- MN FED: Fed Considering Discount Window Readiness Rule - Barr

- MNI FED BRIEF: Restrictive Fed To Weigh On Demand - Jefferson

- MNI ICC Decision On Israel Could Jeopardize Ceasefire Deal - Blinken

- MNI Canada CPI Preview: Consensus For Core Could Still See June Rate Cut Odds Build

- MNI US DATAL=: Index of Consumer Sentiment

Source: Washington Post/ University of Michigan

US

FED (MNI): Fed Considering Discount Window Readiness Rule - Barr: Federal Reserve Governor Michael Barr said Monday the Fed is working actively to improve the functioning of the discount window after last year's regional bank crisis, including considering requiring certain banks maintain a minimum amount of reserves and collateral at the discount window.

- "We are exploring a requirement that banks over a certain size maintain a minimum amount of readily available liquidity with a pool of reserves and pre-positioned collateral at the discount window, based on a fraction of their uninsured deposits," he said. "Incorporating the discount window into a readiness requirement would also reemphasize that supervisors and examiners view use of the discount window as appropriate and unexceptional under both normal and stressed market conditions."

FED BRIEF (MNI): Restrictive Fed To Weigh On Demand - Jefferson: Federal Reserve Vice Chair Philip Jefferson said Monday current U.S. monetary policy is restrictive and will continue to weigh on demand, particularly on interest-sensitive spending.

- "I believe that our policy rate is in restrictive territory as we continue to see the labor market come into better balance, and inflation decline although nowhere near as quickly as I would have liked," said Jefferson in prepared remarks to the Mortgage Bankers Association. Inflation remains above the FOMC's 2% inflation objective and "it is too early to tell whether the recent slowdown in the disinflationary process will be long lasting."

Canada CPI Preview (MNI): Consensus For Core Could Still See June Rate Cut Odds Build: Consensus sees headline CPI two tenths to 2.7% Y/Y for a fourth month within the 1-3% target range. The BoC’s preferred core CPI measures are seen slowing 0.15pps to 2.8% Y/Y having surprised lower in the past three months.

NEWS

ISRAEL (MNI): ICC Decision On Israel Could Jeopardize Ceasefire Deal - Blinken: US President Joe Biden and US Secretary of State Antony Blinken have criticised today's announcement that ICC prosecutors are pursuing arrest warrants against leaders from Israel - Prime Minister Benjamin Netanyahu and Defence Minister Yoav Gallant - and leaders of Hamas - Ismail Haniyeh, Yahya Sinwar, and Mohammed Deif - for alleged crimes during in the war in Gaza and the Hamas attack on October 7, 2023.

FED VC Barr (MNI): Restrictive Policy Needs Further Time, Mulling Regulation Options: Vice Chair for Supervision Barr says in prepared remarks for a keynote address that restrictive policy needs further time to do its work and that the Fed is in a good position to hold rates steady whilst it watches. The economy is strong, growth is solid and unemployment is low.

US JPM - DIMON (BBG): `NOT GOING TO BUY BACK A LOT OF STOCK AT THESE PRICES'; *JPMORGAN EXTENDS DECLINE TO 1.5% AFTER DIMON BUYBACK COMMENTS

IRAN (MNI): President Raisi, FM Amir-Abdollahian Confirmed Dead In Helicopter Crash: First Vice President Mohammad Mokhber convened an emergency meeting of the cabinet after Iranian state media confirmed that President Ebrahim Raisi, Foreign Minister Hossein Amir-Abdollahian and other passengers have died in a helicopter crash in the province of East Azerbaijan. Tasnim News Agency reported that the bodies of the victims have been retrieved and were being taken to the provincial capital of Tabriz.

IRAN (MNI): Next President To Serve Full 4-Yr Term; Nuclear Negotiator Tipped For FM: Following the death of President Ebrahim Raisi in a helicopter crash, Iran's Guardian Council has confirmed that the special election to take place within 50 days will be for a full four-year term in office, not just serving out the remainder of Raisi's term to 2025.

ISRAEL (MNI): ICC Seeks Arrest Warrants Against Netanyahu, Gallant & Hamas Leaders: The International Criminal Court (ICC)'s chief prosecutor Karim Khan has told CNN that he is seeking arrest warrants to be issued against Israeli PM Benjamin Netanyahu, Defence Minister Yoav Gallant, and three Hamas leaders. The Israeli ministers face accusations of war crimes and crimes against humanity, while the three Hamas leaders face charges including extermination, murder, and taking of hostages.

US TSYS Mildly Weaker, Off Lows, Focus on Wednesday's May 1 FOMC Minutes

- Treasuries trading modestly weaker after the bell, generally quiet start to the week with no data until Wednesday, dip in rates coincided with rebound in USD. Treasuries broke a narrow overnight range, extended lows early Monday, traded sideways after recovering approximately half the move by midmorning.

- Decent corporate debt issuance climbed over $15B, rate lock hedging contributed to the early sale. Pick-up in Tsy quarterly futures roll from Jun'24 to Sep'24.

- Vice Chair for Supervision Barr says in prepared remarks for a keynote address that restrictive policy needs further time to do its work and that the Fed is in a good position to hold rates steady whilst it watches. The economy is strong, growth is solid and unemployment is low.

- Rate cut projections have receded vs. this morning's levels (*): June 2024 at -5% w/ cumulative rate cut -1.2bp at 5.318%, July'24 at -20% w/ cumulative at -6.3bp (-7.5bp) at 5.267%, Sep'24 cumulative -19.6bp (-20.9bp), Nov'24 cumulative -27.1bp (-29bp), Dec'24 -41.5bp (-43.9bp).

- Look ahead to Tuesday, similar to Monday: no economic data and a raft of Fed speakers. Focus on the minutes from the May 1 FOMC this Wednesday.

US: Consumer Sentiment Sours In May, Warning Sign For Biden

The University of Michigan index of consumer sentiment saw its biggest drop since 2021 in May - dropping to a six-month low - reflecting consumer concerns over inflation and rising prices.

- The Washington Post notes: "The economy, while still remarkably strong, has slowed in recent months as the Federal Reserve tries to get inflation under control. Employers are adding fewer jobs, wage growth has decelerated, and Americans are holding off on big purchases like homes, cars and washing machines."

- Jeffrey Roach, chief economist for LPL Financial said: “For the last couple of years, the economy has been driven by household spending and now people are starting to say, ‘Let’s retrench here. The pressure from inflation has finally started to hit even upper-income households.”

- The shifting sentiment is a warning sign for President Biden as the White House economic message - largely driving by positive data - has failed to resonate with voters facing persistently high prices.

- Celinda Lake, a Democratic pollster, noted the particular concern of gas prices which have risen by roughly 50 cents per gallon since the start of the year on average: “People tend to know the cost of gas, block by block, and they deeply resent it when gas prices go up right before summer vacation.”

MARKETS SNAPSHOT

- Key market levels of markets in late NY trade:

- DJIA down 192.58 points (-0.48%) at 39810.93

- S&P E-Mini Future up 5.75 points (0.11%) at 5332.75

- Nasdaq up 118.5 points (0.7%) at 16804.3

- US 10-Yr yield is up 2.6 bps at 4.4453%

- US Jun 10-Yr futures are down 5.5/32 at 109-0.5

- EURUSD down 0.0007 (-0.06%) at 1.0862

- USDJPY up 0.62 (0.4%) at 156.26

- WTI Crude Oil (front-month) down $0.45 (-0.56%) at $79.61

- Gold is up $15.36 (0.64%) at $2430.31

- European bourses closing levels:

- EuroStoxx 50 up 10.2 points (0.2%) at 5074.34

- FTSE 100 up 3.94 points (0.05%) at 8424.2

- German DAX up 64.54 points (0.35%) at 18768.96

- French CAC 40 up 28.47 points (0.35%) at 8195.97

US TREASURY FUTURES CLOSE

- 3M10Y +2.627, -96.261 (L: -103.647 / H: -95.151)

- 2Y10Y +0.643, -40.041 (L: -41.254 / H: -39.026)

- 2Y30Y +0.487, -26.315 (L: -27.329 / H: -24.929)

- 5Y30Y +0.276, 11.468 (L: 11.056 / H: 12.497)

- Current futures levels:

- Jun 2-Yr futures down 1.25/32 at 101-21.125 (L: 101-21 / H: 101-23.125)

- Jun 5-Yr futures down 3.25/32 at 105-24.75 (L: 105-23.5 / H: 105-30)

- Jun 10-Yr futures down 5.5/32 at 109-0.5 (L: 108-30.5 / H: 109-09)

- Jun 30-Yr futures down 11/32 at 116-31 (L: 116-25 / H: 117-16)

- Jun Ultra futures down 14/32 at 123-23 (L: 123-13 / H: 124-12)

US 10Y FUTURE TECHS: (M4) Bullish Despite The Latest Retracement

- RES 4: 110-16 50.0% retracement of the Feb 1 - Apr 25 bear leg

- RES 3: 110-06 High Apr 4

- RES 2: 110-00 Round number resistance

- RES 1: 109-31+ High May 16

- PRICE: 109-00+ @ 1540 BST May 20

- SUP 1: 108-27+/108-15 50-day EMA / Low May 14 and key support

- SUP 2: 108-06 Low May 3

- SUP 3: 107-25 Low May 2

- SUP 4: 107-04 Low Apr 25 and the bear trigger

Despite the latest pullback in Treasuries, the short-term trend condition remains bullish. The contract last week moved through resistance at the top of a bear channel, drawn from the Feb 1 high. Note that resistance at 109-09+, the May 3 high, has also been cleared. This reinforces the bullish importance of the channel break and signals scope for an extension higher. Sights are on 110-00 next. Initial key support is at 108-15, May 14 low.

SOFR FUTURES CLOSE

- Jun 24 -0.008 at 94.685

- Sep 24 -0.015 at 94.860

- Dec 24 -0.025 at 95.080

- Mar 25 -0.025 at 95.325

- Red Pack (Jun 25-Mar 26) -0.03 to -0.02

- Green Pack (Jun 26-Mar 27) -0.015 to -0.015

- Blue Pack (Jun 27-Mar 28) -0.02 to -0.015

- Gold Pack (Jun 28-Mar 29) -0.03 to -0.025

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

SOFR Benchmark Settlements:

- 1M +0.00083 to 5.32059 (-0.00011 total last wk)

- 3M +0.00092 to 5.32672 (+0.00382 total last wk)

- 6M +0.00458 to 5.28779 (-0.00110 total last wk)

- 12M +0.01689 to 5.13941 (-0.01641 total last wk)

- Secured Overnight Financing Rate (SOFR): 5.31% (+0.00), volume: $1.964T

- Broad General Collateral Rate (BGCR): 5.30% (+0.00), volume: $722B

- Tri-Party General Collateral Rate (TGCR): 5.30% (+0.00), volume: $711B

- (rate, volume levels reflect prior session)

- Daily Effective Fed Funds Rate: 5.33% (+0.00), volume: $77B

- Daily Overnight Bank Funding Rate: 5.32% (+0.00), volume: $269B

FED Reverse Repo Operation

NY Federal Reserve/MNI

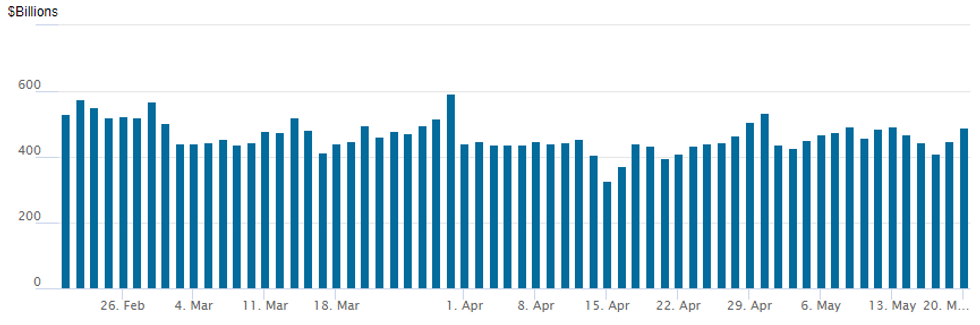

- RRP usage climbs to $489.728B from $449.373B prior; number of counterparties 75. Compares to $327.066B on Monday, April 15 -- the lowest level since mid-May 2021.

PIPELINE: $3.25B Comcast 3Pt Launched

Total of $14.5B corporate debt has issued Monday, Comcast 3pt leads:

- Date $MM Issuer (Priced *, Launch #)

- 5/20 $3.25B #Comcast $750M 5Y +65, $1.3B 10Y +90, $1.2B 30Y +110

- 5/20 $2.6B #Elevance Health $600M 5Y +70, $1B 10Y +95, $1B 30Y +110

- 5/20 $2.6B #UPS $900M 10Y +72, $1.1B 30Y +92, $600M 40Y +105

- 5/20 $1.25B #PayPal $850M 10Y +80, 00M $30Y +100

- 5/20 $1.2B #Entergy 30.5NC5.5, 7.125%

- 5/20 $1B #Handelsbanken $600M 3Y +55, $400M 3Y SOFR+66

- 5/20 $850M #AEP Texas $500M 5Y +100, $350M 10Y +130

- 5/20 $600M #Northwestern Mutual 7Y +73

- 5/20 $600M #Nstar Electric 10Y +98

- 5/20 $550M #F&G Annuities 5Y +210

- 5/20 $500M California Resources 5NC2

- 5/20 $500M Zebra Tech 8NC3

EGBs-GILTS CASH CLOSE: Gilts Underperform With UK CPI Eyed Ahead

European curves lightly bear steepened Monday as the weakness seen late last week extended, with Gilts underperforming.

- Amid light trading volumes on the Whit Monday holiday observed in various European countries, there were few notable catalysts.

- BoE's Broadbent noted it's "possible" rates will be cut in the summer, though gave little away on his view of a June reduction.

- Around 2bp of 2024 BoE cuts were pared from the path on the day with 54bp in reductions now seen; the ECB counterpart was little changed at 67bp.

- A moderate pullback in oil prices helped core FI tick up from session lows in early afternoon trade, though downside resumed from there into the cash close.

- While Bunds and Gilts have now more than reversed last week's rally, today's ranges were relatively tight. Periphery spreads tightened slightly, against a fairly benign risk backdrop with equities higher.

- Tuesday brings an appearance by ECB's Lagarde and German PPI, with UK inflation and flash PMIs featuring later in the week.

Closing Yields / 10-Yr Periphery EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.7bps at 2.993%, 5-Yr is up 1.2bps at 2.573%, 10-Yr is up 1.4bps at 2.529%, and 30-Yr is up 1.3bps at 2.666%.

- UK: The 2-Yr yield is up 3.6bps at 4.346%, 5-Yr is up 3.8bps at 4.047%, 10-Yr is up 4.2bps at 4.169%, and 30-Yr is up 4.9bps at 4.649%.

- Italian BTP spread down 1.5bps at 128.4bps / Spanish down 0.2bps at 75.5bps

FOREX Greenback Consolidates Moderate Gains, Antipodeans Underperform

- While most European markets are open, the observance of the Whit Monday holiday initially tempered activity to start the week, with most G10 currencies exhibiting narrow ranges as we approached the NY crossover. A brief bout of weakness for Treasuries saw the USD index pop to fresh session highs, however, gains have been partially reversed throughout the remainder of the session.

- The index approaches the APAC crossover 0.10% higher on the day, although just 45 pips off the recent lows. Market participants will monitor the April lows just below the 104 handle as the next notable support as markets await further US data to assess short-term Fed pricing.

- The higher US yields prompted a notable move higher for USDJPY, breaking back above 156.00 and printing a high of 156.23. 156.74 remains the notable resistance to watch.

- Ahead of Tuesday’s RBA minutes, AUDUSD has also pulled back slightly. However, a bullish remains intact following last week’s gains where the move higher resulted in the break of a number of short-term resistance points, including a key short-term resistance at 0.6668, the Mar 8 high.

- NZDUSD (-0.33%) is a relative underperformer following a Q2 RBNZ survey of inflation expectations showed households saw a slightly lower median expected inflation rate for the next two years at 3% from 3.2% in 1Q. This comes ahead of the RBNZ meeting on Wednesday, where markets expect an unchanged decision.

- Tuesday’s data calendar will be highlighted by Canada inflation data. Elsewhere, ECB’s Lagarde and another plethora of Fed members will speak.

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Flag | Country | Event |

| 21/05/2024 | 0130/1130 |  | AU | RBA Minutes | |

| 21/05/2024 | 0600/0800 | ** |  | DE | PPI |

| 21/05/2024 | 0800/1000 | ** |  | EU | Current Account |

| 21/05/2024 | 0900/1100 | ** | | EU | Construction Production |

| 21/05/2024 | 0900/1100 | * | | EU | Trade Balance |

| 21/05/2024 | 0900/1000 | ** |  | UK | Gilt Outright Auction Result |

| 21/05/2024 | 1000/1100 | ** | | UK | CBI Industrial Trends |

| 21/05/2024 | 1230/0830 | *** |  | CA | CPI |

| 21/05/2024 | 1230/0830 | ** |  | US | Philadelphia Fed Nonmanufacturing Index |

| 21/05/2024 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 21/05/2024 | 1300/0900 | | US | Fed Governor Christopher Waller | |

| 21/05/2024 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 21/05/2024 | 1545/1145 | | US | Fed Vice Chair Michael Barr | |

| 21/05/2024 | 1700/1800 | | UK | BOE's Bailey Lecture at LSE | |

| 21/05/2024 | 2300/1900 | | US | Atlanta Fed's Raphael Bostic | |

| 21/05/2024 | 2300/1900 | | US | Cleveland Fed President Loretta Mester |