Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMAN DATA

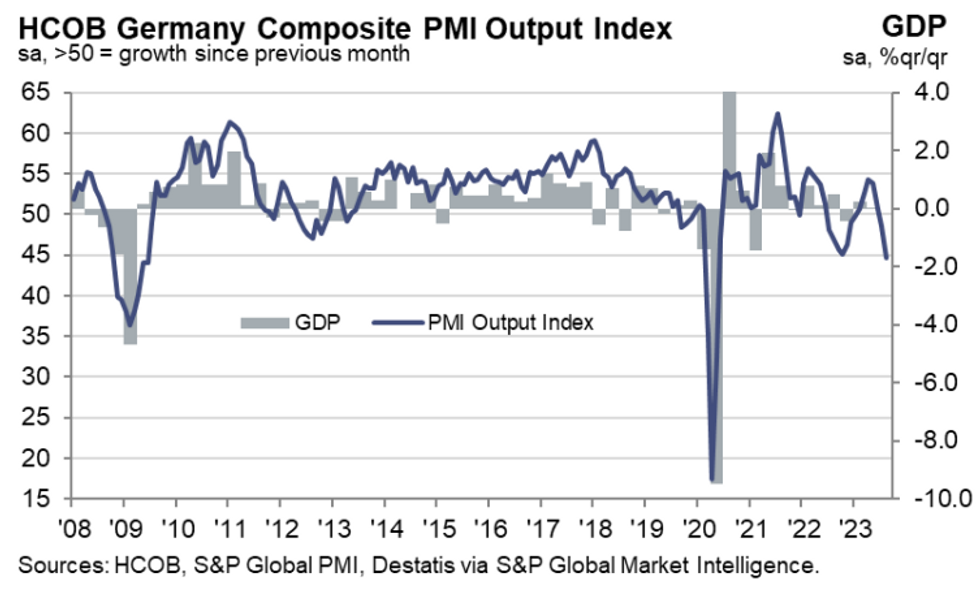

As presaged by a weak French August Flash PMI 15 minutes prior, Germany's report showed more weakness in the Services sector than expected - contrasting with continued inflationary pressures, making for a "stagflationary" report.

- German Manufacturing PMI actually ticked up to to a 2-month high of 39.1 (vs expectations of remaining unchanged at 38.8 in July), but this was more than offset by Services PMI dropping to a 9-month low of 47.3 versus July's 52.3, and expectations that the sector would remain in expansionary territory at 51.5. The Composite reading dropped to a 39-month low (May 2020) 44.7 from 48.5 in July, vs expectations of a more modest dip to 48.3.

- This was very much a recessionary report from HCOB / S&P Global, who note that such readings are consistent with a GDP reading of -1%. The 4th consecutive contractionary reading in the Composite number came alongside a drop in new business inflows across the private sector - manufacturing new orders lowest since May 2020, services since Nov 2022, with both seeing sustained declines in new export business.

- With backlogs declining again, as new orders failed to replace completed orders, total employment was broadly unchanged (the report notes Services job creation "virtually stalled".

- However, "Notably, the survey showed an increase in inflationary pressures, driven by accelerated cost and price increases in the service sector." Input cost and output prices rose for the first time in 11 / 7 months, respectively. There was a "steep and accelerated increase in operating expenses faced by services firms, who not only commented on the higher cost of fuel, but also sustained wage pressures".

- Indeed, the report describes the dynamics in the services sector as "stagflation". As such while it's recessionary, it's not entirely comforting reading for the ECB which has been eyeing stubborn wage / inflation dynamics in the services sector as a reason not to be wary of ending its tightening cycle.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok