Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

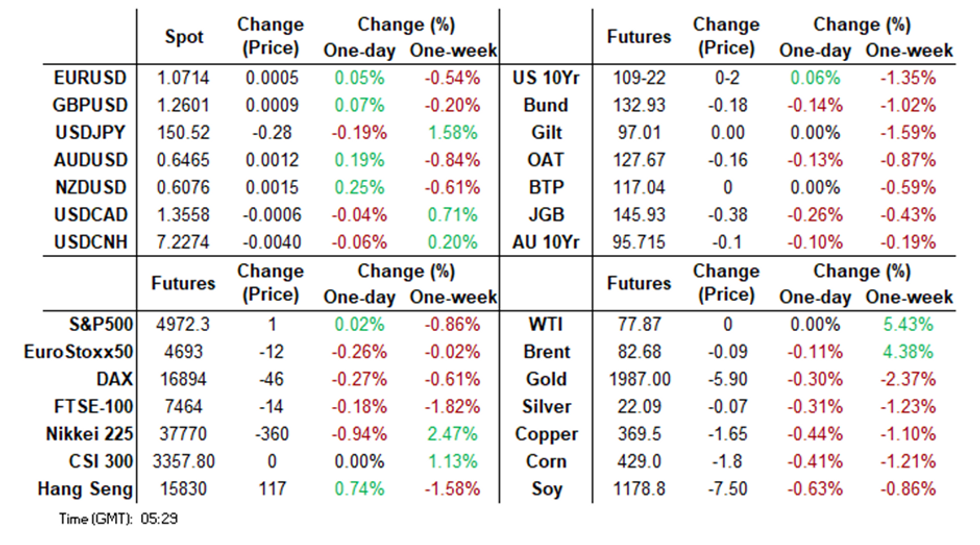

- Treasuries maintained a tight range in Asia, with TYH4 briefly dipping to new lows at 109-16+ during the morning session, rebounding quickly to settle around 109-21.

- USDJPY has continued to trend lower towards 150 after senior currency officials warned that they are prepared to intervene. It is currently down 0.2% to 150.44, close to the intraday low.

- Regional Equities are lower as robust US CPI quashes rate cut expectations, pushing yields higher. While Hong Kong equities reversed early losses to trade higher.

- Later the Fed’s Goolsbee and Barr speak as well as BOE’s Bailey, ECB’s de Guindos and Cipollone. There is no data in the US but UK January CPI/PPI and euro area Q4 preliminary GDP/employment and December IP print.

MARKETS

US TSYS: Tsys Futures Off Lows, As Market Digests US CPI

TYH4 is currently trading at 109-21+, down 01+ from New York closing levels. Treasuries maintained a tight range in Asia, with TYH4 briefly dipping to new lows at 109-16+ during the morning session, rebounding quickly to settle around 109-21.

- Mar'24, 10Y futures opened slightly lower, reaching new lows at 109-16+, a level unseen since late Nov'23 and marking initial technical support (50.0% of the Oct 19 - Dec 27 bull phase). The quick reversal brought them back to 109-21, where they held for the rest of the session. Mar'24 2Y futures performed better, trading off overnight lows of 101-28.75 and gradually climbing to 101-31.125.

- Cash yield curves steepened in Asia, with the 2Y yield, 3bps lower at 4.468%, while the 10Y yield is 0.6bp lower at 4.308%.

- A quiet session for headlines, notable ones include Yellen participating in American events later today, and Democrat Suozzi winning the New York House Race.

- December 2024 expectations and cumulative easing stand at 4.41%, -92bps (FOMC) vs 4.45%, -58bps (BOC); 3.98%, -34bps (RBA); and 5.22%, -45bps (RBNZ).

- Looking ahead, Wednesday's data focuses on PPI revisions and US MBA Mortgage Applications, with Fed speakers Chicago Fed Goolsbee and Fed VC Barr scheduled.

JGBS: Futures Sitting Cheaper & Near Lows, Q4 GDP Data Tomorrow

JGB futures are holding sharply cheaper, -44 compared to settlement levels, but above the session low of 145.75 (-56). With the domestic calendar empty, apart from 10-year climate transition bond supply, local participants appear to have been content to use US tsys for directional guidance.

- (Bloomberg) -- Japan’s climate transition sovereign bond had a yield of 0.74%, according to MOF, lower than the 0.75% yield for regular government notes maturing on the same day, indicating strong demand from investors.

- Cash US tsys are currently dealing flat to 3bp richer, with the benchmark curve steeper, ahead of Wednesday's release of PPI revisions. Fed speakers Chicago Fed Goolsbee and Fed VC Barr are also scheduled.

- (Straits Times) -- Japan's latest growth figures are set to confirm that it slipped to the fourth-largest economy in the world in 2023, a development that reflects the impact of its feeble currency and ageing demographics. (See links)

- The cash JGB curve has bear-steepened, with yields 1-5bps higher. The benchmark 10-year yield is 3.1bps higher at 0.758% versus the morning high of 0.765%.

- The swaps curve is mostly cheaper, with rates 1-4bps higher. Swap spreads are tighter out to the 30-year.

- Tomorrow, the local calendar sees Q4 GDP (Prelim), December Industrial Production (Final) and December Capacity Utilisation data.

- Tomorrow will also see BoJ Rinban operations covering 1-5-year and 10-25-year+ JGBs.

AUSSIE BONDS: Holding Cheaper, RBA Bullock’s Senate Testimony & Jobs Report Tomorrow

ACGBs (YM -11.0 & XM -10.0) are cheaper and not too far from Sydney session lows. With the local calendar empty apart from ACGB weekly supply, local participants have been content to track US tsys in today’s Asia-Pac session following yesterday’s aggressive post-CPI sell-off. Cash US tsys are currently dealing flat to 3bp richer, with the benchmark curve steeper.

- The latest round of ACGB Dec-30 supply prices comfortably through mids but with a relatively modest cover ratio of 2.7125x.

- Cash ACGBs are 9-11bps cheaper, with the AU-US 10-year yield differential 4bps lower at -4bps.

- Swap rates are 9-11bps higher, with the 3s10s curve flatter.

- The bills strip has sharply bear-steepened, with pricing -1 to -11.

- RBA-dated OIS pricing is 6-9bps firmer for meetings beyond June. A cumulative 28bps of easing is priced by year-end.

- Tomorrow's local calendar is busy, starting with RBA Bullock's Senate Testimony, followed by the release of January's Employment Report and February's Consumer Inflation Expectation data.

- Given December’s large 65.1k drop, attention will be on whether labour demand is still strong enough to unwind most of that move. Bloomberg consensus is forecasting a 25k rise in new jobs with the unemployment rate ticking up 0.1pp to 4%. The latter hasn’t started with a ‘4’ since February 2022.

AUSSIE BOND AUCTION: ACGB Dec-30 Auction Result

The AOFM sells A$800mn of the 1.00% 21 December 2030 bond, #TB160:

- Average Yield (%): 4.0856 (prev. 1.1233)

- High Yield (%): 4.0875 (prev. 1.1250)

- Bid/Cover: 2.7125x (prev. 5.4125x)

- Amount Allotted at Highest Accepted Yield as Percentage of Amount Bid at that Yield (%): 61.7

- Bidders 45 (prev. 47), successful 15 (prev. 17), allocated in full 8 (prev. 8)

NZGBS: Cheaper But Off Cheaps, Net Migration Data Tomorrow

NZGBs closed 5-7bps cheaper, with the 2/10 curve steeper. NZGBs finished stronger than their worst levels in sympathy with a slight paring of yesterday’s sell-off in short-end US tsys in today’s Asia-Pac session. Cash US tsys are flat to 3bps richer across benchmarks, with a steepening bias.

- There hasn’t been much in the way of domestic drivers to flag, outside of the previously outlined Retail Card Spending, REINZ House Sales and Food Prices data. The domestic data drop, as expected, failed to be a market-mover.

- Swap rates closed 4-6bps higher, with the 2s10s curve steeper.

- RBNZ dated OIS pricing is 2-9bps firmer, with November leading. A cumulative easing of 44bps is priced for year-end from a peak of 5.66%. This compares to 100bps of easing off 5.53% at the end of January.

- (Bloomberg) -- NZ’s residential construction market was weaker than expected in the six months through December and is likely to remain that way, Fletcher Building said in a presentation. (See link)

- Tomorrow, the local calendar sees the NZ Government’s 6-Month Financial Statements and Net Migration data.

- Tomorrow, the NZ Treasury plans to sell NZ$275mn of the 4.5% Apr-27 bond, NZ$150mn of the 3.5% Apr-33 bond and NZ$75mn of the 2.75% May-51 bond.

NEW ZEALAND: Retail Spending Appears To Have Troughed

NZ card transactions continued to recover in January with the total rising 2% m/m to be up 3.2% y/y but the retail component softer up 1.7% m/m to be only +0.9% y/y. January unwound the December drop in retail sales though and 3-month momentum turned positive but the level is less than a percent higher than the H2 2023 average. Card spending is soft but looks to have troughed and may be tentatively recovering after a period of unchanged rates in line with improving consumer confidence.

- Core retail sales were stronger rising 1.9% m/m with durables up 1.8% and apparel +3.1%.

- Non-retail card transactions ex services rose 2.7% m/m but services fell 0.4%. Hospitality spending rose 1.9% y/y.

STIR: $-Bloc Easing Expectations Pared But Remain Substantial

STIR markets in the $-bloc continue to anticipate an easing cycle in 2024, albeit with significantly reduced expectations relative to late January.

- The trimming of year-end easing projections gained momentum overnight in the US and Canada, and today in Australia and NZ, triggered by the release of unexpectedly high US CPI data for January.

- Relative to early February, official rate expectations for December 2024 sit 26bps (Australia) to 66bps (NZ) higher across the $-bloc.

- December 2024 expectations and the cumulative easing across the $-bloc stand at: 4.41%, -92bps (FOMC); 4.45%, -58bps (BOC); 3.98%, -34bps (RBA); and 5.22%, -45bps (RBNZ).

Source: MNI – Market News / Bloomberg

EQUITIES: Hong Kong Rebounds After Early Decline, Regional Equities Lower

Regional Equities are lower as robust US CPI quashes rate cut expectations, pushing yields higher. While Hong Kong equities reversed early losses to trade higher.

- Hong Kong equities are mostly higher today, after opening lower. Investors are assessing whether Chinese authorities' policies and willingness to halt the overall stock rout will be effective. However, recent sell-offs in Chinese equities have been met with swift buying. Post-lunch, equities recover significantly, with the HSI now 0.50% higher, HS Tech up 1.40%, while Mainland property index was at one point down 3% to now just just 0.50% lower for the day

- Japan equities are lower today erasing most of yesterday’s gains. The Nikkei 225 is still nearing all-time highs at levels not seen since 1989. The put-to-call ratio on the Nikkei 225 has dropped even as the benchmark climbed 13% this year, suggesting that bullishness is growing despite technical signals the rally is getting overheated while the most active index option traded in Japan on Tuesday was a call that benefits if the Nikkei climbs above 40,000 in March. The NIkkei is 0.82% lower today while the Topix is currently off 1.25%.

- South Korea equities decline due to stronger-than-expected US CPI causing a tech sell-off. Samsung leads the decline, down 1.60%, while the Kospi trades 1.00% lower.

- Australia equities are also lower today as the ASX 200 trades down .90%, led by financial as CBA fell 3.40% the largest contributor the the move lower. Elsewhere Graincorp fell by 12% after poor earnings guidance

- Elsewhere in SEA, NZ closed 0.67% lower, Singapore is down 0.42%, while Indonesia is closed today due to presidential elections

OIL: Crude Off Intraday Lows Driven By US Inventory Data

Oil prices are down slightly during APAC trading today following the lower-than-expected US crude inventory report earlier. They rose around a percent yesterday. WTI is off its low of $77.52/bbl and is currently around $77.84, while Brent is down 0.1% to $82.65 up from $82.33. The US dollar is down slightly after rallying Tuesday.

- Bloomberg reported that there was a higher-than-expected crude inventory build of 8.52mn barrels but gasoline stocks fell 7.23mn and distillate -4mn, according to people familiar with the API data. Inventories have been volatile since a cold snap impacted flows and refining in January. The official EIA data is out later today.

- OPEC is positive regarding the demand outlook but its report showed that there was only partial compliance with the new quotas. The IEA sees continued supply growth being able to more than cover demand. Its monthly report is published on Thursday.

- Diesel and gasoline prices are at their highest since October posting strong increases so far this year, according to Bloomberg.

- Later the Fed’s Goolsbee and Barr speak as well as BOE’s Bailey, ECB’s de Guindos and Cipollone. There is no data in the US but UK January CPI/PPI and euro area Q4 preliminary GDP/employment and December IP print.

GOLD: Sharply Lower As US CPI Data Reduced Easing Hopes

Gold is steady in the Asia-Pac session, after closing 1.3% lower at $1993.15 on Tuesday following hotter than expected US CPI data.

- Both headline and core CPI inflation figures for January surpassed expectations by 0.1 percentage points, with rounding pushing the annual figures up by 0.2 percentage points. The core measure increased by 0.4% m/m, maintaining the annual increase of 3.9% y/y, unchanged from the prior month.

- US Treasury yields finished 9-21bps higher, with the 2/10 curve flatter. The January CPI report strongly supported the FOMC's patient stance and dealt a significant blow to dovish expectations for near-term policy easing.

- Projected Fed rate cut pricing continued to ebb: March’s chance of a 25bp rate cut is currently at 11% vs. 18% on Monday. The May meeting finished with a cumulative easing of 10bps at 5.23% and June with a cumulative 24bps at 5.09%.

- Bloomberg reported that Suki Cooper, a precious metals analyst at Standard Chartered Plc, believed bullion also faced further downside risk given the slowdown in seasonal demand in Asia due to the Lunar New Year holidays.

- According to MNI’s technicals team, the yellow metal breached key short-term support at $2001.9 (Jan 17 low) with next firm support seen at $1973.2 (Dec 13 low).

FOREX: G10 Limits Post-CPI Losses, Gradual Yen Strengthening

USDJPY has continued to trend lower towards 150 after senior currency officials warned that they are prepared to intervene. It is currently down 0.2% to 150.44, close to the intraday low. The USD is down slightly during APAC trading with the G10 stronger against the greenback.

- USDJPY weakened to 150.89 following the higher-than-expected US CPI data which drove the BBDXY USD index 0.6% higher. This has prompted officials to talk up the yen today warning that “authorities are ready to respond 24 hours a day, 365 days a year”. Tomorrow Q4 GDP prints.

- AUDUSD is 0.1% higher at 0.6462, close to the intraday high of 0.6464. It fell to 0.6446 early in the session. AUDJPY is down 0.1% to 97.22 and AUDNZD is -0.1% at 1.0641. On Thursday RBA Governor Bullock appears before the Senate economics committee and employment data is released.

- NZDUSD has trended higher today after falling sharply on Wednesday. The pair is up 0.2% to 0.6073 but is still well below yesterday’s highs.

- Asian currencies are generally weaker with USDKRW down 0.6%, USDPHP -0.5% and USDTHB -1.0%. Onshore IDR is not trading due to the holiday for the election.

- European currencies continue to be little changed against the USD today.

- Later the Fed’s Goolsbee and Barr speak as well as BOE’s Bailey, ECB’s de Guindos and Cipollone. There is no data in the US but UK January CPI/PPI and euro area Q4 preliminary GDP/employment and December IP print.

INDONESIA: Prabowo Headed For Presidency Despite Controversy

Indonesians vote today for a new president, vice president, senate, House of Representatives and local legislative councils in one of the largest exercises in democracy globally given its 200mn plus voters. Polls have had defence minister Prabowo in the lead since candidates were confirmed late last year but the latest SPIN poll is showing the highest support for him of any poll on 54.8%, which if that materialises will mean he’ll avoid a runoff vote in June.

- It is worth noting that SPIN was one of the first surveys to show Prabowo with over 50% of the vote but support for him increased almost 4pp from the last SPIN poll in early January. Also all the various surveys taken from mid-January are signalling that he will receive over 50% of the vote. SPIN has Anies in second place on 24.3% and the incumbent PDI-P’s Ganjar on 16.1%.

- Prabowo will also need to win a minimum of 20% of votes in at least half the provinces to avoid a runoff. Vote counting will begin today and continue tomorrow while the official election result will have to be announced by March 20. Survey companies will be at polling stations and publicise the “quick count” which has been an accurate indicator in the past.

- Current popular president Joko Widodo has implicitly given his backing to Prabowo through his son Gibran running as his VP candidate, which has boosted support for the controversial minister. He has said he will continue the current president’s policies. Jokowi is not allowed to run for another term but his influence may continue through his son.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 14/02/2024 | 0700/0700 | *** |  | UK | Consumer inflation report |

| 14/02/2024 | 0700/0700 | *** | | UK | Producer Prices |

| 14/02/2024 | 0700/0800 | ** |  | NO | Norway GDP |

| 14/02/2024 | 0830/0930 |  | EU | ECB's De Guindos speech at Mediterranean CB's conference | |

| 14/02/2024 | 1000/1100 | ** | | EU | Industrial Production |

| 14/02/2024 | 1000/1100 | *** | | EU | GDP (p) |

| 14/02/2024 | 1000/1000 | ** | | UK | Gilt Outright Auction Result |

| 14/02/2024 | 1200/0700 | ** |  | US | MBA Weekly Applications Index |

| 14/02/2024 | 1400/0900 | * |  | CA | CREA Existing Home Sales |

| 14/02/2024 | 1400/1500 | | EU | ECB's Cipollone statement on digital euro | |

| 14/02/2024 | 1430/0930 | | US | Chicago Fed's Austan Goolsbee | |

| 14/02/2024 | 1500/1500 | | UK | BOE's Bailey Lord Economic Affairs Committee | |

| 14/02/2024 | 1530/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 14/02/2024 | 1630/1730 | | EU | ECB's Cipollone in CEO Summit | |

| 14/02/2024 | 1930/1430 | | CA | BOC Deputy Mendes panel talk. | |

| 15/02/2024 | 2350/0850 | *** |  | JP | Japan GDP 1st Estimate |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.