Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

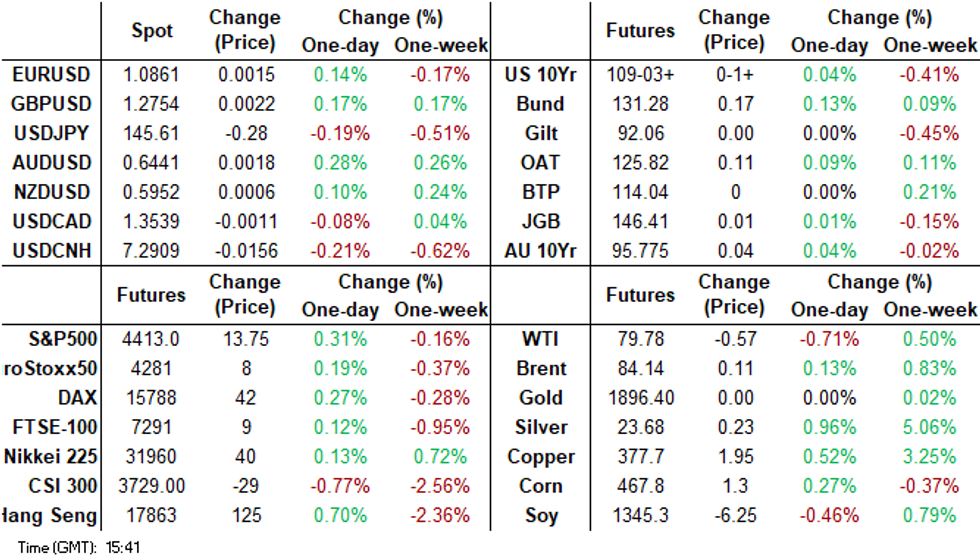

- In Australia the preliminary Judo Bank PMIs for August showed that private sector output continued to contract in August especially in the important services sector. The indices are portraying a weak economy consistent with the RBA on hold. ACGBs (YM +2.0 & XM +4.5) are richer, dealing at or near Sydney session highs. AUD/USD is firmer though (last 0.6640/45), with higher metal prices, particularly for iron ore providing an offset.

- In NZ, Q2 retail sales volumes were weaker than expected falling 1% q/q but since the series has contracted 5 of the last 6 quarters the annual rate improved to -3.4% from -4.3%. This data shows that spending remained subdued in Q2 which the RBNZ said is needed to “reduce inflation pressure”.

- Elsewhere, the cash JGB curve has twist steepened, pivoting at the 3s, with yields 0.1bp lower to 0.9bp higher. The benchmark 10-year yield is 0.9bp higher at 0.675%, close to the post-YCC tweak high.

- Looking ahead, flash PMIs from France, Germany and the Eurozone provide the highlight in today's European session, further out we have US new home sales and S&P Global PMIs. The latest 20-Year Supply is also due.

MARKETS

US TSYS: Curve Marginally Flatter In Asia

TYU3 deals at 109-04+, +0-02+, a 0-06+ range has been observed on volume of ~70k.

- Cash tsys sit flat to 2bps richer across the major benchmarks, light bull steepening is apparent.

- In a data light session Tsys ticked higher alongside a bid US Equity Futures and pressure on the USD as sentiment improved in Asia.

- The move higher didn't follow through and Tsys pared gains to deal in a narrow range through the session. Little meaningful macro newsflow crossed.

- Flash PMIs from France, Germany and the Eurozone provide the highlight in todays European session, further out we have US new home sales and S&P Global PMIs. The latest 20-Year Supply is also due.

JGBS: Futures Holding In Positive Territory, New Post-YCC Tweak High For 10Y Yield

In the Tokyo afternoon session, JGB futures are holding in positive territory, +4 compared to the settlement levels, after trading in a relatively narrow range in the morning session.

- There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined Jibun Bank PMIs.

- US tsys sit flat to 2bp richer across the major benchmarks, with a light bull steepening apparent. There has been little meaningful macro newsflow.

- The cash JGB curve has twist steepened, pivoting at the 3s, with yields 0.1bp lower to 0.9bp higher. The benchmark 10-year yield is 0.9bp higher at 0.675%, close to the post-YCC tweak high.

- The swap curve has bear steepened, with rates flat to 0.9bp higher. Swap spreads are wider, after being tighter in the morning session.

- Tomorrow the local calendar sees Weekly International Investment Flow data, ahead of Tokyo CPI data for August on Friday. Later today sees Machine Tool Orders for July (Preliminary).

- Flash PMIs from France, Germany and the Eurozone provide the highlight in today's European session, further out we have US new home sales and S&P Global PMIs. The latest 20-year supply is also due.

- Tomorrow the MoF plans to conduct Liquidity Enhancement Auctions for OTR 15-5-39.9-year JGBs.

AUSSIE BONDS: Richer, Near Session Highs, PMIs Portray A Weak Economy

ACGBs (YM +2.0 & XM +4.5) are richer, dealing at or near Sydney session highs.

- There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined Judo Bank PMIs for August, which showed that private sector output continued to contract in August, especially in the important services sector.

- A strengthening by US tsys in Asia-Pac trade assisted the local market’s move away session cheaps. Little meaningful macro news flow has crossed. US tsys sit 1-3bps richer across the major benchmarks.

- Cash ACGBs are 3-4bp richer, with the AU-US 10-year yield differential 2bp tighter at -8bp.

- ACGB Nov-33 supply sees strong demand, with average yield printing below the prevailing yield. The cover ratio showed above the 4.00x mark.

- Swap rates are 1-4bp lower, with the 3s10s curve flatter.

- The bills strip has bull flattened, with pricing flat to +3.

- RBA-dated OIS pricing is flat to 2bp softer across meetings. The market continues to attach a 5% chance of a 25bp hike at the September meeting. Terminal rate expectations sit at 4.21%.

- The local calendar is empty for the rest of the week.

- The US calendar sees new home sales and S&P Global Manufacturing PMI later today.

AUSTRALIAn DATA: PMI Data Signal Shrinking Q3 Private Sector Activity

The preliminary Judo Bank PMIs for August showed that private sector output continued to contract in August especially in the important services sector. The indices are portraying a weak economy consistent with the RBA on hold. The AUDUSD hasn’t reacted and is steady around 0.6424.

- The composite index deteriorated to 47.1 from 48.2 in July, the lowest since January 2022, as new orders shrank. Manufacturing is down slightly to 49.4 from 49.6 but services are down to 46.7 from 47.9. Cost of living and tighter financial conditions are reducing demand domestically as domestic orders fell more than those from overseas. Export orders only contracted slightly.

- Employment continued to grow across the economy as businesses are more optimistic re the outlook a year ahead. Business confidence improved to its highest in 7 months.

- The good news was that price pressures eased in the services sector with cost increases slowing enabling selling price inflation to moderate after rising in July. However manufacturing saw an increase in costs due to deteriorating supply conditions which were then passed onto customers.

- See Judo Bank report here.

Source: MNI - Market News/Bloomberg

NZGBS: Closed On A Strong Note, Q2 Real Retail Sales Misses

NZGBs closed at the richest level of the local session, with benchmark yields 7-8bp lower. The richening through the session received a boost from weaker-than-expected Q2 retail sales volumes.

- Q2 retail sales ex-inflation declined 1% q/q but since the series has contracted 5 of the last 6 quarters the annual rate improved to -3.4% from -4.3%. Q1 was revised down 0.2pp to -1.6%. Nominal sales fell 0.2% q/q to be up 2.7% y/y. This data shows that spending remained subdued in Q2 which the RBNZ said is needed to “reduce inflation pressure”. It should be reassured at this point that with rates at 5.5%, it can achieve this.

- US tsys are holding onto early gains in the Asia-Pac session. Little meaningful macro news flow has crossed. US tsys sit flat to 2bp richer across the major benchmarks.

- Swap rates are 9-12bp lower, with the 2s10s curve steeper and implied swap spreads sharply tighter.

- RBNZ dated OIS pricing closed 2-8bp softer across meetings beyond October, with terminal OCR expectations at 5.67%.

- The local calendar is empty for the rest of the week.

- Tomorrow the NZ Treasury plans to sell NZ$250mn of the 4.5% Apr-27 bond, NZ$150mn of the 2.0% May-32 bond and NZ$100mn of the 2.75% May-51 bond.

NEW ZEALAND DATA: Q2 Retail Sales Confirm Subdued Spending

Q2 retail sales volumes were weaker than expected falling 1% q/q but since the series has contracted 5 of the last 6 quarters the annual rate improved to -3.4% from -4.3%. Q1 was revised down 0.2pp to -1.6%. Nominal sales fell 0.2% q/q to be up 2.7% y/y. This data shows that spending remained subdued in Q2 which the RBNZ said is needed to “reduce inflation pressure”. It should be reassured at this point that with rates at 5.5% it can achieve this.

- The weakness was fairly broad based with 11 of the 15 retail industries recording declines with the largest negative contributions from food & beverages and hardware. The strongest sector was motor vehicles & parts which were probably boosted by changes to the Clean Car Discount scheme in July, according to Statistics NZ.

Source: MNI - Market News/Refinitiv

FOREX: Dollar Marginally Pressured In Asia

The USD has been marginally pressured in Asia today as risk sentiment improves, US Equity Futures are higher and US Tsy Yields have ticked lower. There was another strong Yuan fixing by the PBOC which also weighed on the greenback.

- AUD is the strongest performer in the G-10 space at the margins, stronger metals are aiding the AUD outperformance. SGX Iron Ore Futures are up ~1.4%, and are ~13% above levels seen last week. Resistance comes in at $0.6480, high from Aug 16.

- Kiwi is lagging in the space, NZD/USD has trimmed an earlier ~0.3% gain to sit up ~0.1%. Bulls look to regain the $0.60 handle to target the 20-Day EMA ($0.6039). Q2 Retail Sales were softer than expected, adding to concerns about the domestic economy.

- The Yen is firmer benefiting from lower US Tsy Yields, USD/JPY is ~0.2% lower and last prints at ¥145.65/70. Technically the uptrend in USD/JPY remains intact, resistance comes in at ¥146.56 (Aug 17 high) and ¥146.93 (8 Nov 22 high). Support comes in at ¥144.93 (low from Aug 18).

- Elsewhere in G-10, EUR and GBP are up ~0.1%.

- Cross asset wise; e-minis are ~0.3% firmer and BBDXY is down ~0.1%. 10 Year US Tsy Yields are ~2bps lower.

- Flash PMIs from France, Germany and the Eurozone provide the highlight in todays European session.

EQUITIES: China Shares Tracking Lower, Positive US Futures Aiding Sentiment Elsewhere

Regional equities are presenting a mixed backdrop in Wednesday Asia Pac trade to date. China equities have tracked lower in the first part of trade, but HK shares are higher. Other parts of the region are mixed. A positive US futures backdrop, with Eminis last tracking around 4410 (+0.25%) and Nasdaq futures +0.35% has helped sentiment at the margins.

- A lot of the Wednesday US stock market focus is likely to rest on Nvidia's results, with bullish sentiment around the AI sector a key underpinning of the rally seen through parts of Q1/Q2 of this year in the tech related space.

- China markets haven't been able to see positive follow on after yesterday's late session rally. The CSI 300 is back off by ~0.70% at the break, with the index around 3731, which is above intra-day lows from yesterday near 3700. A number of onshore media articles have highlighted potential support points/regulatory changes for local equities (see here and here for more details).

- The HSI is faring better, the index up 0.35% at the break. Trade has been volatile, while the tech sub index is modestly underperforming, albeit up from session lows.

- Japan stocks are a touch firmer, the Topix last +0.10%. Bank stocks were weaker in early trade (following US bank weakness in Tuesday trade post rating downgrades), but the firmer US futures backdrop has helped turn sentiment around.

- The Kospi is down 0.55% at this stage, while the Taiex is faring better, +0.70%.

- In SEA, Thai stocks are a touch higher, following yesterday's +1% gain as the political impasse came to an end. Trends are mixed elsewhere.

OIL: Crude Stabilises On US Inventory Drawdown & Lower USD

Oil prices are off their lows earlier in the session to be moderately higher as the risk tone has improved, the dollar is slightly weaker (USD index -0.1%) and API crude inventories fell. Brent is up 0.2% to $84.16/bbl after trading below $84 earlier in the session. It is just off its high of $84.26. WTI is approaching $80 rising 0.2% to $79.83, close to the intraday high of $79.91.

- Crude is down around a percent this week as demand concerns, especially from China, have outweighed supply tightening. The market is also jittery about the chance of further US rate hikes which Friday’s Jackson Hole speech by Fed Chairman Powell may shed light on. But the market is still projected to be in deficit in H2 2023.

- Bloomberg reported that API data showed US crude inventories fell a further 2.4mn barrels in the latest week, according to people familiar with the data. This has helped to stabilise oil prices. The official EIA data is out later which fell 5.96mn barrels in the latest data.

- Later there are preliminary US and European PMIs for August. There are no Fed speakers.

GOLD: Slightly Firmer But Remains Around Five-Month Lows

Gold is slightly higher in the Asia-Pac session, after closing +0.1% at $1897.48 on Tuesday. The yellow metal briefly pushed to its highest level since Aug 16 on Tuesday but didn’t trouble resistance at $1918.3 (20-day EMA), according to MNI's technicals team.

- Bullion regained some lost ground after a paring of earlier intraday USD strength and the push higher in US tsy yields.

- Nevertheless, gold remained near a five-month low on increasing signs that US interest rates will need to stay higher for longer.

- The pivotal economic event of this week centres on the speech by Fed Chair Powell at the Jackson Hole gathering on Friday. The prevailing concern is that Powell might undermine investors' optimistic expectations, specifically the notion that the Federal Reserve has concluded its interest rate hikes and is poised to initiate rate cuts in the early months of the upcoming year.

INDONESIA: MNI BI Preview - August 2023: FX Stability Centre Stage

- Bank Indonesia (BI) is widely expected to keep rates steady at 5.75% where rates have been since the last hike in January. While inflation has returned to target, which would suggest an imminent easing, the rupiah has weakened. BI has other tools apart from the policy rate to manage FX stability, it is also unlikely to want to put pressure on it by easing policy before the US and others in the Asia region.

- BI has a number of ways it can manage IDR stability including intervention, “operation twist”, and the FX term deposit facility for export earnings. Governor Warjiyo commented that BI doesn’t need to move in line with the Fed even though it expects Fed hikes in both July and September.

- The weaker IDR and BI’s focus on strengthening currency stability are likely to mean that a switch to easing has been postponed to 2024.

- See full preview here.

SOUTH KOREA: MNI BoK Preview - August 2023: Holding Steady, Staying Restrictive

- The BoK is likely to remain firmly on hold at tomorrow's policy announcement. This will mark the 5th straight meeting that the policy rate has been held at 3.50%.

- Recent inflation trends support the on hold stance, but BoK may be reluctant to get too confident in the outlook, given less favorable base effects in H2 and rising local food and global energy prices. Core prices and inflation expectations are also coming down less quickly compared to headline CPI momentum. The weaker won trend could also bring back firmer imported inflation pressures at some stage, so the central bank may not want to sound too dovish.

- Indeed, it may leave scope for rates to go to 3.75%, to retain a hawkish bias, and push back against the notion of rate cuts in the near term. Equally though the bar for another rate hike is likely to remain fairly high, with policy settings already in restrictive territory.

- See the full preview here:

SOUTH KOREA DATA: Business Sentiment Steady, Along With Export Expectations, Price Indices Rise From Low Base

Earlier data showed steady manufacturing and non-manufacturing business sentiment for September. The manufacturing print was at 69, which is above early 2023 lows but down from June highs of 73. The index is still suggesting some improvement in y/y GDP momentum, albeit from a low base. The non-manufacturing index printed at 76, which is also above earlier 2023 lows but down off mid-year highs.

- Both indicators are suggesting some improvement in the growth backdrop, but are well below 2022 levels.

- In terms of the detail, most sub-indices were unchanged or near August levels. On the domestic side, sale expectations nudged down a touch, while production eased to 78 from 82.

- Raw material prices rose to 109, but are coming from a low base. Sale prices also firmed but again from a low base.

- Export expectations were unchanged at 66, see the chart below of this measure against South Korean y/y export growth. The authorities continue to express optimism around the export outlook as we progress through H2.

Fig 1: Manufacturers Export Expectations & South Korea Export Growth Y/Y

Source: MNI - Market News/Bloomberg

ASIA FX: CNH Supported By Intervention Headlines, PHP Weakens

USD/Asia pairs have been mixed today, despite the softer USD tone against the majors. USD/CNH saw some downside traction, with reports of state banks selling USDs onshore helping, but there hasn't been much follow through. Weaker onshore equities aren't helping. USD/PHP has continued to recover. Tomorrow the focus will largely rest on the BOK and BI decisions, with both central banks likely to hold rates steady.

- Bloomberg headlines crossed that state owned banks were seen buying CNY/USD around the 7.2900 level. Earlier highs in USD/CNY came in just above 7.2930, while we now sit at 7.2810, lows for the session coming in at 7.2757. Outside of a sharp move lower in the pair, there hasn't been much follow through. USD/CNH sits at 7.2915/20 currently, also above earlier lows of 7.2830, which likely coincided with onshore USD/CNY spot moving lower. Weakness in onshore equities has provided an offset, with the CSI 300 down nearly 0.75% at this stage.

- USD/HKD spot has consolidated somewhat, with spot finding some resistance to a break above 7.8400 in the near term. The pair was last around 7.8370. Recent highs rest around the 7.8395 level. US-HK yield differentials still remain skewed in favor of the USD, although market participants may not see the same risk/reward given spot USD/HKD is getting closer to the top end of the peg band.

- The Rupee has firmed off multi-month lows in recent dealing, USD/INR had printed its highest level since mid-October before marginally paring gains. RBI Governor Das is slated to give a speech in Mumbai on Wednesday. Looking ahead the data calendar is empty until 31 Aug when Q2 GDP crosses.

- USD/MYR prints at 4.6515/40, the pair is a touch lower on Wednesday. The pair sits a touch off its highest level since mid-July as August's gains are consolidated in a narrow range above the 4.65 handle. We sit ~3.2% above the opening levels from Aug 1. The latest Foreign Reserves data from Aug 15 showed a downtick to $112.2bn from $112.9bn. July CPI crosses on Friday, a downtick in inflation to 2.1% Y/Y from 2.4% is expected.

- The SGD NEER (per Goldman Sachs estimates) is little changed in early dealing and sits a touch off its highest level since 10 Aug. The measure is ~0.7% below the top of the band. Broader greenback trends continue to dominate flows as USD/SGD continues to edge lower while narrow ranges persist. The pair is a touch lower this morning and last prints at $1.3560/65. July CPI printed at 4.1% Y/Y a touch below the estimated 4.2%, core CPI was in line with expectations at 3.8% Y/Y.

- Comments from Philippines Finance Secretary Diokno have crossed the wires. Diokno states he is confident BSP can cut the policy rate by Q1 next year, as inflation will hit the lower end of the 2-4% target range by then. Note he also sits on the BSP board. USD/PHP sits slightly higher now, last at 56.65/70, (+0.55% for the session). Comments around confidence in a Q1 cut next year may be weighing, although broader USD sentiment has stabilized somewhat, so that may also be a factor. Yesterday lows in the pair came in around 56.10.

- USD/THB is holding sub 35.00, last near 34.90, slightly down for the session. Moves up to 35.00 are generally drawing selling interest. Srettha has been confirmed as Thailand PM by the Prime Minister. Focus is now likely to shift to how the new government revives economic growth, which slowed in Q2.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 23/08/2023 | 0715/0915 | ** |  | FR | S&P Global Services PMI (p) |

| 23/08/2023 | 0715/0915 | ** | | FR | S&P Global Manufacturing PMI (p) |

| 23/08/2023 | 0730/0930 | ** |  | DE | S&P Global Services PMI (p) |

| 23/08/2023 | 0730/0930 | ** | | DE | S&P Global Manufacturing PMI (p) |

| 23/08/2023 | 0800/1000 | ** |  | EU | S&P Global Services PMI (p) |

| 23/08/2023 | 0800/1000 | ** | | EU | S&P Global Manufacturing PMI (p) |

| 23/08/2023 | 0800/1000 | ** | | EU | S&P Global Composite PMI (p) |

| 23/08/2023 | 0830/0930 | *** |  | UK | S&P Global Manufacturing PMI flash |

| 23/08/2023 | 0830/0930 | *** | | UK | S&P Global Services PMI flash |

| 23/08/2023 | 0830/0930 | *** | | UK | S&P Global Composite PMI flash |

| 23/08/2023 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 23/08/2023 | 1230/0830 | ** |  | CA | Retail Trade |

| 23/08/2023 | 1345/0945 | *** | | US | IHS Markit Manufacturing Index (flash) |

| 23/08/2023 | 1345/0945 | *** | | US | S&P Global Services Index (flash) |

| 23/08/2023 | 1400/1000 | *** | | US | New Home Sales |

| 23/08/2023 | 1400/1600 | ** | | EU | Consumer Confidence Indicator (p) |

| 23/08/2023 | 1430/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 23/08/2023 | 1530/1130 | ** | | US | US Treasury Auction Result for 2 Year Floating Rate Note |

| 23/08/2023 | 1700/1300 | ** | | US | US Treasury Auction Result for 20 Year Bond |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.