Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS/SUPPLY

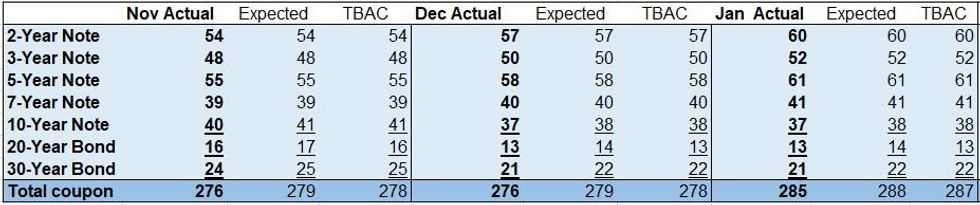

Today's quarterly refunding brought a more market-friendly announcement than expected/feared, both on long-end auction sizes and on Treasury's guidance that "Treasury anticipates that one additional quarter of increases to coupon auction sizes will likely be needed beyond the increases announced today" (some had expected increases through not just Feb but potentially the May refunding).

- The table below shows the actual announced coupon sizes vs MNI expectations (which were close to consensus), and TBAC recommendations. Overall it's about $9B in total nominal coupon size less than expected across the three months, offset somewhat by FRN and TIPS increase (not shown here, though those were broadly in line).

- Treasury's new issue sizes are close to TBAC's recommendations for this quarter - differences are: Treasury went $1B smaller on 10Y and 30Y for this quarter than TBAC's recommendations. See PDF.

- Tsy also boosted FRN reopenings $2B in each of for Nov and Dec whereas TBAC saw no change to those months; TIPS were upsized in line with TBAC's recommendations and weren't surprising (maintain November 10-year TIPS reopening auction size at $15B, increase December 5-year TIPS reopening auction size by $1B to $20B, and increase January 10-year TIPS new issue auction size by $1B to $18B).

- For the following quarter (Feb-Apr 24) TBAC recommends similar increases to those they recommended in this quarter (incl unch 20Y once again).

Underlined figures show tenors where figures differSource: MNI

Underlined figures show tenors where figures differSource: MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok