged to 0.3bps wider. The 10yr sits at 4.181% challenging last week's highs, but has yet to make any material test on the key 4.20%, a break above 4.20% post CPI could open up a move to the Dec 12 highs of 4.28%.

- MNI US CPI Preview: Used Cars Drag Seen Clashing With Firmer Non-Housing Services ( https://roar-assets-auto.rbl.ms/files/59940/USCPIPrevFeb2024.pdf )

JGBS: Futures Holding An Uptick Ahead Of US CPI Data, Narrow Ranges

JGB futures are holding a small gain, +6 compared to settlement levels on Friday, after trading in a relatively narrow range in the Tokyo afternoon session. The local market was closed yesterday for the observance of the National Foundation Day holiday.

- There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined PPI data.

- Cash US tsy yields are dealing little changed across benchmarks in today’s Asia-Pac session, with news flow light, ahead of US CPI data out later today.

- January’s US CPI report is forecast to show the first reading below 3% for annual inflation since March 2021, increasing optimism that the Federal Reserve will be able to start loosening monetary policy this year. See MNI US CPI Preview: Used Cars Drag Seen Clashing With Firmer Non-Housing Services (link)

- Cash JGBs are little changed, with yield movements from +0.8bp (2-year) to -0.3bp (20-year). The benchmark 10-year yield is 0.2bp lower at 0.724% versus the Nov-Dec rally low of 0.555%.

- Swaps are slightly richer out to the 20-year and slightly cheaper beyond. Swap spreads are mixed.

AUSSIE BONDS: Subdued Session, Narrow Ranges, Awaiting US CPI Data

ACGBs (YM -1.0 & XM -1.0) are holding slightly cheaper after dealing in relatively narrow ranges in today’s Sydney session. There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined Consumer and Business Confidence data.

- Cash US tsy yields are dealing little changed across benchmarks in today’s Asia-Pac session, with news flow light, ahead of US CPI data out later today.

- January’s US CPI report is forecast to show the first reading below 3% for annual inflation since March 2021, increasing optimism that the Federal Reserve will be able to start loosening monetary policy this year. See MNI US CPI Preview: Used Cars Drag Seen Clashing With Firmer Non-Housing Services (link)

- Cash ACGBs are 1bp cheaper, with the AU-US 10-year yield differential 1bp wider at -1bp.

- Swap rates are 1bp higher.

- The bills strip is slightly cheaper, with pricing +1 to -2.

- RBA-dated OIS pricing is 2bps firmer for meetings beyond September. A cumulative 36bps of easing is priced by year-end.

- Tomorrow, the local calendar is empty, apart from the AOFM’s planned A$800mn sale of the 1% December 2030 bond.

RBA: Little Changed, RBA Kohler: Some Time Before Inflation In Desired Range

ACGBs (YM -1.0 & XM flat) are slightly weaker after US tsys finished little changed on Monday. It was a subdued start to the week ahead of the much-awaited CPI report later today. Lunar New Year Holidays in Asia and European Carnival celebrations lightened trading volumes too.

- US Inflation expectations in January remained unchanged at the short- and longer-term horizons. They declined slightly at the medium-term horizon, according to the NY Fed's survey of consumers. Meanwhile, consumers were more optimistic about their financial situation.

- US equity markets edged higher, extending the record-breaking run.

- (BBG) Inflation in Australia is in retreat, but it will take some time before it returns to the desired target range and the risks around those expectations remain substantial, the Reserve Bank of Australia's Head of Economic Analysis Marion Kohler said. (See link)

- Cash ACGBs are 1bp cheaper, with the AU-US 10-year yield differential unchanged at -1bp.

- Swap rates are 1bp higher.

- The bills strip has slightly bear-steepened, with pricing flat to -2.

- RBA-dated OIS pricing is 1-2bp firmer for meetings beyond August. A cumulative 37bps of easing is priced by year-end.

- Today, the local calendar sees Westpac Consumer and NAB Business Confidence.

AUSTRALIA DATA: NAB Survey Points To Slowing Growth But Prices/Costs Sticky

The January NAB business survey showed a further easing in conditions to 6 from an upwardly-revised 8. This has now moved just below the series average, the first time in two years. Confidence remains around breakeven at +1 up from 0, below the historical average where it has been since Q3 2022. The data is in line with the RBA’s subdued growth expectations for H1 2024 but while the price/cost pressures are off their peaks they have stalled.

- NAB notes that cost and price pressures “remain solid” but it expects them to ease over the early part of the year, as inflation lags growth. The 3-month increase in labour costs held at 2% but purchase costs rose 0.1pp to 1.8% and demand was strong enough for higher costs to be partially passed onto customers with the price of final products rising 1.2% up from 0.9% in December but in line with November’s increase.

Source: MNI - Market News/Refinitiv

- The drop in conditions was driven by all the components with trading down 3 points, profitability -1 point and employment -2 points. Labour demand is still a couple of points above the series average but is pointing to a further slowdown in employment growth. Exports deteriorated as did capex.

- The forward looking components are still weak despite a 1 point rise in orders to -1 but retail is at -19.

Source: MNI - Market News/Refinitiv

AUSTRALIA DATA: Easing Price Pressures & On Hold RBA Make Consumers Feel Better

Westpac consumer confidence jumped 6.2% to 86.0 in February to its highest since June 2022, the month following the first rate hike this cycle. Sentiment was boosted by lower-than-expected Q4 inflation reported at the end of January and the RBA being on hold again at its February meeting. Households remain depressed but are gradually feeling more positive following the trough a year ago.

- Despite the RBA keeping its options open for another hike, those expecting a rate hike in the next year fell 10pp to 42%. The figure was 61% in December. Declining tightening expectations are helping confidence to recover.

- The time to buy index also jumped 11.3% in February, which is good news for retailers.

- Family finances and the economic outlook both improved. And households continue to expect house prices to rise with the index up 2.1% m/m to a new cycle high.

- The survey included the split by political affiliation and it showed a very divided view of the economy with Liberal/National supporters on 77.6 but Labor voters showing more optimists than pessimists on 103.8.

NZGBS: Closed Little Changed But Near Session Bests After Infl. Expn. Data

NZGBs closed at or near the session’s best levels, with benchmark yields flat to 1bp lower, after the RBNZ’s measures of business inflation expectations eased in Q1. The 2-year ahead is now at the mid-point of the target band at 2.5% down from 2.8% in Q4 and the 1-year ahead is close to the top of the band at 3.2% down from 3.6%, but both are above the RBNZ’s CPI forecasts.

- The RBNZ also monitors household inflation expectations which are released on February 22. The RBNZ Policy Decision is on 28 February.

- Cash US tsy yields are dealing little changed across benchmarks in today’s Asia-Pac session, with news flow light.

- The swap curve has twist-steepened, with rates 5bps lower to 4bps higher.

- RBNZ dated OIS pricing is 3-6bps softer across meetings today. A cumulative easing of 50bps is priced for year-end from a peak of 5.62%. This compares to 100bps of easing off 5.53% at the end of January.

- Tomorrow, the local calendar sees REINZ House Sales, Card Spending and Food Prices data.

NZ: RBNZ Dated OIS Continue To Pare Friday’s Firming After Infl. Expectations Data

The RBNZ’s measures of business inflation expectations eased in Q1. The 2-year ahead is now at the mid-point of the target band at 2.5% down from 2.8% in Q4 and the 1-year ahead close to the top of the band at 3.2% down from 3.6%, but both are above the RBNZ’s CPI forecasts.

- The RBNZ also monitors household inflation expectations which are released on February 22. The RBNZ Policy Decision is on 28 February.

- RBNZ dated OIS is 1-3bps softer across meetings today.

- A cumulative easing of 50bps is priced for year-end from a peak of 5.66% . This compares to 100bps of easing off 5.53% at the end of January.

Figure 1: RBNZ Dated OIS Pricing (%)

Source: MNI – Market News / Bloomberg

NEW ZEALAND: Inflation Expectations Moderate To Mid-Target Band

The RBNZ’s measures of business inflation expectations eased in Q1. The 2-year ahead is now at the mid-point of the target band at 2.5% down from 2.8% in Q4 and the 1-year ahead close to the top of the band at 3.2% down from 3.6%, but both are above the RBNZ’s CPI forecasts. The RBNZ also monitors household inflation expectations which are released on February 22. Despite the stronger-than-expected labour market data, the continued moderation in inflation expectations and lower-than-expected Q4 CPI make another hike from the RBNZ unlikely this cycle. We believe that it is more likely to keep rates restrictive for longer rather than tighten again. The next meeting is February 28.NZ RBNZ business inflation expectations $

Source: MNI - Market News/RBNZ/Refinitiv

EQUITIES: Asia Equities Mostly Higher Led By Tech Names, Aus & NZ Underperform

Asian equities are mostly higher today, Japan leads the way while the BBG Asia Index is 1.63% higher, Tech and Semi-Conductor names outperforming while Bitcoin trades above $50,000 for the first time in 2 years. Hong Kong and China remain closed for Lunar New Year celebrations.

- In Japan, equity markets are moving closer to all-time highs. Today's surge is attributed to strong performances in tech names, particularly Tokyo Electron, which is by 11.65% higher after boosting its operating income guidance for the year, surpassing analyst estimates, while Japan's Largest non-life insurers have surged after the nation’s Financial Services agency asked them to accelerate their disposal of cross-shareholdings. The weaker yen -0.13% is also contributing to broader market strength. PPI data released earlier showed mixed results, with month-on-month numbers softer than expected at 0.0% versus the estimated 0.1%, while year-on-year figures were slightly stronger at 0.2% compared to the estimated 0.1%. Topix is up by 1.80%, and the Nikkei is trading 2.56% higher.

- In Australia, equity markets are lower today, with the ASX200 at 7607, down 0.10%, as gains in the financial sector have been offset by weakness in the health sector with CSL off another 3%, following yesterday’s 5.10% fall. Challenger exceeded expectations, leading to a 9.00% increase, while the country's largest job board, Seek.com.au missed earnings falling 13.35% at once stage, however, has recovered to trade just 4.50% lower.

- New Zealand equities continue their four-day losing streak, down by 0.15%, following remarks from RBNZ Governor Orr hinting at potential further rate hikes due to persistently high inflation. New Zealand inflation expectations fell to their lowest level in two and a half years with 2yr inflation expectation stands at 2.50%, compared to the previous 2.76% in a sign that the RBNZ may not need to raise interest rates further.

- South Korean equities opened higher, with the Kospi trading 1.40% higher after a day off. Semiconductor names were higher today, as the BBG Asia Pac Semiconductor hit highest levels in two years after Tokyo electrons strong earnings forecast and another rally in Nvidia shares overnight. While expectations for a regulatory push to close the "Korea Discount" are boosting markets and attracting significant inflows, with $580 million heading into SK stocks today.

- Indonesian equities are lower today, anticipating the upcoming presidential election on Wednesday, despite witnessing the highest net buying by global investors on Feb 12th in about two months. The Jakarta Composite currently trades 1.00% lower.

- Elsewhere in SEA, Philippines equities are 0.30% higher ahead of BSP's first policy meeting this year, Malaysian equities are 1.00% higher, while Singapore Equities are 0.60% lower.

OIL: Prices Steady As Markets Wait For US CPI & OPEC Report

Oil prices are little changed ahead of US CPI later and the OPEC monthly report. Brent is up 0.1% and is trading above $82 again at $82.07/bbl. WTI is also 0.1% higher at $77.03/bbl. Both benchmarks have been trading in a very narrow range as the Lunar New Year holiday drives thin trading volumes. The USD is 0.1% higher.

- Conflicts in the Middle East remain in focus with Central Command reporting that a Houthi missile hit the MV Star Iris and that there was minor damage to the vessel. Also Israel attacked Rafah despite the US requesting they abstain. A number of third parties are saying that a deal is getting closer with US President Biden calling for all Israeli hostages to be released and for a 6-week ceasefire.

- In terms of Russia, the EU is looking to impose trade restrictions on Russian firms who support the war effort. It is also examining how the price cap on Russian oil can be enforced more strictly.

- The OPEC report will be watched closely for the demand and supply outlook and how closely members are complying with quotas. The group will decide if production cuts will be extended into Q2. In terms of supply, US inventory data from the API is also out today.

- Later the focus is on the US CPI (see MNI US CPI Preview) which is forecast to moderate to 0.5pp to 2.9%. There is also US real earnings for January and UK employment/wages are released. The ECB’s Buch and Tuominen make appearances.

GOLD: Another Decline Ahead Of Key US CPI Data

Gold is little changed in the Asia-Pac session, after closing 0.2% lower at $2020.05 on Monday.

- Bullion finished off its low of $2012.01 for a quick breach of $2015.0 (Feb 5 low) but stopped short of $2001.9 (Jan 17 low).

- The yellow metal saw losses despite the USD index on blance moving sideways, with TD Securities noting it is “being weighed down by CTA selling activity”.

- US Treasuries were little changed after see-sawing in narrow ranges on Monday ahead of the much-awaited CPI report later today. January’s CPI report is forecast to show the first reading below 3% for annual inflation since March 2021, increasing optimism that the Federal Reserve will be able to start loosening monetary policy this year.

- Lunar New Year Holidays in Asia and European Carnival celebrations lightened trading volumes too.

FOREX: FX Range Trading, Kiwi Underperforms Following Lower Inflation Data

The US dollar is stronger in APAC trading today with the BBDXY index up 0.1%. Kiwi is the underperformer followed by Aussie after NZ inflation expectations eased further. Other G10 currencies are minimally lower against the greenback.

- FX markets are range trading ahead of the US CPI data later but regional equities are generally higher.

- NZDUSD is down 0.5% to 0.6098, close to the intraday low. It was trading around 0.6126 ahead of the RBNZ’s Q1 inflation expectations. The 2-year ahead measure is now at the mid-point of the target band at 2.5% down from 2.8% in Q4 and the 1-year ahead close to the top of the band at 3.2% down from 3.6%. The data make any further RBNZ tightening unlikely.

- AUDUSD is down 0.3% to 0.6514 and has followed today’s USD trends with some further downward impetus from the softer kiwi data. AUDNZD has bounced 0.3% to 1.0683.

- USDJPY is little changed rising 0.1% to 149.56 but yen has gained against the Aussie falling to 97.42 and EURJPY is slightly higher at 160.96.

- European currencies are all down around 0.1% against the greenback.

- EM Asia is also little changed against the USD with the USDTHB move of +0.3% the most noteworthy.

- Later the focus is on the US CPI (see MNI US CPI Preview) which is forecast to moderate to 0.5pp to 2.9%. There is also US real earnings for January and UK employment/wages are released. The ECB’s Buch and Tuominen make appearances.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 13/02/2024 | 0700/0700 | *** |  | UK | Labour Market Survey |

| 13/02/2024 | 0730/0830 | *** |  | CH | CPI |

| 13/02/2024 | 1000/1100 | *** |  | DE | ZEW Current Expectations Index |

| 13/02/2024 | 1000/1100 | *** | | DE | ZEW Current Conditions Index |

| 13/02/2024 | 1000/1000 | * | | UK | Index Linked Gilt Outright Auction Result |

| 13/02/2024 | 1100/0600 | ** |  | US | NFIB Small Business Optimism Index |

| 13/02/2024 | 1330/0830 | *** | | US | CPI |

| 13/02/2024 | 1355/0855 | ** | | US | Redbook Retail Sales Index |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.