Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

- Our 6-month ahead Euro Area recession probability estimate (from 1985) rose above 50% for the first time in July 2022, signalling the risk of recession in January 2023. It peaked in September at 59% and has been below 50% since, thus signalling more of a shallow downturn rather than a recession.

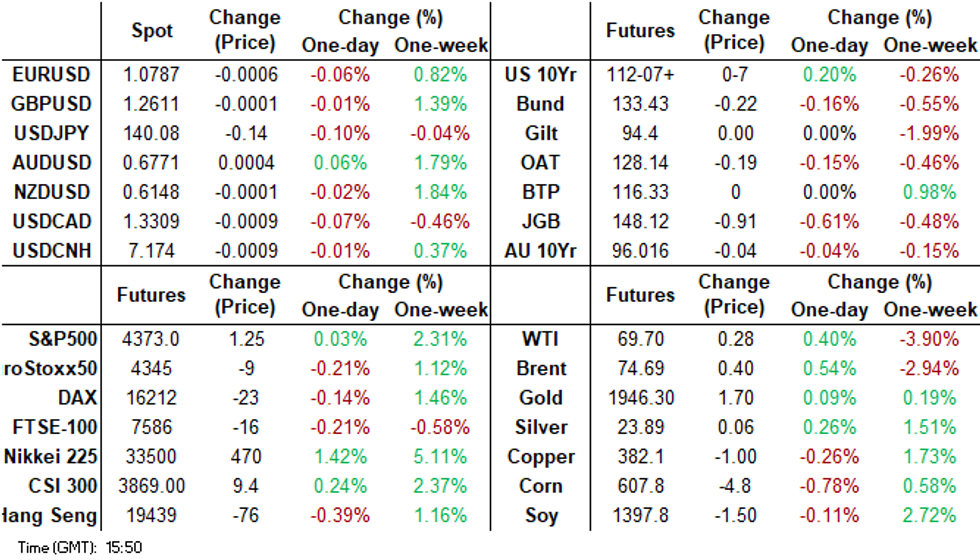

- Near term focus will rest with the upcoming Fed decision. Cash tsys sit 1-2bps richer across the major benchmarks, light bull steepening is apparent. FOMC dated OIS remained stable. The USD index has been steady, although USD/Asia pairs are mostly higher (except USD/CNH).

- China Foreign Minister Qin and US Secretary of State Blinken spoke earlier today via phone. During the discussion Qin said that the US should stop interfering in China’s internal affairs, which is not unusual. But he also said that the US should respect issues which are important to China, such as Taiwan, and should stop hurting China by using competition as an excuse. Blinken is scheduled to travel to travel this Sunday to China.

MARKETS

EUROZONE: Model Signalling Shallow Downturn Rather Than Recession

Euro area Q1 GDP was revised down to -0.1% q/q after -0.1% in Q4. According to the simple rule of thumb that a recession is two consecutive quarters of negative growth, then the euro area went into recession in Q4 2022. However, like the US, they have a business cycle dating committee (see EABCN) but it will be some time before they make the call. Given that unemployment has continued to fall into Q2, it is unlikely that the euro area is in recession.

- Our 6-month ahead recession probability estimate (from 1985) rose above 50% for the first time in July 2022, signalling the risk of recession in January 2023. It peaked in September at 59% and has been below 50% since, thus signalling more of a shallow downturn rather than a recession, consistent with the 0.1% q/q declines seen thus far. GDP can see significant revisions.

- The recession estimates updated for May data were fairly stable and remained below 50% with the 1985 calculation at 16% 6-months ahead and the 1998 at 31%. Real equities, oil prices, REER, unemployment and real 10 year yield all helped to keep the risk down. The latest estimates point to positive growth in H2 2023 even if it is weak.

- It is worth noting that econometric estimates are not predictions or in this case projections.

Source: MNI - Market News/Refinitiv

US TSYS: Marginally Richer In Asia, FOMC In View

TYU3 deals at 112-29, +0-07+, a 0-07 range has been observed on volume of ~76k.

- Cash tsys sit 1-2bps richer across the major benchmarks, light bull steepening is apparent.

- Tsys firmed in early dealing, there was no obvious headline driver. Asia-Pac participants perhaps used Tuesday's cheapening as an opportunity to exit short positions/enter fresh longs.

- The moderate richening held through the remainder of the session. Narrow ranges were observed and little meaningful macro headline flow crossed. The proximity to today's FOMC meeting perhaps limiting activity.

- FOMC dated OIS remained stable, pricing no change for today's meeting with a terminal rate of 5.25% in July. There are ~10bps of cuts in 2023.

- May PPI crosses before the FOMC rate decision is due. The MNI preview of the event is here.

JGBS: Futures Down, But Holding Above Session Lows

Futures sit at 148.08, -.18. There was a slight offered tone this afternoon, as US futures edged down from session highs, but there was little follow through. Earlier session lows just under 148.00 remain intact for now.

- In the cash bond space, yields are touch firmer versus earlier lows, the 10yr creeping back up towards 0.44%, although the 20-40yr space still remains slightly lower in yield terms for the session.

- In the swap space, similar trends are evident. The 10yr is back to 0.596%, range on the day being 0.58125/0.60250%.

- The local data calendar is empty today. We get data tomorrow (May trade balance, core machine orders and weekly investment flows) ahead of Friday's BoJ decision. Tomorrow also has a 3month bill sale and BOJ bond purchase operations.

- The main domestic news today being local media reporting that PM Kishida may dissolve the lower house if the opposition submits a no-confidence motion this Friday.

AUSTRALIAN DATA: Arrivals Are Still Well Below Pre-Pandemic Levels

Total April arrivals rose 25.89k on the month but remain well below pre-pandemic levels. Permanent arrivals fell 2.77k m/m but are still up 47.6% y/y. The 12 month rolling sum of permanent is still 41.9% below December 2019. Given the discussion of strong population growth recently and the pressure it is putting on an already stretched housing market, in the year to April there were 126k permanent arrivals. If levels return to pre-pandemic numbers, then housing is going to become an even bigger problem given lacklustre new building rates and could also add to inflation through rising demand. May population figures will be released with Thursday’s labour market data.

Australia permanent arrivals 12m sum

Source: MNI - Market News/ABS

AUSSIE BONDS: Curve Bear Flattens On Wednesday, May Labour Report Due Tomorrow

ACGB's sit 3-9bps cheaper across the major benchmarks, the curve has bear flattened. The spillover from Tuesday's core global FI cheapening weighed at the open and held through the session.

- Futures are a touch lower, XM (-0.035) and YM (-0.066), however ranges have been narrow thus far today.

- RBA dated OIS remains stable, pricing a terminal rate of 4.49% in December.

- Rabobank Rural Confidence Index improved slightly in Q1 to -22 from -25 as Rabobank noted that farmers are adjusting to a normalisation in economic conditions.

- Looking ahead, on the wires tomorrow we have the May Labour Market Report. The Unemployment Rate is expected to hold steady at 3.7%. June Consumer Inflation Expectations is due.

NZGBs: Cheaper On Wednesday, GDP On Tap Tomorrow

NZGB's finished dealing ~5bps cheaper across the major benchmarks. The spillover from Tuesday's core global FI cheapening weighed at the open and held through the session.

- Swap rates ticked a touch higher, with the 2s10s spread marginally flattening. RBNZ pricing remains stable with a terminal rate of 5.64% seen in October.

- The IMF noted that the RBNZ shouldnt cut rates for a prolonged period, warning that a reignition of demand would need more tightening. More here.

- The Q1 Current Account Balance was a touch narrower than expected printing a $5.215bn deficit vs $6.85bn exp.

- On the wires tomorrow we have Q1 GDP. A fall of -0.1% Q/Q is expected.

NZ DATA: Consensus Expects Moderate Q1 GDP Decline

Q1 GDP prints on Thursday and is expected to decline for the second consecutive quarter. Bloomberg consensus is forecasting a moderate 0.1% q/q drop in the production measure after -0.6% in Q4, which would result in an annual increase of 2.6% after 2.2% (Q1 2022 fell 0.5% q/q). While this would constitute a technical recession, the series has been volatile recently. Also watch the expenditure measure for the state of domestic demand.

- Consensus is below the RBNZ, which is forecasting a 0.3% q/q rise in Q1. There is a chance that Q1 could see some payback for the very weak Q4, as activity may have been pushed into Q1 given capacity constraints. Q1 is also likely to benefit from surging immigration. The national accounts are not published on a regional basis and so it will be difficult to ascertain the impact of extreme weather events at the start of the year.

- Forecasts range from +0.4% q/q to -0.4% q/q with the annual rate varying from 2.2% y/y to 2.9% y/y. Westpac expects -0.4% q/q, BNZ -0.2%, Kiwibank 0%, ASB +0.1% and ANZ +0.2%.

NZ DATA: Current Account Deficit Narrows, Still Elevated

The current account deficit narrowed in Q1 to $5.215bn from $10.065bn in Q4. This brought the YTD deficit as a percent of GDP down to 8.5% from 9%, which is significantly higher than 6.8% in Q1 2022 and remains very high by OECD standards. It is now moving in the right direction though and should reassure ratings agencies.

- The current account deficit improvement over the quarter was due to narrower goods and services deficits.

- The widening of the current account deficit over the last year has been due to goods trade and primary income deficits. Good imports rose 18.4% y/y, driven by petrol (including higher prices), machinery & equipment. Good exports rose 10.7% y/y, driven by dairy.

- There was also a widening of the Q1 services deficit of $0.48bn with imports rising 40.3% y/y and exports 56.6%.

- The Q1 capital account saw an inflow of $2.3bn. Statistics NZ noted that it was “mainly made up of claims by New Zealand insurers on overseas reinsurers, following the larger than usual claims that have arisen from the Auckland flooding and Cyclone Gabrielle”.

Source: MNI - Market News/Refinitiv

EQUITIES: Fresh Highs For Japan Stocks, Korean Shares Slide

Japan stocks again remain outperformers, following positive leads from US/EU markets during Tuesday trade. Trends are mixed elsewhere, the Kospi down, while HK share shares are around flat at the break. US futures have been fluctuating close to flat for much of the session.

- The Nikkei 225 is up a further ~1.50%, hitting fresh highs for this uptrend. Toyota was a strong performer, rising 5%, while construction equipment makers rallied on China stimulus hopes.

- The HSI is around flat, but mainland China shares are firmer, +0.52% at the break for the CSI 300. Education related stocks are higher after the authorities announced plans to improve the vocational school and public education systems. The consensus is also now for a cut in the 1yr MLF rate, announced tomorrow.

- South Korea shares bucked the more positive tech trends, with the Kospi off by 0.60% at this stage, the Kosdaq down 1.8%. The electronics sector is a source of weakness. These moves unwind some of South Korea's recent equity market outperformance. The Taiex is close to flat.

- In SEA trends are mixed, Malaysia shares are higher, with a crude palm oil bounce helping. Indonesian stocks are down though, last off 0.50%.

FOREX: USD Index Steady, NZD Outperforming Modestly

There haven't been any dramatic FX moves since the Asia Pac open. The BBDXY sits slightly above it Tuesday NY closing level, last near 1232.00. We are comfortably above post US CPI lows (near 1229). NZD and AUD are tracking higher though in earlier dealings, albeit below Tuesday session highs. US cash tsys are close to unchanged, reversing an early cheapening impetus.

- USD/JPY is tracking slightly lower, last in 140.05/10 region. EUR/USD is back to 1.0790, with gains above 1.0800 unable to be sustained.

- AUD/USD is at 0.6770/75, slightly above on NY closing levels from Tuesday. Better metals commodity price action helping to offset higher core yields.

- NZD/USD is outperforming at the margins, last in the 0.6155/60 region. Earlier data showed the current account balance for Q1, slightly better than expected (-8.5% of GDP, -9.0% expected). Food prices rose 0.3% in May, versus 0.5% in Apr.

- The data calendar remains light for the rest of the Asia Pac session, with focus likely to firmly rest on the upcoming Fed decision later in the US.

OIL: Prices Hold Onto Gains As Wait For Fed Announcement

Oil prices are in a holding pattern ahead of the Fed decision later. They have maintained gains driven by monetary stimulus in China and US plans to refill the SPR. WTI is remaining below $70 and is flat on the day at $69.45/bbl, close to the intraday high, and Brent has traded below $75 but is up 0.2% to $74.42.

- OPEC estimated in its monthly report on Tuesday that there will a crude shortfall of about 2.7mbd in July following Saudi Arabia’s announcement to cut output by a further 1mbd and based on a forecasted increase in global demand. Saudi Arabia is yet to say whether the move will be extended beyond July. The International Energy Agency’s monthly report is also released later. Previously it also expected the market to be in deficit in H2 2023. So, far these projections have done little to boost oil prices.

- Bloomberg reported that API recorded crude inventories rose 1.02mn barrels last week after a 1.7mn drawdown the previous week, according to people familiar with the data. Gasoline stocks rose 2.075mn and distillate +1.39mn. The official EIA data is published today.

- Later the Fed decision is announced and it is expected to keep rates on hold (see MNI’s Fed Preview here). An unexpected hike would likely drive oil prices sharply lower on US recession fears. There is also US PPI data for May, UK April IP/GDP and euro area IP.

GOLD: Bullion Up Moderately As Waits For Fed Decision

Gold prices finished Tuesday down 0.7% to $1943.72/oz on higher US Treasury yields. Yields fell following the close-to-expected US CPI data but then rose sharply, which weighed on bullion whereas the USD was down. Ahead of the Fed decision later, gold is up 0.3% to $1949.42/oz and the USD has traded sideways.

- Today gold reached an intraday low of $1942.26 followed by a high of $1949.47. Support lies at $1932.20, the May 31 low.

- Later the Fed decision is announced and it is expected to keep rates on hold (see MNI’s Fed Preview here), which should be supportive of gold. If it unexpectedly hikes, then gold prices are likely to fall sharply as yields rise. There is also US PPI data for May, which is forecast to moderate further.

CHINA DATA: 1yr MLF Expected To Be Cut Tomorrow, May Activity Data To Weaken

A reminder that tomorrow delivers the 1yr MLF decision, with 2.65% forecast, a -10bps move lower, with consensus having shifted since the start of the week post yesterday's reverse repo and SLF cuts. In terms of MLF volumes, the consensus is at 212.5bn yuan, versus 125bn prior.

- Also out tomorrow is the May activity data. Expectations mostly sit to the downside relative to Apr outcomes. Any downside surprises may impact China related asset sentiment less though, given this week's rate cuts and renewed talk of stimulus. Conversely upside surprises may help somewhat of a relief rally, given disappointing outcomes in recent months and lowered China growth expectations.

- For IP, the market forecast is 3.5% y/y, prior 5.6% (forecast range 1.2% - 9.4%).

- For retail sales, the market forecast is 13.7% y/y, prior 18.4% (forecast range 10.0% - 19.5%).

- For fixed asset investment, the market forecast is 4.4% ytd y/y, prior was 4.7%, while property investment is expected to remain depressed at -6.7% ytd y/y (prior -6.2%).

- The jobless rate is forecast at 5.2%, unchanged from Apr.

- New home prices for May will also print, there is no consensus but the prior month was +0.32%.

ASIA FX: CNH Steady, USD/KRW Rebounds

USD/Asia pairs are mostly pushing higher today, even with USD/CNH remaining relatively steady. The rebound in USD/KRW has been noticeable, while USD gains elsewhere have been more modest. The INR has outperformed at the margins. Still to come is Indian wholesale inflation, while tomorrow the main focus will be on China's 1yr MLF (a cut is expected) and May activity data. The Taiwan central bank also meets, with rates expected to be held steady.

- USD/CNH has been relatively steady, unable to spend much time sub 7.1700, while finding selling interest closer to 7.1800. Onshore equities are firmer, while China Foreign Minister Qin and US Secretary of State Blinken spoke earlier today via phone. During the discussion Qin said that the US should stop interfering in China’s internal affairs, which is not unusual. But he also said that the US should respect issues which are important to China, such as Taiwan, and should stop hurting China by using competition as an excuse. Blinken is scheduled to travel to travel this Sunday.

- 1 month USD/KRW has bounced strongly from recent lows, last tracking in the 1277/78 region, after closing Tuesday in NY at ~1265. Onshore equities are weaker, -0.70% for the Kospi, -2.5% for the Kosdaq. These moves look to be unwinding recent outperformance rather than fundamentally driven. 1280 may a near term upside target for the 1 month NDF. Earlier the unemployment rate ticked down to 2.5%, better than expected, and supporting the BoK's hawkish stance at the margins.

- USD/INR has opened dealing ~0.1% softer today, last printing at 82.25/30. Bears look to target low from May 4 at 81.6563. Bulls look to target a break of the 83 handle, the last test of 83 saw the RBI intervene in the FX market. RBI's Das noted yesterday that the disinflation process is likely to be slow and protracted. Also noting that the bank may meet its 4% target only in the medium term. More here. On the wires today we have May Wholesale Prices, a fall of 2.50% Y/Y is expected.

- The SGD NEER (per Goldman Sachs estimates) has firmed in the wake of yesterday's US CPI report printing a fresh cycle high before moderating gains. We now sit ~0.5% below the upper end of the band. USD/SGD has had a muted start to today's session, narrows have been narrow and SGD is a touch firmer. Today's FOMC meeting provides the next risk event for the pair. The Fed is expected to hold rates, however attention will be on any forward guidance that the bank provides.

- The Ringgit has pared Tuesday's gains in early dealing, USD/MYR prints at 4.6180/6220 up ~0.2% from closing levels. Broader greenback trends continue to dominate flows in recent sessions however ranges do remain relatively narrow as the pair consolidates above 4.60. Palm Oil futures are at their highest level since 30 May and now sit ~9% above cycle lows seen in early June. Stronger soybean prices and the risk of an El Nino weather pattern on production have offset concerns about growing supply. A reminder that the domestic data calendar is empty for the remainder of the week.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Flag | Country | Event |

| 14/06/2023 | 0600/0700 | ** |  | UK | UK Monthly GDP |

| 14/06/2023 | 0600/0700 | *** | | UK | Index of Production |

| 14/06/2023 | 0600/0700 | ** | | UK | Index of Services |

| 14/06/2023 | 0600/0700 | ** | | UK | Trade Balance |

| 14/06/2023 | 0600/0700 | ** | | UK | Output in the Construction Industry |

| 14/06/2023 | 0600/0800 | *** |  | SE | Inflation Report |

| 14/06/2023 | 0900/1100 | ** |  | EU | Industrial Production |

| 14/06/2023 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 14/06/2023 | 1230/0830 | * |  | CA | Household debt-to-income |

| 14/06/2023 | 1230/0830 | *** | | US | PPI |

| 14/06/2023 | 1430/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 14/06/2023 | 1800/1400 | *** | | US | FOMC Statement |

| 15/06/2023 | 2245/1045 | *** |  | NZ | GDP |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.