Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Regional equity sentiment has been weaker, weighed by Hong Kong market losses. This has lent some support to the USD, but overall moves have been modest.

- US Tsy ranges have been very tight and we trade near overnight lows. The minutes from the May 7 RBA meeting noted that the data had come in “stronger than expected” but it decided to look through short-term developments to “avoid excessive fine-tuning”. ACGBs are cheaper but away from session lows.

- The RBNZ meets tomorrow and will also release updated staff forecasts and hold a press conference. It is unanimously expected to leave rates at 5.5% as it is yet to be confident that inflation will sustainably return to target. We don't expect the tone of the statement or the updated projections to be significantly changed with guidance that “a restrictive monetary policy stance remains necessary” retained.

- Later the Fed’s Barkin, Waller, Williams, Bostic and Barr and BoE’s Bailey speak. US Philly Fed non-manufacturing for May and Canadian April CPI print.

MARKETS

US TSYS: Treasury Futures Trade Steady Ahead Of Busy Day Of Fed Speaker

- Ranges have been very tight and we trade near overnight lows. The 2Y contract is unchanged at 101-21.375, while the 10Y contract is (- 02) at 109-01.

- Volumes: TU 30k, FV 39k, TY 60k

- Tsys Flows: Block seller of 1.8k FV, Block Steepener 9k TU | 2.5k US

- Looking at technicals, support holds at 108-27+/108-15 (50-day EMA / May 14 low), while resistance holds at 109-31+ (May 16 high)

- The treasury curve is slightly steeper today, yields are flat to 1.5bps lower, the 2Y yield is -1.3bps at 4.835%, 10Y -0.2bp to 4.441%, while the 2y10y +1.093 at -39.783

- Looking across APAC rate markets: ACGBs are 1.5-2bps higher, NZGBs flat to 2.5bps higher, curve is steeper, JGBs yields are flat to 1bps higher

- Rate cut projections have receded vs. this morning's levels (*): June 2024 at -5% w/ cumulative rate cut -1.2bp at 5.318%, July'24 at -20% w/ cumulative at -6.3bp (-7.5bp) at 5.267%, Sep'24 cumulative -19.6bp (-20.9bp), Nov'24 cumulative -27.1bp (-29bp), Dec'24 -41.5bp (-43.9bp).

- Busy day ahead for fed speakers with Barkin, Waller, Williams, Collins, Bostic & Barr all speaking

JGBS: Cash Bonds Little Changed, 40Y Supply Tomorrow

JGB futures are unchanged compared to the settlement levels and sit in the middle of today's range.

- There hasn’t been much in the way of domestic drivers to flag. April Tokyo condominiums for sale are on tap later.

- After yesterday’s modest sell-off, cash US tsys have slightly bull-steepened in today’s Asia-Pac session. The US data calendar is light until mid-week. The focus is on the minutes from the May 1 FOMC on Wednesday.

- Cash JGBs are slightly mixed, with yield movements bounded by +/- 0.7bp. The benchmark 10-year yield is 0.1bp lower at 0.980% after reaching 0.984% earlier, its highest level since 2013, on speculation of further BoJ rate hikes and reduced debt-purchase amounts at operations.

- The breakeven inflation rate for the 10-year CPI-linked bonds rose 2bps to 1.644%.

- The swaps curve has twist-flattened, pivoting at the 3s, with rates 0.4bp higher to 1bp lower. Swap spreads are mixed.

- Tomorrow, the local calendar sees Trade Balance and Core Machine Orders alongside 40-year supply.

RBA: Inflation Risks “Risen Somewhat”, RBA Seems Firmly On Hold

The minutes from the May 7 RBA meeting noted that the data had come in “stronger than expected” but it decided to look through short-term developments to “avoid excessive fine tuning”. As a result, the Board decided to leave rates unchanged but as Governor Bullock said in the press conference a hike was discussed. While the “risks around inflation had risen somewhat”, the general tone of the minutes was neutral demonstrating a strong desire to hold rates thus the bar remains high for a move in either direction.

- The downside risks to growth offset the upside ones to inflation. There is significant uncertainty and the path back to target is unlikely to be “smooth” and so the RBA is on hold for now as it is “difficult to rule in or rule out future changes in the cash rate”.

- A hike was discussed due to the stronger-than-expected inflation and labour data. There was also concern that the assumptions around the projection that inflation returns to target by end-2025 were “overly optimistic”. The risk that consumption picked up more than expected driven by the labour market, real incomes and wealth was also discussed. The risk to achieving target from slow productivity with high wages growth was also mentioned.

- The policy hold was determined from the “balanced set of risks around the central forecasts” and inflation’s return to target as previously expected. It was also deemed to be appropriate if demand proved softer than expected or if the labour market is already “close to full employment”.

- See minutes here.

AUSTRALIAN DATA: Consumers Pessimistic, Budget “Relatively Well-Received”

Westpac consumer confidence for May fell 0.3% m/m to 82.2, the third straight fall. Households continue to remain extremely pessimistic. The response followed the May 7 RBA meeting and its upward revision to 2024 inflation and the May 14 budget which included cost-of-living relief which Westpac says was “relatively well-received”. The data signal that consumption is likely to stay very weak with most of the upcoming tax cuts being saved.

- Inflation remains household’s main concern and as a result over half expect rate hikes to resume over the next year due to the higher-than-expected Q1 CPI and more hawkish sounding RBA. Rate hike fears eased post the budget despite being stimulatory.

- Before the budget sentiment was up 5.3% m/m whereas afterwards responses were down 7.4% more in reaction to the soft economic outlook rather than the fiscal measures, according to Westpac. Normally a net 20-25% believe they will be worse off after the budget, whereas this year it was only 3%, the lowest in 14 years ex Covid. 18% expect to benefit.

- 37% of those surveyed expect to pay less tax from July 1 with 27% expecting no impact. Of those anticipating a tax cut, 30% plan to save all of it and 50% at least half. Westpac estimates that around 80% will be saved, which would boost spending by 0.35pp.

- Current assessments of finances and the economy deteriorated offsetting the better outlook.

- The “time to buy a major item” fell 2.8% m/m to 76.5. It is rare to sit below 80.

- Unemployment expectations rose 4.1% to be just above the historical average driven by NSW and Victoria.

- Households continue to say it is a terrible time to buy a house while expecting well-above -average price rises.

Source: MNI - Market News/Refinitiv

AUSSIE BONDS: Cheaper But Off Worst Levels, Jun-54 Supply Tomorrow

ACGBs (YM -2.0 & XM -2.0) sit cheaper but off session cheaps.

- The minutes from the May 7 RBA meeting noted that the data had come in “stronger than expected” but it decided to look through short-term developments to “avoid excessive fine-tuning”.

- As a result, the Board decided to leave rates unchanged but as Governor Bullock said in the press conference a hike was discussed. While the “risks around inflation had risen somewhat”, the general tone of the minutes was neutral demonstrating a strong desire to hold rates thus the bar remains high for a move in either direction.

- (MNI) The RBA will need to alter its forecasts for inflation and employment should its key assumptions on consumption growth, labour market capacity or price rise prove overly optimistic, according to the recently published minutes from the May meeting. (See here)

- Cash ACGBs are 2bps cheaper, with the AU-US 10-year yield differential at -19bps.

- Swap rates are 1-2bps higher.

- The bills strip is cheaper, with pricing -2.

- RBA-dated OIS pricing is 3-4bps firmer for meetings beyond August. A cumulative 10bps of easing is priced by year-end off an expected terminal rate of 4.34%.

- Tomorrow, the local calendar is empty apart from the AOFM's planned sale of A$300mn of 4.75% Jun-54 bond.

RBNZ: MNI RBNZ Preview – May 2024: Policy To Stay Restrictive

- The RBNZ meets on May 22 and will also release updated staff forecasts and hold a press conference. It is unanimously expected to leave rates at 5.5% as it is yet to be confident that inflation will sustainably return to target. We don't expect the tone of the statement or the updated projections to be significantly changed with guidance that “a restrictive monetary policy stance remains necessary” retained.

- Given elevated non-tradeables inflation, the MPC will likely still want to see a couple of quarters of CPI data to determine if domestic price pressures have eased sufficiently. With Q3 CPI not released until October 16 and only one meeting left before year end thereafter, it looks like the RBNZ’s prolonged hold will continue through this year.

- The pricing level of 5.51% for the May meeting also represents the anticipated terminal OCR. By year-end, a cumulative 45bps of easing is factored into the pricing.

- See full preview here.

NZGBS: Closed Slightly Cheaper Ahead Of The RBNZ Policy Decision

NZGBs closed flat to 2bps cheaper but around the session’s best levels ahead of tomorrow’s RBNZ Policy Decision. Updated staff forecasts will also be released.

- The RBNZ is unanimously expected to leave rates at 5.5% as it is yet to be convinced that inflation will sustainably return to target. We don't expect the tone of the statement or the updated projections to be significantly changed with guidance that “a restrictive monetary policy stance remains necessary” retained.

- Given elevated non-tradeables inflation, the MPC will likely still want to see a couple of quarters of CPI data to determine if domestic price pressures have eased sufficiently. With Q3 CPI not released until October 16 and only one meeting left before year end thereafter, it looks like the RBNZ’s prolonged hold will continue through this year. (See full preview here)

- Swap rates closed 1bp lower to 1bp higher, with the 2s10s curve steeper.

- RBNZ dated OIS pricing closed little changed across meetings. There's a 7% probability priced in for a 25bp hike at tomorrow’s meeting.

- The pricing level of 5.52% for the May meeting also represents the anticipated terminal OCR. By year-end, a cumulative 45bps of easing is factored into the pricing.

FOREX: Dollar Modestly Higher, Weaker Commodities/Lower Equities Weigh On A$

The USD BBDXY index sits higher in the first part of Tuesday trade. We were last near 1247.5 (+0.10% firmer), slightly off session highs just above 1248.0.

- USD gains have been fairly uniform and broad based, albeit modest at this stage. USD/JPY was last around 156.50, this is close to session highs. We aren't too far away from May 14 highs at 156.74.

- AUD/USD is back to 0.6655/60, off close to 0.2%. We have seen some retracement in commodity prices from recent frothy levels, which has likely weighed at the margins. Regional equities are also mostly weaker, led by Hong Kong markets. The RBA mins didn't offer any great surprises relative to policy outcome earlier in May.

- NZD/USD has also weakened last under 0.6100.

- US Tsy futures sit off session highs, but have tracked tight ranges overall. Cash Tsy yields are little changed.

- Later the Fed’s Barkin, Waller, Williams, Bostic and Barr and BoE’s Bailey speak. US Philly Fed non-manufacturing for May and Canadian April CPI print.

ASIA STOCKS: HK & China Equities Head Lower, Tech Forms Double Top

Hong Kong & Chinese equities are lower today, equities are being dragged lower following Li Auto's 19% drop after weaker-than-expected first quarter results, Tech is lower after Tencent shut down new game DNF Mobile within an hour of debut with the HSTech index forming a doble top and now on track for the worst day in this month, while property indices are holding up slightly better than the wider markets. There is little in the way of market data today, focus will turn to FOMC minutes on Wednesday.

- Hong Kong equities are lower today, property is holding up slightly better than the wider markets with the Mainland Property Index down just 1.60% although the Hang Seng Property Index is down 1.79%, the HSTech Index is down almost 3.20%, while the HSI is down 2.05%. In China onshore markets, the CSI300 is trading down 0.40% while the small-cap indices CSI1000 & CSI2000 are down 0.80%, while the ChiNext is down 0.62%

- In the property space, China Vanke is securing more bank loans to enhance liquidity while awaiting government support for builders, the company applied for a 1.2 billion yuan loan from Bank of China for a development project in Changzhou

- Li Auto Inc.'s first-quarter vehicle sales fell short of analyst estimates, with sales reaching 24.25 billion yuan ($3.4 billion) against an expected 26.71 billion yuan. Net income was 1.3 billion yuan, below the forecasted 1.6 billion yuan. The company delivered 80,400 vehicles, including the new MEGA van, whose tepid demand led to a revised delivery target of 76,000-78,000 units, down from 100,000-130,000. Li Auto faces increased competition and a price war in China's EV market. It expects second-quarter revenue of 29.9-31.4 billion yuan, below the forecasted 38.6 billion yuan, and deliveries of 105,000-110,000 units, versus an expected 130,692

- Looking ahead, quiet week for China on the data front

ASIA PAC STOCKS: Asian Equities Head Lower As Investors Take Profit

Asia markets are lower today as investors look to take profits. Japan opened higher following moves made overnight in the US markets, however we have since reversed all those gains as corporate earnings weigh on the tech sector, metals prices continue to edge higher and trade near all-time-highs helping miners, while the Chinese property sector sold off heavily on concerns recent policy announcements will be enough to support the sector, the MSCI Asia Pacific is trading down 0.70%. There was little in the way of economic data in the region today, although the RBA released minutes from their May policy meeting where they resumed a discussion of interest rate hikes.

- Japanese equities opened higher this morning, following moves made in US markets overnight and insurers rose after positive earnings outlooks and buyback announcements, however we have since pared gains and now trade little changed. The Nikkei 225 is down 0.02%, while the Topix is up 0.06%.

- South Korean equities are lower today as local tech stocks slide, Samsung is the largest contributed to the loss. There is little on the calendar today, with PPI and Business Survey Manufacturing due out tomorrow, while focus will be on the BOK Thursday. The Kospi is trading down 0.65%, while the small-cap Kosdaq is down 0.18%.

- Taiwan equities are slightly lower today, regional tech prices are lower which is leading to the weakness in the local market. This week we have the unemployment rate due out tomorrow and Industrial Production on Thursday. The Taiex is down 0.20%.

- Australian equities are lower today, focus has been on the RBA minutes where they discussed interest-rate hikes and that inflations risks had risen somewhat. Financials and Materials are the worst performing sectors, offsetting gains in Consumer Discretionary, Industrials and Tech, the ASX200 is down 0.05%

- Elsewhere in SEA, New Zealand equities are down 0.42%, Singapore equites are down 0.38%, Indonesian equities are down 0.55%, Philippines are down 0.75% & Malaysian equities are down 0.24%.

OIL: Crude Lower On Weaker Risk Sentiment But Still In Recent Ranges

Oil prices have fallen driven by a general pullback in risk with commodities lower and HK equities down sharply. WTI is down 0.6% to $78.84/bbl close to the intraday low. Brent is 0.5% lower at $83.26 but continues to move in a narrow range. Recent geopolitical events have been overlooked by the market. The USD index is up 0.1%.

- Market signals are pointing to an easier crude outlook with the Brent prompt spread at its narrowest since January, according to Bloomberg. Other indications include money managers reducing their longs and the reduction of refining margins.

- With the focus back on fundamentals, US inventory data is being watched closely. Later today the API sourced information will be released.

- Later the Fed’s Barkin, Waller, Williams, Bostic and Barr and BoE’s Bailey speak. US Philly Fed non-manufacturing for May and Canadian April CPI print.

GOLD: Pullback After Reaching A Fresh All-Time High

Gold is 0.5% lower in the Asia-Pac session, after closing 0.4% higher at $2425.31 on Monday. Earlier in yesterday’s session bullion hit a fresh all-time high of $2,450. There was no headline flow of note, with markets generally shaking off weekend political risk.

- China’s bullion imports slowed last month as demand in the world’s biggest consumer begins to buckle in the face of record prices. Overseas purchases of physical gold fell to 136 tons in April, a 30% decline from the previous month and the lowest total for the year, according to the latest customs data (BBG).

- Having traded through resistance at $2431.5 (the Apr 12 high and bull trigger), the focus turns to 2452.5, a Fibonacci projection, according to MNI's technical team.

- Meanwhile, silver outperformed again yesterday, with its price hitting the highest level since end-2012.

- Sights are on $33.887 next for silver, a Fibonacci projection. Short-term pullbacks would be considered a correction. A key support zone lies between $27.229-36.948, the 20- and 50-day EMA values.

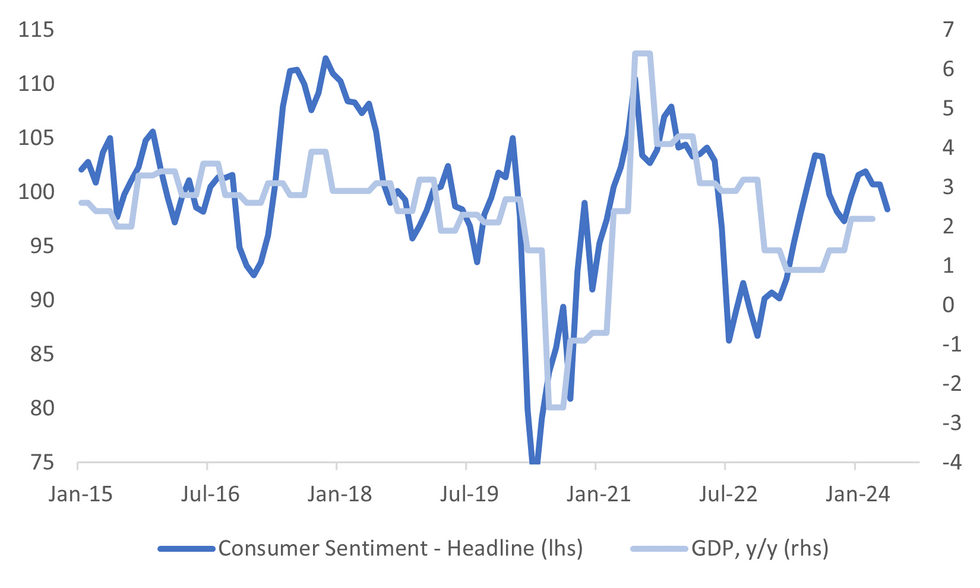

SOUTH KOREA DATA: Headline Consumer Sentiment Index Dips, Inflation Expectations Nudge Higher

Earlier data showed headline consumer confidence dipped further in May to 98.4 (from 100.7 in April). This is back to around October 2023 levels and for the first time since December last year, pessimists outweigh optimists in terms of the headline reading. More broadly, sentiment is within ranges and while it isn't suggesting further upside in GDP growth, it also isn't suggesting a sharp deceleration either, see the first chart below.

- Nevertheless, the result likely underscores the need for easier policy settings from a domestic standpoint. They may not be forthcoming in the near term though with the BoK widely expected to stay on hold this Thursday.

- Most of the sub-indices dipped in relation to the domestic economy and spending intentions. Consumers also became more pessimistic around the chance of rate cuts from the BoK.

Fig 1: South Korea CSI Headline Versus GDP Y/Y

Source: MNI - Market News/Bloomberg

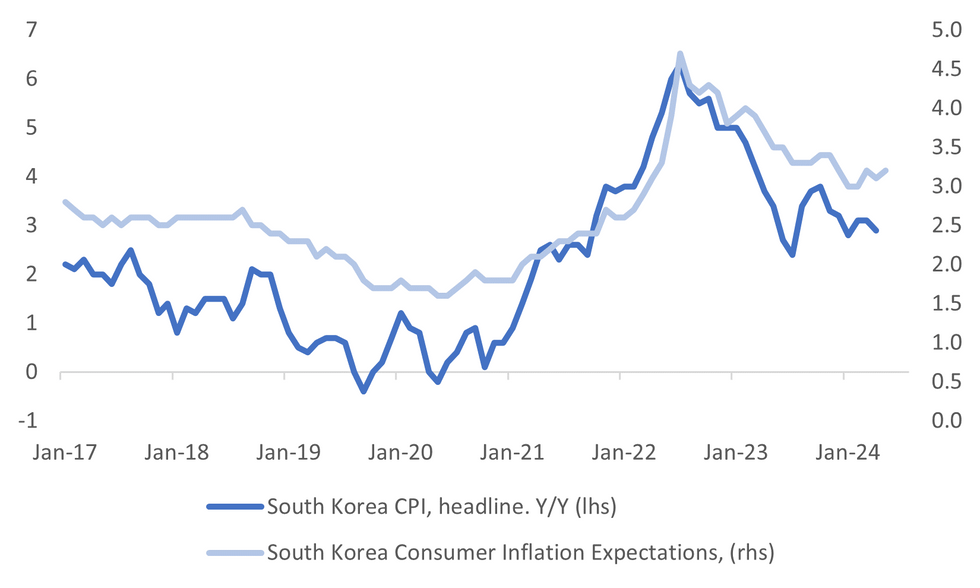

- Also noteworthy was the pick up in inflation expectations. This rose to 3.2% from 3.1% last month. While only a marginal increase, expected inflation hasn't been able to break sub 3% on the downside.

- This index and headline CPI show somewhat of a wedge, see the second chart below. At the margin this adds to the on hold case for the BoK at this week's policy meeting.

Fig 2: South Korea CPI Y/Y & Consumer Inflation Expectations

Source: MNI - Market News/Bloomberg

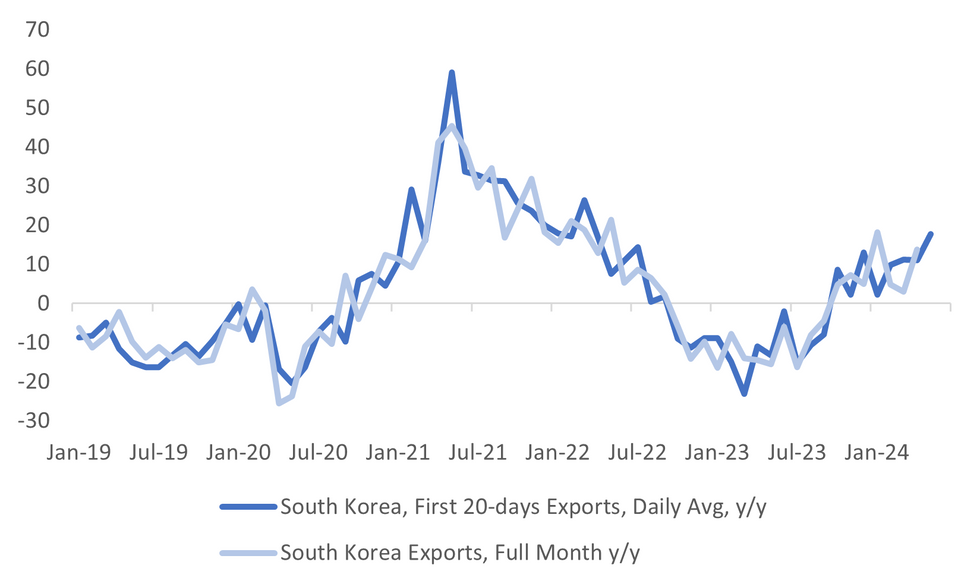

SOUTH KOREA DATA: First 20-Day Export Y/Y Momentum Slows, But Detail Suggests Continued Recovery

South Korea's first 20-days of trade data for May showed slower momentum versus the equivalent April outcome. Headline exports were +1.5% y/y, versus 11.1% prior, while imports fell to -9.8% y/y from +6.1% prior. The trade deficit was $304mn.

- The detail painted a more upbeat picture though. Average daily exports for the first 20-days were up 17.7% y/y. This compares with +11.1% for the first 20-days of April. The chart below shows this metric against full month export growth. It paints a positive underlying trend for the export recovery.

- Recall in May the Labor Day holiday, as well as other holidays, which may have had an impact.

- Note export growth to China eased back to +1.3% y/y from 9.0% in April. Exports to the US also slowed to 6.3%, from 22.8%.

- By product chip exports remained very robust up 45.5% y/y for the first 20-days (prior was +43% y/y).

Source: MNI - Market News/Bloomberg

ASIA FX: KRW & THB Weaken, CNH Outperforms

Most USD/Asia pairs are higher, albeit to varying degrees. USD/CNH has bucked the broader trend and sits slightly lower, unable to break above 7.2500. The won and the baht have seen the sharpest falls in spot terms. Regional equity sentiment is weaker, led by Hong Kong. Tomorrow, we have the South Korean PPI and business sentiment up first. Later on, the BI decision is due with no change expected by the consensus.

- USD/CNH looked set to test above 7.2500, while spot onshore pushed above 7.2400. However, sentiment has stabilized since then. USD/CNH last around 7.2430/40. The earlier USD/CNY fixing rose modestly but was still the highest result since late Feb this year. The weaker HK/mainland equity tone is not helping. Recent data suggested strong capital outflow pressures in April, which is likely weighing in the background, although it may also be keeping the authorities on gaurd against fresh depreciation pressures.

- 1 month USD/KRW got through Monday highs, pushing to a high of 1365. We sit slightly lower in recent dealings last near 1362. We had earlier resilient export figures for the first 20-days of May, but his hasn't done much for sentiment. The weaker regional equity tone, coupled with lower JPY and CNY levels are working the other way so far today.

- USD/THB has rebounded sharply so far today. The pair last near 36.30. Intra-session lows from Monday trade came in at 35.845 post firmer than expected Q1 GDP results. Broader USD sentiment has weighed on the baht and we have seen some recent outperformance unwound today. The Thailand government is considering a supplementary budget soon (up to 122bn baht) to aid the economic backdrop.

- USD/PHP has risen above 58.00 for the first time since 2022. This figure level was eyed as a potential resistance point (particularly from an intervention standpoint), so we may be seeing some technical/stop related buying after piercing this level. The pair was last 58.10/15, 0.40% weaker in PHP terms.

- USD/IDR is around 0.30% firmer. The pair was last near 16020, slightly off session highs. Again, this is well within May ranges to date, but IDR is displaying reasonable beta with respect to USD/Asia moves.

INDONESIA: INDON Sov Curve Steepens Ahead Of BI Decision

The INDON sov curve has bear-steepened today. Calendar is empty today, as we await the BI rate decision on Wednesday, the market expected rates to be left on hold tomorrow after the surprise 25bps rise last month, the USDIDR is up 0.30% and holds above 16,000.

- The INDON curve has bear-steepened today, yields are 1-3bps higher, the 2Y yield is 1bp higher at 5.255%, 5Y yield is 1.5bp higher at 5.07%, the 10Y yield is 2.5bps higher at 5.16%, while the 5-year CDS is 0.5bp higher at 70.5bps.

- The INDON to UST spread diff the 2Y is now 42bps (unchanged), 5yr is 61bps (-1bps), while the 10yr is 72bps (Unchanged).

- In cross-asset moves, USD/IDR is up 0.30% at 16,004, the JCI is down 0.53% Palm Oil is 0.51% higher, while US tsys yields are flat to 1.5bps higher.

- BI Rate decision tomorrow - Bank Indonesia is expected to keep its key rate at 6.25% following last month's unexpected rate hike. The rupiah, down 3.6% against the dollar this year, has recovered some losses after April's decline. BI's tightening aims at rupiah stability rather than curbing domestic demand. Despite inflation at 3.0% in April, above BI's target range, rising oil, food, and shipping costs suggest that tight policy will continue through the summer.

- Looking ahead; Bank Indonesian rate decision on Wednesday

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 21/05/2024 | 0600/0800 | ** |  | DE | PPI |

| 21/05/2024 | 0800/1000 | ** |  | EU | Current Account |

| 21/05/2024 | 0900/1100 | ** | | EU | Construction Production |

| 21/05/2024 | 0900/1100 | * | | EU | Trade Balance |

| 21/05/2024 | 0900/1000 | ** |  | UK | Gilt Outright Auction Result |

| 21/05/2024 | 1000/1100 | ** | | UK | CBI Industrial Trends |

| 21/05/2024 | 1230/0830 | *** |  | CA | CPI |

| 21/05/2024 | 1230/0830 | ** |  | US | Philadelphia Fed Nonmanufacturing Index |

| 21/05/2024 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 21/05/2024 | 1300/0900 | | US | Fed Governor Christopher Waller | |

| 21/05/2024 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 21/05/2024 | 1545/1145 | | US | Fed Vice Chair Michael Barr | |

| 21/05/2024 | 1700/1800 | | UK | BOE's Bailey Lecture at LSE | |

| 21/05/2024 | 2300/1900 | | US | Atlanta Fed's Raphael Bostic | |

| 21/05/2024 | 2300/1900 | | US | Cleveland Fed President Loretta Mester |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.