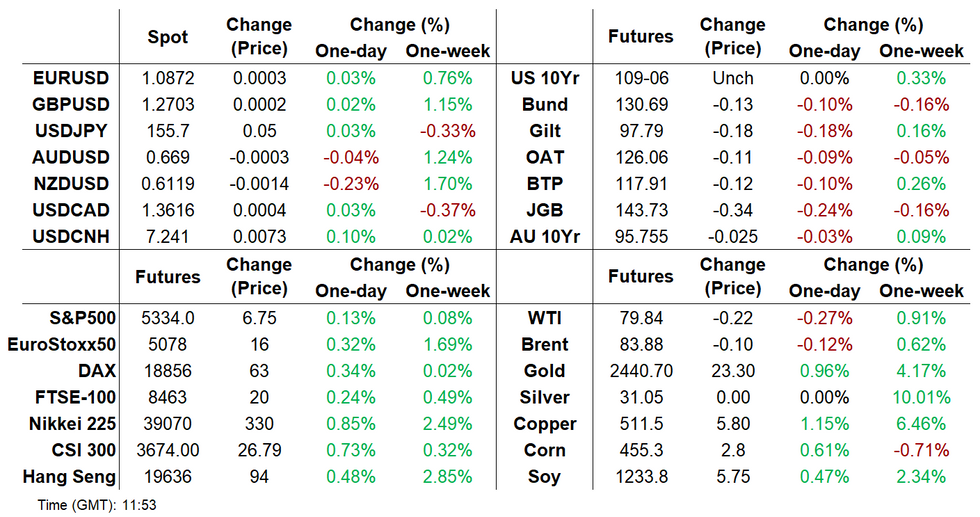

- FI & FX markets generally shrug off latest geopolitical headlines.

- Bonds and Antipodean offered FX, while gold makes new highs.

- Fedspeak highlights a thin global calendar from here, holidays in Canada and Europe are set to thin out broader liquidity.

US TSYS: Light Twist Steepening On Thin Volumes, Awaiting Fedspeak

Treasuries trade marginally twist steeper with little by way of headline drivers, with the long end outperforming EGBs and Gilts.

- Cash yields range from 0.8bp lower (3s) to 0.3bp higher (30s), with 2s10s at -39.6bps (+0.5bp) within Friday’s range.

- TYM4 has kept to narrow ranges overnight on particularly low volumes of 185k for less than 70% of recent averages for the time of day. Roll pace to the September expiry remains low, expected to pick up later this week.

- At 109-05+, it’s close to lows of 109-04, with the recent pullback going against a bullish short-term trend condition. Support is seen at 108-27+ (50-day EMA) whilst resistance is seen at 109-31+ (May 16 high).

- No data, compensated for by a heavy Fedspeak line-up.

- Fedspeak: Bostic (0730ET), Bostic (0845ET), Barr (0900ET), Waller (0900ET), Jefferson (1030ET), Mester (1400ET) and Bostic (1900ET) – see STIR bullet.

- Bill issuance: US Tsy $70B 13W, $70B 26W bill auctions (1130ET)

US TSY FUTURES: OI Points To Mix Of Short Setting & Long Cover On Friday

The combination of Friday's weakness in Tsy futures and preliminary OI data points to a mix of net short setting (TU, FV, UXY & WN futures) and long cover (TY & US futures) with the latter having slightly more impact in net curve DV01 equivalent terms.

- This came as markets continued to unwind Fed rate cut premium in a headline light session.

- Comments from ECB's Schnabel provided some pressure during pre-NY trade.

- A deeper overview of positioning in Tsy futures can be found in our weekly CFTC CoT round up.

| 17-May-24 | 16-May-24 | Daily OI Change | OI DV01 Equivalent Change ($) | |

| TU | 4,050,583 | 4,039,343 | +11,240 | +394,966 |

| FV | 6,251,048 | 6,224,339 | +26,709 | +1,091,772 |

| TY | 4,326,869 | 4,370,493 | -43,624 | -2,774,396 |

| UXY | 2,138,521 | 2,137,517 | +1,004 | +86,443 |

| US | 1,613,838 | 1,621,419 | -7,581 | -973,988 |

| WN | 1,677,086 | 1,668,679 | +8,407 | +1,671,931 |

| Total | -3,845 | -503,272 |

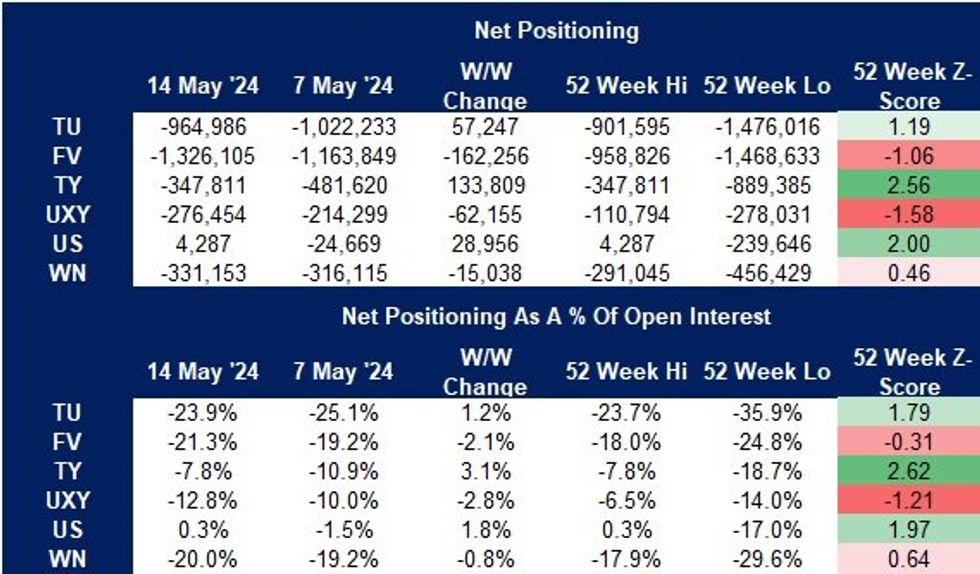

US TSY FUTURES: CFTC CoT Shows A/M Generally Adding To Duration, Hedge Funds Extending Most Shorts

The latest CFTC CoT noted a mix of net non-commercial positioning movements through Tuesday of last week.

- Net shorts were added to in FV, UXY & WN futures.

- Net shorts were pared in TU & TY futures.

- Positioning flipped net long in US futures for the first time since June '22.

- Asset managers extended on their recent run of adding to duration longs (outside of TU & TY futures).

- Meanwhile, hedge funds trimmed their net short position in TU futures. That comes after that positioning metric posted a record net short outright level in late April. They also trimmed net shorts in TY futures, but added to net shorts across the remainder of the curve.

- A reminder that the report covers a period that saw an increase in the frequency of stagflation discussions owing to U.S. data developments and doesn't cover the period seen since last Wednesday's CPI print.

STIR: Fed Rates Unchanged, Vice Chair Jefferson Headlines Fedspeak Deluge

- Fed Funds implied rates are unchanged from Friday’s close, consolidating a push further above pre-CPI/retail sales levels.

- Cumulative cuts from 5.33% effective: 1.5bp Jun, 7bp Jul, 20bp Sep, 28bp Nov and 43bp Dec.

- Today sees particularly heavy Fedspeak to compensate for a barren data docket, all from permanent voters or 2024 voters.

- On mon pol matters, we focus on Vice Chair Jefferson although Governor Waller should also be watched even if the format could limit headlines (Bostic and Mester both spoke last week) – both have had sizeable impact on markets in the past.

- Jefferson said May 13 (before PPI and CPI) that he was concerned the decline in inflation has attenuated and that it’s appropriate to hold rates steady until the Fed is more confident.

- Waller last meaningfully spoke Mar 27 when he said rate cuts are likely appropriate this year but not yet, and that the economy is giving us no reason to implement big cuts. We suspect Waller will leave the more impactful comments to tomorrow’s discussion on the US economy or Friday’s keynote address on r*.

- VC for Supervision Barr should also be watched for any new information around Basel III proposals.

Fedspeak schedule

- 0730ET – Bostic (’24) on BBG TV

- 0845ET – Bostic (’24) welcome remarks for financial mkts conference (text tbd)

- 0900ET – VC Supervision Barr (voter) gives keynote remarks on mon pol and bank regulation (text and Q&A)

- 0900ET – Waller (voter) welcoming remarks at conference for the USD’s international role (text, no Q&A)

- 1030ET – VC Jefferson speaks on US economic outlook and house prices (text and Q&A)

- 1400ET – Mester (’24 voter retiring June) on BBG TV

- 1900ET – Bostic (’24 voter) moderates keynote remarks

STIR: OI Points To Mix Of Short Setting & Long Cover In Most SOFR Contracts On Friday

The combination of Friday’s move lower in SOFR futures and preliminary OI data points to a mix of net short setting (in the red and blue packs) & long cover (in the white and green packs).

- Asia-Pac block activity in the SFRZ4 contract boosted volumes, with OI suggesting that those trades represented short cover.

- This came as markets continued to unwind Fed rate cut premium in a headline light session.

- Comments from ECB's Schnabel provided some pressure during pre-NY trade.

- Markets price in ~45bp of Fed rate cuts through year end as NY traders start to filter in on Monday.

| 17-May-24 | 16-May-24 | Daily OI Change | Daily OI Change In Packs | ||

| SFRH4 | 934,996 | 935,329 | -333 | Whites | -12,005 |

| SFRM4 | 1,203,121 | 1,197,324 | +5,797 | Reds | +9,431 |

| SFRU4 | 1,094,565 | 1,092,015 | +2,550 | Greens | -3,741 |

| SFRZ4 | 1,243,798 | 1,263,817 | -20,019 | Blues | +10,467 |

| SFRH5 | 793,308 | 781,224 | +12,084 | ||

| SFRM5 | 796,622 | 797,108 | -486 | ||

| SFRU5 | 711,139 | 711,761 | -622 | ||

| SFRZ5 | 817,024 | 818,569 | -1,545 | ||

| SFRH6 | 533,202 | 530,338 | +2,864 | ||

| SFRM6 | 518,899 | 525,093 | -6,194 | ||

| SFRU6 | 417,259 | 420,599 | -3,340 | ||

| SFRZ6 | 362,588 | 359,659 | +2,929 | ||

| SFRH7 | 250,745 | 250,732 | +13 | ||

| SFRM7 | 189,244 | 186,666 | +2,578 | ||

| SFRU7 | 180,190 | 173,094 | +7,096 | ||

| SFRZ7 | 162,960 | 162,180 | +780 |

EGBS: Biased Weaker With Headline Flow Light

Core/semi-core EGBs have traded in tight ranges this morning, currently trading weaker vs Friday’s close.

- Bunds are -15 ticks at 130.67, with volumes light due to the observance of the Whit Monday public holiday across many Eurozone countries. OAT and BTP futures trade similarly.

- Weekend news that Iran’s President had died in a helicopter crash has not generated any meaningful geopolitical risk premium, with no evidence of external involvement at this stage.

- Comments from BoE Deputy Governor Broadbent have not generated any meaningful spillovers into EGBs.

- German and French cash yields are little changed, while 10-year peripheral spreads to Bunds are biased slightly tighter.

- Primary focus this week will be the ECB’s Q1 indicator of negotiated pay growth and the May flash PMIs, both due on Thursday.

- Sell-side estimates we have seen suggest that Eurozone Q1 negotiated pay growth is set to remain above 4.0% Y/Y, although a deceleration from the 4.5% seen in Q423 is still likely.

GILTS: A Little Softer, No Meaningful Clues From BoE’s Broadbent

Bulls failed to solidify the early rebound back above 98.00 in futures, with the contract fading to fresh session lows of 97.74 in the time since.

- Initial support at 97.23 is still some way off.

- Cash gilt yields are ~1.5bp higher across the curve.

- Gilts widen vs. all major European peers across the curve.

- Some desks have noted that they are looking for entry points in gilt/bund wideners after the recent outperformance for UK paper.

- SONIA futures are flat to -4.0, with BoE-dated OIS pricing 50/50 odds of a June cut and ~54bp of easing through year end.

- Outgoing BoE Deputy Governor Broadbent spent little time discussing the upcoming policy decision - simply noting that it's “possible” that Bank Rate can be cut in the summer (and gives little hint as to his view regarding June - only that the MPC decisions are data dependent).

- Broadbent will cast his final MPC vote in June, before departing at the end of the same month.

- The DMO will hold its quarterly consultation with investors/GEMM today and the BoE will conduct GBP750mn of medium term APF gilt sales.

EUROPEAN ISSUANCE UPDATE

Slovakia auction results:

- E101mln of the 3.00% Feb-26 SlovGB. Avg yield 3.4733% (bid-to-cover 2.34x).

- E46mln of the 3.00% Feb-28 SlovGB. Avg yield 3.2473% (bid-to-cover 2.43x).

- E418mln of the 3.75% Mar-34 SlovGB. Avg yield 3.7049% (bid-to-cover 1.82x).

- E85mln of the 0.375% Apr-36 SlovGB. Avg yield 3.7865% (bid-to-cover 2.32x).

FOREX: Tight Holiday Ranges Across Global FX Markets, NZD Underperforms

While most European markets are open, the observance of the Whit Monday holiday is tempering activity to start the week, with most G10 currencies exhibiting narrow ranges as we approach the NY crossover.

- The USD index remains unchanged and hovers around 40 pips off the recent lows. Market participants will monitor the April lows just below the 104 handle as the next notable support as markets await further US data to assess short-term Fed pricing.

- NZDUSD (-0.24%) is a relative underperformer following a Q2 RBNZ survey of inflation expectations showed households saw a slightly lower median expected inflation rate for the next two years at 3% from 3.2% in 1Q. This comes ahead of the RBNZ meeting on Wednesday, where markets expect an unchanged decision.

- For USDJPY, the pullback from 156.74, the May 14 high, continues to signal the end of the corrective recovery between May 3 - 14, and a possible resumption of a short-term bearish cycle. Attention is on 153.45, the 50-day EMA, and 152.49, trendline support drawn from the Dec 28 low. Clearance of these two price points would strengthen a bearish threat. 156.74 is the resistance to watch.

- No data is due for the rest of the session, however, there could be comments from multiple Fed speakers including Bostic, Barr, Waller, Jefferson and Mester speak. The RBA minutes and Canadian inflation highlight Tuesday’s calendar.

FX OPTIONS: Expiries for May 20 NY cut 1000ET (Source DTCC)

- EURUSD: 1.0850 (859mln), 100855 (694mln), 1.0875 (935mln), 1.0890 (604mln), 1.0900 (792mln)

- GBPUSD: 1.2645 (459mln)

- USDJPY: 155.00 (644mln), 156.00 (447mln)

- NZDUSD: 0.6100 (842mln)

- EURNOK: 11.60 (568mln)

EQUITIES: EUROSTOXX 50 Trend Structure Remains Bullish

In the equity space, S&P E-Minis traded higher last week as the contract extends the bull cycle from Apr 19. Recent gains have resulted in a break of key resistance at 5333.50, Apr 1 high. This confirms a resumption of the primary uptrend and signals scope for a climb to 5372.73, 1.764 projection of the Apr 19 - 29 - May 2 price swing. Initial support is at 5218.92, the 20-day EMA.

- EUROSTOXX 50 futures maintain a bullish tone despite the latest pullback. Last week’s gains resulted in a break of key resistance at 5079.00, the Apr 2 high, to confirm a resumption of the uptrend and maintain the price sequence of higher highs and higher lows. This opens 5127.70 next,1.382 projection of the Jan 17 - Feb 12 - 13 price swing. The initial support zone to watch is 5006.50/4934.90, the area between the 20- and 50- day EMAs.

COMMODITIES: Gold Bulls Remains In The Driver's Seat

On the commodity front, the medium-term trend structure in Gold is unchanged and remains bullish. Today’s gains reinforce this condition - the yellow metal has traded through resistance at $2431.5, the Apr 12 high and bull trigger. The break confirms a resumption of the primary uptrend and opens 2452.5 next, 2.618 projection of the Oct 6 - 27 - Nov 13 price swing. Initial support lies at $2343.6, the 20-day EMA.

- In the oil space, despite the latest move higher, a bearish theme in WTI futures remains intact and short-term gains are considered corrective. Price has recently traded below the 50-day EMA, strengthening a bearish set-up. Scope is seen for a move to $76.07, the Mar 11 low. Initial firm resistance to watch is at $84.46, the Apr 26 high.

| Date | GMT/Local | Impact | Flag | Country | Event |

| 20/05/2024 | - |  | UK | DMO to hold quarterly consultation investors / GEMM consultation | |

| 20/05/2024 | 1530/1130 | * |  | US | US Treasury Auction Result for 26 Week Bill |

| 20/05/2024 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |

| 21/05/2024 | 0130/1130 |  | AU | RBA Minutes | |

| 21/05/2024 | 0800/1000 | ** |  | EU | Current Account |

| 21/05/2024 | 0900/1100 | ** | | EU | Construction Production |

| 21/05/2024 | 0900/1100 | * | | EU | Trade Balance |

| 21/05/2024 | 0900/1000 | ** | | UK | Gilt Outright Auction Result |

| 21/05/2024 | 1000/1100 | ** | | UK | CBI Industrial Trends |

| 21/05/2024 | 1230/0830 | *** |  | CA | CPI |

| 21/05/2024 | 1230/0830 | ** | | US | Philadelphia Fed Nonmanufacturing Index |

| 21/05/2024 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 21/05/2024 | 1300/0900 | | US | Fed Governor Christopher Waller | |

| 21/05/2024 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 21/05/2024 | 1700/1800 | | UK | BOE's Bailey Lecture at LSE | |

| 21/05/2024 | 2300/1900 | | US | Atlanta Fed's Raphael Bostic | |

| 21/05/2024 | 2300/1900 | | US | Cleveland Fed President Loretta Mester |