- Firmer than expected Eurozone core CPI & GDP data weigh on EGBs, support EUR.

- Estimates from BoJ data start to quantify Monday's potential JPY intervention.

- US Q1 ECI, February house prices, April MNI Chicago PMI and consumer confidence all print ahead of Wednesday’s Fed decision and Friday’s employment report. Canadian GDP for February is also scheduled.

MNI Fed Preview - May 2024: Disinflation Delayed, Not Yet Denied

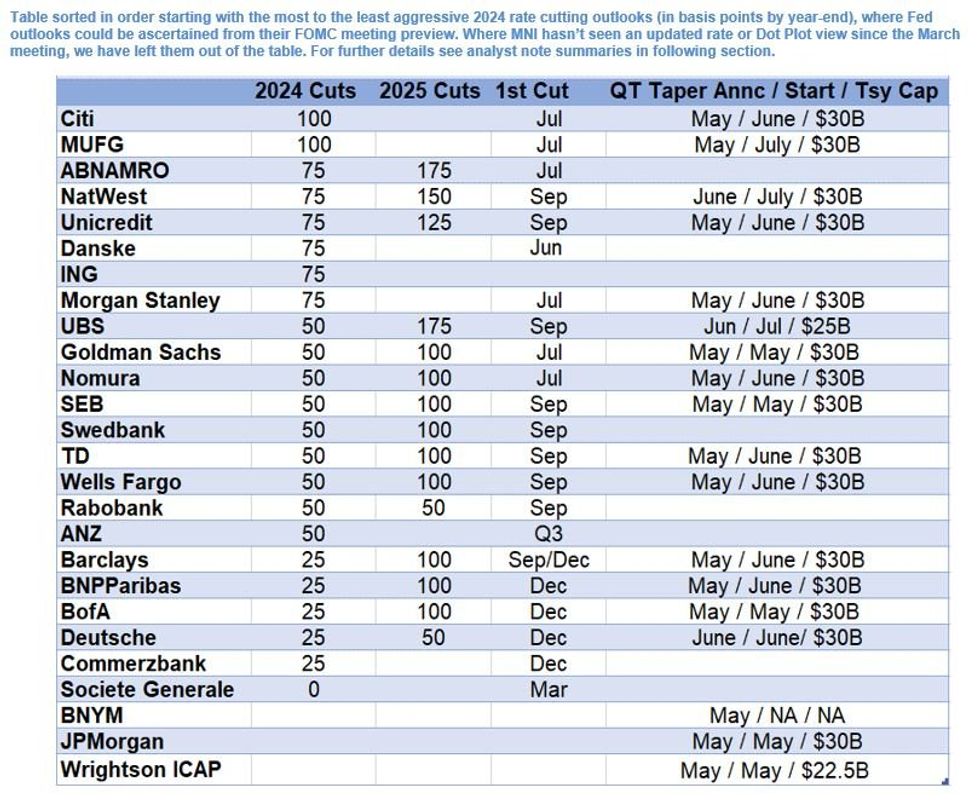

Analysts generally look for a more hawkish message from the FOMC in May compared with March, in light of strong inflation and economic activity data.

- None expect the Statement forward guidance to be changed, though a few see potential for tweaks. Several eye risks of the characterization of inflation to be changed in a hawkish fashion.

- Generally, Powell is expected to tilt more cautious on the inflation outlook than in previous appearances, with potential flashpoints for markets including whether he acknowledges that 3 cuts are less likely to be the base case for the FOMC in 2024, and/or whether June is too early for the first cut.

- On tapering QT, consensus is clearly for an announcement at this meeting, with Treasury runoff capped at $30B (vs $60B currently) starting in June. Some see caps set slightly lower ($22.5-25B).

- Only one analyst (Danske) whose preview we read still sees a cut as early as June. Consensus for the first cut is clustered around Jul/Sep, though at least one (SocGen) sees the first only in 2025.

- A plurality of analysts see 50bp of cuts in 2024, with 100bp in 2025, though the range is somewhere from 75bp to 250bp cumulatively to end-2025 (incorporating analysts who provided forecasts for both years).

- FULL PUBLICATION PDF HERE

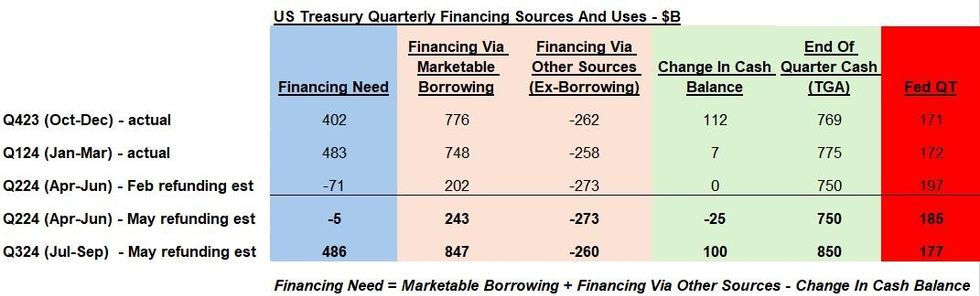

US TSYS: Q3 Financing Needs Above-Expected, But QT Taper Should Offset

The quarterly refunding process began on April 29 with Treasury’s release of its latest financing requirement estimates. As broadly expected, Treasury increased the anticipated amount of borrowing from private markets for Apr-Jun (calendar Q2, to $243B from the $202B estimated in the February refunding round, and vs the roughly $220B MNI consensus), though its Jul-Sep (calendar Q3) borrowing estimate was on the very high side of expectations at $847B (MNI consensus looked for something in the neighborhood of $700B, with some estimates well below $600B).

- Looking at the details, for Q2, the higher estimate vs expectations looks due in part to slightly disappointing tax revenues at the end of April (“largely due to lower cash receipts”) leading to $66B more financing required, offset partially by a $25B higher cash balance to start the quarter, though the overall difference vs expectations is marginal.

- For Q3, the main reason for the upside surprise was the higher end-of-quarter cash pile of $850B, which all else equal implies an additional $100B in required funding.

- The overall implication is that bill issuance will be higher in Q3 than most had expected in order to build the cash pile up by end-September. Unanimous expectation is that coupon auction sizes will not be changed for the upcoming quarter.

- Of course, Fed QT is another consideration: the Treasury assumes in its estimates that SOMA runoff will continue at $60B a month through September, but the FOMC is widely expected to announce on Wednesday that it will immediately lower the caps on redemptions from $60B to $30B (more in MNI’s May FOMC Preview).

- That would mean $90B less financing per quarter that the Treasury would be required to raise, effectively offsetting (and partially accounting for) the $100B upside surprise to the Q3 estimate.

- MNI's full refunding preview will be out later today.

Source: US Treasury, MNI

Source: US Treasury, MNI

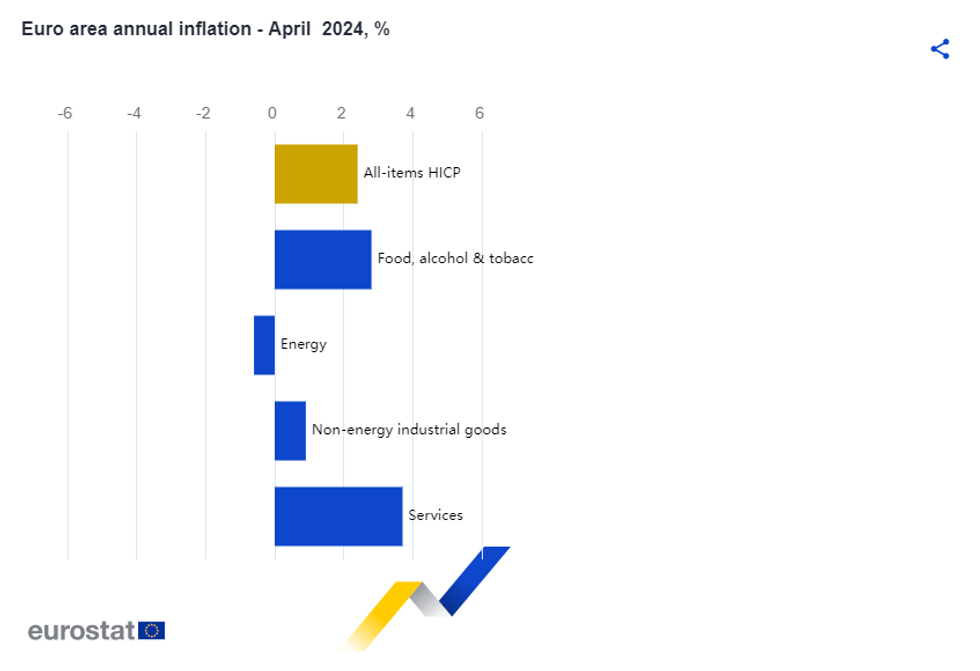

EUROZONE DATA: Services Inflation Breaks Lower, Core Slightly Higher Than Expected

Eurozone April flash headline printed in line with consensus while core inflation came in a touch above on a rounded basis, in line with MNI's tracking based on the national data released earlier today and yesterday.

- Headline HICP was 2.4% Y/Y (vs 2.3/2.4% cons; 2.4% prior) and 0.6% M/M (vs 0.6% cons; 0.8% prior). On an unrounded basis, headline was 2.38% Y/Y and 0.59% M/M.

- Core HICP came in a touch higher than expected at 2.7% Y/Y (vs 2.6% cons; 2.9% prior). This is a marginally bigger surprise than the headline number, given Spain Core CPI surprised to the downside, suggesting some of the countries not having reported an April core figure yet (such as France) might have printed relatively strongly. On an unrounded basis, core was 2.67% Y/Y and 0.71% M/M.

- Looking at the individual categories, services inflation finally broke lower in April, coming in at 3.7% Y/Y after 5 consecutive prints at 4.0%. Non-energy industrial goods saw its longer-term disinflation trend continuing and printed at 0.9% Y/Y (vs 1.1% prior), while energy prices saw their expected uptick materialize at -0.6% Y/Y (vs -1.8% prior).

- At a country level, annual HICP fell in 13 countries, and was the same or higher in the remaining 7.

MNI, Eurostat

MNI, Eurostat

CHINA: Politburo Highlights Potential For Monetary Easing And Further Support For Housing

The initial round of post-meeting comments from April’s Politburo covered well-known risks and policy focus areas. There was a continued focus on reform, economic challenges, the need to extinguish debt-linked risks and support for demand.

- The Politburo also highlighted the potential for both policy rate & RRR cuts going forwards. Most China watchers already looked for further monetary easing during ’24, but the comments may deepen/front load expectations for looser monetary policy in Q2.

- The Politburo then went on to stress the need to expedite ultra-long bond issuance and the use of special bonds.

- The readout then flagged that China will study steps to digest the existing housing stockpile. This was probably the most interesting part of the release, with the property overhang continuing to hamper the embattled sector.

- A reminder that recent days have seen increased speculation re: deeper property sector support, this adds credence/momentum to those ides.

- CGBs yields softened on those headlines, as the potential for deeper policy support (housing and monetary) and focus on lower broader funding costs dominated, even with the Politburo wanting to expedite special bond issuance.

- Equities of Hong Kong listed developers rallied on the headline.

- When it came to broader policy settings, the Politburo reiterated the need for fiscal policy to remain “proactive” and monetary policy to remain “prudent,” although the descriptions surrounding the policy levers were seemingly shortened.

- Some of the wording surrounding fiscal policy pointed to the potential for greater support on that front.

- A reminder that Chinese local markets are closed Wednesday through Friday owing to the observance of a public holiday.

US TSYS: Bear Steeper Ahead Of ECI, MNI Chicago PMI To Offer Mfg Clues

Treasuries have reversed overnight gains to see yields climb slightly on the day, up between 0.5-2bps and bear steepening with 2s10s at -34.5bps (+1.5bp).

- European matters again help set the tone, with Treasuries outperforming after higher-than-expected French flash inflation data and stronger-than-expected Q1 GDP prints from the four largest EZ economies.

- TYM4 has touch fresh session lows of 107-25 (- 05+), pulling back towards the middle of yesterday’s range on reasonable volumes just north of 300k.

- Resistance is seen at 108-14 (20-day EMA) but the trend needle points south with support at 107-04 (Apr 25 low).

- Today’s focus is on the Q1 Employment Cost Index but the MNI Chicago PMI also offers a useful update ahead of tomorrow’s ISM mfg print after regional Fed and PMI surveys have moved in opposite directions in April. The Conference Board’s labor differential will also be watched ahead of Friday’s payrolls report.

- Data: ECI Q1 (0830ET), FHFA and S&P CoreLogic house prices Feb (0900ET), MNI Chicago PMI Apr (0945ET), Conf Board consumer survey Apr (1000ET) and Dallas Fed services Apr (1030ET)

- Bill issuance: US Tsy $65B 42 Day CMB auction (1130ET)

US TSY FUTURES: OI Points To Mix Of Modest Long Setting & Short Cover On Monday

Yesterday’s uptick in Tsy futures and preliminary OI data point to modest net long setting in some contracts (TU, TY, UXY & WN) and limited net short cover in others (FV & US). The former provided the dominant positioning factor on the curve, but the net swing was contained.

- The positioning move came in the wake of Friday’s notable short covering.

- Spill overs from EGBs and block flow aided Monday’s rally, although Tsy futures volume was relatively subdued.

| 29-Apr-24 | 26-Apr-24 | Daily OI Change | OI DV01 Equivalent Change ($) | |

| TU | 4,086,320 | 4,080,930 | +5,390 | +194,067 |

| FV | 5,998,883 | 6,005,531 | -6,648 | -272,012 |

| TY | 4,452,623 | 4,432,980 | +19,643 | +1,238,630 |

| UXY | 2,067,489 | 2,056,607 | +10,882 | +923,209 |

| US | 1,558,797 | 1,561,927 | -3,130 | -390,617 |

| WN | 1,634,111 | 1,630,442 | +3,669 | +699,521 |

| Total | +29,806 | +2,392,797 |

STIR: Fed Rate Path Unchanged With ECI Eyed

Fed Funds implied rates are unchanged on Monday’s close with the Dec’24 holding within 2bps of highs seen after last week’s core PCE upside surprise for Q1.

- Cumulative cuts from 5.33% effective: 0.5bp May, 3.5bp Jun, 8.5bp Jul, 18bp Sep, 24bp Nov and 35bp Dec.

- Further Q1 data is in focus today, with the Employment Cost Index giving a more comprehensive look at wage pressures ahead of Friday’s AHE update for April.

STIR: OI Suggests Long Setting In SOFR Whites & Reds Dominated On Monday

The combination of yesterday’s twist flattening of the SOFR futures strip and preliminary OI data points to the following net positioning swings on Monday.

- Whites: Net long cover in SFRH4 & M4 and net long setting in SFRZ4. Positioning movement in SFRU4 is clouded by the contract’s unchanged priced status come settlement, but we would point to net long setting in that contract if we had to guess.

- Reds: Net long setting was seemingly seen in all contracts.

- Greens & Blues: Rounds of net long setting and net short cover generally offset when it came to net pack OI movement.

- Year-end FOMC-dated OIS was little changed on the day, showing about 35bp of cuts.

| 29-Apr-24 | 26-Apr-24 | Daily OI Change | Daily OI Change In Packs | ||

| SFRH4 | 923,634 | 926,962 | -3,328 | Whites | +36,390 |

| SFRM4 | 1,126,999 | 1,128,558 | -1,559 | Reds | +34,263 |

| SFRU4 | 1,009,447 | 995,928 | +13,519 | Greens | +1,336 |

| SFRZ4 | 1,215,432 | 1,187,674 | +27,758 | Blues | -378 |

| SFRH5 | 744,876 | 735,594 | +9,282 | ||

| SFRM5 | 823,018 | 821,363 | +1,655 | ||

| SFRU5 | 719,707 | 710,885 | +8,822 | ||

| SFRZ5 | 814,424 | 799,920 | +14,504 | ||

| SFRH6 | 484,408 | 484,771 | -363 | ||

| SFRM6 | 515,947 | 514,855 | +1,092 | ||

| SFRU6 | 391,316 | 384,682 | +6,634 | ||

| SFRZ6 | 345,030 | 351,057 | -6,027 | ||

| SFRH7 | 234,463 | 228,693 | +5,770 | ||

| SFRM7 | 183,159 | 184,399 | -1,240 | ||

| SFRU7 | 165,159 | 167,486 | -2,327 | ||

| SFRZ7 | 140,130 | 142,711 | -2,581 |

EUROPEAN ISSUANCE UPDATE

DSL auction results

- E2.5bln of the 2.50% Jul-34 DSL. Avg yield 2.828%.

Green Bobl auction results

- There was strong demand for the new Green Bobl launch with bids of E5.158bln the second highest ever for a Green Bobl / Bund with only the inaugural Green Bobl auction in November 2020 saw a higher volume of bids (syndications have of course seen larger books than E5.158bln but they are not directly comparable).

- The bid-to-cover was a bit lower than in the last couple of Green Bobl auctions - but only due to the larger volume issued today (E3bln).

- So overall a very successful launch today.

- E3bln (E2.723bln allotted) of the 2.10% Apr-29 Green Bobl. Avg yield 2.55% (bid-to-offer 1.72x; bid-to-cover 1.89x).

Gilt auction results

- A wider tail and a lower bid-to-cover than the previous 5-year gilt auction (at the launch of the new 4.125% Jul-29 gilt). However, as we noted in the preview, we had been looking for a wider tail than previously and a fall in the bid-to-cover is also not surprising given that we saw the more normal size of GBP4.0bln sold today (whereas in March GBP3bln was sold so the DMO didn't overshoot its funding target too much at the end of the fiscal year).

- So on paper, the auction looks weaker than previously, but taking into account that this is a new issue and the regular auction size, it is stronger than it appears at first look.

- GBP4bln of the 4.125% Jul-29 Gilt*. Avg yield 4.251% (bid-to-cover 3.21x, tail 0.8bp).

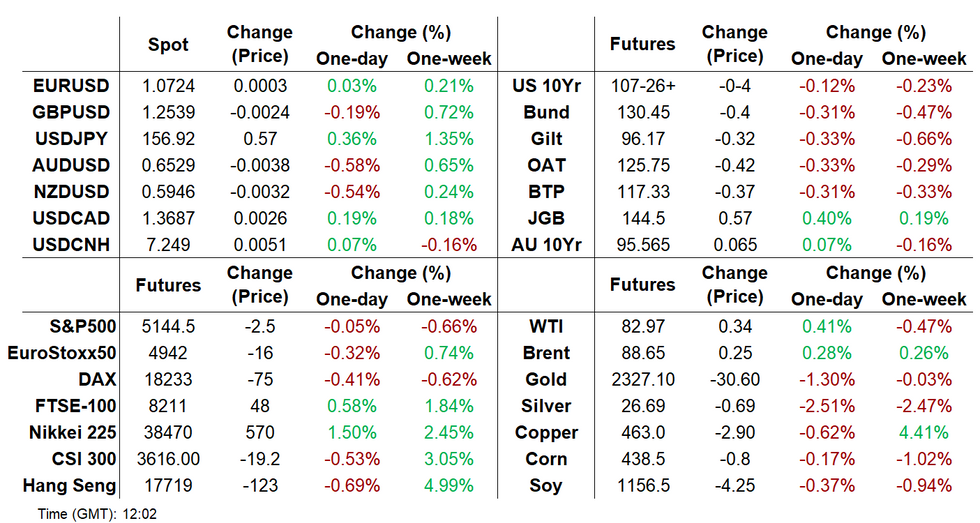

FOREX: Antipodean FX Relinquish Monday Gains, US Data Awaited

EURUSD has had a brief bout of strength to session highs following the broadly in line Eurozone CPI data. The pair printed up to 1.0735, however, momentum has been subdued as we break above a narrow overnight range.

- Solid gains for the USD index overnight have been eroded in early European trade, although the DXY remains 0.10% in the green as we approach the NY crossover.

- USDJPY has climbed, but has yet to reclaim the 157.00 level. We were last near 156.90, around 0.35% weaker in yen terms. The market is testing the waters post yesterday's strong rebound amid intervention speculation. Earlier comments from Chief FX Diplomat Kanda reiterated the authorities are ready to deal with FX at any time of the day. Mixed Japan data outcomes didn't shift FX sentiment.

- Weaker-than-expected data overnight has weighed on both the Australian dollar and Kiwi, placing a temporary halt to the bullish developing sentiment for AUDUSD. However, the current bullish phase for the pair remains intact despite today’s pullback. Furthermore, signs of expedited easing and bond issuance in the latest Politburo report should be AUD supportive at the margin.

- Overall, resistance at 0.6528, the 50-day EMA, has been breached and the clear break highlights a stronger reversal that signals scope for a climb towards 0.6644, the Apr 9 high. Initial support comes in at 0.6441.

- Later US Q1 ECI, February house prices, April MNI Chicago PMI and consumer confidence all print ahead of Wednesday’s Fed decision and Friday’s employment report. Canadian GDP for February is also scheduled on Tuesday.

JPY: Timeline Update for Further Information on Suspected Intervention

Headlines this morning from Bloomberg have been related to the BOJ’s release of projected "Sources of Changes in Current Account Balances at the Bank of Japan and Market Operations" for May 1 when FX transactions on Apr 29 settle. Link here: https://www3.boj.or.jp/market/en/stat/jx240430.htm

- BofA point out that the "treasury funds and others category" shows the change in financial institutions' account balance due to transactions with the government. Some money market brokers have projections for other factors that may affect this data so the market then estimates the potential size of intervention.

- Going forward, typically on the 5th business day of month (May 09) - the MoF will then disclose the composition of its official reserves for end-April. BofA say that assuming the MoF financed intervention by deposits ($155bn as of end-Mar) and securities ($995bn), the updated balances could also tell the rough size of FX interventions. They estimate that the valuation change and carry on the deposits and securities would add up to a decline of $14-16bn (due to higher rates) for the month of April.

- May 31 – official MoF publication of the monthly size of interventions for the Apr 26-May 29 period.

FOREX OPTIONS: Expiries for Apr30 NY cut 1000ET (Source DTCC)

- EURUSD: 1.0650 (563mln), 1.0685 (210mln), 1.0700 (582mln), 1.0750 (687mln), 1.0775 (309mln)

- USDJPY: 157.00 (325mln)

- AUDNZD: 1.0950 (422mln)

- USDCNY: 7.2200 (499mln), 7.2400 (272mln), 7.2600 (1.09bn)

EQUITIES: S&P E-Minis Tests Resistance At The 20-Day EMA

The short-term trend condition in S&P E-Minis remains bearish and the latest recovery appears to be a correction. A resumption of the bear leg would open 4907.57, 50.0% of the Oct 27 ‘23 - Apr 1 bull leg. Firm resistance at 5139.03, the 20-day EMA, has been pierced, a clear break would instead signal a reversal and expose key resistance at 5333.50, the Apr 1 high.

- EUROSTOXX 50 futures are holding on to their recent gains from 4762.00, the Apr 19 low. The contract has breached the 20-day EMA and resistance at 4990.00, the Apr 15 high. This continues to highlight a potentially stronger reversal and the end of the correction between Apr 2 - 19. An extension higher would expose the bull trigger at 5079.00, the Apr 2 high. Initial support to watch is 4877.40, the 50-day EMA.

COMMODITIES: Gold Bear Cycle Remains In Play

Gold remains in consolidation mode and is trading closer to its recent lows. The precious metal is testing the 20-day EMA and this highlights the start of a possible corrective cycle. A continuation lower would signal scope for an extension towards $2237.6, the 50-day EMA. Note that a short-term bear cycle would allow a significant overbought condition to unwind. Key resistance and the bull trigger is at $2431.5, the recent Apr 12 high.

- In the oil space, WTI futures are trading lower but for now remain above key short-term support at $81.20, the 50-day EMA. The recent move down between Apr 12 - 22, highlights a corrective phase and a clear break of the 50-day average would signal scope for a deeper retracement towards $76.07, the Mar 11 low. On the upside, key resistance and the bull trigger has been defined at $86.97, the Apr 12 high. A breach of this level would resume the uptrend.

| Date | GMT/Local | Impact | Flag | Country | Event |

| 30/04/2024 | 1230/0830 | *** |  | US | Employment Cost Index |

| 30/04/2024 | 1230/0830 | *** |  | CA | Gross Domestic Product by Industry |

| 30/04/2024 | 1255/0855 | ** | | US | Redbook Retail Sales Index |

| 30/04/2024 | 1300/0900 | ** | | US | S&P Case-Shiller Home Price Index |

| 30/04/2024 | 1300/0900 | ** | | US | FHFA Home Price Index |

| 30/04/2024 | 1300/0900 | ** | | US | FHFA Home Price Index |

| 30/04/2024 | 1345/0945 | *** | | US | MNI Chicago PMI |

| 30/04/2024 | 1400/1000 | *** | | US | Conference Board Consumer Confidence |

| 30/04/2024 | 1400/1000 | ** | | US | housing vacancies |

| 30/04/2024 | 1430/1030 | ** | | US | Dallas Fed Services Survey |

| 30/04/2024 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 01/05/2024 | 2245/1045 | *** |  | NZ | Quarterly Labor market data |

| 01/05/2024 | 2300/0900 | ** |  | AU | IHS Markit Manufacturing PMI (f) |

| 01/05/2024 | 0030/0930 | ** |  | JP | IHS Markit Final Japan Manufacturing PMI |

| 01/05/2024 | 0830/0930 | ** |  | UK | S&P Global Manufacturing PMI (Final) |

| 01/05/2024 | 0900/1000 | ** | | UK | Gilt Outright Auction Result |

| 01/05/2024 | 1100/0700 | ** | | US | MBA Weekly Applications Index |

| 01/05/2024 | - | *** | | US | Domestic-Made Vehicle Sales |

| 01/05/2024 | 1215/0815 | *** | | US | ADP Employment Report |

| 01/05/2024 | 1230/0830 | *** | | US | Treasury Quarterly Refunding |

| 01/05/2024 | 1345/0945 | *** | | US | IHS Markit Manufacturing Index (final) |

| 01/05/2024 | 1400/1000 | *** | | US | ISM Manufacturing Index |

| 01/05/2024 | 1400/1000 | * | | US | Construction Spending |

| 01/05/2024 | 1400/1000 | *** | | US | JOLTS jobs opening level |

| 01/05/2024 | 1400/1000 | *** | | US | JOLTS quits Rate |

| 01/05/2024 | 1430/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 01/05/2024 | 1800/1400 | *** | | US | FOMC Statement |

| 01/05/2024 | 2015/1615 | | CA | BOC Governor at Senate Banking Committee |