Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY

- MNI FED: Former Fed Pres' Dudley, Lacker on Rates

- MNI: Italy Wants Permanent Lending Facility In EU Debt Talks

- BOE'S BAILEY: `I'M VERY UNEASY ABOUT THE INFLATION SITUATION', Bbg

US

FED: Former NY Fed Pres Bill Dudley and Richmond Fed Jeffrey Lacker commented on BBG TV earlier, estimating rising rates in 2022 as the Fed combats rising inflation.

- Dudley estimated rates could rise to 3-4% while Lacker said "It seems to be plausible we get to 3.5% or 4% and in addition that we push the economy into a recession."

US OUTLOOK/OPINION: Jefferies Quicktake on Tapering, Policy, Labor

Jefferies Chief Economist Aneta Markowska and Money Market Economist Thomas Simons looking for a quicker asset purchase tapering than currently expected as well as two hikes in 2022.

- With inflation pressures mounting, we expect the Fed to respond by accelerating the taper at the December meeting and finishing by the end of March. This will make room for two hikes next year, most likely in September and December.

- On Labor market, Markowska and Thomas "believe the US is entering the tightest labor market conditions since the 1950s. Thus, even after supply chain bottlenecks are cleared, inflation is unlikely to go back to 2% and is more likely to settle in a 2.5%-3% range."

EU

ITALY: Italy and other southern states are pressing for talks on a new fiscal regime for the European Union to include the creation of a permanent European Union lending facility along the lines of the Recovery and Resilience Facility implemented in the wake of the Covid pandemic, MNI understands.

- The talks, expected to last well into next year at least, currently centre on redrawing rules on public borrowing and indebtedness contained in the Stability and Growth Pact. Italy argues that the experience of the RRF, which conditions disbursement of funds on progress in key reforms, shows that access to a new facility could be an effective way of incentivising compliance with a new fiscal regime, one source said. For more see MNI Policy main wire at 1246ET.

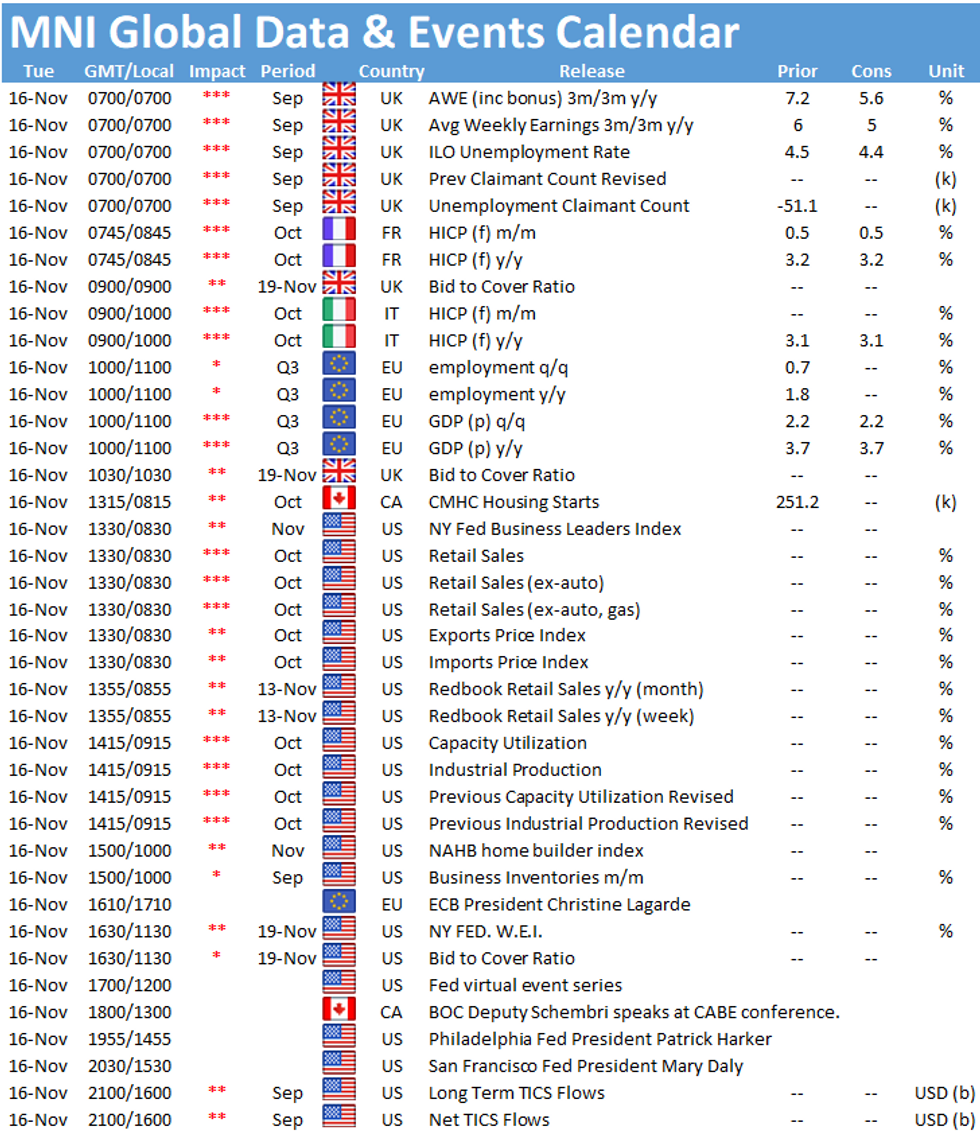

US TSYS: Tsy Futures Back To Early Nov Levels, Data Picks Up Tuesday

Carry-over moderate support for rates overnight dissipated quickly after the NY open, initially triggered by weaker German Bunds Monday. No obvious headline trigger on moves as rate futures continued to make new lows after the close while equities traded mildly lower (ESZ1 -2.5).- Some desks cited higher yields for weaker stocks, while former Fed pres' Dudley and Lacker interview on Bbg TV didn't help: estimated rates could rise to 3-4% while Lacker said "It seems to be plausible we get to 3.5% or 4% and in addition that we push the economy into a recession."

- Limited data: NY Empire State Manufacturing survey was stronger than expected in November, bringing with it further inflationary pressures; mfg business conditions index was above consensus in Nov, up from 19.8 to 30.9 (survey 22). Focus on Tue's Retail Sales, Import/export prices, IP/Cap-U.

- Tsys drew sporadic fast$ buying covering tactical shorts, two-way deal-tied hedging/unwinds, while larger theme remains better real$ and bank portfolio selling in 10s and 30s as volumes gradually improved. Yield curves bear steepened as Tsy futures slipped back to early Nov levels (5s30s well off early Fri's 63.704 low to 75.673 in late trade).

- The 2-Yr yield is up 0.6bps at 0.5177%, 5-Yr is up 3.1bps at 1.2522%, 10-Yr is up 5.7bps at 1.618%, and 30-Yr is up 7bps at 2.0008%.

OVERNIGHT DATA

- US NY FED EMPIRE STATE MFG INDEX 30.9 NOV

- US NY FED EMPIRE MFG NEW ORDERS 28.8 NOV

- US NY FED EMPIRE MFG EMPLOYMENT INDEX 26.0 NOV

- US NY FED EMPIRE MFG PRICES PAID INDEX 83.0 NOV

- CANADIAN SEP MANUFACTURING SALES -3.0% MOM

- CANADA SEP FACTORY INVENTORIES +1.3%; INVENTORY-SALES RATIO 1.67

- CANADA SEP WHOLESALE SALES +1.0%; EX-AUTOS +1.6%

- CANADA SEP WHOLESALE INVENTORIES +1.4%: STATISTICS CANADA

NY Empire Mfg: Stronger Conditions, Stronger Prices

The NY Empire State Manufacturing survey was stronger than expected in November, bringing with it further inflationary pressures.

- The NY Empire State Mfg business conditions index was above consensus in Nov, up from 19.8 to 30.9 (survey 22).

- The prices paid component increased to the second-highest on record with an immediate response in selling prices to the highest in twenty years of data.

- Other areas more mixed, with strong labour market indicators and a minor improvement in supply-chains but a deteriorating six-month outlook.

- The initial reaction saw a bear steepening in Tsys with relatively little response in shorter-end (2s/10s up 2bps to 106.5bp) and minimal response in DXY.

MARKET SNAPSHOT

Key late session market levels:

- DJIA down 2.57 points (-0.01%) at 36186.77

- S&P E-Mini Future down 2.5 points (-0.05%) at 4685.25

- Nasdaq down 34.4 points (-0.2%) at 15888.74

- US 10-Yr yield is up 5.5 bps at 1.6162%

- US Dec 10Y are down 6.5/32 at 130-10.5

- EURUSD down 0.0057 (-0.5%) at 1.144

- USDJPY up 0.17 (0.15%) at 113.97

- WTI Crude Oil (front-month) up $0.13 (0.16%) at $79.46

- Gold is up $1.95 (0.1%) at $1861.29

- EuroStoxx 50 up 15.86 points (0.36%) at 4379.46

- FTSE 100 up 3.95 points (0.05%) at 7335.69

- German DAX up 54.57 points (0.34%) at 16127.49

- French CAC 40 up 37.23 points (0.53%) at 7124.39

US TSY FUTURES CLOSE

- 3M10Y +7.449, 158.003 (L: 148.255 / H: 158.003)

- 2Y10Y +5.587, 109.968 (L: 102.718 / H: 110.4)

- 2Y30Y +7.504, 148.832 (L: 139.911 / H: 149.247)

- 5Y30Y +4.652, 75.297 (L: 69.992 / H: 75.673)

- Current futures levels:

- Dec 2Y steady at at 109-19 (L: 109-17.75 / H: 109-20.375)

- Dec 5Y down 2.5/32 at 121-13 (L: 121-12 / H: 121-21)

- Dec 10Y down 8/32 at 130-9 (L: 130-08.5 / H: 130-27.5)

- Dec 30Y down 1-6/32 at 160-6 (L: 160-05 / H: 162-02)

- Dec Ultra 30Y down 2-4/32 at 193-15 (L: 193-12 / H: 196-31)

US EURODOLLAR FUTURES CLOSE

- Dec 21 +0.000 at 99.790

- Mar 22 +0.010 at 99.745

- Jun 22 +0.010 at 99.550

- Sep 22 +0.005 at 99.325

- Red Pack (Dec 22-Sep 23) steady to +0.010

- Green Pack (Dec 23-Sep 24) -0.015 to -0.005

- Blue Pack (Dec 24-Sep 25) -0.035 to -0.025

- Gold Pack (Dec 25-Sep 26) -0.04 to -0.035

SHORT TERM RATES

US DOLLAR LIBOR: Latest settlements

- O/N +0.00025 at 0.07500% (+0.00212 total last wk)

- 1 Month +0.00200 to 0.09113% (+0.00050 total last wk)

- 3 Month +0.00288 to 0.15788% (+0.00550 total last wk) ** Record Low 0.11413% on 9/12/21

- 6 Month -0.00062 to 0.22538% (_0.01087 total last wk)

- 1 Year -0.00425 to 0.39425% (+0.04875 total last wk)

- Daily Effective Fed Funds Rate: 0.08% volume: $74B

- Daily Overnight Bank Funding Rate: 0.07% volume: $264B

- Secured Overnight Financing Rate (SOFR): 0.05%, $868B

- Broad General Collateral Rate (BGCR): 0.05%, $343B

- Tri-Party General Collateral Rate (TGCR): 0.05%, $324B

- (rate, volume levels reflect prior session)

- Tsy 0Y-2.25Y, $10.851B accepted vs. $39.274B submission

- Next scheduled purchases

- Tue 11/16 1010-1030ET: Tsy 4.5Y-7Y, appr $5.275B

- Tue 11/16 1100-1120ET: Tsy 10Y-22.5Y, appr $1.425B

- Thu 11/18 1010-1030ET: Tsy 22.5Y-30Y, appr $1.600B

- Fri 11/19 1010-1030ET: TIPS 1Y-7.5Y, appr 1.775B

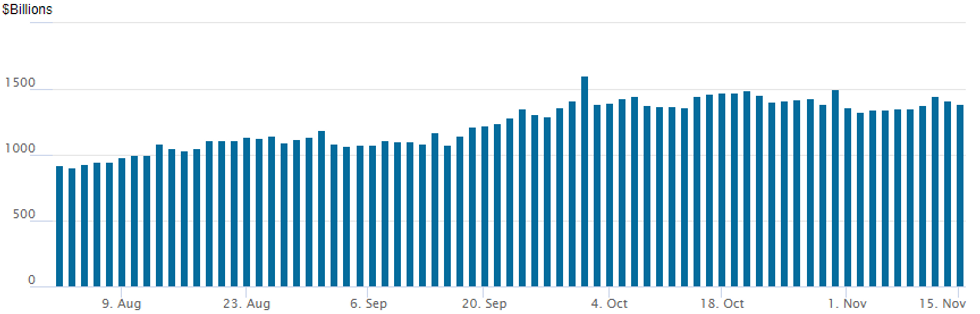

FED Reverse Repo Operation

NY Federal Reserve

NY Fed reverse repo usage recedes: $1,391.657B from 78 counterparties vs. $1,417.643B on Friday. Record high remains at $1,604.881B from Thursday, September 30.

PIPELINE: At Least $18.5B Launched Monday

At least $18.5B launched Monday, waiting on Westpac and DBS Grp

- Date $MM Issuer (Priced *, Launch #)

- 11/15 $6B #HSBC $500M 3NC2 FRN FOFR+58, $1.25B 3NC2 fix/FRN +65, $2.5B 6NC5 fix/FRN +100, $1.75B 11NC10 fix/FRN +125

- 11/15 $2B #NXP Semiconductors $1B +10Y +105, $500M +20Y +115, 30Y +130

- 11/15 $1.6B #Chubb $600M 30Y +83, $1B 40Y +105

- 11/15 $1.6B #Zimmer Biomet $850M 3NC1 +58, $750M 10Y +98

- 11/15 $1.5B #Blackstone Private Cr $500M 3Y +150, $1B +5Y +205

- 11/15 $1B #Virginia Electric & Power $500M 10Y +70, $500M 30Y +95

- 11/15 $1B #Banco Santander 11NC10 +160

- 11/15 $750M #Mastercard 10Y +43

- 11/16 $700M #Alabama Power 30Y +100, upsized from $600M

- 11/15 $500M #Ameren +5Y +70

- 11/15 $500M #State Street 6NC5 fix-FRN +43

- 11/15 $500M *Healthpeak Properties 7Y Green +72

- 11/15 $500M #Moody's WNG 40Y +115

- 11/15 $Benchmark Westpac 5Y +46a

- 11/15 $Benchmark DBS Group 3Y

- 11/15 $Benchmark British Telecom 60NC5.5, 60NC10 investor calls

- 11/15 $Benchmark Canadian Pacific investor calls

FOREX: Single Currency Spiked on Re-Routing of Rate Expectations

- Several central bankers further reinforced the yawning gap in EZ/UK rate expectations Monday, with the ECB President Lagarde stating that a rate hike in 2022 - as markets are currently pricing - would be very unlikely. This was in stark contrast to an appearance from the BoE governor Bailey, who stressed that a December rate hike was still in play, with incoming labour market data crucial for the next decision.

- EUR/GBP resultingly corrected lower, with the 50-day EMA support giving way ahead of the close. Recent price action has worked well against a previously bullish near-term outlook, opening initial firm support at 0.8463, Nov 3 low.

- Elsewhere, a re-steepening of the US yield curve worked in favour of the greenback, which rose against most others and got a decent leg up from the downside in EUR/USD. The USD Index now sits at its best levels since mid-2020, prompting focus to turn to the Fed speakers due throughout the week, with Clarida's appearance Friday possibly being most interesting.

- UK jobs data takes focus Tuesday, with US retail sales and import/export price indices also on the docket. Markets see little progress being made between Xi and Biden at their virtual summit, but markets will be on watch for any comments on trade or diplomatic relations.

- Central bank speakers include Fed's Bullard, ECB's Lagarde and BoC's Schembri.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.