- Both USD/JPY and JGB futures went higher as the BoJ kept its bond buying pace unchanged. Follow through has been limited, while JGB yields have been more resilient this past week compared to UST yield downside.

- More broadly, the USD index has firmed modestly, but is still down comfortably for the week.

- China data was, on balance, weaker than expected. It highlights the narrow base of economic strength in the industrial sector. Headlines have crossed around further housing market support, with removed mortgage rates floors and reduced downpayments for homebuyers the highlights so far.

- Looking ahead, the focus turns to the final reading of Eurozone CPI and any further commentary from Fed officials.

MARKETS

US TSYS: Tsys Futures Edge Higher, SFRZ4 Volumes Spike, Leading Index To Come

- Treasury futures traded in a very narrow range today, volumes were slightly higher than normal although well done on yesterday, front-end performed slightly better with the 2Y up (+ 00.75) at 101-25.125 while the 10Y contract is up (+ 01) at 109-16+.

- The treasury curve has bull-steepened today, yields are flat to 2.5bps lower, the 2Y yield -2.2bps at 4.774%, 10Y -0.6bps to 4.369%, while the 2y10y +1.586 at -40.660

- There were multiple Block trades in SFRZ4 options earlier for total size of 52k at 95.135 to 95.145.

- MNI BRIEF: Bostic Repeats Fed Rate Cut At End of Year Likely - (See link)

- Rate cut projections gradually receded from Wed's post-data highs. At the moment: June 2024 at -10% w/ cumulative rate cut -2.5bp at 5.313%, July'24 at -22% vs. -28% earlier w/ cumulative at -8bp (-9.5bp earlier) at 5.258%, Sep'24 cumulative -21.6bp (-23.6bp earlier), Nov'24 cumulative -30.3bp (-33.8bp earlier), Dec'24 -45.4bp (-49.5bp earlier).

- Looking Ahead: Leading Index. Fed Speak: Waller, Kashkari, Daly, Kugler

JGBS: Underperformance Against US Tsys Continues, BoJ Held Bond Buying Steady

JGB futures sit off session highs. JBM4 was around 144.09, -.18 in latest dealings. Earlier we got to 144.19 as the BoJ bond buying ops were unchanged, with some market concern we could have seen another reduction (as was the case for Monday's session). The US Tsy futures trend in the 10yr has been very steady today.

- More broadly we sit within recent ranges for JGB futures, albeit slightly towards the bottom end of ranges for the past month.

- US-JP yield differentials sit comfortably off April highs. The 10yr spread around +343bps, the 2yr spread around +444bps. Focus will remain on the BoJ outlook and the potential for curbing of bond purchases.

- On this point, the latest from our Tokyo policy team notes: "The Bank of Japan is concerned the market could interpret any reduction to its Japanese government bond buying programme as an attempt to curb yen weakness and a sign of earlier-than-expected rate hikes, and will hold off plans to shrink its purchases until stability returns to the foreign-exchange market, MNI understands." (see this link for more details).

- For cash JGB yields, we sit higher in yield terms, the 10yr pushing back up to around 0.94%, while the 20-40yr tenors have seen +2bps gains today. The 10yr swap rate holds above 0.99%.

- Next week focus is likely to largely rest on Friday's national CPI print.

AUSSIE BONDS: ACGBs Cheaper, Curve Steepens

ACGBs (YM -1.0 & XM -2.0) are cheaper today, we trade near best levels for the session. It has been a relatively quiet session for global rates, focus has been in Japan where the BoJ refrained from cutting bond purchases. The past week has seen yields move 5-11bps lower, with the 5 & 30yr tenors seeing the largest moves, looking ahead to next week it will be a relatively quiet one with Westpac Consumer Conf on Tuesday, a 30yr auction Wednesday and a 5yr auction on Friday.

- Cross-asset moves: Risk assets are lower today, regional equities seeing profit taking although have ended the week higher with the MSIC Asia Pacific up about 2%, US equities futures are trading unchanged, in the FX space the yen is the worst perfoming following AUD, NOK & NZD with the BBDXY up 0.13%, Iron Ore is up 0.26% at $117.15/ton

- US Tsys curve bull-steepened with the 2y10y +1.392 at -40.855, yields were flat to 2.5bps lower

- The ACGB curve is slightly steeper today and has pivoted at the 10y with the 2y10y +1.30 at 29.100, yields are flat to 2.5bps higher, while the AU-US 10-year yield differential is 1.5bps lower at -16.5bps

- Swap rates are 1bp lower

- The bills strip is flat to 1bps higher

- RBA-dated OIS implied rate is little changed today into year-end with 17bps of easing into the year-end to a terminal rate of 4.18%

- Looking ahead, we have Westpac Consumer Conf on Tuesday.

NZGBS: Cheaper, Curve Bear-Flattened, RBNZ On Wednesday

NZGBs are 1-3bps cheaper, curve has bear-flattened largely mirroring moves made by US Tsys. The past week have seen yields move 12-17bps lower, the long-end saw the most support with the 20 & 30yr 16bps richer, the moves were driven largely from US Tsys as the market priced two 25bps cuts in by year-end, looking ahead to next week focus locally will be on the RBNZ who meet on Wednesday

- US treasury futures have traded in tight ranges today, with volume slightly higher than normal although well down on Thursday volumes. Front-end futres are outperforming with the 2Y up (+ 00.75) at 101-25.125 while the 10Y contract is up (+ 01) at 109-16+. Earlier there was a large amount of Block SFRZ4 option buys for a total size of 52k.

- The NZGB curve is has bear-flattened today, yields are 1-3bps higher with the 2Y +3bps at 4.669% and the 10Y is +2.6bps at 4.586%.

- Swap rates are 1-2bps lower, curve steepened

- (BBG) ANZ Sees RBNZ Holding Rate Until May 2025 on Sticky Inflation - (see link)

- RBNZ dated OIS is 2-3bps weaker over the day and is now pricing a cumulative 47bps of easing into year-end

- Looking Ahead: RBNZ on Wednesday

FOREX: USD Index Pares Weekly Loss, Yen Weaker As BoJ Maintains Bond Purchase Pace

The BBDXY USD index sits just off session highs, last near 1247.5. This is near 0.20% firmer versus end NY levels from Thursday. Still, we are comfortably tracking lower for the week, off around 0.50% at this stage. The weaker US yield backdrop has weighed, with the 10yr yield off around 13bps through this period. Focus has been on Fed easing risks in light of data outcomes, albeit with some push back from Fed officials around the progress on inflation in recent sessions.

- Today, USD/JPY is up around 0.30%, last near 155.80. This is slightly off session highs (155.93). Yen was weighed by an unchanged BoJ bond buying stance, as there was no follow up after Monday's reduced purchases for 5-10yr bonds. The pair remains above all key EMAs (the 20-day sits near 155.00).

- AUD/USD is softer, back towards 0.6660, down around 0.25%. On balance, weaker China data hasn't aided sentiment. China IP growth and retail sales showing diverging trends. Property indicators and house price data were also weak. NZD/USD is off by around 0.15%, last near 0.6110/15.

- Regional equity sentiment has been mixed today, with softer mainland China equities a likely headwind for AUD and NZD. Cross asset sentiment elsewhere has seen slightly lower front end US yields, while equity futures are near flat.

- Looking ahead, the focus turns to the final reading of Eurozone CPI and any further commentary from Fed officials.

ASIA STOCKS: HK Equities Continue Their Strong Run, China Falls On Mixed Data

Hong Kong & Chinese equities are off earlier highs and now trade mixed for the day, Industrial production beat estimates coming in at 6.7% vs 5.5%, investors focused on the poor retail sales that came in at 2.3% vs 3.7% while property investment fell to -9.8% in Apr vs -9.6% in March. Focus this week has been largely on the China property space after a proposal by the Chinese government to allow local governments to purchase unsold properties from distressed developers, we expect further updates around this policy today as government officials are set to meet with Banks to discuss the property market, Chinese markets have also been impacted this week by news that the US will be imposing further tariffs on Chinese sectors including EVs, Semiconductors and Batteries. Looking back over the week Hong Kong markets have continued their outperformance over their China Mainland peers with the HSI outperforming the CSI300 by 2.22% and 17.89% for the month.

- Hong Kong markets have had a shortened week, property names have been the major focus with the Mainland Property Index up 0.25% today, 4.63% for the week and 35% from the lows made on Apr 19th. Big tech names including Alibaba and Tencent reported this week, with mixed results the HSTech Index is up 0.65% for the day and 3.50% for the week, while the HSI is trading up 0.23% today and 2.35% for the week with the index now up almost 20% for the month we now sit well into overbought territory when looking at the 14-Day RSI and trade well above all moving averages, signally there may be a pull-back to come shortly.

- China markets have under performed HK markets ever since Chinese officials announced measures to support the HK markets by driving quality IPOs to list there and other supportive measures. The US announced further tariffs on some Chinese EVs, Semiconductors and Battery sectors during the week, the China EV Index is down 3.34% for the week. China's main large-cap Index the CSI300 is down 0.20% today, 0.82% for the week and has underperformed the HSI by almost 18% for the month, small-caps have been slightly worst this week with the CSI1000 down 1.54% while the growth focused ChiNext is 0.22% lower today and down 2.00% for the week.

- In the property space, the major news this week was around the Chinese government putting together the proposal for local governments to by unsold homes from distressed developers, while earlier on Friday China Evergrande suspended trading, although there was no reason listed but it should be noted their equity surged 73% before the halt.

- Looking over the data for the week: Saturday we have PPI slightly below consensus at -2.5% vs -2.3%, CPI beat estimates coming in at 0.3% vs 0.2%, Money Supply missed estimates at 7.2% vs 8.3%, the MLF was held unchanged at 2.5%, New Home Prices fell 0.58% m/m, while Used Homes Prices fell 0.94% m/m . Earlier today Industrial Production beat estimates at 6.7% vs 5.5%, Retail Sales missed estimates coming in at 2.3% vs 3.7% and Fixed Assets ex Rural were 4.2% vs 4.6%.

- Looking ahead, quiet week for Chinese data with the 1 & 5yr LPR on Sunday, while Hong Kong has the unemployment rates on Sunday and the CPI composite on Thursday

ASIA PAC STOCKS: Asian Equities On Track For Third Week Of Gains

Asian markets are mostly lower today ending a 5-day winning streak, tech stocks have been the biggest detractor in the region and weak Chinese data hasn't done much to help the market. Looking back over the week the MSCI Asia Pacific is up about 2%, as markets have been aided by optimism that the Fed will start cutting rate later this year. There hasn't been much in the way of data, other than South Korean unemployment today.

- Japan equities are mixed today, tech shares have given back some of their recent gains as investors look to book profits, while the yen is trading back above 155.50 after the BoJ left bond buying amounts unchanged, with one former BOJ chief economist suggested the central bank may raise interest rates three more times this year with the next move coming as early as June. The Topix is outperforming today up 0.32% and 0.64% for the week, while the Nikkei 225 is off 0.28% largely due to weaker tech prices, although is up 1.52% for the week.

- South Korean equities are weaker today with the likes of Samsung off over 1%, as investors look to book profits after a strong run of late. Earlier, the unemployment rate came in at 2.8% in line with estimates, while next week we have PPI, Business Survey's and the BOK rate decision. The Kospi is down 1% today and now trade unchanged for the week.

- Taiwan equities are lower today, after hitting new all-time-highs on Thursday. There has been little in the way of local markets new and no data out of the region this week, equities have benefitted from strong global tech prices, US imposing more tariffs on Chinese semiconductors and the market now pricing two US rate cuts heading into the year end. The Taiex is down 0.25% today, although still trade up 2.61% for the week.

- Australian equities are lower today, after yesterday having their best session of the year. Looking back over the week, NAB business surveys were largely ignored by the market, confidence was was unchanged from march, while conditions dropped to 7 from 9, wage price index was slightly below estimates at 4.1% vs 4.2%, while employment data was mixed, showing a growth of 38.5k jobs vs 23.7k, however 44.6k were part time jobs compare to a loss of 6.1k full time jobs, the unemployment rate ticked higher to 4.1% as the participations rate increased to 66.7% from 66.6%. The ASX200 is down 0.70% for the day although trade up 1% for the week.

- Elsewhere in SEA, New Zealand equities close the week down 0.60%, Indonesian equities are up 1.10% for the day and 3.38% for the week, Philippines equities unchanged today but up 1.71% for the week, Malaysian equities are up 0.35% today and 1% for the week and finally Indian equities are up 1.40% for the week although foreign investors have been dumping stock.

ASIA EQUITY FLOWS: Equity Flow Positive For the Week, Tech Stocks See Majority Of Flow

- South Korean equity markets were higher on Thursday with equity flows positive. It was a shortened week with the local market out on Wednesday for Buddha's Birthday we have seen $508m of net buying by foreign investors for the week, with the Kospi currently up 0.68% over the same period. It has been a quiet week for economic data with just employment data, which was in line with expectations at 2.8%. The 5-day average is now $65m, in line with the 20-day average of $69m, but well down on the longer term 100-day average at $177m.

- Taiwan equities were again higher on Thursday, foreign investors bought $1.7b of equities making it the the largest since Feb 15th. The Taiex is up 2.88% for the week and have made new all-time-highs. There was very little in terms of economic data or local market headlines over the week. The 5-day average now sits at $826m, well above the 20-day average at $158m and the 100-day average at $96m.

- Thailand equities have see-sawed over the week and currently trade 0.42% higher for that period, foreign investors bought $98.5m of equities on Thursday taking the weekly net inflow to $120m. It was a quiet week for local data or market headlines, with markets now focused on GDP data that will be released on Monday. The 5-day average now at $20m, the 20-day average -$9.17m, while the 100-day average is -$18.63m.

- Indonesian equity ended their run of net selling by foreign investors on Thursday, although we now sit at just 3 of the past 29 of net buying, flows over the past week are still negative with a net outflow of $148m. The JCI is up 2.23% for the week and has broken back above all moving averages, while the 14-day RSI has ticked above 50 for the first time this month. The 5-day average now -$43m in slightly above the 20-day average at -$54m while the 100-day average is still positive at $4.3m.

- Philippines equities have seen 11 of the past 12 days of selling by foreign investors, although an inflow on Monday has more than covered the outflows for the remainder of the week, the past 5 sessions have seen a net inflow of $43m while the PSEi is up 1.79% over the same period. The 5-day average is $8.7m, above the 20-day average at -$18m and the 100-day average of -$2.8m

- Indian equities have seen foreign investors sell stocks for the 10th straight session, investor flow data is a day behind in India, however the past 5 sessions have seen a net outflow of $2b over that period, with the Nifty 50 up 1.58% for the week. We have bounced right off the 100-day EMA and now trade back above all moving averages. The 5-day average now -$412m, the 20-day average is -$230m while the 100-day average is still positive but declining quickly and sits at $26m.

- Malaysian equities continue making new highs with the Malay KLCI trading above 1,600. Equity flows have been positive for the past two week, with just a single $2.2m outflow on Apr 9th. Over the past week foreign investors have purchased $100m of equities, with the 5-day average now $20m, in line with the 20-day average at $22m and above the longer term 100-day average at $0.06m.

Table 1: EM Asia Equity Flows

| Yesterday | Past 5 Trading Days | 2024 To Date | |

| South Korea (USDmn) | 344 | 325 | 15499 |

| Taiwan (USDmn) | 1740 | 4132 | 4377 |

| India (USDmn)* | -301 | -2419 | -3268 |

| Indonesia (USDmn) | 33 | -217 | -5 |

| Thailand (USDmn) | 99 | 103 | -1849 |

| Malaysia (USDmn) * | 20 | 100 | -94 |

| Philippines (USDmn) | -3 | 20.8 | -277 |

| Total | 1931 | 2045 | 14383 |

| ** Data Up To Apr 15th |

COMMODITIES: Oil & Gold Tracking Higher For The Week, Technicals More Positive For Bullion

Oil sits close to highs for this week, with the front month Brent contract near $83.50/bbl. This is +0.25% on end Thursday levels in NY, while for the week we are tracking around 0.80% higher, which would be the first weekly gain since the end of April. WTI was last near $79.30/bbl, currently up near 1.4% for the week.

- The past week has seen relatively narrow trading ranges for oil, as demand and supply factors have largely offset each other. Lower crude stockpiles in the US have been a positive, along with signs of a potential soft landing scenario for the US economy (which could bring earlier Fed cuts).

- Still broader demand concerns continue to cloud the outlook. Today's China data reinforced the uneven nature of the current economic backdrop, with consumer spending softer relative to industrial acitivty.

- In terms of levels, a bearish theme in WTI futures remains intact and scope is seen for a move to $76.07, the Mar 11 low. Initial firm resistance is at $84.46, the Apr 26 high.

- For gold, we are tracking up a further 0.70% for the week at this stage, last near $2377. The first part of Friday trading has been range bound. The broader uptrend looks positive, although we haven't been able to breach the $2400 level. A continued push higher would refocus attention on $2,431.50, the Apr 12 high and bull trigger

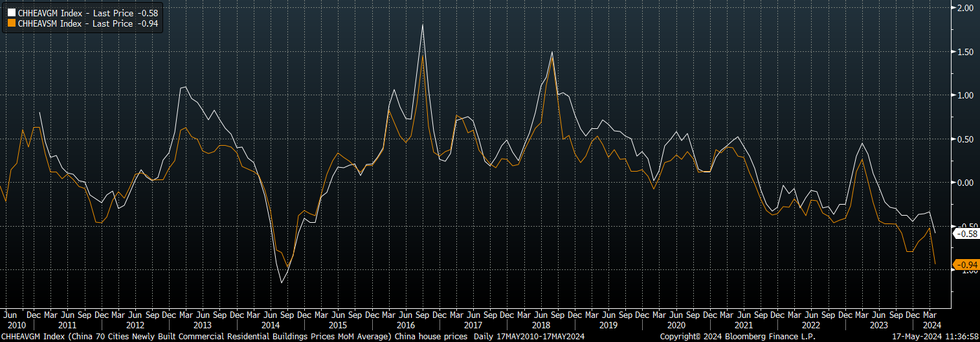

CHINA DATA: House Price Falls Accelerated In April, Underscoring Need For Policy support

China April house price trends showed renewed downside momentum after a modest recovery in recent months. New home prices fell -0.58% m/m, versus -0.34% in March. Used home prices fell -0.94% m/m from -0.53% recorded in March.

- Both series are back towards 2014 lows, see the chart below. Note used houses m/m change is the orange line.

- In terms of city outcomes, we saw 64 cities record a fall in April for new home prices. We were at 57 cities in March (6 recorded an increase, compared with 11 in March). For existing or used homes these stats were unchanged with 69 cities seeing falls in April. In y/y terms these stats were similar.

- For the larger cities, Shanghai remained a bright spot, up 4.2% y/y for April. Beijing was back to -0.5% y/y, Guangzhou was -6.9%y/y, while Shenzhen -6.7% y/y. These are all for new homes.

- The data underscores efforts by the authorities to boost sentiment/support in the sector. Today a meeting between key stakeholders in terms of China's property sector is taking place (see this BBG link for more details).

Fig 1: China House Prices See Renewed Downside Pressure

Source: MNI - Market News/Bloomberg

CHINA DATA: April Data Shows IP & Retail Sales Divergence, Property Indicators Still Weak

China April activity data was mixed, albeit with more downside surprises than up relative to consensus expectations. It continues to highlight some divergent trends within the economy, particularly in terms of retail spending and industrial output, see the chart below.

- Industrial production was firmer than expected at +6.7% y/y (forecast was 5.5% and prior 4.5%). We are back to late 2023 levels from a y/y standpoint. Strength was seen in tech related areas, along with motor vehicles. EV production maintained a heady +39.2% y/y pace. Part of the commodity space were weaker though, with cement and steel down in y/y terms.

- Retail sales surprised on the downside, printing at +2.3% y/y versus 3.7% forecast and 3.1% prior. Most sub-sectors saw weaker spending in y/y terms versus March outcomes. Clothing, office supplies, cars and construction materials are all running at negative y/y pace.

- Fixed asset investment was +4.2% y/y ytd, against a 4.6% forecast. Private sector investment eased from 0.5% to 0.3%. Infrastructure spending remain firm at +6.0%.

- Property investment remained depressed at -9.8% y/y ytd, slightly weaker than expected. New home sales are down -31.1%, while new property construction was -24.6%, which is similar to March outcomes.

- The surveyed jobless rate was 5.0%, against a forecast of 5.2%.

- Overall, the data is likely to see further calls for policy support in the property space, while the divergence in retail spending and IP highlights the unevenness of the current economic backdrop.

Fig 1: China Retail Sales & Industrial Production Growth Diverging

Source: MNI - Market News/Bloomberg

ASIA FX: USD/Asia Pairs Higher, Won Drops, PHP Weighed By BSP

USD/Asia pairs are mostly higher, which is in line with the USD index gaining ground against the majors, particularly the yen. USD/CNH is off highs from above 7.2300, as headlines around further housing market support filter out, removed mortgage rates floors and reduced downpayments for homebuyers have been the highlights so far. The won has seen a large drop, while in SEA, THB and IDR are both off around 0.30%, PHP is slightly underperforming, down 0.45%, with dovish BSP rhetoric a likely factor.

- We had mixed China data earlier, with retail sales and fixed asset investment weaker than forecast. Property sales/investment trends remained quite weak, while house prices falls accelerated compared to March. USD/CNH pushed to 7.2330, but we sit back lower now, as headlines filter out from China's housing market meeting. Eased mortgage rules and reduced downpayments, highlighted by the PBoC, is aiding property related equity sentiment in afternoon trade.

- 1 month USD/KRW was up strongly in the first part of Friday dealings. We 1356.5, +0.60% from NY closing levels on Thursday, but we sit slightly lower now, last near 1353/54.. We were around 15 won weaker versus intra-session lows from Thursday (near 1340). Weakness in the yen is not helping sentiment today BBG also notes some onshore demand for USDs from local firms. Local equities are off by 0.90%, but the Kospi remains above 2700. More broadly, the 1 month NDF couldn't sustain the break of the 100-day EMA (around 1345).

- USD/PHP is back close to 57.70/75, around 0.45% weaker in PHP terms for the session so far. This is in line with other SEA FX. The pair remains sub recent highs of 57.89 from earlier in the week. Focus is likely to remain on whether we can test 58.00 on the upside. Note the 20-day EMA sits back near 57.42, while the 50-day is around 56.96.PHP weakness today is in line with regional trends, but it has underperformed over the past week, off nearly 0.50%, despite a softer USD backdrop elsewhere. Earlier comments from BSP Governor Remolona are likely to reinforce risks around easier policy setting as we move into H2 of this year, a likely PHP headwind.

- USD/THB is back to 36.25/30, around 0.30% weaker, while USD/IDR is back towards 15975, also off around 0.30% in rupiah terms.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 17/05/2024 | 0720/0920 |  | EU | ECB's De Guindos at Banking Sector Industry Meeting | |

| 17/05/2024 | 0800/0900 |  | UK | BOE's Mann Speech at Economics Statistics Centre of Excellence Conference | |

| 17/05/2024 | 0900/1100 | *** | | EU | HICP (f) |

| 17/05/2024 | 1230/0830 | * |  | CA | International Canadian Transaction in Securities |

| 17/05/2024 | 1415/1015 |  | US | Fed Governor Christopher Waller | |

| 17/05/2024 | 1700/1300 | ** | | US | Baker Hughes Rig Count Overview - Weekly |