Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- The underlying risk tone was negative for most of the Asia-Pac session, with U.S. e-minis losing altitude as the session progressed, after Wednesday's poor showing from benchmark indices on Wall Street. However, risk assets got some reprieve from a BBG report flagging debates among Chinese officials on whether to reduce the mandatory quarantine period for inbound travellers, stressing that any such decision would have to be cleared by senior leaders.

- Core FI markets looked through the report re: Chinese quarantine matters, but were biased lower, with the BoJ once stepping in to defend its YCC parameters via unscheduled Rinban operations.

- Data highlights going forward include U.S. jobless claims, existing home sales & Philly Fed Biz. Survey. Elsewhere, Fed's Harker, Jefferson, Cook & Bowman, ECB's de Cos & Norges Bank's Bache will speak.

US TSYS: Light Cheapening Overnight

TYZ2 deals -0-04 at 109-28, operating 0-02 off the base of its narrow 0-06 overnight range, on volume of ~86K. The contract has registered a fresh cycle low, with the nearby 30 Nov ’07 low (109-23+) providing the next level of technical support for bears to target. Cash Tsys sit ~1bp cheaper across the curve.

- Tsys held a modest cheapening bias in Asia-Pac hours, as regional participants reacted to Wednesday’s sell off, registering fresh cycle highs for yields across the curve in the process.

- It wasn’t all one-way in flow terms, with softer than expected Australian headline job growth and a small block buy in WN futures (+750) helping to support the space at one point.

- Note that we also saw block sellers of TY futures (-1.5K & 01.4K) during Asia-Pac hours.

- Tsys have looked through a BBG source report which suggested that “Chinese officials are debating whether to reduce the amount of time people coming into the country must spend in mandatory quarantine.” Those headlines generated a light bid for oil, e-minis & the Chinese yuan, within broader risk-on flows, pulling e-minis away from worst levels of the day alongside a bid in Chinese & HK equities.

- Chicago Fed President Evans provided the now standard hawkish Fed rhetoric.

- Thursday’s NY docket will see the release of the latest Philly Fed survey, weekly jobless claims and existing home sales data. We will also get 5-Year TIPS supply and Fedpseak from Bowman, Jefferson, Cook & Harker.

JGBS: Unscheduled BoJ Fails To Provide Meaningful Support

The major benchmark JGBs have seen a mixed afternoon, with super-long paper recovering from lows, leaving wider cash JGBs little changed to ~2bp cheaper on the day. 7s and 20s provide the weakest points on the curve (tied to a move lower in futures & potential structural demand issues, respectively), while 2s and 10s are little changed, with the latter of course limited by the presence of the BoJ’s YCC scheme. 30+-Year paper is nearly back to flat, perhaps on fresh interest from lifers and pension funds, which seemed to become apparent on Wednesday afternoon as well.

- Futures print -30, at worst levels of the session, and 25 ticks off September’s low, where initial technical support lies. A break there would expose levels not seen since June, when the BoJ’s will re: its YCC scheme was being tested.

- The show higher in yields triggered an unscheduled round of 5- to 25+-Year BoJ Rinban operations (as we suggested may be the case). However, this did little to placate the market, with 10-Year JGB yields immediately showing above the upper limit of the range permitted under the BoJ's YCC (per BBG), while JGB futures nudged lower in the wake of the announcement.

- Tomorrow’s local docket will see the release of national CPI data & 1- to 10-Year BoJ Rinban operations.

AUSSIE BONDS: Bear Flattening Holds

A shift higher in RBA terminal rate pricing & payisde flow in swaps, which was linked to Wednesday’s move in the likes of Fed & BoC pricing, applied further pressure to ACGBs in Sydney trade, which allowed the space to extend on the weakness seen in futures during the overnight session.

- That leaves YM & XM -13.0 apiece on the day into the bell, a little off of worst levels, with bear flattening observed on the wider cash ACGB curve, where 11-13bp of cheapening was seen across the major benchmarks.

- The latest round of labour market data saw a brief bid come in, with less than 1K of jobs added in September (vs. BBG median of +25K), while the unemployment rate and participation rates held steady, matching expectations. A reminder that leading labour market indicators have flagged a slight colling in the labour market, although vacancies have stuck at elevated levels.

- The space looked through the latest BBG source piece re: a potential trimming of the Chinese COVID quarantine for international travellers.

- Bills run 3-17bp cheaper through the reds, with RBA dated OIS pricing a terminal rate of ~4.25%.

- A$700mn of ACGB Apr-25 supply and the release of next week’s AOFM issuance slate headline the domestic docket on Friday.

AUSTRALIA: Tight Conditions Weigh On Jobs, Shouldn’t Change RBA Thinking

Employment rose 0.9k in September which was below the lower end of expectations of +10k but August was revised up to 36.3k from 33.5k). The unemployment rate was stable at 3.5%, as expected, and so was the participation rate at 66.6%. The details, however, point to labour shortages continuing to transition people from part-time jobs (-12.4k) to full-time jobs (+13.3k). As a result, this data is unlikely to change the RBA’s +25bp thinking.

- Hours worked fell by 0.2%m/m for employed full-time persons due to a higher-than-usual number of people taking annual leave in September for the school holidays compared to the previous 2 years which were Covid affected.There was also a 14% increase in people working fewer hours due to illness. Hours worked in all jobs were flat on the month.

- The underemployment rate was also steady at 6% down from 6.6% at the start of the year. While underutilisation rose 0.1pp to 9.6% (10.8% in January). The number of unemployed rose 8.8k but the series is still down 21%y/y and showing negative 3-month momentum.

- While the vacancies-to-unemployment ratio appears to have peaked, it remains extremely high implying that employment gains should continue, even if at a more moderate pace because firms continue to find suitable candidates scarce.

Source: MNI - Market News/ABS

Fig 2: ANZ Vacancies-to-unemployment ratio %

Source: MNI - Market News/ANZ/Refinitiv/ABS

AUSTRALIA: Advertised Salaries Point To Contained Wage-Setting Psychology

SEEK advertised salaries for September showed continued growth up 0.3%m/m and 3.7%y/y. This has moderated from August’s 0.4% and 3.9% signalling that inflation and wage-setting psychology has not shifted significantly. The information from this report will be a relief to the RBA and validate its 25bp per meeting rate path.

- This data also shows that even advertised salaries are not keeping up with inflation and so workers continue to face falling pay packets in real terms, which is already depressing consumer confidence and may eventually weigh on spending too.

- It also suggests that growth in the official wages data should pick up again in Q3 but may peak around the turn of the year (see chart).

- Advertised salary growth is off of its mid-year peak of 4.4%. But it is worth noting that to 2-decimal places September’s monthly rise is almost the same as August’s at 0.34% versus 0.35%. Also both the 3-month and 6-month measures of momentum are trending higher.

- Strong monthly gains in Q3 last year are weighing on the current annual growth rate in SEEK advertised salaries.

Source: MNI - Market News/ABS/SEEK

NZGBS: Off Lows As Swaps Reverse & Longer Dated NZGB Supply Is Well Received

NZGBs peeled away from session cheaps on Thursday, after initially cheapening on spill over from Wednesday’s U.S. Tsy trade and concession into weekly NZGB supply.

- The weekly NZGB auctions (covering NZGB May-28, Apr-33 & May-51) saw firm demand for the two longer bonds, with cover ratios of 4.41x & 3.44x, respectively, while the shortest bond on offer saw more muted demand, registering a cover ratio of 1.20x, with worries re: more aggressive RBNZ tightening probably limiting demand there.

- Benchmark NZGBs, finished 2.5-9.0bp cheaper on the day, with bear flattening in play.

- Swaps fully reversed their early push higher into the bell, resulting in swap spread tightening across the curve.

- This came alongside a pullback in terminal RBNZ OCR pricing in the dated OIS strip, which moved from as high as ~5.50% at one point, back to just below 5.40% into the close.

- Looking ahead, Friday will see the release of the monthly NZ trade balance data.

FOREX: Risk-Off Pattern Holds Despite Incremental Relief From Report On China Border Rules Debate

The underlying risk tone was negative, with U.S. e-minis losing altitude as the session progressed, after Wednesday's poor showing from benchmark indices on Wall Street. However, risk assets got some reprieve from a BBG report flagging debates among Chinese officials on whether to reduce the mandatory quarantine period for inbound travellers, stressing that any such decision would have to be cleared by senior leaders.

- The greenback benefitted from safe haven demand, with the BBDXY testing 1,350 as a result. The index wiped out gains in a knee-jerk reaction to the China story, but then gradually unwound the reaction move.

- Expected Gotobi Day flows and 10-Year JGB yield sitting above the 0.25% cap raised the risk of further gains for USD/JPY but the pair respected a very tight range, as risk aversion favoured the yen. Participants monitored the pair for signs of an intervention by Japanese officials on approach to the psychologically significant Y150 figure, which has held for now.

- Japanese officials stood their ground. The BoJ announced an unscheduled round of bon-buying in defence of its YCC framework, reaffirming its dovish bias. Elsewhere, FinMin Suzuki pledged readiness to act appropriately on excessive FX moves.

- The Antipodeans fell prey to the wider cautious mood, with losses facilitated by a weaker than expected Australian jobs report. Employment growth was meagre, but doesn't move the needle much for the RBA, as forward-looking indicators already pointed to a slower but still very tight labour market.

- The kiwi paced losses, confirming its sensitivity to swings in market sentiment. Selling pressure was amplified by the partial withdrawal of hawkish RBNZ bets. Meeting-dated OIS price ~78bp worth of tightening next month versus yesterday's peak of 91bp. NZD/USD has now fully erased gains registered after the strong Q3 CPI print earlier this week.

- USD/CNH showed above the upper end of the PBOC's permitted USD/CNY trading band (+/-2% from fixing mid-point) but failed to hold above there and retreated, extending losses to new session lows as the aforesaid BBG report crossed the wires.

- Data highlights going forward include U.S. jobless claims, existing home sales & Philly Fed Biz. Survey. Meanwhile Fed's Harker, Jefferson, Cook & Bowman, ECB's de Cos & Norges Bank's Bache will speak.

FX OPTIONS: Expiries for Oct20 NY cut 1000ET (Source DTCC)

- EUR/USD: $0.9685-00(E1.9bln), $0.9750(E787mln), $0.9800(E1.9bln), $0.9850(E1.3bln), $0.9870-80(E $0.9990-00(E1.4bln)

- USD/JPY: Y145.00($3.5bln), Y147.90-00($3.7bln)

- GBP/USD: $1.1145-60(Gbp606mln)

- EUR/JPY: Y146.00(E753mln)

ASIA FX: China Quarantine News Leaves USD/CNH Comfortably Off Highs

USD/Asia pairs are mostly higher, in line with a firmer USD tone against G10. USD/CNH is the exception, as headlines of a potential cutting of inbound Covid quarantine requirements has lifted sentiment this afternoon. USD/KRW and USD/TWD are also away from worse levels. Still to come is Taiwan export orders and the BI decision, see this link for more details. Tomorrow the focus will be on South Korea first 20 days trade data.

- USD/CNH spiked to 7.2800 in early trade but has spent much of the rest of the session trending lower. The extra kick came this afternoon on reports the China officials are considering cutting inbound covid quarantine to 7 days from the current 10, although this is yet to be presented to top leaders. The pair hit a low near 7.2350, but we are now back in a rough 7.2400/7.2500 range. Earlier the CNY fixing was the strongest on record relative to expectations, while the 1yr and 5yr LPR rates were left unchanged.

- USD/KRW 1 month found early selling resistance above 1436, but dips sub 1430 have been supported. Equities are still down 1% but away from worse levels.

- USD/TWD has cemented its break above 32.00 (last 32.15). Onshore equities are weaker and net equity outflows continue. The 1 month NDF is back to 32.11, away from recent highs near 32.20. The market expects -5% y/y dip in September export orders which print later.

- USD/INR has pushed above 83.00, last 83.15. This follows yesterday's +0.76% gain in the pair. The sharp moved followed resistance above 82.40 giving way. Onshore equities are weaker, down 0.20%, while onshore bond yields are +5bps in the 10yr to 7.50 for the session so far.

- USD/IDR is close to session highs, last near 15580, +0.50% for the session so far. Again, this is fresh highs back to early 2020. Bank Indonesia is expected to raise the 7-Day Reverse Repo Rate by 50bp, although analysts are split. Out of the 31 surveyed by Bloomberg, 19 are siding with the median estimate, 11 expect a 25bp move and 1 is forecasting a 100bp rate rise.

- Bangko Sentral ng Pilipinas vowed to "utilise other tools to respond to fluctuations in exchange rate," such as liquidity management measures, as it intervened in FX markets less than its peers. Assistant Gov Sicat said the central bank was trying to "smooth out excess daily volatility rather than defend any specific level or trend," even as PHP59 has provided a line in the sand for USD/PHP over the past three weeks.

- USD/MYR is just off session highs, last close to 4.7275. Malaysia will hold the 15th general election (GE15) on November 19, the Election Commission said after a special meeting in its headquarters on Thursday.

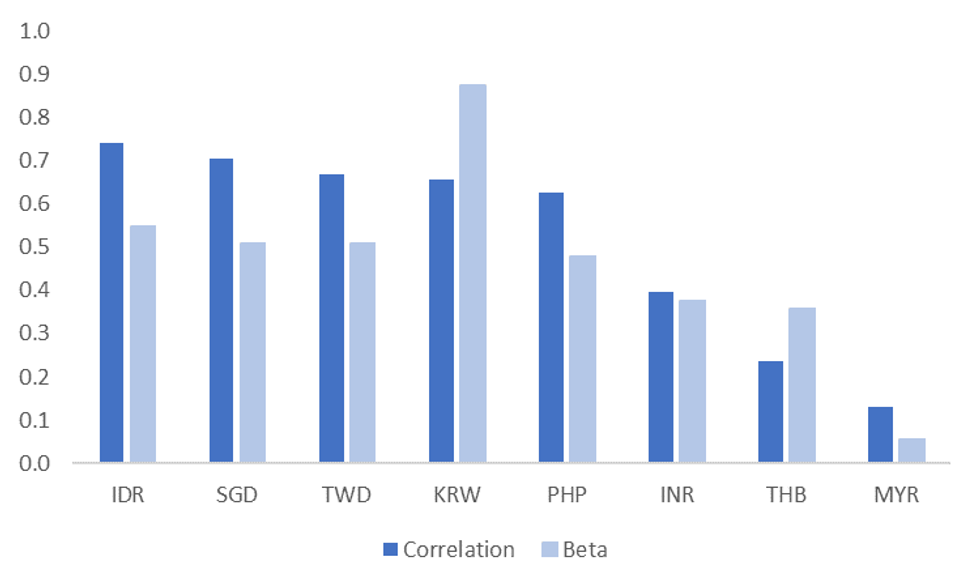

ASIA FX: Spill Over From Weaker CNH Levels Evident For Asia FX, Particularly KRW

Fresh record highs in USD/CNH can be expected to impart a spill over to other USD/Asia pairs, all else equal. The chart below plots the correlation and betas between CNH and other major Asian currencies for the past month. Note we utilize daily percentage changes to calculate the correlations and betas.

- Correlations are all positive, albeit to varying degrees. For the past month, USD/IDR, USD/SGD, USD/TWD, USD/KRW & USD/PHP all have correlations above 60%. Current correlations are lower for INR, THB & MYR.

- The betas present a similar story, sitting closely to 0.50 for those pairs with high correlations. USD/KRW is somewhat of a standout though, with a current beta of 0.875.

- Trade linkages between South Korea and China are obviously very strong, although the won may also be serving as somewhat of a proxy for China currency/economic weakness. This factor could be influenced by efforts to curb depreciation pressures on the part of the China authorities.

- Correlations for the past month are slightly above 2022 averages as well for nearly all USD/Asia pairs (except for USD/THB & USD/MYR).

Fig 1: USD/CNH & USD/Asia Correlations/Betas (Past Month).

Source: MNI - Market News/Bloomberg

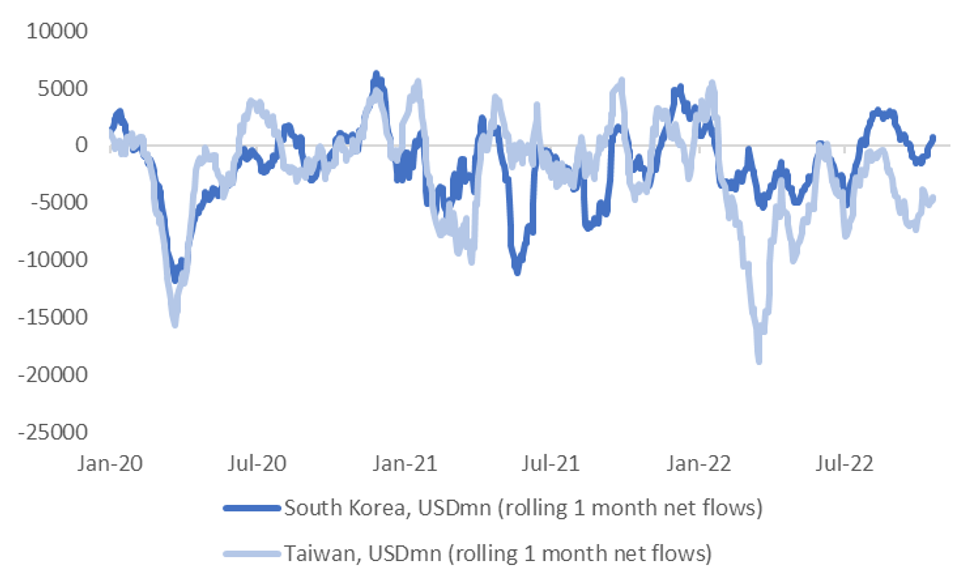

TWD: USD/TWD Cements Break Above 32.00, Equity Flows Diverge From South Korean Trends

USD/TWD is just off fresh cyclical highs above 32.16, last at 32.13. Resistance around the 32.00 level in spot has given way, although today's move in spot largely reflects catch up with the 1-month NDF, which pushed into the 32.15/20 range overnight (last 32.14). Early 2017 highs around 32.36 remain the upside target from a spot standpoint.

- Onshore equities are trading at fresh cyclical lows, with levels last seen in late 2020 (sub 12760 for the Taiex). The onshore financial regulator is moving to boost defences (see this link for more details).

- Offshore investors continue to unload local equities. The past month has seen close to $5bn in net outflows, see the chart below. Whilst this is away from 2022 trough points, monthly net inflow momentum has barely been positive this year.

- Taiwan's flow picture is also underperforming South Korea by a decent margin, which may reflect Taiwan's greater exposure to tech.

- Coming up later is September export orders. The market looks for a -5.0% y/y dip, versus +2.0% in August. The CBC Governor pointed to harder economic challenges in 2023 during a speech yesterday (see this link for more details).

Fig 1: Taiwan & South Korea Net Equity Flow Trends

Source: MNI - Market News/Bloomberg

MNI Bank Indonesia Preview - October 2022: A Close Call But 50bp Expected

EXECUTIVE SUMMARY:

- Bank Indonesia (BI) meets on October 20 and economists are projecting it to raise rates 50bp again, but the forecast is not unanimous. Of the 31 economists surveyed by Bloomberg 19 expect rates to be raised by 50bp, 11 by 25bp and 1 by 100bp.

- In September, BI said that it raised rates by an unexpected 50bp to be forward-looking and pre-emptive and this could be behind its monetary policy decision making again this month, especially as it was behind the rest of Asia in starting its tightening cycle.

- Inflation, growth and FX policy were also given as reasons for the September move and can all be used again to justify either a 25bp or 50bp rate hike. On balance, though, the current environment suggests a further 50bp move to 4.75%, but there is a high probability that they could opt for a more moderate 25bp.

- For the full piece, see here:BI Preview - October 2022.pdf

MNI CBRT Preview - October 2022: Another 100bp Cut Seen in Next Step Toward Single Digits

EXECUTIVE SUMMARY:

- Following the unanticipated 100bps rate cut in August, the CBRT are firmly expected to again cut the policy rate by 100bps for the third consecutive month.

- This would bring the one-week repo rate to 11.00%, in line with the majority of sell-side views.

- This decision comes despite inflation accelerating for the 16th consecutive month to a hot 83.45% in September and the lira’s value eroding further.

- The CBRT maintains an unorthodox approach to monetary policy, seen persisting for the foreseeable future, with President Erdoğan’s call for single-digit rates into year-end likely to materialise.

EQUITIES: HSI At Fresh 13 year Lows, As Tech Headwinds Continue

Asia Pac equities are weaker, outside of a few South East Asian Markets. Wall St declines from overnight, coupled with lower futures since the open, led by the tech sector (Nasdaq futures off by over 1% on disappointing Tesla revenue), have been the major headwinds.

- The HSI is off by close to 2.5%, making fresh lows back to 2009. The tech sub-index -4.60%. This comes after the China Golden Dragon Index lost just over 7% overnight. The China authorities have reportedly held meetings with top China chip makers in light of US curbs on export/technology sharing in the sector. No clear policy response is evident at this stage.

- Mainland stocks are also lower, but to a more modest degree. The CSI 300, is down around 0.70%. Higher covid case numbers in Beijing are weighing on sentiment, while higher frequency growth indicators, like subway rides have moderated in recent weeks. Earlier 1yr and 5yr LPR rates were left unchanged, as expected.

- The Nikkei 225 is off by 1.3%, while the Taiex is down 1.65%, again led by declines in TSMC. The chip sector is facing headwinds from the slowing global growth backdrop/along with US-China tensions. The Kospi is down 1.6%.

- Indonesian stocks have outperformed, up close to 1.4%, led by local bank shares.

GOLD: Yield Spike Weighs

Downside levels are once again in focus for gold. The precious metal lost 1.38% through yesterday's session and is down a further 0.20% so far today. Spot levels currently hold close to $1626.

- Today's trends have been a continuation of the overnight price action, although we have made fresh lows close to $1622.50, before support emerged. Moves back towards the $1630 have generally drawn selling interest since late NY trading.

- September 28 lows around $1615 are in focus, only 0.65% away in percentage terms.

- The resurgent US yield backdrop, particularly in terms of real yields (10yr closed a fresh cyclical high at 1.72%), is a clear headwind for gold. This is feeding into USD strength, which is mostly outweighing safe haven/risk aversion benefits gold otherwise might be receiving.

- The gold/copper ratio has broadly been stable in recent months, likewise for gold to oil.

OIL: Prices Surge On China Quarantine News

After rallying strongly overnight on supply worries, oil prices have been fairly stable during trading today but have just surged on reports that China is considering reducing inbound quarantine periods to 7 days. WTI is up 0.8% to $86.20/bbl and Brent is +0.6% and is around $93.

- Oil prices continue to be thrown around by concerns that a global slowdown will depress demand for oil on one side and supply issues on the other (OPEC+ cuts, EU sanctions on Russian seaborne oil exports, Kazakhstan).

- The market has not reacted to President Biden’s announcement to add 15mn barrels from the Strategic Petroleum Reserve. The information had already been expected and on the other hand the EIA announced an unexpected drawdown in crude inventories of 1.725mn barrels.

- The US also only has 25 days of diesel available, the lowest since 2008, which is important for heating in winter. Europe’s fuel inventories are also declining. (Bloomberg)

- WTI moving averages have been converging and prices are now just above 5- and 20-day moving averages but still below the 50-day MA.

UP TODAY (Times GMT/Local)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 20/10/2022 | 0600/0800 | ** |  | DE | PPI |

| 20/10/2022 | 0645/0845 | ** |  | FR | Manufacturing Sentiment |

| 20/10/2022 | 0720/0320 |  | ID | Bank of Indonesia Rate Decision | |

| 20/10/2022 | 0800/1000 | ** |  | EU | EZ Current Account |

| 20/10/2022 | 1100/0700 | * |  | TR | Turkey Benchmark Rate |

| 20/10/2022 | 1230/0830 | ** |  | US | Jobless Claims |

| 20/10/2022 | 1230/0830 | ** | | US | Philadelphia Fed Manufacturing Index |

| 20/10/2022 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 20/10/2022 | 1400/1000 | *** | | US | NAR existing home sales |

| 20/10/2022 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 20/10/2022 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 20/10/2022 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 20/10/2022 | 1600/1200 | | US | Philadelphia Fed's Patrick Harker | |

| 20/10/2022 | 1630/1230 | | US | Fed Governor Lisa Cook | |

| 20/10/2022 | 1700/1300 | ** | | US | US Treasury Auction Result for TIPS 5 Year Note |

| 20/10/2022 | 1730/1330 | | US | Fed Governor Philip Jefferson | |

| 20/10/2022 | 1745/1345 | | US | Fed Governor Lisa Cook | |

| 20/10/2022 | 1805/1405 | | US | Fed Governor Michelle Bowman |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.