Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Cash Tsys sit 2-6bps cheaper across the major benchmarks, the curve has bear flattened. Asia-Pac participants added to yesterday's NY weakness in Tsys as they digested Fed Chair Powell's remarks at his Senate appearance. 2 Year-Yield breached yesterday's highs (highest since '07) and the 2s10s inversion printed a fresh cycle extreme.10-Year Yield did briefly print above 4%, however, the lack of follow through above there and subsequent tick back below the round number stabilised the long end a little (much like NY trade on Tuesday).

- Higher Tsy yields supported the USD, while the JPY found itself at the top of the G10 FX table.

- Highlights today include comments from Fed Chair Powell & ECB President Lagarde. ADP employment and JOLTS job openings data out of the U.S> is due, as is the latest BoC monetary policy decision.

MNI Insight: Global Macro Chart Pack - 2023 Is Likely To Be A Bumpy Ride

EXECUTIVE SUMMARY:

- 2022 finished on a soft note for global trade/growth indicators. Early indications are that 2023 has started on a better footing, with key PMIs proving resilient, while consensus forecasts are generally nudging higher for key economies/regions but official projections suggest 2023 will be a challenging year.

- How global growth expectations unfold will be important for the USD, particularly in the EM FX space, notwithstanding Fed outcomes and outlook.

- Inflation is the other key watch point. 2023 could see more diverges in inflation outcomes, which is already playing out in Asia. This in turn is driving divergences in policy outcomes. How inflation evolves will feed back into broader risk appetite in the equity space and can also influence growth expectations via the tightening/money supply channel.

- See full chart pack here:Global Macro March 8 2023 .pdf

US TSYS: Pressured In Asia, Powell Testimony Continues Today

TYM3 deals at 110-23, 0-07+, a touch off the base of the 0-11 range on elevated volume of ~185K.

- Cash Tsys sit 2-6bps cheaper across the major benchmarks, the curve has bear flattened.

- Asia-Pac participants added to yesterday's NY weakness in Tsys as they digested Fed Chair Powell's remarks at his Senate appearance.

- 2 Year-Yield breached yesterday's highs (highest since '07) and the 2s10s inversion printed a fresh cycle extreme.

- 10 Year Yield did briefly print above 4%, however, the lack of follow through above there and subsequent tick back below the round number stabilised the long end a little (much like NY trade on Tuesday)

- On the sell side Goldman Sachs raised their Fed terminal rate forecast by 25bps to 5.5-5.75%.

- Block sales in TU (3.7k lots), FV (2.25k lots) and TY (~2.8k lots) provided the highlight on the flow side.

- There was little meaningful macro headline flow through the Asian session.

- In Europe today we have final Eurozone GDP and ECB-speak from Lagarde. Further out MBA Mortgage Applications, ADP Employment , Trade Balance and JOLTS Job Openings will cross. Elsewhere, Fed Chair Powell’s Congressional testimony continues and we have the latest 10-Year Tsy supply.

JGBS: Long End Weakness Promotes Twist Steepening Post-Powell & Pre-BoJ

JGB futures have moved further away from their early Tokyo lows during afternoon trade, printing -3 ahead of the bell.

- The early steepening dynamic and leg lower in JGB futures was seemingly a product of follow through from Fed Chair Powell’s hawkish warnings. Super-long paper remained heavy throughout the day with U.S. Tsys operating on the backfoot in Asia.

- The twist steepening dynamic in JGBs thereafter was potentially a product of continued unwinds of hawkish flattener plays pre-BoJ and a subdued to average round of cover ratios in the latest round of BoJ Rinban operations (1- to 25-Year JGBs). Cash JGBs are 0.5bp richer to 3bp cheaper into the close, with only 30s and 40s sitting cheaper on the session.

- Local headline flow was subdued.

- There isn’t much to inspire on the local calendar on Thursday, with final Q4 GDP readings providing the pick of the bunch. We will also get the latest liquidity enhancement auction covering off-the-run 1- to 5-Year JGBs.

- Focus remains squarely on Friday’s BoJ decision. A clear consensus looks for no change in BoJ policy settings come the end of outgoing Governor Kuroda’s final policy meeting. However, the Bank’s recent propensity to shock (see the surprise widening of the YCC band back in December) means that this view is held with varying degrees of conviction. There will be more on that matter in our full preview of the event.

AUSSIE BONDS: Reverse Direction With Weaker U.S Tsys

After an initial spike higher with the release of RBA Governor Lowe’s speech this morning, ACGBs quickly reversed and then cheapened over the session to close near lows (YM -9.0 and XM -6.0). With Lowe clarifying yesterday’s dovish message, that a pause as soon as April is possible (offering little new), ACGBs turned to U.S Tsys for direction. Cash ACGBs weakened 5-8bp with the 3/10 cash curve 2bp flatter.

- The 3s10s swaps curve bear flattened with rates 4-6bp higher and EFPs 1-2bp tighter.

- Bills closed 2-7bp cheaper, steepening.

- After yesterday’s aggressive RBA-induced softening, RBA-dated OIS firmed +3-6bp for meetings beyond June with terminal rate pricing pushing back out to 4.07% versus yesterday’s of ~4%. The strip took the lead from Tuesday's repricing of FOMC expectations.

- Futures roll activity will pick up from the overnight session, with tick sizes shrinking ahead of next week's expiry.

- With the local calendar light for the remainder of the week, the market will be guided by developments abroad. Later today we hear from Fed Chair Powell when he testifies before the House. The BOC is also scheduled to deliver a policy decision. With the RBA now openly discussing a policy pause, the market will be keen to see if the BOC carries through with its no-change guidance today.

NZGBS: Close On Cheaps As U.S Tsys Weaken

Today threatened to be a volatile session as the market caught up with developments in AU and U.S., and it didn't disappoint with the 2-year NZGB benchmark trading in a 10bp range (the 10-year traded in a more modest 4bp range). NZGB benchmarks close at session cheaps with Fed Chair Powell-induced U.S Tsy weakness the key driver. The 2/10 cash curve bear flattened with yields little changed to +7bp higher.

- On a relative basis, the NZGB benchmarks outperformed U.S. Tsys with the 10-year yield differential -4bp tighter and the 2-year yield differential -12bp lower. Not surprisingly after recent RBA developments, the NZ/AU 10-year yield differential closed +4bp wider.

- A similarly heavy session for swaps with rates 4-9bp higher, implying wider swap spreads, and the 2s10s curve 5bp flatter.

- With the strongly divergent messages from the RBA and the Fed since the local close yesterday RBNZ-dated OIS has taken its cue from U.S. developments. Pricing is 3-9bp firmer across meetings with August leading. April pricing firms to 45bp of tightening. Equally noteworthy, terminal rate expectations have pushed well above the RBNZ’s projected OCR peak of 5.50% to ~5.60%.

- The local calendar has card spending data for February scheduled on Thursday, while RBNZ Deputy Governor Hawkesby will appear at a private event, fleshing out the previous monetary policy decision (no new information will be divulged).

FOREX: Greenback Firms On Rising US Yields

The USD is on the front foot in Asia as rising US Treasury Yields boost the greenback. Yen is the weakest performer in G-10 space at the margins.

- USD/JPY prints at ¥137.80/90, approaching upside resistance is at ¥137.95 high from 2 March and bull trigger. Early in the session weaker than expected trade balance and current account figures weighed on the Yen. JPY was a relative outperformer on Tuesday so today's move may reflect a partial reversal of the trend.

- Kiwi is also softer, NZD/USD is down ~0.2%. The pair has been pressured and registered a fresh YTD low at $0.6085 before marginally paring losses to sit a touch below $0.6100.

- AUD is marginally outperforming, AUD/USD registered its lowest level since early November before paring losses to sit a touch firmer. The next downside target is $0.6547 61.8% retracement Oct - Feb bull cycle. RBA Gov Lowe noted that this morning the RBA is getting closer to a pause but that the peak in rates hasn't been reached however there was little follow through and the losses were pared.

- AUD/NZD is ~0.3% firmer, the cross has recovered above the $1.08 handle recouping some of yesterday's losses.

- EUR and GBP sit ~0.1% softer as the greenback strength marginally weighs.

- Cross asset wise, 2 Year US Treasury Yields are at a cycle high (5.07%). US Equity futures are little changed. BBDXY is ~0.2% firmer.

- In Europe today we have final Eurozone GDP. Further out MBA Mortgage Applications, ADP Employment , Trade Balance and JOLTS Job Openings will cross. Elsewhere, Fed Chair Powell’s appears before the House Finance Committee.

MNI BoC Preview, Mar'23: Maintaining The Conditional Pause

EXECUTIVE SUMMARY

- The BoC is unanimously expected to keep rates on hold at 4.5% on Wednesday and for the most part echo January’s pivot to guidance of a conditional pause whilst leaving the door open to further hikes.

- Data has been mixed. Employment was far stronger than expected but CPI showed some moderation and GDP was surprisingly soft, albeit partly offset by hawkish implications from weaker productivity growth.

- Surprises should never be ruled out from the BoC, with a weaker CAD adding inflationary pressure at the margin. However, market reaction could be limited with focus on nuances of the single page statement before potentially more detail in Thursday’s Economic Progress Report from Senior Dep Gov Rogers.

- PLEASE FIND THE FULL REPORT HERE: BOCPreviewMar2023.pdf

Canadian rates have been dragged higher by the substantial higher for longer push in the US

FX OPTIONS: Expiries for Mar08 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0500-05(E797mln), $1.0560-65(E2.5bln), $1.0600(E902mln), $1.0645-60(E1.5bln), $1.0670-90(E2.3bln), $1.0715-35(E1.5bln), $1.0745-55(E1.5bln)

- USD/JPY: Y135.00($1.2bln), Y137.00($1.6bln)

- USD/CAD: C$1.3550-60($623mln)

- USD/CNY: Cny6.8650($1.1bln)

ASIA FX: USD/Asia Pairs Away From Session Highs, CNH Outperforms

USD/Asia pairs are higher across the board, with the ADXY back sub 100 in index terms. Higher US yields and weakness in the equity space have been headwinds for regional FX today. We are away from dollar highs though, with a number of pairs close to YTD highs, which means intervention risks have arguably firmed. CNH has outperformed, as USD/CNH has backed away from a test of the 7.00 level. Tomorrow, we have China inflation data, the BNM decision (close call but no change expected), along with Thailand consumer confidence and Philippines jobs data.

- USD/CNH has been offered today, but we haven't drifted too far away from the 6.9800 level. The CNY fixing was noticeably stronger than expected, suggesting some reluctance to see a sharp break through 7.00 in the near term. Tomorrow's inflation prints are expected to be benign.

- 1 month USD/KRW found selling interest above 1320, with the pair last near 1319. Spot has weakened 1.6% so far today and is just above 1321. Onshore equities are down 1.3%, with offshore investors net sellers of -$224.2mn of local shares today. The authorities stated they will strengthen FX cooperation with the US authorities.

- USD/IDR continues to push higher, spot has gained a further +0.60% today for the pair, last near 15450. The pair is above all key EMAs, while we have broken above the simple 100-day MA as well (15429.50). Early Jan highs are in focus, just above the 15600 level. The currency is once again showing its sensitivity to core yield movements. IDR is the worst performer within the region month to date. Late headlines have hit of BI intervention.

- USD/INR is firmer today, +0.25% to 82.10/15, but still outperforming on a relative value basis. In the first 3 days of March Foreign Investors bought ~$1.67bn of Indian equities, this comes after reports last week of GQG Partners buying shares in four Adani groups. At the margins this will have helped INR outperformance against the rest of the USD/Asia bloc. INR has slipped to second best performer in the region, +0.66% month to date (THB is +0.83%), but March is traditionally a stronger seasonal month for the currency.

- The SGD NEER (per Goldman Sachs estimates) is marginally softer today, although the measure remains within recent ranges. We sit ~0.8% below the top end of the band. USD/SGD printed its highest level since late December. The broad based USD strength after Fed Chair Powells Senate testimony has weighed on the SGD. The pair is ~0.1% firmer today, last printing $1.3545/55.

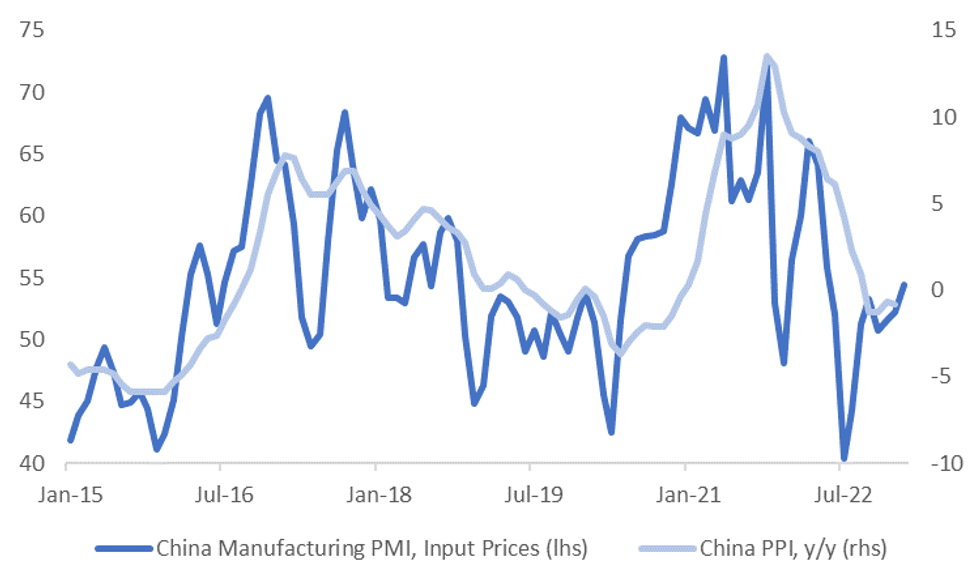

CHINA: Benign Inflation Prints Expected, But PMI Price Indices Recovered In February

A reminder that China Feb inflation figures are out tomorrow. CPI is expected at 1.9% y/y (forecast range is 1.2% to 2.3%), with the prior read at 2.1% from Jan. PPI is expected at -1.3% y/y (forecast range is -0.5% to -1.7%). The prior read in Jan was -0.8%.

- Headline consumer prices are expected to be weighed down by lower food prices and a return to more normal conditions in the services sector, post the LNY period. Note core prices rebounded to 1.0% y/y in Jan.

- Last week's PMIs showed increased price pressures in the manufacturing space. Input prices rose to 54.4 from 52.2, although this arguably suggests more upside risks to the PPI rather than CPI. Base effects and weaker commodity prices in Feb are expected to offset.

- Output prices for the manufacturing PMI were more muted but still back above 50 (51.7 versus 48.7 in Jan).

- For the non-manufacturing PMI, input prices were 51.1, down slightly, while selling prices nudged up to 50.8 from 48.3.

Fig 1: China PPI & China Manufacturing PMI Input Prices

Source: MNI - Market News/Bloomberg

MNI BNM Preview - March 2023: Likely On Hold, But External Pressures Growing

EXECUTIVE SUMMARY

- The consensus rests on no change at tomorrow’s BNM policy meeting. This would leave the policy rate at 2.75%. It is a close call though, with the Bloomberg consensus survey showing that 9 out of 20 economists expect a 25bps rate hike. The remaining 11 are forecasting no change in the policy rate. Domestic developments point to a pause, external developments are leaning the other way in terms of further tightening. On balance, we sit in the no change camp.

- Since the last policy meeting, January CPI printed in line with expectations, with the headline at 3.7% y/y. This showed a further cooling from the 2022 peak. Core pressures also moderated further, back to 3.9% y/y. We are down slightly from the late 2022 peak of 4.2%. We remain elevated by historical standards, but after January’s pause by BNM, the most recent inflation outcomes are unlikely to have shifted the BNM’s outlook.

- BNM is likely to be mindful though of external pressures in terms of renewed Fed hawkishness and fresh pressure on spot ringgit. Continued MYR weakness risks raising imported inflation pressures. Such a backdrop certainly leaves a rate hike on the cards the further we push into 2023. However, for this meeting, we suspect BNM is likely to remain in wait and see mode as it continues to assess how domestic growth and inflation dynamics are unfolding.

- See the full preview here:

EQUITIES: Weakness Across The Board, Although Nikkei Outperforms

Regional equities are mostly in the red, with Japan the outlier. With the continued move higher in US yields, particularly in the short end, the tech sector has underperformed today. US futures did dip into negative territory but are now back close too flat.

- The HSI is off around 2.5% at this stage, with the tech sector off by close to 3.8%. Outside of the hawkish Fed developments, there has also been focus on China's plans for a bureau that will tighten data security. Oversight of the banking and insurance industries is also expected.

- Mainland stocks are weaker, with the CSI 300 off by 0.66% at this stage. Northbound outflows have been modest.

- The Kopis is off by 1.3%, while the Taeix is off by 0.50%. The Nikkei 225 is an outperformer, +0.40%, with the weaker yen (near 138.00) likely helping at the margins.

- Weakness is evident elsewhere, but losses are generally under 1%.

GOLD: Bullion Struggling Under Hawkish Fed Comments, Powell Speaks Again Later

Gold prices fell 1.8% m/m on Tuesday as Fed Chairman Powell not only said that rates are likely to peak at a higher rate than expected at the last meeting but another 50bp hike is possible. His comments were more hawkish than expected by markets and Treasury yields and the USD rose, and equities sold off. He speaks in front of the House later today and in anticipation gold is down another 0.2% during APAC trading. It is currently around $1810.55/oz, close to the intraday low of $1809.50 following a high of $1814.30 earlier.

- A close to 50bp hike is now priced in by markets for the March 22 meeting, which is negative for non-yielding gold. On the other hand, China increased its gold reserves for the fourth consecutive month in February. Asia has generally been increasing its holdings of bullion.

- Gold remains above the bear trigger of $1804.90, the February 28 low. But it is approaching its 100-day simple moving average.

- Later today Fed Chairman Powell appears before the House Financial Services Committee, Barkin speaks and the Beige Book is published. ECB President Lagarde also speaks. The Bank of Canada is expected to pause. Ahead of Friday’s US employment data, there is February ADP employment and also JOLTS vacancy data. US January trade data are also released.

OIL: Crude Stable Ahead Of Further Comments From The Fed’s Powell

Oil prices fell sharply on Tuesday following Fed Chairman Powell’s more hawkish comments implying a possible 50bp move. WTI was down 4% to $77.58/bbl and is currently trading around that level, which is close to today’s intraday high. Brent is currently up 0.2% to be trading around $83.45/bbl. The USD index is up 0.2%.

- Tuesday’s correction in crude reversed the recent bull cycle. WTI held above support of $75.83, the March 3 low, and has continued to do so today.

- US API data showed that crude stocks fell 3.8mn barrels last week after rising 6.2mn. Distillate rose 1.9mn and gasoline 1.8mn. This is an early indication that extensive refining maintenance may be coming to an end. The official EIA data is published later today.

- OPEC+ Secretary General Al-Ghais said that the market was concerned about reduced oil demand from Europe and the US, even as Asian consumption is “phenomenal”.

- China imported 10.4mbd of crude in February, which was down 11% on December and -3% y/y. This data may be reflecting the build up in stocks over the last two years. (bbg)

- Later today Fed Chairman Powell appears before the House Financial Services Committee, Barkin speaks and the Beige Book is published. ECB President Lagarde also speaks. The Bank of Canada is expected to pause. Ahead of Friday’s US employment data, there is February ADP employment and also JOLTS vacancy data. US January trade data are also released.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 08/03/2023 | 0700/0800 | ** |  | DE | Industrial Production |

| 08/03/2023 | 0700/0800 | ** | | DE | Retail Sales |

| 08/03/2023 | 0900/1000 | * |  | IT | Retail Sales |

| 08/03/2023 | 0930/0930 |  | UK | BOE Dhingra at Resolution Foundation | |

| 08/03/2023 | 1000/1000 | ** | | UK | Gilt Outright Auction Result |

| 08/03/2023 | 1000/1100 | *** |  | EU | GDP (final) |

| 08/03/2023 | 1000/1100 | * | | EU | Employment |

| 08/03/2023 | 1000/1100 | | EU | ECB Lagarde at Women's Day WTO Event | |

| 08/03/2023 | 1000/1100 | | EU | ECB Panetta Intro at Euro Cyber Resilience Board | |

| 08/03/2023 | 1200/0700 | ** |  | US | MBA Weekly Applications Index |

| 08/03/2023 | 1300/0800 | | US | Richmond Fed's Tom Barkin | |

| 08/03/2023 | 1315/0815 | *** | | US | ADP Employment Report |

| 08/03/2023 | 1330/0830 | ** | | US | Trade Balance |

| 08/03/2023 | 1500/1000 | *** |  | CA | Bank of Canada Policy Decision |

| 08/03/2023 | 1500/1000 | ** | | US | JOLTS jobs opening level |

| 08/03/2023 | 1500/1000 | ** | | US | JOLTS quits Rate |

| 08/03/2023 | 1500/1000 | | US | Fed Chair Jerome Powell | |

| 08/03/2023 | 1530/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 08/03/2023 | 1700/1200 | *** | | US | USDA Crop Estimates - WASDE |

| 08/03/2023 | 1800/1300 | ** | | US | US Note 10 Year Treasury Auction Result |

| 08/03/2023 | 1900/1400 | | US | Fed Beige Book |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.