Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY:

- GERMANY PREPARED FOR ALL GAS SUPPLY SCENARIOS: ECON MINISTER HABECK

- ZEW SURVEY SEES GERMAN ECONOMIC CONFIDENCE COLLAPSE

- JAPAN SUZUKI, U.S. YELLEN TO CLOSELY COOPERATE ON FX

- NAGEL URGES ECB ACTION ON RISK OF HIGHER MEDIUM-TERM INFLATION

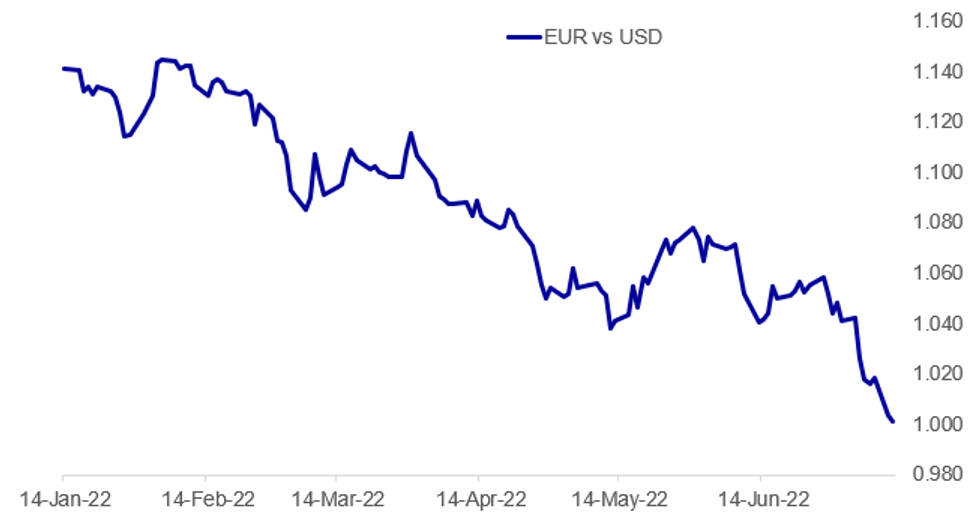

Fig. 1: EURUSD On The Cusp Of Parity

Source: BBG, MNI

Source: BBG, MNI

NEWS:

GERMANY / EUROPE ENERGY: Wires carrying comments from German Economy Minister and Vice-Chancellor Robert Habeck claiming that 'Germany is prepared for all gas supply scenarios'.

- There has been escalating concern in Germany that following a 40% reduction in gas supplies via the Nord Stream pipeline recently, that Russia could eventually fully halt supplies during the height of winter, resulting in a major energy crisis.

- Nord Stream is at present shut for a minimum of 10 days to allow for routine maintenance. The pipeline is also waiting on the shipping of a turbine from Canada, where it was being repaired. Canada could not ship the part directly to Russia due to sanctions, so is shipping it to Germany before it is passed on.

US / JAPAN (RTRS): U.S. Treasury Secretary Janet Yellen on Tuesday acknowledged the Japanese yen's substantial depreciation in recent weeks, but said the U.S. view remained that currency intervention was warranted only in "rare and exceptional circumstances."Yellen, speaking after separate meetings with Japanese Finance Minister Shunichi Suzuki and Bank of Japan Governor Haruhiko Kuroda, said they had reviewed the yen's recent depreciation, but did not discuss currency intervention or related policy. She told reporters that the United States believed that countries such as Japan, the United States and other members of the Group of Seven rich nations should have market-determined exchange rates, and "only in rare and exceptional circumstances is intervention warranted."

US / JAPAN: Japan’s Finance Minister Shunichi Suzuki told reporters on Tuesday that he and U.S. Treasury Secretary Janet Yellen agreed to closely contact with movements of foreign exchange rates and they also agreed to closely cooperate with them in an appropriate manner. Suzuki also said that they agreed with the view that high volatility of forex rates caused by the Russian’s invasion of Ukraine has had an adverse impact on the stability of forex rates. He told Yellen that Japanese authorities keep close eye on forex moves with a sense of urgency, and later issued a joint statement. Earlier in the day, Yellen appeared to have met with Bank of Japan Governor Haruhiko Kuroda at the BOJ headquarters in Tokyo to exchange view on global economic and financial conditions. A BOJ spokesman did not confirm and deny the meeting.

ECB (BBG): The European Central Bank must act to prevent faster-than-expected inflation from becoming increasingly self-sustained, according to Governing Council member Joachim Nagel. Euro-area price growth hit a fresh record of 8.6% in June -- above what most economists had expected and more than four times the 2% goal -- with Nagel warning that “this also increases the risk that inflation will remain higher in the medium term.” “As the Governing Council, we are measured by our words and, above all, by our actions,” he told an event Tuesday in Munich. “We need to bring inflation back to our target in the medium term.”

US / OPEC: Joe Biden will push for higher crude output levels from OPEC nations when he meets Gulf Leaders in Saudi Arabia this week according to White House national security adviser Jake Sullivan.

- "We will convey our general view…that we believe that there needs to be adequate supply in the global market to protect the global economy and to protect the American consumer at the pump," Sullivan said.

- Biden heads for his first Middle East trip as president today, with stops in Israel, the West Bank and Saudi Arabia on his agenda.

UK POLITICS: The Conservative party leadership contest officially begins today, with nominations to get on the ballot opening and closing. Last night, following elections to the executive of the 1922 Committee of backbench Conservative MPs, the body decided on the official rules for the party's leadership campaign. Nominations are open today, closing at 1800BST. Meanwhile, Labour is expected to table a vote of no confidence in the government today, with a vote likely to be held tomorrow. There is very little chance of this passing given that a Conservative leadership contest is already underway and the process is as expediated as it can be given the timing of the summer recess. It is more political theatre with no real impact. The other UK story to look out for today (other than if there are any other names thrown into the hat for the leadership contest) are more details on Rishi Sunak's leadership campaign.

UK: The UK will see limited near-term economic impact from the resignation of Prime Minister Boris Johnson, but uncertainties are growing, ratings agency DBRS Morningstar said Tuesday. An incoming new leader of the Conservative Party -- and therefore de facto PM -- could change the overall direction of fiscal and monetary policy, with potential implications for the outlook, but overall, 'in the longer term, (the government's) fiscal policy will follow a broadly prudent path," according to Adriana Alvarado, Senior Vice President in the Global Sovereign Ratings Group.

UKRAINE - RUSSIA: Interfax reports that the next round of consultations between Russian and Turkish militaries on Ukrainian grain exports will take place in Istanbul tomorrow. Ukraine and the United Nations are to join Russia and Turkey in the consultations concerning a grain export corridor.

DATA:

GERMANY JUL ZEW CURRENT CONDITIONS -45.8

- MNI: GERMANY JUL ECONOMIC SENTIMENT INDEX -53.8

FIXED INCOME: Moving higher as risk-off themes continue

Core fixed income has moved higher again in response to risk-off themes - a combination of Chinese concerns surrounding Covid-19 , a disappointing ZEW survey and continued USD appreciation (with the focus in FX-land very much on EURUSD being very close to breaking parity). Again we have seen UST and gilt curves flatten but the German curve steepen.

- Today there is not much on the calendar in terms of data, but there are a couple of important speeches due later, particularly from the Fed's Barkin and BOE's Bailey (see a preview of the latter's speech here).

- UK politics will continue to make headlines today, with the deadline to enter the race to be next Tory leader (and PM) due to close today at 18:00BST. Sunak (current favourite in betting markets) is also due to set out more of his policies today.

- The market also already has one eye on tomorrow's US CPI data.

- TY1 futures are up 0-20+ today at 119-00+ with 10y UST yields down -7.2bp at 2.923% and 2y yields down -8.0bp at 2.995%.

- Bund futures are up 1.67 today at 153.07 with 10y Bund yields down -12.8bp at 1.114% and Schatz yields down -9.7bp at 0.329%.

- Gilt futures are up 1.08 today at 116.14 with 10y yields down -12.0bp at 2.056% and 2y yields down -14.5bp at 1.717%.

FOREX: EUR/USD Seeing Fierce Support at Parity... So Far

- Currency markets continue to keep a very close eye on EUR/USD as the pair trades at new multi-decade lows and within striking distance of the key psychological parity level - a price markets haven't traded below since 2002.

- Today's test of the level is notable for a number reasons - the USD is seeing broad-based strength as has been the case in a number of recent sessions, but the EUR is also weaker on Tuesday, with a soft ZEW Survey and continued concerns surrounding the outage of the Nord Stream pipeline knocking sentiment.

- Additionally, today 1.0000 does not only mark psychological support, but also the base of the bear channel drawn off the February high (see chart below) - a technical indicator that has successfully provided support on numerous occasions this year. Additionally, this week's price action has put EUR/USD solidly in oversold territory. On an RSI basis, EUR/USD is now the most technically oversold since Q1 2020 and the depths of the COVID crisis.

- GBP is the worst performer in G10 so far Tuesday, closely followed by the EUR. JPY is seen strongest, closely followed by the dollar.

- With no major data releases due Tuesday, focus turns to speeches from ECB's Villeroy, Fed's Barkin and BoE's Bailey.

EQUITIES: Defensives Shine Again Amid Broad Losses

- Asian markets closed lower: Japan's NIKKEI closed down 475.64 pts or -1.77% at 26336.66 and the TOPIX ended 31.36 pts lower or -1.64% at 1883.3. China's SHANGHAI closed down 32.117 pts or -0.97% at 3281.467 and the HANG SENG ended 279.46 pts lower or -1.32% at 20844.74.

- European equities are softer, with defensives (eg Utilities, Consumer Staples) alone in the green the German Dax down 87.42 pts or -0.68% at 12790.44, FTSE 100 down 7.67 pts or -0.11% at 7177.74, CAC 40 down 10.72 pts or -0.18% at 5974.07 and Euro Stoxx 50 down 20.28 pts or -0.58% at 3458.99.

- U.S. futures are lower, with the Dow Jones mini down 165 pts or -0.53% at 30974, S&P 500 mini down 20.75 pts or -0.54% at 3835.75, NASDAQ mini down 57.75 pts or -0.49% at 11824.75.

COMMODITIES: Dollar Continues To Weigh

- WTI Crude down $2.36 or -2.27% at $103.89

- Natural Gas up $0.06 or +0.96% at $6.489

- Gold spot up $1.35 or +0.08% at $1735.94

- Copper down $6.45 or -1.88% at $341.95

- Silver down $0.19 or -1.01% at $19.182

- Platinum down $16.91 or -1.94% at $872.33

LOOK AHEAD:

| Date | GMT/Local | Impact | Flag | Country | Event |

| 12/07/2022 | 1000/0600 | ** |  | US | NFIB Small Business Optimism Index |

| 12/07/2022 | - |  | EU | ECB de Guindos at ECOFIN Meeting | |

| 12/07/2022 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 12/07/2022 | 1400/1000 | ** | | US | IBD/TIPP Optimism Index |

| 12/07/2022 | 1530/1130 | ** | | US | US Treasury Auction Result for 52 Week Bill |

| 12/07/2022 | 1600/1200 | *** | | US | USDA Crop Estimates - WASDE |

| 12/07/2022 | 1630/1230 | | US | Richmond Fed's Tom Barkin | |

| 12/07/2022 | 1700/1300 | ** | | US | US Note 10 Year Treasury Auction Result |

| 13/07/2022 | 0600/0700 | *** |  | UK | Index of Production |

| 13/07/2022 | 0600/0700 | ** | | UK | Output in the Construction Industry |

| 13/07/2022 | 0600/0700 | ** | | UK | Trade Balance |

| 13/07/2022 | 0600/0700 | ** | | UK | Index of Services |

| 13/07/2022 | 0600/0700 | ** | | UK | UK Monthly GDP |

| 13/07/2022 | 0600/0800 | *** |  | DE | HICP (f) |

| 13/07/2022 | 0645/0845 | *** |  | FR | HICP (f) |

| 13/07/2022 | 0900/1100 | ** | | EU | industrial production |

| 13/07/2022 | 1100/0700 | ** | | US | MBA Weekly Applications Index |

| 13/07/2022 | - | *** |  | CN | Trade |

| 13/07/2022 | 1230/0830 | *** | | US | CPI |

| 13/07/2022 | 1400/1000 | *** |  | CA | Bank of Canada Policy Decision |

| 13/07/2022 | 1400/1000 | | CA | BOC Monetary Policy Report | |

| 13/07/2022 | 1430/1030 | ** | | US | DOE weekly crude oil stocks |

| 13/07/2022 | 1430/1030 | ** | | US | DOE weekly crude oil stocks |

| 13/07/2022 | 1500/1100 | | CA | BOC press conference | |

| 13/07/2022 | 1700/1300 | *** | | US | US Treasury Auction Result for 30 Year Bond |

| 13/07/2022 | 1800/1400 | ** | | US | Treasury Budget |

| 13/07/2022 | 1800/1400 | | US | Federal Reserve Beige Book |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.