Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- As US CPI comes into view, the tone in Tuesday Asia Pac markets has been USD weakness and lower US Tsy yields. Cash tsys are 1-3bps richer across benchmarks after reversing early Asia-Pac session weakness. The BBDXY is down nearly 0.20%, with NZD, JPY and AUD outperforming. Asian currencies have generally lagged. Regional equity trends have been mixed.

- Elsewhere, one of our EU recession probability estimates for 6 months ahead is signaling that there is the risk of a recession from around the turn of the year until at least Q2, see below for more details.

- Later US CPI data for November print and are expected to show a slight easing in headline to 3.1% and core steady at 4% (see MNI US CPI Preview). There are also real earnings and the November budget statement. UK labour and wages data are on the schedule.

MARKETS

US TSYS: Slightly Richer Ahead Of Tonight's US CPI Data, Post-JGB Auction Spillover

TYH4 is currently trading at 110-15, +0-04+ from NY closing levels.

- Cash tsys are 1-3bps richer across benchmarks after reversing early Asia-Pac session weakness.

- There has been no meaningful newsflow so far in the session.

- Asia-Pac session strength appears tied to spillover from the post-5Y auction rally in JGBs. In contrast to the recent 2-, 10-, and 30-year supply, which experienced challenges in market digestion, today’s outcome stands out.

- Nevertheless, investors are likely to remain close to the sidelines in anticipation of the US inflation data scheduled for later today and the Federal Reserve's decision on Wednesday.

EUROPE: Non-Negligible Recession Risk

Q3 euro area GDP fell 0.1% q/q to be flat on the year as the economy has stagnated for the last year. There hasn’t been two consecutive quarters of falling growth yet and in the euro area a recession is dated by the EABCN business cycle dating committee. While it is likely growth will continue to stagnate over the coming quarters, there is a non-negligible risk of recession which is likely to be monitored closely by the ECB especially as inflation approaches the 2% target.

- One of our recession probability estimates for 6 months ahead is signalling that there is the risk of a recession from around the turn of the year until at least Q2. The probability from 1998 has been above the 50% signal since July and was as high as 71% in September. It moderated to 55% in November, as real oil prices and economic sentiment indicator outweighed the yield curve and real equity prices.

- The calculated recession probability from 1985 has remained very low all year at under 20%.

- It is worth noting that econometric calculations are only estimates and not predictions.

Source: MNI - Market News/Refinitiv

JGBS: Richer After 5Y Supply, US CPI Data Tonight

JGB futures are sharply richer, +22 compared to settlement levels, after today’s 5-year supply sees mixed results. The auction's low price beat dealer expectations but the cover ratio declined relative to the previous month's auction. The tail also lengthened slightly.

- Nonetheless, today’s result stood out relative to recent 2-, 10-, and 30-year supply, which experienced greater challenges in market digestion. However, it's important to note that the result still fell short of presenting a convincingly robust outcome.

- There hasn’t been much in the way of domestic data drivers to flag, outside of the previously outlined Nov PPI data, which came close to expectations. The print is unlikely to shift BOJ thinking ahead of next week's policy meeting.

- US tsys are 1-3bps richer in the Asia-Pac session ahead of tonight's US CPI data.

- The cash JGB curve has twist-flattened, pivoting at the 2s, with yields 1.3bps higher to 2.4bps lower. The benchmark 10-year yield is 1.6bps lower at 0.749% versus the morning high of 0.778%.

- The swap curve is richer, with swap spreads mixed.

- Tomorrow, the local calendar sees the Tankan Mfg and Non-Mfg Indices, along with BOJ Rinban operations covering 1-3-year, 5-10-year, and 25-year+ JGBs.

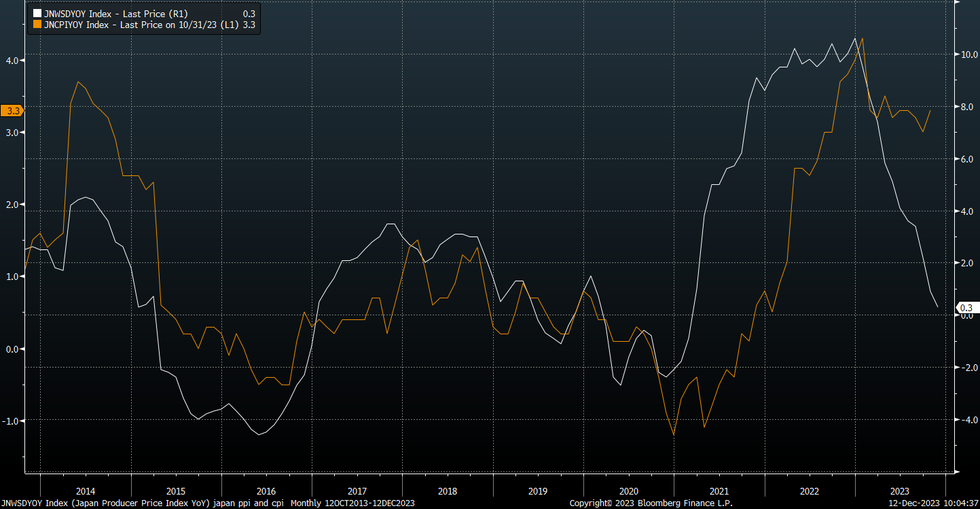

JAPAN DATA: PPI Close To Expectations, Y/Y Momentum Continues To Ease

Japan's Nov PPI was close to expectations, rising 0.2% m/m (in line with the projection), while the prior was -0.3%. The y/y outcome rose 0.3%, slightly above the 0.1% forecast, while the prior was 0.9%.

- The evolution of the PPI continues to be waning y/y momentum. The chart below plots the headline in y/y terms against Japan's headline CPI.

- Base effects for the PPI will be less favorable as we progress through the first half of 2024.

- In terms of the detail, we saw a decent m/m rise in petroleum, coal (+3.1%) and metals +1.4%. Elsewhere though m/m pressures were either close to flat or negative.

- The print is unlikely to shift BOJ thinking ahead of next week's policy meeting.

Fig 1: Japan PPI Y/Y & CPI Y/Y

Source: MNI - Market News/Bloomberg

AUSSIE BONDS: Slightly Richer Ahead Of US CPI Data, JGB Spillover

In futures roll-impacted trading, ACGBs (YM +1.4 & XM +1.8) are slightly stronger after dealing in relatively tight ranges in today’s Sydney session. There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined Westpac Consumer Sentiment and NAB Business Confidence data.

- RBA Governor Bullock largely discussed payments at the AusPayNet Summit today. That said, when asked about monetary policy she said that the RBA still believes that it can slow the economy enough to return inflation to target while preserving most of the employment gains.

- Afternoon strength appears tied to spillover from the post-5Y auction rally in JGBs. In contrast to the recent 2-, 10-, and 30-year supply, which experienced challenges in market digestion, today’s outcome stands out.

- US tsys are 1-3bps richer in the Asia-Pac session.

- Cash ACGBs are 2bps richer, with the AU-US 10-year yield differential 2bps wider at +11bps.

- Swap rates are 3bp lower.

- The bills strip is slightly richer, with pricing flat to +1.

- RBA-dated OIS pricing is little changed.

- Tomorrow, the local calendar sees CBA Household Spending.

- The Mid-Year Economic and Fiscal Outlook (MYEFO) is also scheduled to be published tomorrow with Treasurer Chalmers giving a press conference in the late morning according to Treasury.

AUSTRALIAN DATA: Cost/Price Pressures Rise In November

The NAB business survey showed that cost pressures rose again in November and as a result there was also a pickup in selling prices. While the RBA is likely to be pleased that the survey is showing slowing business activity, which is important to bring demand and supply back into balance, it is likely to be concerned that inflationary pressures remain elevated. All of the NAB price/cost components are running well above series averages.

- In terms of costs, labour costs rose 2.2% over the 3 months to November up from 2% and 1pp above the historical average. Purchase costs rose 2.5% after 1.9%.

- Final product prices rose 1.2% up from 1% and double the average, while retail prices rose 1.9% compared with the 0.7% average. RBA Governor Bullock noted recently that firms still have the pricing power to pass higher costs onto customers and the NAB survey is in line with this.

Source: MNI - Market News/Refinitiv

AUSTRALIA: Fiscal Update Tomorrow, Likely Improved But Debt Servicing Higher

The Mid-Year Economic and Fiscal Outlook (MYEFO) is published tomorrow with Treasurer Chalmers giving a press conference in the late morning according to Treasury. Chalmers has said that it will be a “traditional” update with revised forecasts and report on any new spending that has come up but there won’t be “big, new initiatives”. The MYEFO will continue to work towards avoiding any additional inflationary pressures stemming from fiscal policy so as not to make the RBA’s job harder.

- In May, the government estimated the FY24 deficit at $13.9bn but the budget was $9.1bn better than expected in the financial year to October. Many economists expect the MYEFO to show a predicted surplus for FY24.

- Finance Minister Gallagher has already announced that there will be $9.8bn of additional savings and spending reprioritisations which brings the total since the start of the government’s term to $49.6bn.

- The growing issue for the budget is the interest bill on the debt due to rising rates. It is estimated that it will be an additional $80bn over the decade ahead making it the fastest growing expense pushing the NDIS into second place. According to The Australian the average long-term rate for new borrowing will be revised up 1.3pp to 4.7% from May’s forecast. Gross debt-to-GDP is still expected to be revised down over the forecast horizon.

- Continued robust jobs growth and resilient commodity prices are likely to result in an upward revision to the current financial year revenue estimates.

AUSTRALIAN DATA: Inflation Remains Main Issue For Consumers

Westpac’s consumer sentiment for December rose 2.7% to 82.1, the highest level since April, in a month where the RBA left rates unchanged. It is one point higher than the 2023 average and hasn’t deteriorated over H2 this year in line with data showing stagnating consumption. The level remains depressed though and Westpac reports that 2023 was the second worst year since 1974.

- The RBA’s December pause boosted sentiment with the index rising 5.4% between responses taken before and after the meeting. But 60% of those surveyed after the decision believe that rates will rise again next year, which is down from 73% in November but still elevated.

- Inflation remained the most recalled of news topics with 55% of respondents noticing it. It has been the main issue for two years now and by “a wide margin”. The “budget and taxation” had the second highest recall at 35%, followed by the economy with 32%, employment 29% and rates 23%.

- Consumers were more optimistic on the medium- to long-term outlook for the economy and their own finances. But inflation continues to weigh on buying intentions with the “time to buy a major household item” down 3.8% in December.

- Unemployment expectations fell 1.2% and Westpac observes that it continues to remain around the historical average.

- In terms of housing, “time to buy a dwelling” rose 1.6% but is still very weak. It rose almost 20% post the RBA decision. House price expectations rose 0.7%.

Source: MNI - Market News/Refinitiv

NZGBS: Subdued Session Ahead Of US CPI Data

NZGBs have closed flat to 2bps richer across benchmarks following a relatively uneventful local session.

- There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined Total Spending and Net Migration data.

- Given the potential for significant developments in the upcoming days, local investors have opted to stay on the sidelines during today’s session in anticipation of the US inflation data scheduled for later today and the Federal Reserve's decision on Wednesday. This week also sees ECB and BOE policy meetings before the BOJ policy decision next Tuesday.

- The RBNZ’s annual re-weighting of TWI will come into effect on December 13, with the AUD weight rising to 17.7% from 16.5%. The Yuan weight falls to 22.6% from 25.6%, while the USD weight rises to 14.5% from 13.8%.

- Despite the subdued session, swap rates closed at their best levels, with rates 3-4bps lower.

- RBNZ dated OIS pricing is little changed across meetings, with terminal OCR expectations at 5.56%.

- Tomorrow, the local calendar sees REINZ House Sales (Nov), BoP Current Account Balance (Q3) and Food Prices (Nov).

NEW ZEALAND DATA: Spending Solid But Supported By Record Migration

Electronic card transactions rose 0.8% m/m and 3.3% y/y in November up from 1% y/y, while retail increased by a robust +1.6% but is only up 1.3% y/y. Retail was likely boosted by November’s cyber week sales. Spending is holding up but is signalling further slowing in Q4 to date. It has been supported by the increase in the population and so per person consumption is declining. The RBNZ remains concerned though about the inflationary impact of increased demand from higher migration.

NZ retail spending y/y%

Source: MNI - Market News/Refinitiv

- Core retail spending rose 2.2% m/m with apparel up 5.2%, durables +0.9% and motor vehicles +1.4%. Services fell 0.5% m/m with hospitality spending up 5.1% y/y.

- Net migration was 7810 in October with September revised up by 2500 to 10010. In the year to October, migration has added 130.8k to the population, the highest since the series began in 2001. The new government has stated that it plans to slow net inward migration.

Source: MNI - Market News/Refinitiv

FOREX: USD Slips Ahead Of CPI Print

The dollar sits lower as the US CPI comes into view. The BBDXY off 0.10-0.15% for the session, last near 1242. A slightly softer US Tsy yield backdrop hasn't aided sentiment for the dollar, with NZD, AUD and JPY the top performers against the USD.

- Yen was the early gainer, USD/JPY getting down to 145.54, before stabilizing. The pair last near 145.60/65, +0.35% firmer in yen terms for the session. Lower US yields have helped, but yen strength appeared before such trends emerged, unwinding some gains from Monday's session. On the data front, the PPI continued to slow in y/y terms.

- NZD/USD is outperforming marginally, last near 0.6150 (+0.40%). Earlier data showed a better card spending backdrop, supported by migration flows.

- AUD/USD shrugged off a weaker business sentiment reading from NAB, while consumer sentiment firmed marginally. The pair was last near 0.6590 (+0.35%). Comments from RBA Governor Bullock didn't shed any fresh light on the rate outlook (still very much data dependent).

- Outside of the US CPI print later, note we have the German ZEW out prior, along with UK jobs data.

EQUITIES: Most Major Indices Higher, Mixed Trends in SEA

Major indices in North East Asia are higher, while China headline bourses are flat, although property sub-indices are doing better. Trends are more mixed in South East Asia. US futures sit marginally firmer at this stage, ahead of key US CPI data later. Eminis late near 4680, while Nasdaq futures are outperforming at the margin, last 16469.

- US Tsy yields couldn't sustain early upside, with the back end of the curve around 2bps lower at this stage. This has likely helped equity sentiment at the margin.

- The HSI is up 0.85% at the break, with the tech sub index up +1.65%. China's CSI 300 and Shanghai Composite indices are close to flat at the break, but the break, but property sub indices are notably higher.

- Share buy back announcements are helping the CSI 300, while potentially more fiscal stimulus may be a priority next year as the Central Economic Work Conference meeting is expected to conclude today. This meeting will also focus on 2024 economic targets.

- The Kospi and Taiex are marginally higher, despite a strong lead from the SOX in Monday US Trade. In Japan, the Topix is close to flat, while the Nikkei 225 is +0.30%.

- In SEA, Thailand stocks continue to underperform, down nearly 0.40. We may see fiscal news outlined by the government later. Other markets are either flat or modestly higher at this stage.

OIL: Oil Prices Climb Higher Ahead Of Key Events, US CPI & EIA Report Coming Up

Oil prices have risen for the last 3 trading days and have trended higher again during today’s APAC session. There are a number of key events for the oil market this week including today’s US CPI, Wednesday’s Fed decision and monthly reports from OPEC (Wed), IEA (Thurs) and EIA (today). The USD index is down 0.1%.

- Brent has traded above $76 for most of today’s session and is up 0.3% to $76.24/bbl, close to the intraday high. WTI is also 0.3% higher at $71.54.

- Prices remain well down in December to date as the market has worried that there will be a widening surplus despite OPEC+ planning cuts worth 2.2mbd in Q1 2024. With the focus on supply, the API US inventory data out later today and the EIA report will be monitored closely. The US has seen strong crude output.

- The market is sceptical that OPEC members will adhere to their new quotas but if they do, analysts believe that prices will find some support.

- Later US CPI data for November print and are expected to show a slight easing in headline to 3.1% and core steady at 4% (see MNI US CPI Preview). There are also real earnings and the November budget statement. UK labour and wages data are on the schedule.

GOLD: Unexpectedly Weak On Monday Ahead Of US CPI Data

Gold is slightly stronger in the Asia-Pac session, after closing 1.1% lower at $1981.95 on Monday. Bullion’s weakness came despite limited USD strength and only a small lift in US Treasury yields. Yields initially moved higher on the back of poor US Treasury auctions yesterday but the sell-off was quickly reversed.

- Monday’s downturn precedes the release of today’s US CPI data and the forthcoming FOMC decision on Wednesday. Investors eagerly await the CPI figures, hoping for insights into whether the recent disinflation trend persists, seeking clues about the Federal Reserve's prospective interest rate trajectory for 2024.

- An earlier low of $1976.05 briefly cleared support at $1978.2 (50-day EMA) to open a key support at $1931.7 (Nov 13 low), according to MNI’s technicals team.

PHILIPPINES DATA: Trade Deficit Wider Than Expected On Export Dip

Philippines Oct trade figures were weaker than expected. Exports were -17.5% y/y, versus -8.2% forecast. This puts us back close to earlier lows around -20%. Imports were -4.4% y/y, close to expectations (-4.9%, prior -14.1%). This left the trade balance wider than forecast at $-4175mn, against a -$3490mn projection (prior -$3582mn).

- Exports were -5.5% m/m, dragged down by electronic exports -11.4% m/m. This sub sector is now down -28.9% in y/y terms. Manufacture exports were down -6.8% m/m, -21.1% y/y.

- On the import side, the main shift from the prior month came through via higher crude oil imports (+20.5%, versus -24.5%m/m prior). This sub sector is still down -5.3% in y/y terms.

- The trade position has largely moved sideways since the middle of the year. We are above 2022 lows though (around -$6000mn).

ASIA FX: USD/Asia Pairs Underperform Broader USD Weakness

USD/Asia pairs have drifted down a touch, although USD/THB has been marked higher as onshore markets return, while USD/IDR is firmer, despite the better risk backdrop. This is underperforming the generally softer USD tone seen against the majors. The BBDXY is off -0.17% ahead of the upcoming US CPI print. PHP shrugged off a wider than expected trade deficit, while MYR hasn't reacted to a cabinet reshuffle. Still to come today is Nov CPI for India, as well as Oct IP.

- USD/CNH has tracked tight ranges overall. The pair sits under 7.1900, which is where we have spent much of the session. We are around 0.1% stronger in CNH terms. The CNY fixing error widened, while onshore equity indices are close to flat at this stage, although property sub-indices are doing better. Focus is on the outcomes of a key economic meeting, which should outline key 2024 economic targets/stimulus plans.

- 1 month USD/KRW has drifted lower, last in the 1313/14 range. Onshore equities are firmer, up +0.50% for the Kospi, but this hasn't seen local FX outperformance. Tomorrow we get Nov trade prices early.

- USD/IDR sits near 15630 in recent dealings, down slightly from session highs at 15648. This is still fresh multi week highs in the pair. We are above all key EMAs, with Nov 13 highs back at 15721. Note on the downside, the 50-day EMA is back near 15560. IDR is underperforming a generally firmer global risk appetite backdrop, particularly in the equity space. Locally 5yr CDS remain very close to recent lows around 75bps. Note later today we have the presidential debate from 7pm local time.

- USD/THB has gaped higher as onshore markets return after yesterday's holiday. The pair was last in the 35.60/50 region, slightly below session highs. We are above all key EMAs and have pushed through the simple 100-day MA (35.535). Note the simple 50-day MA rests higher at 35.90. Baht weakness looks to be stretching beyond what is implied by a slightly firmer USD index backdrop. Likewise, when we look at USD/THB versus US-TH yield differentials. Local equities remain underperforming, with the SET near recent cyclical lows, which continues to imply higher USD/THB levels. We may get fiscal news later today, as PM Srettha chairs a meeting.

- USD/PHP sits slightly lower, last near 55.56. This is down from recent highs (55.665), but comfortably above earlier Dec lows at 55.24. On the data front, we had the Oct trade deficit print wider than expected, but this didn't impact market sentiment.

- USD/MYR is around 4.6840 in recent dealings, little changed for the session. As expected, PM Anwar announced a cabinet reshuffle. The PM will share the Finance portfolio with Amir Hamzah, who currently heads the Malaysia's largest pension fund (see this BBG link for more details).

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 12/12/2023 | 0700/0800 | ** |  | NO | Norway GDP |

| 12/12/2023 | 0700/0700 | *** |  | UK | Labour Market Survey |

| 12/12/2023 | 1000/1100 | *** |  | DE | ZEW Current Conditions Index |

| 12/12/2023 | 1000/1100 | *** | | DE | ZEW Current Expectations Index |

| 12/12/2023 | 1000/1000 | ** | | UK | Gilt Outright Auction Result |

| 12/12/2023 | 1100/0600 | ** |  | US | NFIB Small Business Optimism Index |

| 12/12/2023 | - | *** |  | CN | Money Supply |

| 12/12/2023 | - | *** | | CN | New Loans |

| 12/12/2023 | - | *** | | CN | Social Financing |

| 12/12/2023 | 1330/0830 | *** | | US | CPI |

| 12/12/2023 | 1355/0855 | ** | | US | Redbook Retail Sales Index |

| 12/12/2023 | 1500/1000 | * | | US | Services Revenues |

| 12/12/2023 | 1630/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 12/12/2023 | 1800/1300 | *** | | US | US Treasury Auction Result for 30 Year Bond |

| 12/12/2023 | 1900/1400 | ** | | US | Treasury Budget |

| 13/12/2023 | 2145/1045 | ** |  | NZ | Current account balance |

| 13/12/2023 | 2350/0850 | *** |  | JP | Tankan |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.