Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- US Equity futures firmed in early dealing with tsys as reports crossed that despite there being no deal on the US Debt Ceiling Republicans were "optimistic" of one being struck. However there was little follow through to the moves and narrow ranges were observed for the remainder of the Asian session.

- A similar theme was observed in Oil markets, WTI futures ticked away from best levels after an early rally.

- RBNZ dated OIS pricing is 3-11bp firmer across meetings ahead of tomorrow’s RBNZ policy meeting. 36bp of tightening is priced for tomorrow’s RBNZ meeting, terminal rate expectations are at a new cycle high of 5.93%.

MARKETS

US TSYS: Curve Marginally Flatter In Asia

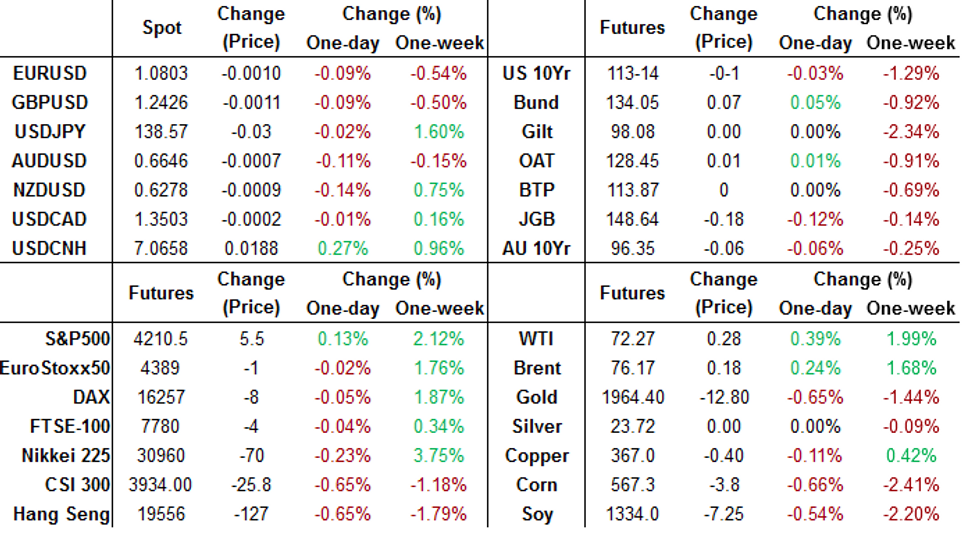

TYM3 deals at 113-15, unchanged from Monday's settlement level, a 0-04 range has been observed on volume of ~97k.

- Cash tsys sit 1bp cheaper to 1 bp richer across the major benchmarks, the curve has twist flattened pivoting on 10s.

- Tsys firmed as reports surfaced of President Biden and House Leader McCarthy's talks on the US debt ceiling. Despite ending with no deal the talks were described as "optimistic" and will continue.

- There was little follow through on the early move and tsys pared gains to deal in a narrow range for the remainder of the session.

- FOMC dated OIS price a terminal rate of ~5.20% in July with ~50bps of cuts scheduled for 2023.

- In Europe today we have flash Eurozone, German and French PMIs. Further out we have a slew of US data including Philadelphia Fed Non-Mfg Activity, New Home Sales and flash Services & Mfg PMIs. Fedspeak from Dallas Fed President Logan will cross. We also have the latest 2-Year supply.

JGBS: Futures Hit Tokyo Session Cheaps In Afternoon Trade

JGB futures have weakened in afternoon Tokyo trade, reaching session lows and currently standing at -15 compared to the settlement levels.

- There haven't been significant domestic factors worth highlighting, apart from the previously mentioned positive results of the May Preliminary Jibun Bank Services and Manufacturing PMI. Consequently, local market participants are likely monitoring headlines and observing the movements in US tsys. In Asia-Pacific trade, US tsys have shown a twist flattening, with yields +1bp to -1bp.

- Cash JGBs are mixed across the curve with yields +1.3bp to -0.6bp. The 40-year zone is the strongest performer ahead of the scheduled supply on Thursday. The benchmark 10-year yield is 0.3bp lower at 0.396%. The futures-linked 7-year zone is the weakest with its yield +1.2bp.

- The auction of 10-year inflation-indexed JGBs draws a higher-than-expected cut-off price, indicating strong demand as the Asian nation’s inflation remains elevated. The bid-to-cover ratio rose to 3.5 from 3.06 on Feb. 9, which was the lowest since August 2021.

- Swap rates are higher with the curve steeper. Swap spreads are wider across the curve, beyond the 1-year zone.

- Tomorrow will see BoJ Rinban operations covering 1- to 25-Year JGBs along with Machine Tool Orders (April final).

AUSSIE BONDS: Weaker, Sitting Just Off Cheaps

ACGBs are weaker (YM -6.0 & XM -5.5) sitting just off Sydney session lows with a relatively light local calendar. Without domestic drivers, local participants were likely on headlines and US tsys watch. US tsys have twist flattened in Asia-Pac trade with yields +1bp to -1bp.

- Cash ACGBs are 5bp cheaper with the AU-US 10-year yield differential +1bp at -7bp.

- Swap rates are also 5-6bp higher with EFPs little changed.

- The bills strip is steeper with pricing -1 to -7.

- RBA dated OIS are 1-4bp firmer across meetings beyond June. The market attaches a 16% chance of a 25bp hike at the June meeting.

- A Bloomberg article reports an A$8.6 billion debt levy on businesses with payrolls above A$10 million a year and property investors form the centrepiece of Victoria’s budget to “pay off our COVID credit card”, Treasurer Tim Pallas revealed on Tuesday – AFR. (link)

- The local calendar is light tomorrow with the Westpac-MI Leading Index as the only release.

- RBA Jacobs, Head of Domestic Markets, speaking at a Fixed Income Forum in Tokyo (0810 BST / 1710 AEST).

- The AOFM plans to sell A$800mn of the 3.50% 21 December 2034 bond tomorrow.

NZGBS: Weaker, At Cheaps, RBNZ Policy Decision Tomorrow

NZGBs ended the session on a low note with the 2-year and 10-year benchmark yields respectively rising by 8bp and 6bp, ahead of tomorrow’s RBNZ policy meeting.

- The RBNZ will review revised projections that are expected to indicate stronger economic growth, sustained inflation, and a lower peak in the unemployment rate. It is likely that the projection for a recession in 2023 will be removed due to increased demand resulting from reconstruction spending and a surge in migration.

- A Bloomberg survey of economists revealed a median expectation of a 25bp hike to 5.50% from the RBNZ tomorrow. 18/21 economists expected a 25bp increase with ASB, TD Securities and UBS expecting a 50bp increase.

- RBNZ dated OIS pricing is 4-14bp firmer across meetings. 37bp of tightening is priced for tomorrow’s RBNZ meeting. Terminal rate expectations are at a new cycle high of 5.94%.

- Pricing has shunted firmer over recent days, following a more stimulatory than expected NZ budget. With a fiscal impulse moving into positive territory next year, pricing has firmed 9-38bp across meetings post-budget with early ’24 leading.

- Swap rates are 9-11bp higher with implied swap spreads 2-3bp wider.

- The local calendar sees the release of Retail Sales Ex-Inflation ahead of the RBNZ policy decision tomorrow.

FOREX: Greenback Little Changed In Asia, Fresh Multi-Month High For USD/JPY

The USD is little changed in Tuesday's Asian session, USD/JPY printed a fresh multi month high before meeting resistance ahead of ¥139 and paring losses to deal unchanged.

- USD/JPY prints at ¥138.45/55, unchanged from yesterday's closing levels. The pair printed its highest level since 29 Nov before meeting resistance ahead of ¥139 and paring losses in volatile trade. The latest round of flash PMIs showed the Japanese economy's recovery is gaining momentum.

- AUD/USD prints at $0.6650/55 little changed on Tuesday. Flash Judo Bank PMIs for May crossed Services PMI fell to 51.8 from 53.8, Mfg PMI remained in contractionary territory at 48.0. The Composite measure printed at 51.2.

- Kiwi has also traded in narrow ranges and is little changed in Asia. NZD/USD briefly firmed above $0.63 before paring gains after being unable to follow through on the move higher. The pair last prints at $0.6280/85.

- Elsewhere in G-10 NOK and SEK are marginally pressured however liquidity is generally poor in Asia.

- Cross asset wise; BBDXY is flat, e-minis are ~0.2% firmer.

- In Europe today we have Eurozone, German and French flash PMIs before a slew of US data including Philadelphia Fed Non-Mfg Activity, New Home Sales and Services & Mfg PMIs.

OIL: Prices Supported By Improved Risk Sentiment, But Demand Jitters Remain

Oil prices rose strongly on better risk sentiment following the announcement that although there hadn’t been a debt-ceiling deal following talks between President Biden and House Speaker McCarthy, they had been “productive” and both sides said a default was off the table. Prices have retreated since then but are still higher over the session. The USD index is flat.

- WTI is up 0.3% to $72.24/bbl after reaching an intraday high of $72.62 earlier. Brent is 0.2% higher to $76.14 following a high of $76.53. WTI remains comfortably below key short-term resistance at $73.81, the May 10 high. And for Brent resistance is at $77.60.

- Increased expected US gasoline demand, refilling the US SPR, the IEA’s expected crude deficit, and reduced OPEC output with possibly more announced at the June meeting are all supporting prices. On the other hand uncertainty over China’s economy, further Fed hikes, robust Russian supply and the debt-ceiling impasse have been weighing on the market.

- The immediate outlook for oil prices is highly dependent on debt-ceiling talks. See Debt: No Agreement Yet, But Talks Continue for today’s developments.

- The Saudi Arabian energy minister is due to speak at the Qatar Economic Forum today. Also API weekly US fuel inventory data prints. Later the Fed’s Logan gives welcoming remarks and preliminary May PMIs, May Richmond Fed business confidence and April US new home sales are released.

GOLD: Weighed Down By Debt Ceiling Stand Off & Fedspeak

In Asia-Pacific trade, gold has declined by 0.4% to reach 1963.15, following a modest drop of 0.3% to 1971.86 during Monday's trading session. Investors are carefully evaluating the ongoing US debt-ceiling standoff and the remarks from Federal Reserve officials, which have contributed to the cautious sentiment surrounding gold.

- A deal is one step closer following talks between President Biden and House Speaker McCarthy which has finished. Comments from McCarthy indicate that the meeting was “productive” and that the tone of discussions had improved.

- Given the uncertainties surrounding the debt-ceiling X-date, it is expected that gold trading will continue to be volatile unless a resolution is reached.

- Despite Federal Reserve Chair Powell's recent comments indicating a potential pause, market expectations for a 25bp interest rate hike at the upcoming FOMC meeting in June are slowly rising, currently reaching 22%. This sentiment was reinforced by overnight statements from Fed Bullard, a non-voting member for 2023, who voiced support for two more 25bp rate increases. Additionally, Fed Kashkari, a voting member for 2023, hinted at his preference for further tightening of monetary policy.

- According to a Bloomberg article, gold appears to be in the throes of a triple top, setting up a substantial correction in the coming months. (link)

RBNZ Dated OIS - Expected Terminal OCR Moves To A New High

RBNZ dated OIS pricing is 3-11bp firmer across meetings ahead of tomorrow’s RBNZ policy meeting. Pricing has shunted firmer over recent days, following a more stimulatory than expected NZ budget.

- With a fiscal impulse moving into positive territory next year, pricing has firmed 8-34bp across meetings post-budget with early ’24 leading.

- 36bp of tightening is priced for tomorrow’s RBNZ meeting.

- Terminal rate expectations are at a new cycle high of 5.93%.

Figure 1: RBNZ Dated OIS Terminal Rate Pricing (%)

Source: MNI – Market News / Bloomberg

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 23/05/2023 | 0600/0700 | *** |  | UK | Public Sector Finances |

| 23/05/2023 | 0715/0915 | ** |  | FR | S&P Global Services PMI (p) |

| 23/05/2023 | 0715/0915 | ** | | FR | S&P Global Manufacturing PMI (p) |

| 23/05/2023 | 0715/0915 |  | EU | ECB de Guindos Address at European Financial Integration Conf | |

| 23/05/2023 | 0730/0930 | ** |  | DE | S&P Global Services PMI (p) |

| 23/05/2023 | 0730/0930 | ** | | DE | S&P Global Manufacturing PMI (p) |

| 23/05/2023 | 0800/1000 | ** | | EU | EZ Current Account |

| 23/05/2023 | 0800/1000 | ** | | EU | S&P Global Services PMI (p) |

| 23/05/2023 | 0800/1000 | ** | | EU | S&P Global Manufacturing PMI (p) |

| 23/05/2023 | 0800/1000 | ** | | EU | S&P Global Composite PMI (p) |

| 23/05/2023 | 0830/0930 | *** | | UK | S&P Global Manufacturing PMI flash |

| 23/05/2023 | 0830/0930 | *** | | UK | S&P Global Services PMI flash |

| 23/05/2023 | 0830/0930 | *** | | UK | S&P Global Composite PMI flash |

| 23/05/2023 | 0900/1000 | * | | UK | Index Linked Gilt Outright Auction Result |

| 23/05/2023 | 0915/1015 | | UK | BOE Bailey, Pill, Tenreyro, Mann at MPR Hearing | |

| 23/05/2023 | 1230/0830 | * |  | CA | Industrial Product and Raw Material Price Index |

| 23/05/2023 | 1230/0830 | ** |  | US | Philadelphia Fed Nonmanufacturing Index |

| 23/05/2023 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 23/05/2023 | 1300/0900 | | US | Dallas Fed's Lorie Logan | |

| 23/05/2023 | 1345/0945 | *** | | US | IHS Markit Manufacturing Index (flash) |

| 23/05/2023 | 1345/0945 | *** | | US | S&P Global Services Index (flash) |

| 23/05/2023 | 1400/1000 | *** | | US | New Home Sales |

| 23/05/2023 | 1400/1000 | ** | | US | Richmond Fed Survey |

| 23/05/2023 | 1445/1545 | | UK | BOE Haskel Panellist at Richmond Fed Conference | |

| 23/05/2023 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 23/05/2023 | 1700/1300 | * | | US | US Treasury Auction Result for 2 Year Note |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.