Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

Highlights:

- PBoC fire first warning shot on CNY weakness

- Downtrend in Gilt futures accelerates

- Market focus turns to Powell appearance alongside London close

US TSYS: Recent Cheapening As US Desks Come In Ahead Of Powell et al

- Some recent cheapening pressure as the US comes in sees Cash Tsys back almost unchanged on the day with only the 2Y more modestly outperforming. More broadly, Treasuries heavily outperform core EU FI. Today’s is headlined by three important Fed speakers, even more so considering the dearth of any other releases, with any r* discussions closely watched for at the Laubach Research Conference.

- 2YY -0.9bp at 4.242%, 5YY +0.0bp at 3.685%, 10YY -0.2bp at 3.644%, 30YY +0.2bp at 3.906%.

- TYM3 trades just 1 tick higher at 113-30+, keeping to a relatively narrow range off a low of 113-28+. Cumulative volumes are higher than recent averages at 280k. It came close to initial resistance at yesterday’s low of 113-27+, in turn closely followed by 113-26 (May 22 low) and 113-23 (50% retracement of Mar 2-24 rally).

- Fedspeak: NY Fed’s Williams (0845ET, text + Q&A), Gov. Bowman (0900ET, text + Q&A), Chair Powell (1100ET, panel/Q&A)

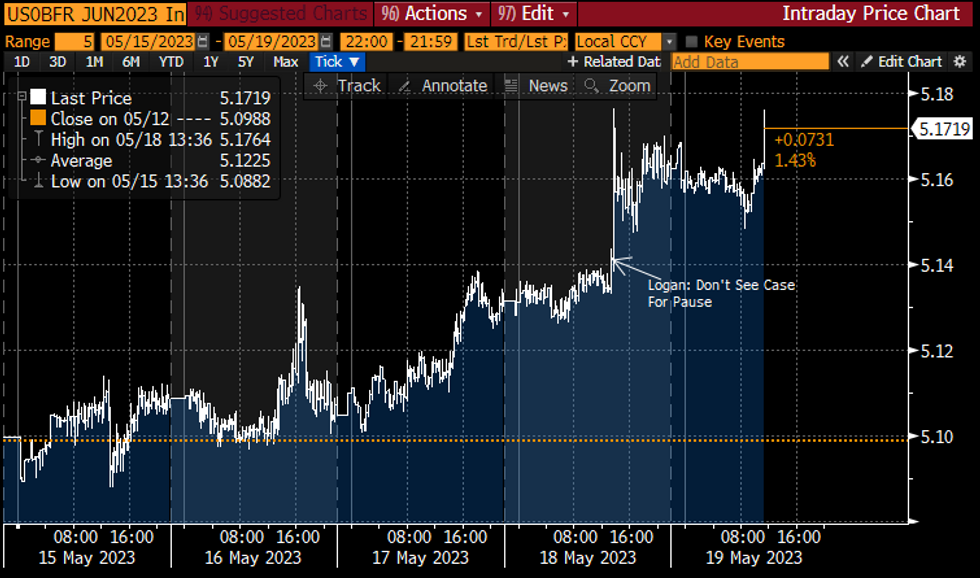

STIR FUTURES: Fed Rate Path Nears Post-Logan Highs With R* Discussions Watched

- Fed-dated OIS implied rates have quickly stepped higher in recent trade at/nearer to yesterday’s highs seen after Logan suggested a higher bar to a June pause than first thought.

- Cumulative changes from 5.08% effective: +9.5bp Jun (+1.5bp on the day), +7.5bp Jul (+1bp), -3bp Sep (+1bp), -21.5bp Nov (+0.5bp), -43bp Dec (+0.5bp) and -65bp Jan (+0.5bp).

- Musings at the Thomas Laubach Research Conference likely headline the session. NY Fed’s Williams delivers the keynote address with text + Q&A at 0845ET before Chair Powell is in a panel with Bernanke 1100ET coming after a session on the consequences of declining natural rates. The Laubach-Williams r* connection sees markets eagerly await any discussion on the matter.

OIS implied rate for June FOMCSource: Bloomberg

OIS implied rate for June FOMCSource: Bloomberg

CHINA: PBoC Fires First Warning Against CNY Weakness

- The PBoC re-state their vow to curb speculation in the FX market, urging institutions to maintain FX market stability. The statement sees curbing of speculation "when necessary".

- USD/CNH edging to fresh daily lows on the back of that headline - pair prints 7.0206 to extend losses on the day to 0.4%.

- Yesterday's Asia-Pac session low next up at 7.0078 - and could presage a symbolic move back below the 7.00 handle

- Warning from the PBoC follows the ~1% rally in USD/CNY this week. Notably, the USD/CNY fix today was the first above 7.00 since December last year - showing that the authorities were not standing against the CNY drift lower (perhaps until now). * Recall back in March PBOC governor stated that USD/CNY at 7.00 was no longer a 'psychological hurdle' for the pair.

MNI PBOC WATCH: LPR Change Unlikely Despite Calls For Cut

China’s reference lending rate will likely remain unchanged this month, with banks having already cut loan rates under central bank guidance, and despite calls for a cut to boost credit demand and support economic recovery, policy advisors and economists told MNI

The People’s Bank of China will update the loan-prime rate Monday based on the PBOC’s Medium-term Lending Facility (MLF) rate and quotes submitted by 18 banks. The LPR's one-year maturity (3.65%) and the over-five- year maturity (4.3%) have remained unchanged since August 2022.

The PBOC kept the MLF rate steady this month and lenders’ loan rates have fallen at a faster pace than the LPR, suggesting a cut is unlikely, according to Wen Bin, chief economist at China Minsheng Banking Corp. Wen noted that while the one-year and over-five-year LPR have been cut by 15bp and 35bp since 2022, the general loan rate has dropped by 62bps and the mortgage rate has slumped over 100bps as of the end of 2022.

Kremlin-Last Remnants Of Arms Control Agreements w/US Disappearing

Wires reporting comments from Kremlin spox Dimitri Peskov has stated that the 'last remnants' of any arms control agreements between Russia and the United States are disappearing. On 18 May, US Senator Tom Cotton (R-AK) introduced a bill with the support of nine other GOP senators seeking to withdraw the US from the New START treaty.

- Sen. Marco Rubio (R-FL): “Treaties aren’t effective when one party lies and cheats. We’ve seen evidence for the last decade that Russia is no longer honoring its obligations under the New START Treaty. It is irresponsible and dangerous for America to unilaterally limit itself in the face of growing hostility abroad, including from the Chinese Communist Party,”

- In February, Russian President Vladimir Putin officially suspended his country's participation in New START.Andoulou Agency outlines the treaty's restrictions: "The treaty limits the number of deployed missiles and bombers to 700, deployed warheads (including multiple independently targetable reentry vehicles and bombers) to 1,550, and deployed and non-deployed launchers – missile tubes and bombers – to 800."

- The two nations have already stopped sharing nuclear data with one another. While the Biden administration has not given any signal that it intends to withdraw from New START, and the Cotton bill is unlikely to make it past the Senate, the trend towards fewer nuclear arms control treaties inevitably raises geopolitical risks worldwide.

FOREX: Greenback Strength Abates, Providing Relief Among Majors

- The greenback sits softer early Friday as the currency pulls back a small part of this week's rally. Nonetheless, the USD Index remains stronger on the week by around 0.7%. GBP is similarly weak, allowing the EUR/GBP May pullback to abate slightly off the mid-month lows at and prevent the RSI from tilting into oversold territory.

- Antipodean currencies are firmer, keeping AUD and NZD top of the pile in G10. NZD/USD remains pinned within the 50- and 100-dma channel, leaving 0.6275 as the main upside level. Market moves come ahead of the RBNZ rate decision next week, at which consensus looks for a 25bps hike to 5.50% - with a number of sell-side analysts switching their views to see a peak rate further north of current levels after this week's budget.

- Weakness in the Chinese currency put in a minor reversal Friday, helping drag USD/CNH back below the 7.04 level - nonetheless, the onshore currency close cemented a 1% decline on the week.

- A light data slate Friday should keep focus on the speaker calendar - with Fed's Powell, Williams & Bowman scheduled as well as ECB's Schnabel, Lagarde and de Cos. Canadian retail sales round off the week's economic releases, expected to slow to -1.4% from -0.2% prior for the headline.

FX OPTIONS: Expiries for May19 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0750(E539mln), $1.0820-35(E747mln), $1.0850(E943mln), $1.0900(E831mln)

- USD/JPY: Y136.00($650mln)

- GBP/USD: $1.2280-90(Gbp732mln)

- AUD/USD: $0.6645-50(A$545mln)USD/CAD: C$1.3500($1.4bln)

- USD/CNY: Cny7.00($2.4bln)

EQUITIES: Eurostoxx 50 Futures, E-Mini S&Ps Trade to Fresh Cycle Highs

- Eurostoxx 50 futures traded higher yesterday and cleared resistance at 4363.00, the Apr 21 high and the bull trigger. The break confirms a resumption of the bull cycle that started Mar 20 and confirms a continuation of the medium-term uptrend. This opens the 4400.00 handle ahead of 4409.50, the Nov 18 2021 high on the continuation chart and a key resistance. Key support has been defined at 4233.00, the May 4 low.

- S&P E-minis traded higher again Thursday and the contract has cleared key resistance and the bull trigger at 4206.25, the May 1 high. Clearance of this level confirms an extension of the bull trend from Mar 13. This opens 4244.00, the Feb 2 high and the next key short-term resistance. Key support is at 4062.25, the May 4 low. A move through this level would highlight a bearish threat.

COMMODITIES: Gold Remains in Bearish Cycle and Close to Recent Lows

- WTI futures traded higher Wednesday. However, a short-term bearish threat remains present and initial resistance at $73.93, the Apr 28 low, is intact. A resumption of weakness and a break of $69.41, the May 15 low, would strengthen near-term bearish conditions. The recent print below $64.58, the Mar 20 low and a key support, is a medium-term bearish development. A clear break of it would resume the broader downtrend.

- Gold remains in a bearish cycle and is trading closer to its recent lows. The yellow metal has cleared support at $1976.2, the 50-day EMA and $1969.3, the Apr 19 low. A clear break of this support zone highlights a stronger bearish threat and opens $1934.3, the Mar 22 low. Key resistance and the bull trigger is at $2063.0, the May 4 high. Initial firm resistance is at $2022.6, the May 12 high.

| Date | GMT/Local | Impact | Flag | Country | Event |

| 19/05/2023 | 1230/0830 | ** |  | CA | Retail Trade |

| 19/05/2023 | 1245/0845 |  | US | New York Fed's John Williams | |

| 19/05/2023 | 1300/0900 | | US | Fed Governor Michelle Bowman | |

| 19/05/2023 | 1400/1000 | * | | US | Services Revenues |

| 19/05/2023 | 1455/1655 |  | EU | ECB Schnabel Speech at Conference on Financial Stability and Monetary Policy | |

| 19/05/2023 | 1500/1100 | | US | Fed Chair Jerome Powell | |

| 19/05/2023 | 1600/1800 | | EU | ECB Schnabel Panels Conference on Financial Stability and Monetary Policy | |

| 19/05/2023 | 1900/2100 | | EU | ECB Lagarde Video Presentation at Banco Central Brasil |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.