Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

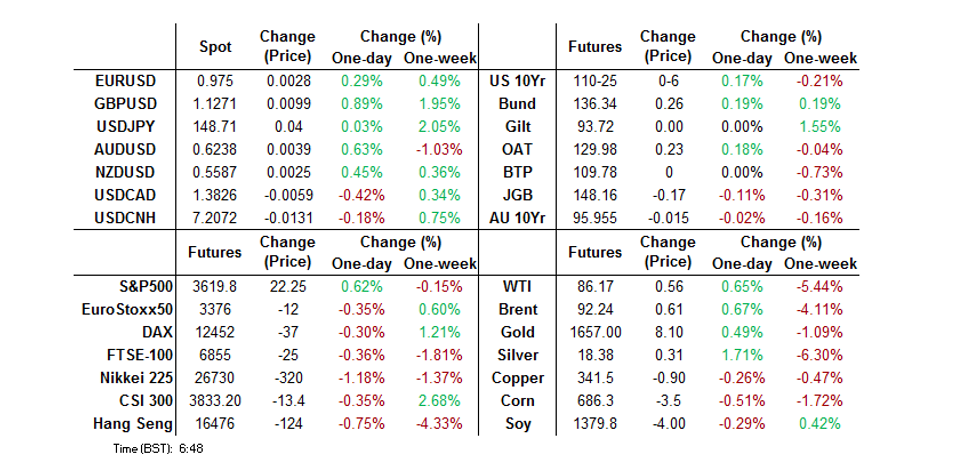

- The GBP appreciated at the start to the week as the new UK Chancellor flagged the potential for further U-turns on the fiscal plans that had roiled UK financial markets. BoE Gov Bailey spoke with Hunt over the weekend, noting that there was a "meeting of minds" on the importance of sustainable fiscal policy.

- U.S. Tsys saw some light richening in Asia hours, while e-minis were bid, also linked to hope re: UK fiscal policy.

- Note that Chinese President Xi's opening address at the CPC Congress provided nothing in the way of curveballs re: major policy areas.

- U.S. Empire State Manufacturing Survey headlines the global data docket today. ECB members dominate the central bank speaker slate, with Lane, de Guindos, de Cos and Nagel set to take the floor. Also note that UK C'llr Hunt will make an address later today, with fiscal U-turns expected.

US TSYS: A Touch Firmer On UK Fiscal Hopes

Tsys are a touch richer on the back of the weekend rhetoric from the new UK C’llr & UK press reports pointing to a more viable/responsible fiscal approach after the “mini” Budget disaster, with the major cash benchmarks printing 2.0-3.5bp firmer, as 5s lead the bid.

- Still, a block sale in TY futures has helped cap the space, while a lack of meaningful headline flow since the re-open has limited wider activity after the initial richening impulse.

- TYZ2 last prints +0-05 at 110-24, 0-01+ off the peak of its 0-07+ Asia range, with volume limited to ~57K lots.

- Outside of the UK news, the weekend saw St. Louis Fed President Bullard fail to rule out the idea of back-to-back 75bp hikes across the two remaining Fed meetings of ’22, although he flagged that ’23 could be a more data-dependent year for the central bank, maybe entailing more two-way risk to rates vs. what we have seen in ’22.

- Chinese President Xi’s opening round of remarks at the CPC congress provided nothing in the way of curveballs re: the major policy areas.

- A thin NY docket, with the Empire m’fing survey headlining, will leave headline flow front and centre as we move through the day, with UK Gilt market gyrations likely to set the tone in European hours (once again).

JGBS: Bear Steepening Extends Through Afternoon Post-Rinban

JGB futures held lower on Monday, looking through a modest uptick in U.S. Tsys linked to UK fiscal matters., last -14, respecting the base of their overnight session range thus far.

- Cash JGBs run flat to 6bp cheaper across the curve, bear steepening. 10s are limited by their proximity to the upper end of the range permitted by the BoJ’s YCC settings and 7s sold off more than surrounding lines on the weakness in futures.

- A steady to slightly higher round of cover ratios in today’s BoJ Rinban operations has added the steepening, particularly given the recent upsizing of the super-long end purchases from the Bank (i.e. more super-long sellers were seen this time out in nominal terms).

- The idea of higher business tax rates was flagged by the ruling LDP Party tax chief over the weekend, but that did little to support the space.

- BoJ Governor Kuroda reiterated his previous musings re: the need for continued monetary easing, while Finance Minister Suzuki and top FX diplomate Kanda reiterated their own recent rhetoric re: FX matters.

- Japanese PM Kishida once again pointed to the need for continued government-BoJ cooperation, which will factor into his choice for Kuroda’s successor.

- 20-Year JGB supply headlines domestic matters on Tuesday.

AUSSIE BONDS: Rebounding From Lows

Aussie bond futures initially showed through their overnight session lows shortly after the Sydney re-open, as the impulse from Friday’s Gilt-driven cheapening, alongside an expected uptick in food price inflation owing to notable floods in food producing areas of Australia and PM Albanese outlining a A$9.6bn round of infrastructure spending, generated fresh pressure.

- That was before some hope surrounding a firmer fiscal footing in the UK provided a bit of a bid for the space, leaving the major cash ACGB benchmarks flat to 2bp cheaper across the curve ahead of the bell, as the 10- to 12-Year zone leads the weakness, while YM is unch. and XM is -2.0.

- A word of caution from Treasurer Chalmers re: the broader economic situation probably aided the rebound at the margin.

- Swaps have lagged the move in bonds, with the early narrowing of EFPs reverting to widening, led by 10s, as the 3-/10-Year EFP box steepens.

- Bills run 1-3bp cheaper across the curve, with RBA dated OIS pointing to a terminal rate of ~4.05%, little changed on the day.

- Tomorrow’s domestic docket is headlined by the minutes covering the latest RBA decision and an appearance RBA Deputy Governor Bullock, with her address on in front of the AFIA annual conference to be on the topic of “Policymaking at the Reserve Bank.”

AUSTRALIA DATA: Week To Be Dominated By RBA And Labour Market Data

The focus of the week in Australia is likely to be RBA commentary and the September labour force report.

- On Tuesday, RBA Deputy Governor Bullock is scheduled to speak at the Australian Finance Industry Association annual conference at 11.05AEDT. This will be followed by the minutes from the October 4 RBA meeting. Given the surprise 25bp move, the minutes could be more on the dovish side and likely to be studied for more detail on the Board’s reasoning.

- The MI/Westpac leading indicator for September is published on Wednesday. August marked the third consecutive fall and brought the 6-month annualised growth rate into negative territory for the first time since January. Further monetary tightening and the deteriorating global outlook are likely to weigh on the index again this month.

- September employment data is released on Thursday. Another moderate gain of 25k is expected after 33.5k last month, which should keep the unemployment rate steady at 3.5%. A result around this mark is unlikely to change the RBA’s 25bp per meeting stance.

Source: MNI - Market News, ABS

NZGBS: Swap Spread Payside Activity Seemingly Aids Cheapening

NZGBS cheapened on Monday, with the major benchmarks seeing yields move 4-5bp higher.

- This came after Friday’s weakness in UK Gilts & U.S. Tsys, with a relief bounce in the latter on the back of weekend news flow out of the UK which triggered hope re: the adoption of a more realistic fiscal footing in London doing little for NZGBs.

- Payside swap flows probably helped this dynamic, with swap spreads wider on the day, as outright 2-Year swaps registered fresh cycle highs above the 5.00% mark.

- Q3 CPI data headlines Tuesday’s docket, with moderations in headline readings expected (BBG median points to +6.6% Y/Y & +1.5% Q/Q vs. respective priors of +7.3% & +1.7%), although non-tradable inflation is expected to accelerate (BBG median of +1.8% Q/Q vs. the +1.4% seen in Q3). Such a dynamic would justify continued tightening from the RBNZ with domestic inflationary pressures remaining evident, while headline inflation is set to remain comfortably above the RBNZ’s 1-3% target band.

- RBNZ dated OIS shows terminal OCR pricing just above 5.00%.

- Non-resident bond holding data for Sep is also due.

- Elsewhere, any trans-Tasman impulse from the minutes covering the most recent RBA monetary policy decision and an address from RBA Deputy Governor Bullock will be eyed.

NEW ZEALAND: Q3 CPI Preview: Underlying Inflation To Keep RBNZ Hawkish

NZ CPI for Q3 is published on Tuesday and is expected to rise 1.5%q/q (down from 1.7% in Q2), according to Bloomberg, but the range of forecasts is wide from 1.3% to 2.0%. The median would leave headline inflation at 6.6%y/y down from the Q2 32-year high of 7.3%, and past its peak.

- The expected easing in headline inflation is unlikely to be a reason to expect a more dovish RBNZ, as underlying inflation pressures probably didn’t improve in Q3.

- The domestically-driven non-tradeable CPI is expected to have outpaced the tradeable component in Q3, as softer energy and food prices weigh on the latter. Non-tradeable CPI is expected to rise 1.8%q/q (Q2 1.4%)and tradeables +1.2% (Q2 1.9%).

- If economists are correct, this would show that domestic inflation pressures rose during the quarter leaving the annual non-tradeable inflation rate steady at around 6.3%, thus justifying the RBNZ’s continued hawkishness.

Source: MNI - Market News, Refinitiv

FOREX: Potential For More Prudent Fiscal Policy Supports GBP, Risk-On Flows Take Hold

The GBP appreciated at the start to the week after PM Truss sacked Chancellor Kwarteng and appointed Jeremy Hunt to succeed him. The new Chancellor flagged potential for further U-turns on the fiscal plans that had roiled UK financial markets. BoE Gov Bailey spoke with Hunt over the weekend, noting that there was a "meeting of minds" on the importance of sustainable fiscal policy.

- Cable added ~50 pips before stabilising, while EUR/GBP is down ~270 pips as we type. GBP/USD implied volatilities edged higher, with one-month tenor last at 18.8%.

- UK news helped support broader risk appetite, with safe-haven currencies trading on the back foot. The greenback paced losses, with a slip in the BBDXY index facilitated by lower U.S. Tsy yields.

- Participants were on the lookout for signs of Japanese officials intervening in FX markets as FinMin Suzuki & top FX diplomat Kanda reiterated that they stand ready to step in. It had earlier been flagged that the option of a stealth intervention remains on the table.

- Spot USD/JPY oscillated near neutral levels after printing 32-year highs last Friday. It last sits at Y148.71 and the psychologically significant Y145.00 figure is firmly in sight, with BoJ Gov Kuroda adamant to keep powerful monetary easing in place.

- As spot USD/CNY was testing the CNY7.2 threshold, RTRS reported that major Chinese state-owned banks were swapping yuan for dollars in forwards market and selling USD in spot market to stabilise the redback.

- U.S. Empire State Manufacturing Survey headlines the global data docket today. ECB members dominate the central bank speaker slate, with Lane, de Guindos, de Cos and Nagel set to take the floor.

AUDNZD: Can We Hold Above The 100-Day MA?

AUD/NZD has seen some support on dips just below the 100-day MA in recent sessions, see the chart below. We have spent very little time sub this support level in 2022. It currently comes in at 1.1140, versus spot at 1.1170/75. Note the 50-day comes in just under 1.1219 on the topside. Relative short-term drivers are still skewed in favor of NZD, but we do have some important data releases this week.

- The AU-NZ 2yr swap spread is back to -100bps. The last time we were at this level the cross had a 1.0800 handle. It's a slightly better picture for AUD in terms of government bond yield spreads, but only at the margin.

- Relative data surprises are still in NZ's favor, according to the Citi surprise indices, although the rate of NZ outperformance is slowing. For relative commodity prices it is a similar theme.

- The A$ is also not enjoying the same outperformance during global equity sell-off period compared to late September/early October.

- From a data standpoint, tomorrow's NZ Q3 CPI will be important, while in Australia, tomorrow's RBA minutes are in focus, as well as a speech from Deputy Governor Bullock. Thursday delivers AU September employment data.

Fig 1: AUD/NZD Wedged Between 50 & 100 Day MAs

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

ASIA FX: Little Reprieve For USD/Asia Pairs, State Banks Reportedly Curbing Onshore CNY Weakness

Asia FX, for the most part, has not enjoyed the rally some of the majors have seen against the USD at the start of this week. Most USD/Asia pairs are higher. Spot USD/CNH and 1 month USD/KRW are the exceptions, although both pairs have been supported on dips. Tomorrow the focus is likely to rest on China's Q3 GDP print, along with the September monthly round of activity data (see this link for more details).

- USD/CNH has tracked within recent ranges. We got above 7.2200 post the CNY fixing, which was a record lean against depreciation pressures but did little to boost sentiment. We dipped back sub 7.2000 but buying interest emerged. Negative covid headlines are not helping sentiment this afternoon around lockdowns in a tech hub. It was also reported this afternoon, across the wires, state banks had been selling USDs in the onshore spot market. This looked to be aimed at curbing a fresh break above the 7.2000 level.

- Spot USD/KRW got above 1440 in early trade but found selling interest around this level. Onshore equities have outperformed, which has helped, although only at the margin. Dips sub 1435 were supported. The pair was last at 1437.

- USD/TWD breached 32.00, fresh highs back to early 2017. Onshore equities slumped, in line with tech weakness in US markets on Friday. The 1month NDF is close to 32.10.

- USD/IDR is higher today, spot +57.5 figs to 15480, which is fresh highs back to early 2020. Bulls look to take out the 61.8% retracement of the 2020 sell-off/Apr 23, 2020 high of IDR15,574/15,598. The September trade surplus was close to expectations, just under $5bn, but both export and import growth surprised on the downside. Bank Indonesia will deliver its monetary policy decision this Thursday. Most (19/29) analysts surveyed by Bloomberg expect a 50bp hike to the 7-Day Reverse Repo Rate, while the rest have pencilled in a smaller 25bp rate rise.

- The 59.00 figure level for USD/PHP remains a key line in the sand as the pair struggles to penetrate this all-time high amid Bangko Sentral's activity in the market. Officials reiterated that they keep watching peso moves. FinSec/ex-BSP Gov Diokno said the central bank is monitoring FX transactions to detect speculative activity after implementing "measures to moderate sudden movements in the peso."

- USD/THB is above 38.20, not too far from recent cyclical highs (38.45 in late September). BoT commentary didn't suggest a great deal of alarm in terms of weak FX levels. It stated it stands ready to manage excessive volatility and that the country should return to a current account surplus next year.

CHINA DATA: Q3 GDP & September Monthly Data Prints Due Tomorrow

A reminder that China Q3 GDP prints tomorrow. The market expects a decent rebound from the fall in Q2. Q/Q growth is expected at +2.8% (versus -2.6% in Q2), while would take the y/y pace to 3.3% from 0.4%. Also out is the monthly run of activity indicators - IP, retail sales, fixed asset investment and the jobless rate.

- The range for q/q GDP estimates is 2.5% to 4.4%. A positive outcome is no surprise, as Shanghai emerged from lockdown conditions, which hit Q2 growth.

- Still, given the deterioration in survey numbers at the end of Q3, such as PMI prints, the market may not get too excited by any bounce.

- For September IP, the market expects a further improvement to 4.8% y/y from 4.2%.

- For retail, 3.1% y/y is forecast against a 5.4% gain last month. This would be in line with weaker services PMI readings for September, with the Chengdu lockdown weighing.

- Fixed asset investment is expected to improve slightly to +6.0% ytd y/y from 5.8%, although property investment is still forecast to remain weak at -7.5% ytd y/y versus -7.4%. Finally, the jobless rate is forecast to edge down to 5.2%, against 5.3% in August.

EQUITIES: Asia Pac Follows Wall St Lower, Kospi Outperforms

Most Asia Pac markets are following the negative lead from US markets on Friday night and are weaker for Monday’s. Losses aren't large, at least by recent standards, with higher US futures helping at the margin. Of the major indices, the Kospi is the main outperformer, around flat for the session.

- US futures are higher across the 3 main indices. Eminis back above 3600, close to +0.50% for the session. Some positive spill-over from UK fiscal developments has aided sentiment at the margin today. US yields are lower as well (2yr back to 4.46%, -3bp for the session).

- China and HK equities have lost ground. Xi's speech from the party congress over the weekend didn't give any major indications of a turnaround in policies related to Covid, housing etc. The HSI is down 1.2% at this stage, with tech off by 3%. In China, the CSI 300 is down -0.44%. Note Q3 GDP and September monthly activity figures are due tomorrow.

- The Nikkei 225 is off by over 1.20%, the Taiwan Taiex by 1.5%, in line tech weakness in US markets on Friday. The Kospi has outperformed, flat for the session and back above 2200. We were sub 2180 in early trading. Foreign buying has reportedly returned for tech names like Samsung.

- The ASX 200 is off by 1.40%, dragged lower by mining names for the most part. Lower commodity prices will be weighing.

GOLD: Stabilizes On USD Weakness

Gold is around 0.35% higher so far today, putting the precious metal back close to $1650. We closed last week just under $1645, dropping nearly 3% for the week.

- In terms of levels, late last week we saw a low close to $1640, beyond that is just under $1620 from September 28th, a cyclical low. On the topside, rallies last week rain out of momentum above $1680.

- Broader risks still appear skewed to the downside for gold, as it continues to be closely aligned with USD sentiment. Today's rebound has coincided with the DXY down by around -0.25%, with the index sitting back close to the 113.00 level.

- Gold ETF holdings continue to track lower, now back to April 2020 levels. Holdings are down around 10% from their April peak of this year.

OIL: Futures Suggest That Oil Market May Be Easing

Oil prices are higher on the day, as the USD weakened. WTI is up about 0.7% to $86.17 and Brent 0.8% to $92.35 while DXY is down 0.2%.

- The upside to oil prices has been limited after Chinese President Xi Jinping signalled no change in the country’s Zero-Covid Policy, which is weighing on growth.

- Brent’s prompt spread was in backwardation today and is signalling a tentative easing in the oil market.

- The market is still very nervous regarding global growth prospects and the subsequent impact on energy demand. Last week’s IEA warning that OPEC+ production cuts could push the world economy into recession has added to fears.

- WTI is still below its 50-day moving average but hasn’t broken the 20-day MA yet on the downside or the 5-day on the upside.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 17/10/2022 | 0800/1000 | ** |  | IT | Italy Final HICP |

| 17/10/2022 | 0800/1000 |  | EU | ECB de Guindos Speaks on Euro Anniversary | |

| 17/10/2022 | 1230/0830 | ** |  | US | Empire State Manufacturing Survey |

| 17/10/2022 | 1430/1030 | ** |  | CA | BOC Business Outlook Survey |

| 17/10/2022 | 1500/1700 | | EU | ECB Lane at Bocconi Uni & Deutsche Bank Roundtable | |

| 17/10/2022 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 17/10/2022 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 17/10/2022 | 2000/1600 | | CA | BOC Deputy Rogers panel talk at Toronto Centre |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.