Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

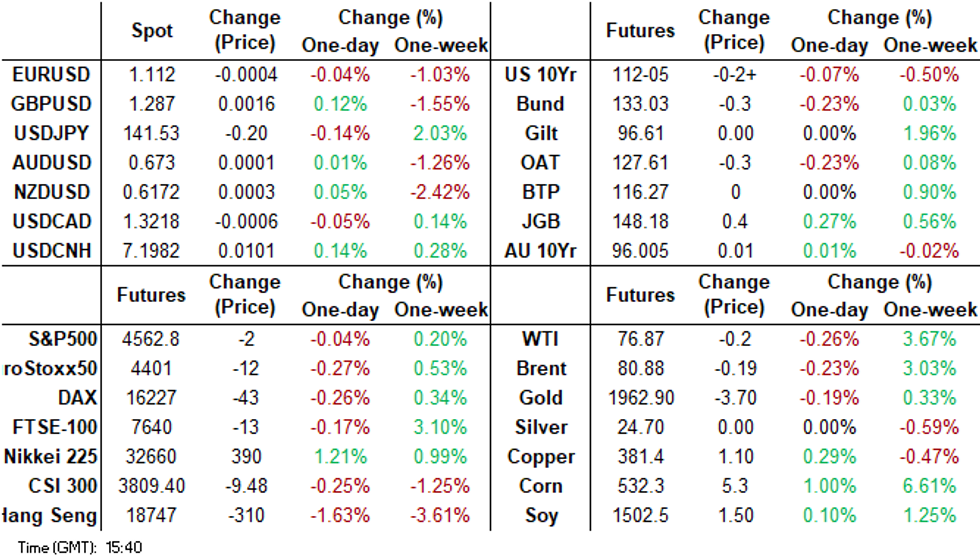

- It has been a mixed start to the week in Asia Pac today. Cash tsys sit ~1bp cheaper across the major benchmarks. JGB futures have rallied but are sub recent highs. In the FX space, yen has marginally outperformed, but USD/JPY has maintained the bulk of Friday's gain, last around 141.50.

- In the equity space, focus has again been on weakness for HK and China bourses. Concerns around property developer liquidity weighing today. USD/CNH has pushed back towards 7.2000, with negative equity spill over likely weighing.

- Looking ahead, European preliminary July PMIs are out, then Later the US preliminary S&P Global PMIs for July and the June Chicago Fed index print.

MARKETS

US TSYS: Narrow Ranges In Asia

TYU3 deals at 112-05, -0-02+, a 0-05 range has been observed on volume of ~43k.

- Cash tsys sit ~1bp cheaper across the major benchmarks.

- Tsys have observed narrow ranges in Asia with little follow through on moves.

- During today's Asian session little meaningful macro newsflow has crossed.

- With Wednesday's FOMC rate decision in view, FOMC dated OIS remain stable. A 25bp hike is priced into the meeting with a terminal rate of 5.40% seen in November. There is are ~60bps of cuts seen by June 2024.

- On the wires today we have S&P Global Mfg and Services PMI, the latest 2-Year Supply is also due.

JGBS: Futures Richer But Gains Pared During The Tokyo Session, 10Y Zone Underperforms

In the Tokyo afternoon session, JGB futures are stronger at 148.16, +38 compared to settlement levels, but well off the post-Tokyo high (148.74) ahead of the weekend.

- There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined Jibun Bank PMI data.

- The Japan breakeven inflation rate for the 10-year CPI-linked bonds rose 3 basis points to 1.168% on Monday from the previous business day, according to Bloomberg. The measure is headed for the biggest increase in two weeks. Breakevens have risen 32bp since the start of the year. (See link)

- Cash JGBs are richer across the curve apart from the 10-year zone, which is dealing 1.5bp cheaper. The outperformer on the curve has been the 20-year zone, which is 1.8bp richer. The 40-year zone is 1.3bp richer at 1.485% ahead of tomorrow’s supply.

- The swap curve has bear steepened with rates flat to 3.5bp higher. Swap spreads are wider across the curve.

- Later today sees Department Store Sales data. Tomorrow the local calendar sees no data releases. The week’s highlight will be the BoJ policy meeting on Friday.

- Globally, the calendar later today sees the release of S&P Global PMIs (Jul) along with the Chicago Fed Activity Index (Jun).

- Tomorrow the MoF plans to sell Y700mn of 40-year JGBs.

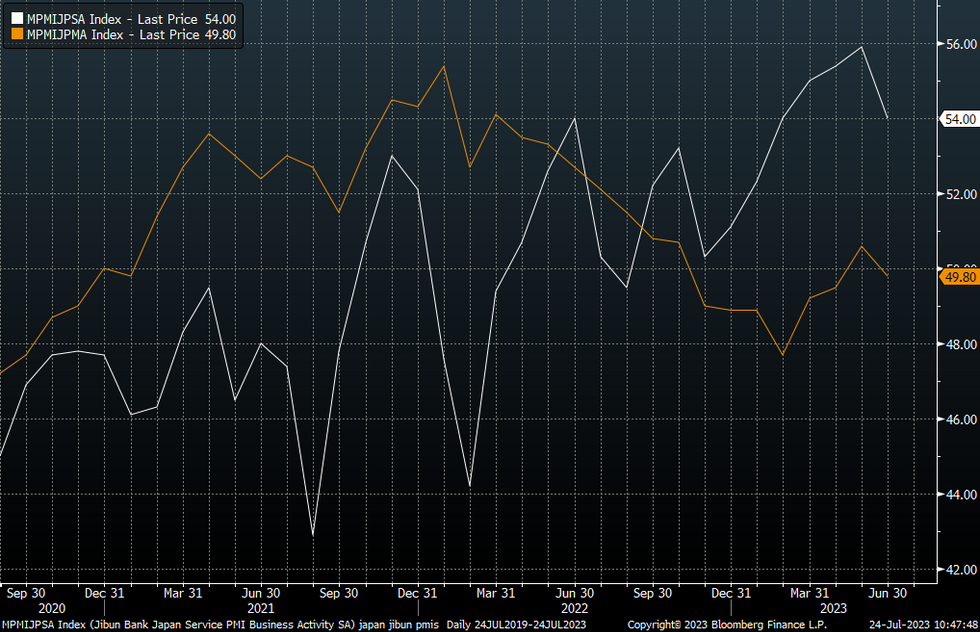

JAPAN DATA: July PMIs Hold Close To June Levels

Preliminary PMI prints for July were reasonably close to June outcomes. The Jibun Bank manufacturing PMI edged back to 49.4 from 49.8, while the services slipped to 53.9 from 54.0. This still left the composite PMI unchanged at 52.1 for the month.

- The manufacturing PMI has edged back under the expansion/contraction line in recent months, but we remain above February lows from earlier in the year at 47.70 (see the chart below). The detail showed the output index a touch higher at 48.4 versus 48.1 in June, but new orders fell versus the prior month.

- On the services side, we remained comfortably in expansion for the headline index, albeit with a modest loss of momentum. Details showed the employment sub-index falling to 49.9 from 52.9 prior, but prices charged rose versus the previous month.

Fig 1: Japan PMIs

Source: MNI - Market News/Bloomberg

AUSSIE BONDS: Richer, Narrow Range, Q2 CPI On Wednesday

ACGBs (YM +2.0 & XM +2.0) are slightly richer after trading in a narrow range in the Sydney session. There hasn’t been much local data other than the preliminary Judo Bank PMI data.

- US tsys are holding marginally cheaper in today’s Asia-Pac session with ranges narrow.

- Cash ACGBs are 2bp richer with the AU-US 10-year yield differential -3bp at +15bp.

- The 3s10s swap curve has bull steepened with rates flat to -2bp.

- The bills strip has bull steepened with pricing flat to +3.

- RBA-dated OIS pricing 1-2bp softer across meetings. A 60% chance of a 25bp hike is priced for August.

- (AFR) Economists are urging Jim Chalmers to give the Reserve Bank more voting power on the new monetary policy board, warning the central bank may lose control of interest rates to outsiders under the proposed model. (See link)

- Tomorrow the local calendar sees no data releases ahead of Q2 CPI on Wednesday. Bloomberg consensus expects headline CPI to print +1.0% q/q (5.5% y/y) versus +1.4% q/q (5.6% y/y) in Q1. Power rebates are holding down inflation while goods prices continue to rise. Trimmed Mean CPI is forecast to print +1.1% q/q (6.0% y/y) from +1.2% (6.6% y/y) in Q1, +1.7% in Q4 and +1.9% in Q3.

AUSTRALIAN DATA: PMIs Show Rising Inflation Trends As Activity Shrinks

The preliminary Judo Bank composite index showed that activity contracted in July for the first time since March driven by weaker services performance due to higher rates. The index fell to 48.3 from 50.1 with services down to 48 from 50.3 but manufacturing rose to 49.6 from 48.2. Judo Bank believes the data continues to point to a soft landing, as it sees “no signs of impending recession”.

- News on the inflation front was not good with input costs rising to their highest in four months due to higher wages and selling prices rising in the services sector, consistent with inflation of around 4-5% according to Judo Bank. Manufacturing inflation fell to a 34-month low though.

- “The disinflationary trend evident in the PMI price indicators over the course of 2022 appears to have ceased,” notes Judo Bank’s Hogan, which is likely to mean further RBA tightening.

- Despite activity contracting in July, new orders were “broadly unchanged” after growing the previous three months but driven by services with manufacturing falling again. New export orders fell in both sectors. Business confidence dipped to its lowest since the start of the pandemic due to services pessimism.

- Employment growth remained positive but at its softest rate this year. But Judo Bank observes that it is higher than activity/orders would require suggesting that labour hoarding continues.

- See Judo Bank PMI new release here.

Source: MNI - Market News/Judo Bank/Bloomberg

NZGBS: Subdued Session, Closed Richer, Global PMI Data Due

NZGBs closed on a positive note with key benchmarks 3-4bp richer after trading in a narrow range in the local session.

- June’s trade surplus narrowed to NZ$9mn from a revised NZ$52mn in May. Exports to China declined 20.4% m/m (-7.2% y/y) while exports to Australia rose +8.3% m/m (+30.3% y/y).

- Swap rates are 5-6bp lower with the 2s10s curve flatter.

- RBNZ dated OIS flat to 3bp softer across meetings. Terminal OCR expectations sit at 5.69%, just off the highest level since early July.

- RBNZ published monthly credit card spending data for June. Total spending in NZ in June rose 1.9% m/m and gained 5% y/y, after seasonal adjustment. Spending on overseas-issued cards used in NZ was NZ$423m, falling for the third consecutive month. Overseas billings on NZ-issued cards was NZ$632m, the highest value recorded in a month since August 2019.

- Tomorrow the local calendar is scheduled to release no data. The next key release is ANZ Consumer Confidence (Jul) on Friday.

- Globally, the calendar today sees the release of S&P Global PMIs (Jul) along with the Chicago Fed Activity Index (Jun).

FOREX: Yen Firmer In Asia

The Yen is firmer in Asia today, there was no headline catalyst for the move with pre BOJ positioning perhaps sparking a mild bid in JPY. Elsewhere in G-10 moves have been limited with little follow through.

- USD/JPY is ~0.2% lower and last prints at ¥141.40/50. Support comes in at ¥137.25, low from July 14 and resistance is at ¥141.96 Friday's high.

- AUD is a touch firmer, AUD/USD erased early losses and sits ~0.1% firmer last printing at $0.6730/35. The pair sits a touch above the 50-Day EMA ($0.6719), resistance comes in at $0.69.

- Kiwi is little changed, NZD/USD prints at $0.6170/75 little changed from opening levels.

- Elsewhere in G-10, SEK erased early losses of ~0.3% to sit little changed. EUR and GBP are marginally firmer.

- Cross asset wise; BBDXY is a touch lower and US Tsy Yields are ~1bp firmer across the major benchmarks. E-minis are flat and the Hang Seng is down ~1.5%.

- Today's docket is headlined by preliminary Services and Manufacturing PMI's from Europe and the US.

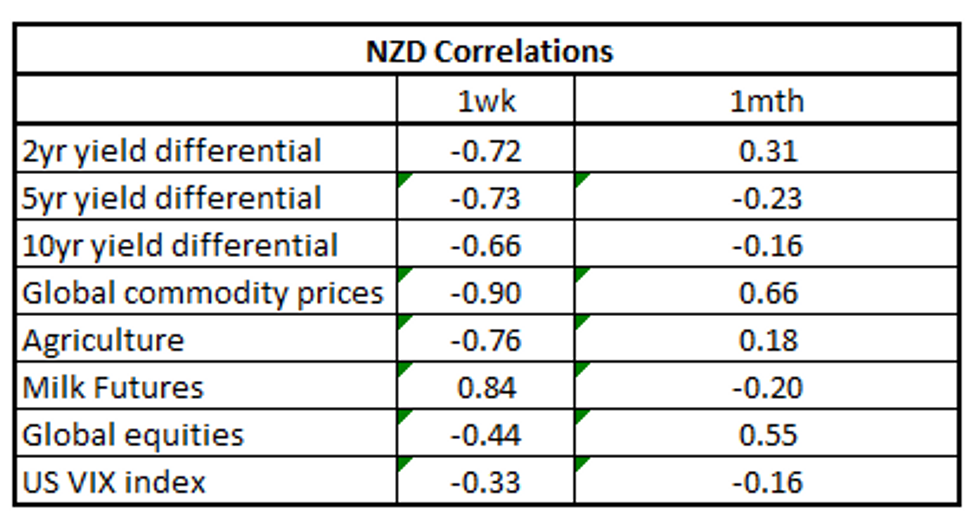

NZD Correlations: Milk Futures Dominant Driver Last Week

NZD/USD correlations with Milk Futures have strengthened over the past week, standing out as a key macro driver in recent dealings. The table below presents levels of correlations between NZD and key macro drivers (note the yield differential reflects swap rates).

- Last week's weakness in NZD/USD looks to be associated with falling milk futures prices. NZD/USD fell ~3%, its biggest weekly fall since late May.

- The pair looked through widening rate differentials as well as strength in Global Commodity prices.

- Over the longer time frame Global Commodity prices and global equities stand out as the dominant drivers.

Fig 1: NZD/USD Correlation with Global Macro Drivers:

Source: MNI/Bloomberg

EQUITIES: Weaker China Property Developers Weigh On the HSI, More Positive Moves Elsewhere

Regional equities are mixed to start the week. HK and China markets are again a soft point but there are positive signs elsewhere. US equity futures have traded tight ranges so far and sit close to flat. Eminis were last around 4564, down a touch, while Nasdaq futures were ear15547.

- Hong Kong's HSI has been the main regional drag. The index sits down 1.40% at the break. Property related names have been hit, with a sub-index gauge for the sector down nearly 2.90%. Country Garden has fallen after J.P. Morgan cut the company to UW, owing to liquidity concerns for private sector developers. The company also doesn't see last week's urban development announcement as shifting the property sector narrative.

- Mainland indices are mixed. The CSI down 0.25% at the break, while the Shanghai Composite is slightly higher. China's State Planner announced released measures to boost private sector investment today (see this link for more details).

- The Kospi has outperformed up 0.40% at this stage, although is away from earlier highs. Posco has surged on better earnings and positive investor sentiment around the electric-battery vehicle outlook. The Taiex is close to flat, despite a rebound in the SOX during Friday US trade.

- In Japan major indices are higher, with the Topic near +0.85%, while the Nikkei 225 is close to +1.35% firmer. Late last week, news wires reported the BoJ was likely to hold steady this week in terms of YCC. Bank names have underperformed somewhat, but sectors linked to a weaker yen (such as autos) and the electrical appliance sector have rallied.

- In SEA trends are mostly positive except for Singapore shares. Gains elsewhere are under 0.50% at this stage.

OIL: Crude Down Slightly But Holds Onto Most Of Friday’s Gains

Oil is trading off its intraday lows but is still down around 0.1% on Friday’s close, as Fed jitters have limited upside. WTI is around $76.98/bbl close to the intraday high of $77.05 but off the low at $76.56. Brent is $80.97 just beneath the high of $81.04 which followed a low of $80.51. The USD index is off its low to be flat.

- WTI has faced round-number resistance at $77 as the break above was very brief. $76.60 has provided support. Brent hasn’t been able to sustain moves above $81 but $80.50 has provided a floor today. It is holding above its 200-day MA.

- The widely expected 25bp Fed hike following Wednesday’s meeting should already be priced into the oil market, but the accompanying comments could drive some volatility in prices. A hawkish tone could push prices sharply lower, as the crude market fears a US recession.

- Later the US preliminary S&P Global PMIs for July and the June Chicago Fed index print. There are also European preliminary July PMIs.

GOLD: Second Consecutive Decline On Friday Ahead Of Major Central Bank Meetings This Week

Gold is slightly weaker (-0.1%) in the Asia-Pac session as the world's major central banks gear up for a crucial week. The Fed is scheduled to meet on Wednesday, followed by the ECB on Thursday, and the BoJ on Friday. Investors are confident that both the Fed and ECB will implement further tightening measures, with 24bp of hikes already factored in for each of them. With respect to the BoJ, Bloomberg and Reuters have cited sources in reporting that the board were leaning toward no change in approach in the coming policy meeting, countering recent speculation that a policy switch would be imminent.

- Gold closed lower (-0.4%) at $1961.9 on Friday for its second consecutive day after another step higher in the USD index.

- However, bullion didn't trouble support at $1934.4 (20-day EMA) whilst resistance remains at the early Thursday high of $1987.5.

- Money managers are turning more bullish on gold, having increased net-long positions to a 10-week high. (See link)

ASIA FX: USD/CNH Pushing Back Towards 7.2000

USD/Asia pairs have been mixed today. USD/CNH has pushed higher towards 7.2000, amid further equity headwinds. TWD and MYR have also underperformed. KRW has fared better, while mostly flat trends are evident elsewhere. Still to come is Taiwan unemployment and IP figures for June. Tomorrow, South Korea Q2 GDP is out, along with the BI decision in Indonesia (no change expected).

- USD/CNH has pushed higher today, the pair last in the 7.1980/90 region. Highs came in just above 7.1990, while an earlier dip sub 7.1800 was supported. We are seeing a weaker equity tone in HK and to a lesser extent mainland equities, as property related names underperform on the back of continuing liquidity concerns. The CNY fixing was stronger than expected, although the fixing error term less wide compared to late last week.

- The won has outperformed today, with the 1 USD/KRW month NDF last sub 1280, around 0.50% firmer in won terms versus Friday closing levels in NY. Better earnings from Posco have helped local equities track higher. The Kospi was last +0.70%. Offshore investors have still been net sellers so far today (-$136.3mn).

- USD/TWD has pushed higher again today. The pair sits just below session highs, last near 31.36 (earlier highs close to 31.39). The 1 month NDF is close at around 31.34. A break above 31.40 for spot would be fresh YTD highs in the pair and levels not seen since mid November last year. In NEER terms we are already at fresh YTD lows, last near 120.0 in terms of the J.P. Morgan index. The tail end of last week saw decent offshore outflows from foreign investors. Friday saw -$979.60mn in net outflows, bringing last week's outflows to -$1.24bn, representing roughly half the outflows seen in July to date.

- The Ringgit is softer in early trade as it continues to trim its post US CPI gains. USD/MYR prints at 4.5730/65 and is ~0.3% firmer in early dealing today. The pair sits ~1.4% above July to date lows. The June CPI print came in as expected at 2.4% Y/Y and there has been little reaction thus far in FX.

- The SGD NEER (per Goldman Sachs estimates) is little changed in early dealing, the measure sits a touch off cycle highs and is ~0.2% below the top of the band. USD/SGD is see-sawing around the $1.33 handle in a narrow range in todays dealing. On the wires a short time ago headline CPI printed at 4.5% Y/Y a touch firmer than the expected 4.4%. Core CPI was in line with expectations at 4.2% Y/Y. On Wednesday June Industrial Production is due, a rise of 3.8% M/M is expected. The June Unemployment Rate will cross on Thursday or Friday.

- USD/THB tracks back near 34.50 in latest dealings, around 0.10% weaker in baht terms versus closing levels from last Friday. A cluster of EMA sit between 34.60 to 34.70. Recent highs also rest above the 35.00 level, while on the downside, recent lows are near 33.76. The combination of a stronger USD trend, coupled with uncertainty around the election outcome, is likely weighing on baht sentiment. As we noted, earlier Pheu Thai will decide over the next few days on the PM candidate after consulting with the Senate and coalition partners. It remains to be seen if the Move Forward Party is part of that coalition. The next parliamentary PM vote scheduled for July 27th.

- USD/IDR sits little changed in the first part of trading today. The pair last at the 15025/30 level, which is close to where we opened. We did tick up to 15035 but had little follow through. On the topside, the 200-EMA isn't too far away, sitting at 15041. Earlier July highs came in above 15200. The 20 and 100 day EMAs are just below current spot levels, while further south is the 50-day 14981. The main focus from a macro standpoint will be tomorrow's BI meeting outcome, which is widely expected to deliver no change to the policy rate (currently at 5.75%).

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 24/07/2023 | 0700/0900 | ** |  | ES | PPI |

| 24/07/2023 | 0715/0915 | ** |  | FR | S&P Global Services PMI (p) |

| 24/07/2023 | 0715/0915 | ** | | FR | S&P Global Manufacturing PMI (p) |

| 24/07/2023 | 0730/0930 | ** |  | DE | S&P Global Services PMI (p) |

| 24/07/2023 | 0730/0930 | ** | | DE | S&P Global Manufacturing PMI (p) |

| 24/07/2023 | 0800/1000 | ** |  | EU | S&P Global Services PMI (p) |

| 24/07/2023 | 0800/1000 | ** | | EU | S&P Global Manufacturing PMI (p) |

| 24/07/2023 | 0800/1000 | ** | | EU | S&P Global Composite PMI (p) |

| 24/07/2023 | 0830/0930 | *** |  | UK | S&P Global Manufacturing PMI flash |

| 24/07/2023 | 0830/0930 | *** | | UK | S&P Global Services PMI flash |

| 24/07/2023 | 0830/0930 | *** | | UK | S&P Global Composite PMI flash |

| 24/07/2023 | 1345/0945 | *** |  | US | IHS Markit Manufacturing Index (flash) |

| 24/07/2023 | 1345/0945 | *** | | US | S&P Global Services Index (flash) |

| 24/07/2023 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 24/07/2023 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 24/07/2023 | 1700/1300 | * | | US | US Treasury Auction Result for 2 Year Note |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.